Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

-1-ercot%20image.avif)

Scarcity events in ERCOT have persisted in recent years, and changing grid conditions could lead to an increase in both the severity and duration of these events. Growing population and load, increasing renewable capacity, the isolated nature of the ERCOT grid, and several extreme weather events have continued to test the system’s resilience. The continuation of these trends, coupled with the financial risks associated with building new gas generation beyond the limited quantity subsidized by the Texas Energy Fund, will increase reliability risks on the ERCOT grid.

Currently, critical system conditions are usually constrained to a few hours each year and are typically associated with sunset hours on particularly hot days. In the near term, short-duration batteries are well poised to generate during these brief periods of limited supply and high demand when prices reach their peak. However, as critical conditions stretch into longer peak periods and winter overnights, storage durations will need to increase to ensure grid reliability. These changing conditions in the context of ERCOT’s energy-only market structure bring into question the financial viability of longer-duration storage and other dispatchable assets that operate during infrequent extreme conditions. Evolving grid conditions and new market structures in ERCOT will need to incentivize the buildout of flexible resources that can address reliability risks that are growing in duration and frequency.

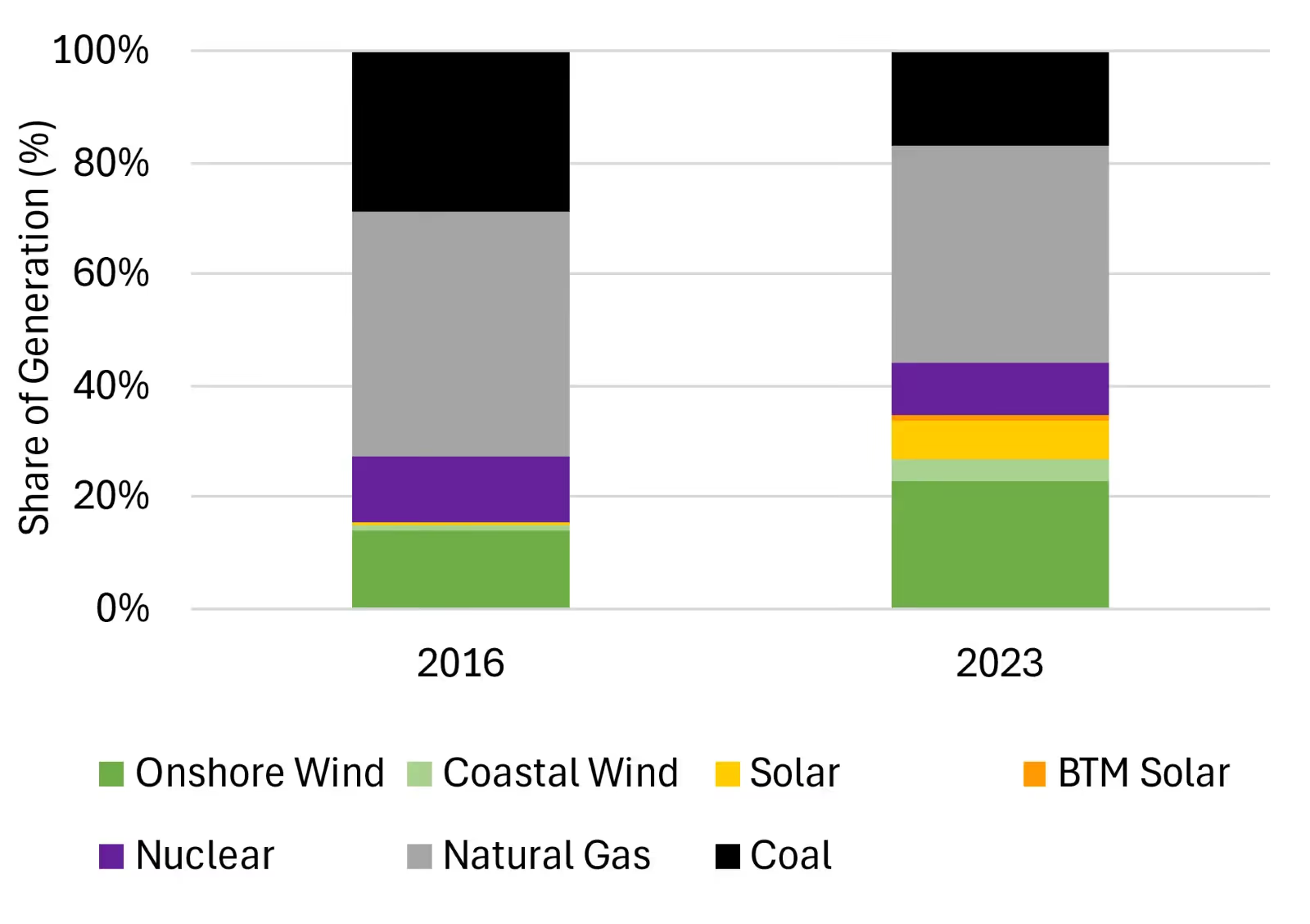

Texas produces the most renewable energy of any state in the country, and the share of the state’s electricity coming from renewables has increased significantly in the past several years (Figure 1). Solar capacity alone increased from less than one gigawatt in 2016 to over 32 GW in 2024. During hot summer days, solar generation during daylight hours supplies a significant and growing portion of the system's load when cooling demand is highest. Wind generation usually picks up after sunset, which helps offset the evening sundown ramp.

