Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

Originally published by Jigar Shah, Senior Advisor and Podcaster, Accelerating Climate Wealth, October 10, 2025

When companies want to build large energy projects like solar farms, wind farms, or natural gas plants, they need to understand a few key things: how much money they can make from selling the electricity, and how to finance the project. To figure this out, they use special software and expert analysis to predict how much power they'll produce, how much they’ll earn, and what their costs and risks will be. Investors won’t fund these projects unless they’re confident in these forecasts.

But the energy grid is changing quickly. In the past, models used to predict energy markets were based mainly on traditional factors like fuel costs. Now, with more renewable energy sources like solar and wind, the way prices are set and how the market operates have shifted. If we rely on old models that don’t account for these changes, we might get inaccurate answers, which can lead to overestimating the value of a project or missing opportunities altogether. If you only see a portion of the picture in front of you, your answers are limited by your constrained vision, a concept called model-limited choice.

In areas where there’s a lot of wind and solar power, like the parts west of the Mississippi River, old models for predicting energy markets can give a misleading picture. When renewable energy sources produce more power than the grid needs—especially during times when electricity demand is low—this excess energy is often cut back or "curtailed." This means the energy doesn’t get used, and prices can even go negative.

In the first half of 2025, for example, over 2,300 gigawatt-hours of solar energy and more than 3,700 gigawatt-hours of wind energy were cut back because the market didn’t need the power. While older models do try to simulate these situations, they don’t fully capture how uncertain renewable supply and market bidding strategies impact prices. Even the most detailed models used for planning, like those predicting day-to-day market operations, have underestimated the amount of curtailment by almost double this year. This means projects relying only on legacy models might overvalue renewable energy opportunities or misjudge revenue potential in these regions.

As power markets evolve, and as renewables make up increasingly larger portions of supply stacks in markets across the world, projects must be modeled differently to get financed and built.

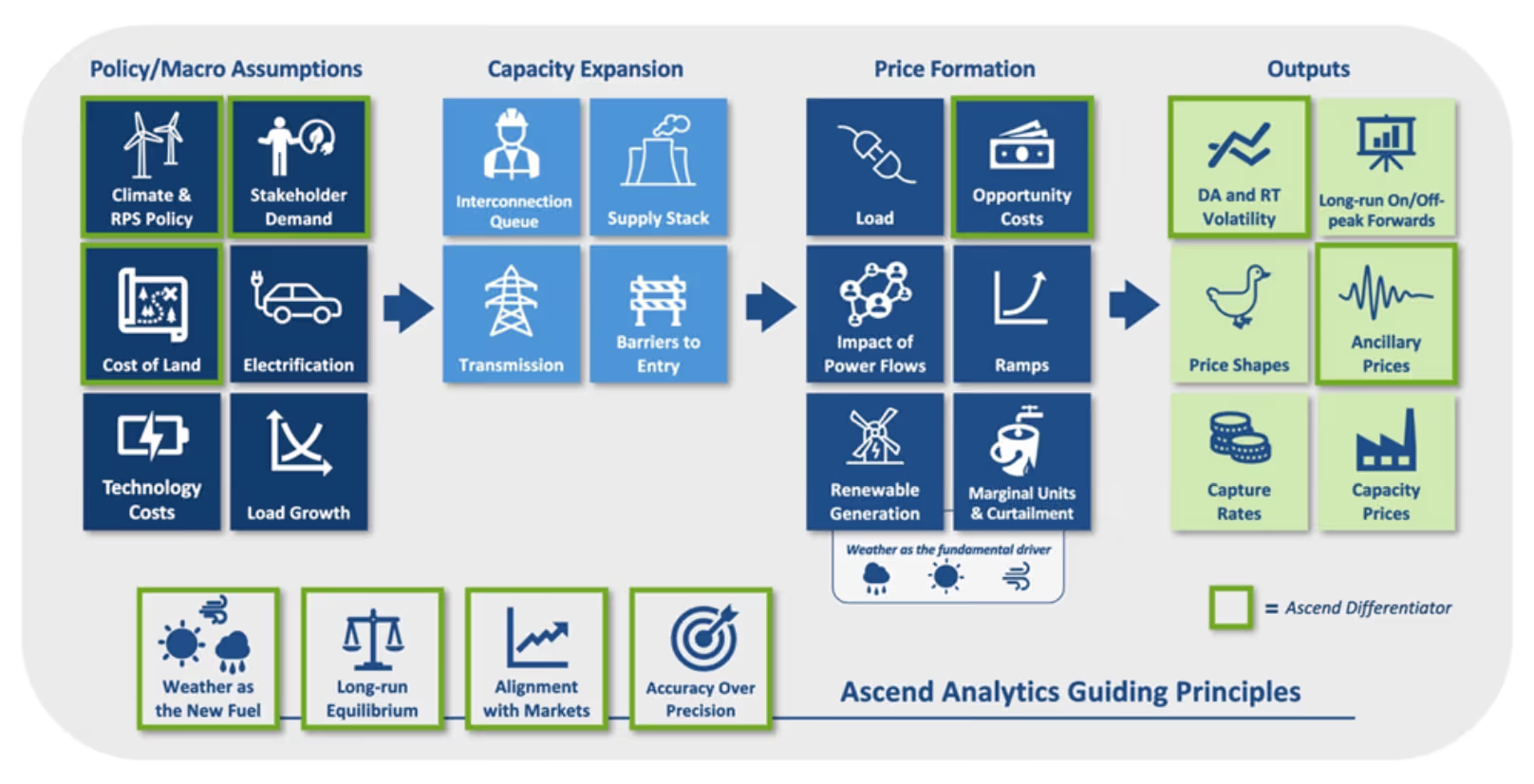

One company, Ascend Analytics, calls this an Opportunity Cost Forecasting Framework, and it incorporates some fundamental differences versus legacy models:

Weather is the new fuel – The weather influences not just how much people use electricity but also how much renewable energy is generated. This makes energy prices more unpredictable and more closely tied to weather conditions.

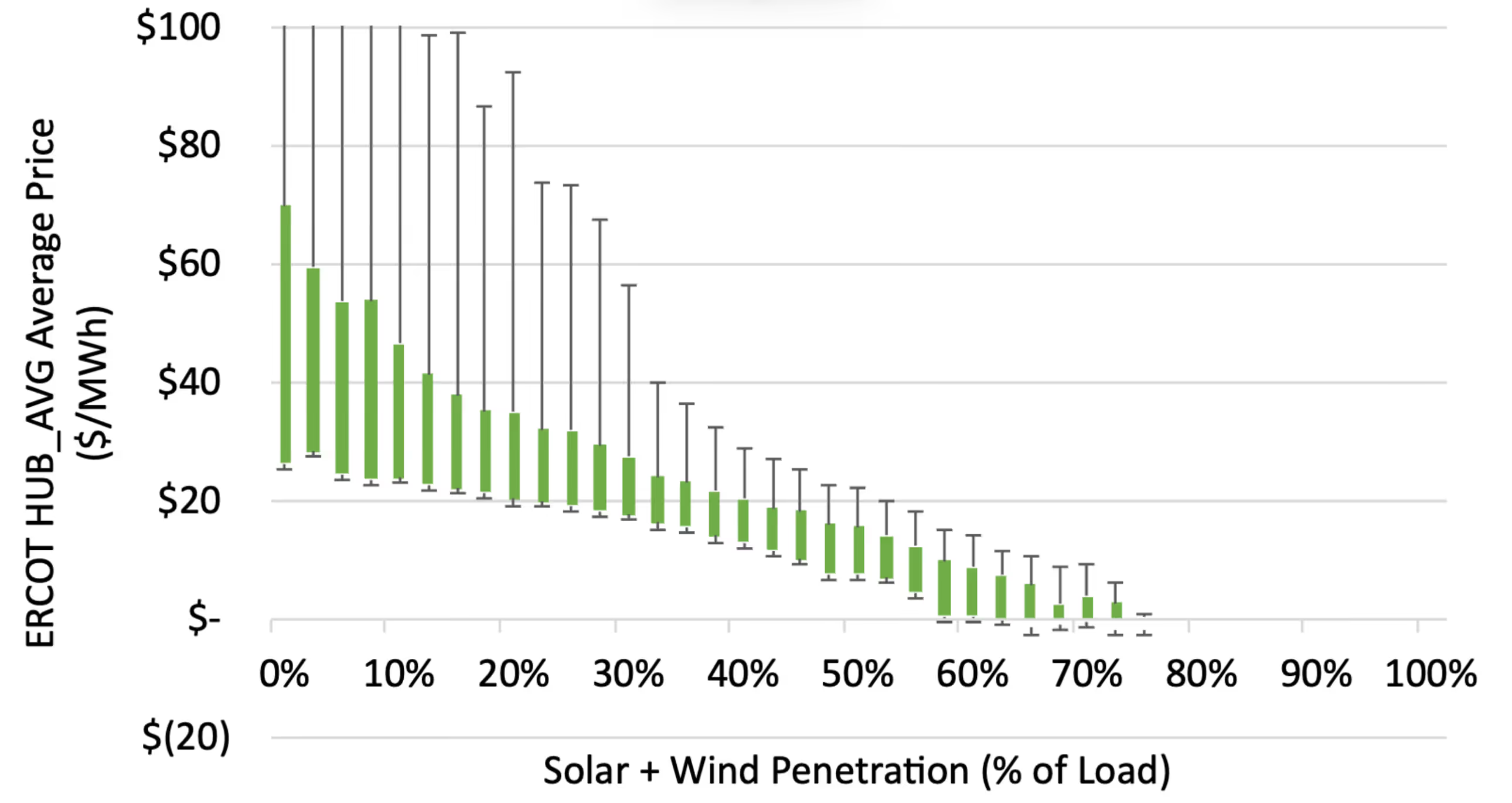

As renewable penetration increases, energy prices decline, as shown in Figure 2. In markets like California (CAISO) or Texas (ERCOT), renewables and storage already set prices in energy, capacity, and ancillary markets. This dynamic is increasingly becoming apparent in other US markets as renewable penetration accelerates.