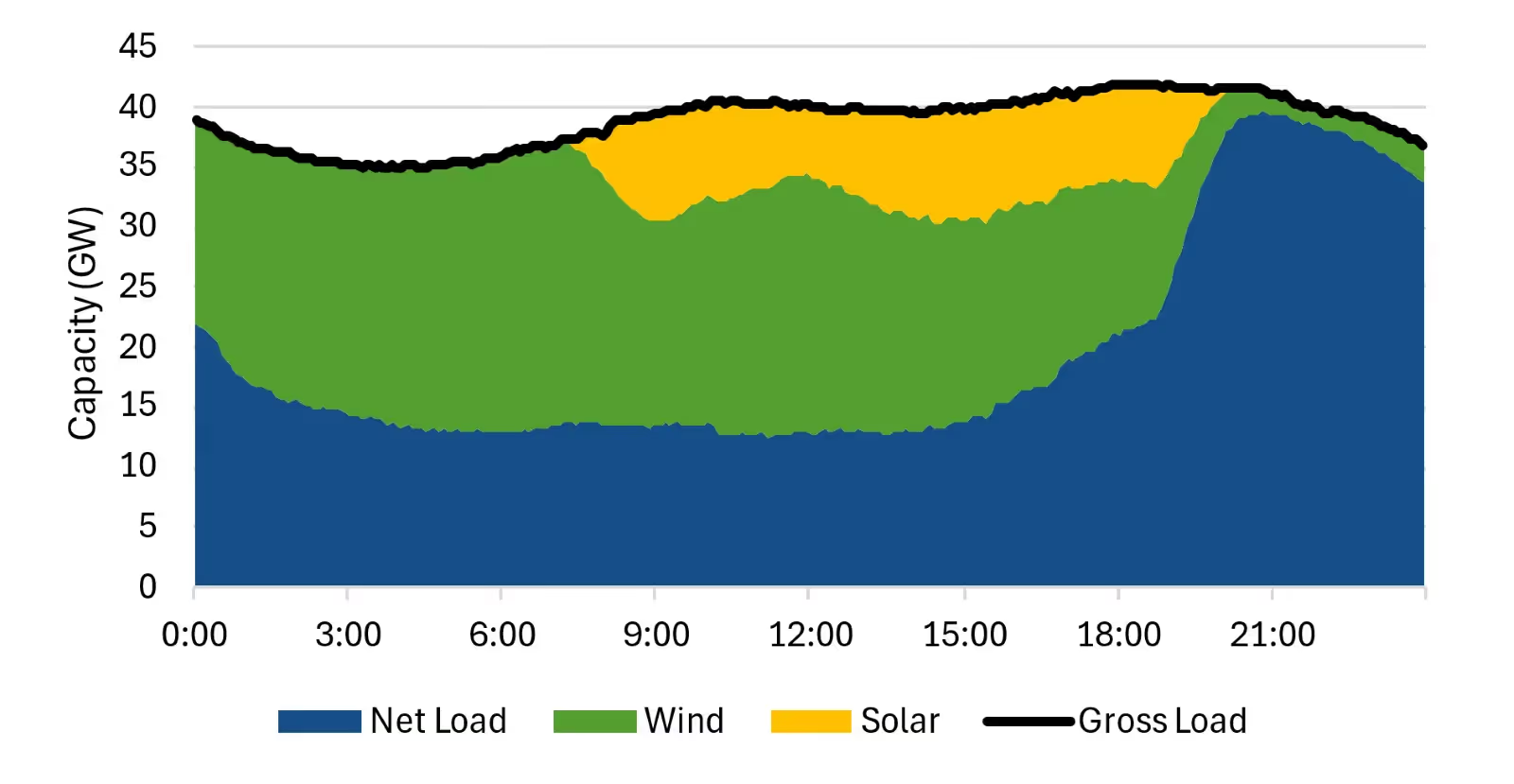

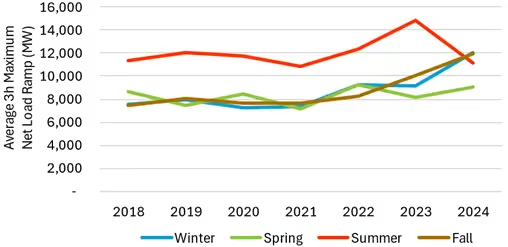

However, wind generation sometimes stays low or declines at sunset, compounding the evening solar drop-off and leaving the grid scrambling for fast-responding resources to meet the steep net load ramp during these ‘superduck’ events (Figure 2). Growing renewable capacity and changing demand conditions have caused the average three-hour net load ramps to increase in recent years, with seasonal variation in the magnitude of these ramps (Figure 3). For example, summer months regularly see larger evening net load ramps due to the elevated demand for power to cool homes and the significant solar generation that drops off quickly during sunset.1

These extreme ramps create power balancing challenges that are already visible in ERCOT, and upcoming wind and solar capacity additions will continue to exacerbate this phenomenon. Any thermal retirements from coal and older gas plants decrease the amount of dispatchable generation available to the system, although this is partially offset by battery storage additions and new gas incentivized by the Texas Energy Fund.2

Figure 1: Share of generation by fuel in 2016 and 2023

Figure 2: Steep net load ramp from coincident declines of wind and solar on April 20, 2023

Figure 3: Growth in three-hour net load ramps across seasons

Recent population growth has been accompanied by an increase in power-intensive industries such as AI data centers, cryptocurrency data mining facilities, and the electrification of vehicles and heating systems. These demographic and industrial changes drive up demand across all hours of the day, including peak demand hours which are already the most difficult to serve. Extreme weather events create additional risk, leading to tight conditions and sometimes straining the grid. The combination of load growth and extreme weather are changing grid conditions quickly and dramatically.

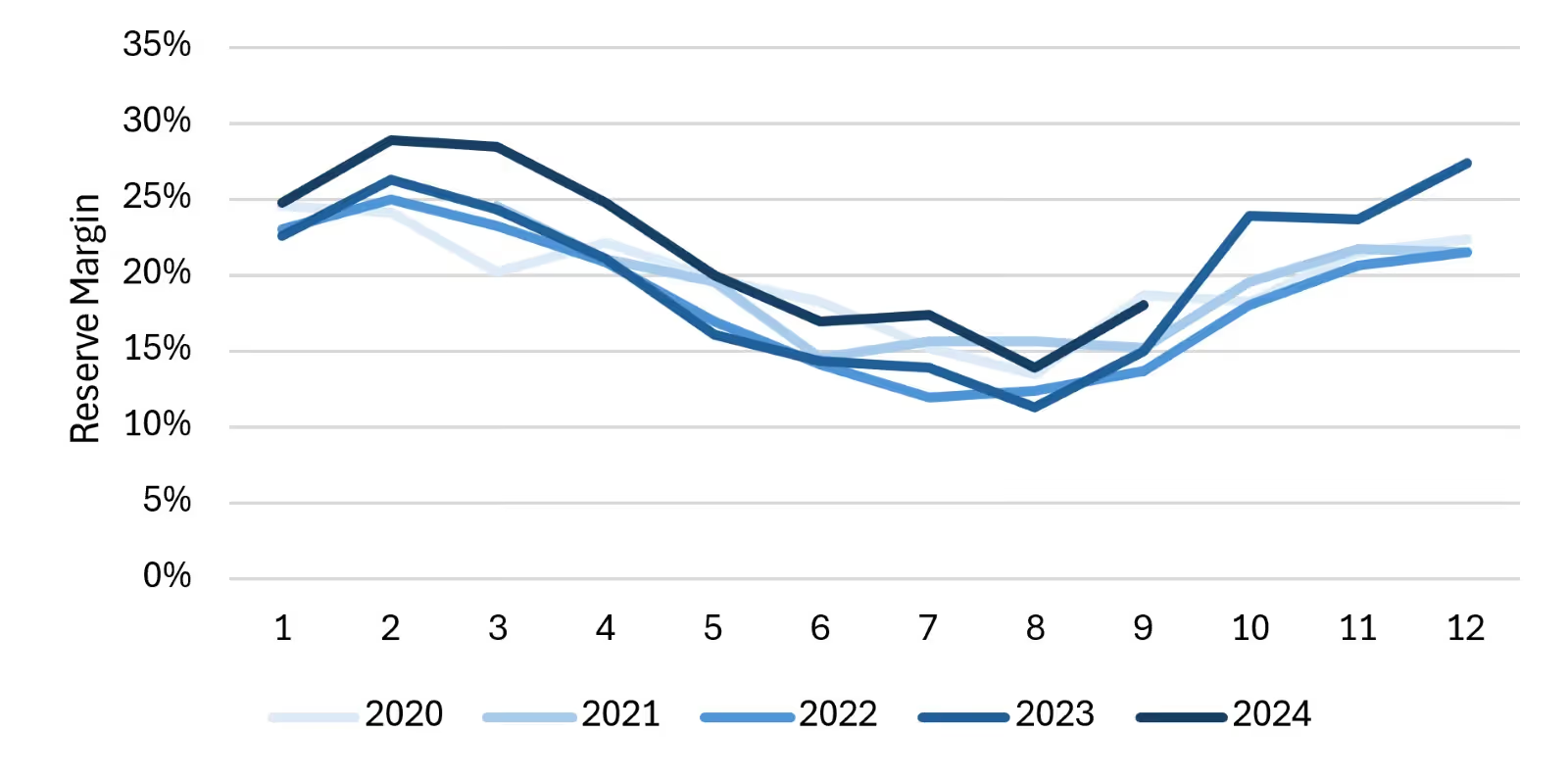

In May 2019, the peak demand record was about 60 GW, and the record increased to over 74 GW by the end of that summer. During summer 2022, peak demand again increased to nearly 80 GW. In summer 2023, a heat dome settled over Texas which caused ERCOT to set several new peak demand records, reaching over 85 GW. Most recently, in August 2024, Texas heat pushed demand to just under 86 GW, marking yet another peak demand record for the state. Extreme heat in summer months regularly pushes power demand far higher than in winter months, and this leads to seasonal variation in the system’s reserve margin. Figure 4 shows that the reserve margin is generally at its lowest in August when extreme heat most frequently occurs in Texas.

Figure 4: Seasonal variation in ERCOT's reserve margin during peak hours3

Peak power demand during heat waves usually lasts for several hours in the afternoon when cooling demand is highest. Solar resources generally produce during most of these hours, reducing net load when gross demand is at its highest, but solar generation ramps down quickly at sunset before power demand falls for the evening. These demand and generation profiles push peak net load periods to the evening hours when solar is no longer generating but cooling demand remains high, often leading to price spikes, as shown in Figure 5. These price spikes reflect the value of fast-responding dispatchable generation and illustrate the reliability challenge associated with sundown hours. These windows of high prices are relatively brief, leaving a reliability challenge that offers opportunities for two-hour duration storage.