A modern framework captures the causal effects of weather as the new fuel that drives renewable generation, load, transmission congestion, outages, prices, opportunity costs, and capture rates, accounting for the impact of weather on both demand and supply. Additionally, the dynamics of renewables and storage create a price settlement framework based on opportunity cost, not traditional production costs.

Market prices don’t just cover costs – Today, prices reflect the opportunity costs of producing electricity, meaning they depend on what it costs to produce power and what else could be done with that energy. This creates more price ups and downs, including times when prices can go negative.

Legacy models forecast prices with an assumption that the market clearing price of electricity equals production costs. However, today’s market prices are a function of opportunity costs and can be thought of in the context of game theory, with participants setting prices to buy and sell power based on maximizing their individual outcome. They are acting in their own best interests as rational agents in the energy markets. Collectively, maximizing individual outcomes in this construct results in greater volatility, including negative prices for surplus conditions and price spikes for scarcity conditions. This disassociation of opportunity cost from product cost is a signature condition of today’s power markets, where renewables and storage make up a larger portion of the energy supply and increasingly become price setters.

Failing to intentionally model the structural elements of weather and opportunity cost bidding behaviour results in price forecasts that are inconsistent with the market, often under-valuing storage and over-valuing thermal generation and renewables (exclusive of environmental benefits), for example. For large irreversible energy infrastructure investments, stewarding capital based on the flawed framework of production cost models introduces biases and inconsistencies that hamper realized investor returns.

External policies and trends matter more – Government rules, regulations, and policies are constantly changing. Markets must adapt to these changes, which can impact renewable energy development and costs.

If there is one lesson to be learned over these last months, it’s that energy policy will change often, and sometimes significantly. Models that account for “status-quo policies” are assured one thing – they will be wrong.

Models have to be able to incorporate anticipated state- and federal-level clean energy policy evolution in base-case forecasts. We have also all watched as new federal policies work directly against renewable supply increases. And while corporate offtakers value speed-to-market first and foremost, they also continue to be willing to pay for renewable generation as they work to adhere to decarbonization commitments. These are all factors beyond what an economic model alone would predict.

Long-term balance is key – In competitive markets, if a project is very profitable, many will jump into it, which eventually pushes down prices and returns to more normal levels. Over time, the market tends to reach a balance.

As load growth surges in energy markets across the world and numerous project developers compete to provide supply to meet demand, rational investments will converge markets towards an equilibrium between the locational cost of new entry and locational project value. Premium locations cannot stay premium.

A medium-term exception is where technology and innovation provide a longer runway for premium returns, as renewables and storage costs continue to decline in cost over the medium- to long-term. These cost declines are a driving reason why, despite policy shifts, renewables continue to dominate new supply being added to the grid.

The energy grid is undergoing its greatest transformation since its inception 140 years ago, so it should not be surprising that how we model future generation should change fundamentally as well to avoid model-limited choices.

The opportunity cost modeling framework has been battle-tested and consistently demonstrates its soundness in forecasting market dynamics, including the evolution of price dynamics for ancillary services, long-run on and off-peak forwards, price shapes, capacity prices, and day-ahead and real-time price volatility. This credibility is critical as we face unprecedented load growth that urgently needs new supply to be modeled, financed, and built in this new power era.

Originally published by Jigar Shah, Senior Advisor and Podcaster, Accelerating Climate Wealth, October 10, 2025

When companies want to build large energy projects like solar farms, wind farms, or natural gas plants, they need to understand a few key things: how much money they can make from selling the electricity, and how to finance the project. To figure this out, they use special software and expert analysis to predict how much power they'll produce, how much they’ll earn, and what their costs and risks will be. Investors won’t fund these projects unless they’re confident in these forecasts.

But the energy grid is changing quickly. In the past, models used to predict energy markets were based mainly on traditional factors like fuel costs. Now, with more renewable energy sources like solar and wind, the way prices are set and how the market operates have shifted. If we rely on old models that don’t account for these changes, we might get inaccurate answers, which can lead to overestimating the value of a project or missing opportunities altogether. If you only see a portion of the picture in front of you, your answers are limited by your constrained vision, a concept called model-limited choice.

In areas where there’s a lot of wind and solar power, like the parts west of the Mississippi River, old models for predicting energy markets can give a misleading picture. When renewable energy sources produce more power than the grid needs—especially during times when electricity demand is low—this excess energy is often cut back or "curtailed." This means the energy doesn’t get used, and prices can even go negative.

In the first half of 2025, for example, over 2,300 gigawatt-hours of solar energy and more than 3,700 gigawatt-hours of wind energy were cut back because the market didn’t need the power. While older models do try to simulate these situations, they don’t fully capture how uncertain renewable supply and market bidding strategies impact prices. Even the most detailed models used for planning, like those predicting day-to-day market operations, have underestimated the amount of curtailment by almost double this year. This means projects relying only on legacy models might overvalue renewable energy opportunities or misjudge revenue potential in these regions.

As power markets evolve, and as renewables make up increasingly larger portions of supply stacks in markets across the world, projects must be modeled differently to get financed and built.

One company, Ascend Analytics, calls this an Opportunity Cost Forecasting Framework, and it incorporates some fundamental differences versus legacy models:

Weather is the new fuel – The weather influences not just how much people use electricity but also how much renewable energy is generated. This makes energy prices more unpredictable and more closely tied to weather conditions.

As renewable penetration increases, energy prices decline, as shown in Figure 2. In markets like California (CAISO) or Texas (ERCOT), renewables and storage already set prices in energy, capacity, and ancillary markets. This dynamic is increasingly becoming apparent in other US markets as renewable penetration accelerates.

A modern framework captures the causal effects of weather as the new fuel that drives renewable generation, load, transmission congestion, outages, prices, opportunity costs, and capture rates, accounting for the impact of weather on both demand and supply. Additionally, the dynamics of renewables and storage create a price settlement framework based on opportunity cost, not traditional production costs.

Market prices don’t just cover costs – Today, prices reflect the opportunity costs of producing electricity, meaning they depend on what it costs to produce power and what else could be done with that energy. This creates more price ups and downs, including times when prices can go negative.

Legacy models forecast prices with an assumption that the market clearing price of electricity equals production costs. However, today’s market prices are a function of opportunity costs and can be thought of in the context of game theory, with participants setting prices to buy and sell power based on maximizing their individual outcome. They are acting in their own best interests as rational agents in the energy markets. Collectively, maximizing individual outcomes in this construct results in greater volatility, including negative prices for surplus conditions and price spikes for scarcity conditions. This disassociation of opportunity cost from product cost is a signature condition of today’s power markets, where renewables and storage make up a larger portion of the energy supply and increasingly become price setters.

Failing to intentionally model the structural elements of weather and opportunity cost bidding behaviour results in price forecasts that are inconsistent with the market, often under-valuing storage and over-valuing thermal generation and renewables (exclusive of environmental benefits), for example. For large irreversible energy infrastructure investments, stewarding capital based on the flawed framework of production cost models introduces biases and inconsistencies that hamper realized investor returns.

External policies and trends matter more – Government rules, regulations, and policies are constantly changing. Markets must adapt to these changes, which can impact renewable energy development and costs.

If there is one lesson to be learned over these last months, it’s that energy policy will change often, and sometimes significantly. Models that account for “status-quo policies” are assured one thing – they will be wrong.

Models have to be able to incorporate anticipated state- and federal-level clean energy policy evolution in base-case forecasts. We have also all watched as new federal policies work directly against renewable supply increases. And while corporate offtakers value speed-to-market first and foremost, they also continue to be willing to pay for renewable generation as they work to adhere to decarbonization commitments. These are all factors beyond what an economic model alone would predict.

Long-term balance is key – In competitive markets, if a project is very profitable, many will jump into it, which eventually pushes down prices and returns to more normal levels. Over time, the market tends to reach a balance.

As load growth surges in energy markets across the world and numerous project developers compete to provide supply to meet demand, rational investments will converge markets towards an equilibrium between the locational cost of new entry and locational project value. Premium locations cannot stay premium.

A medium-term exception is where technology and innovation provide a longer runway for premium returns, as renewables and storage costs continue to decline in cost over the medium- to long-term. These cost declines are a driving reason why, despite policy shifts, renewables continue to dominate new supply being added to the grid.

The energy grid is undergoing its greatest transformation since its inception 140 years ago, so it should not be surprising that how we model future generation should change fundamentally as well to avoid model-limited choices.

The opportunity cost modeling framework has been battle-tested and consistently demonstrates its soundness in forecasting market dynamics, including the evolution of price dynamics for ancillary services, long-run on and off-peak forwards, price shapes, capacity prices, and day-ahead and real-time price volatility. This credibility is critical as we face unprecedented load growth that urgently needs new supply to be modeled, financed, and built in this new power era.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

.avif)

.png)

.avif)

.png)