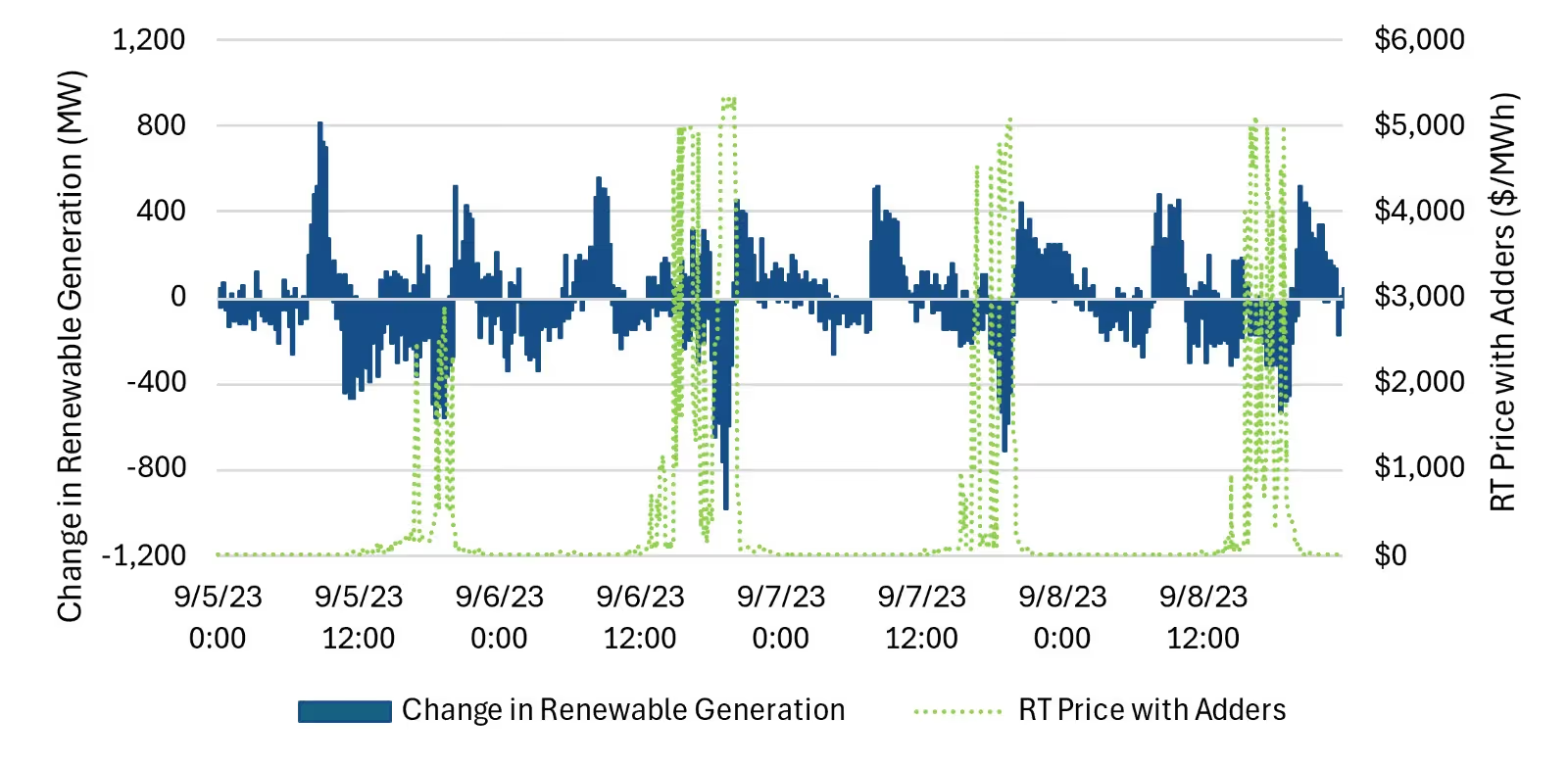

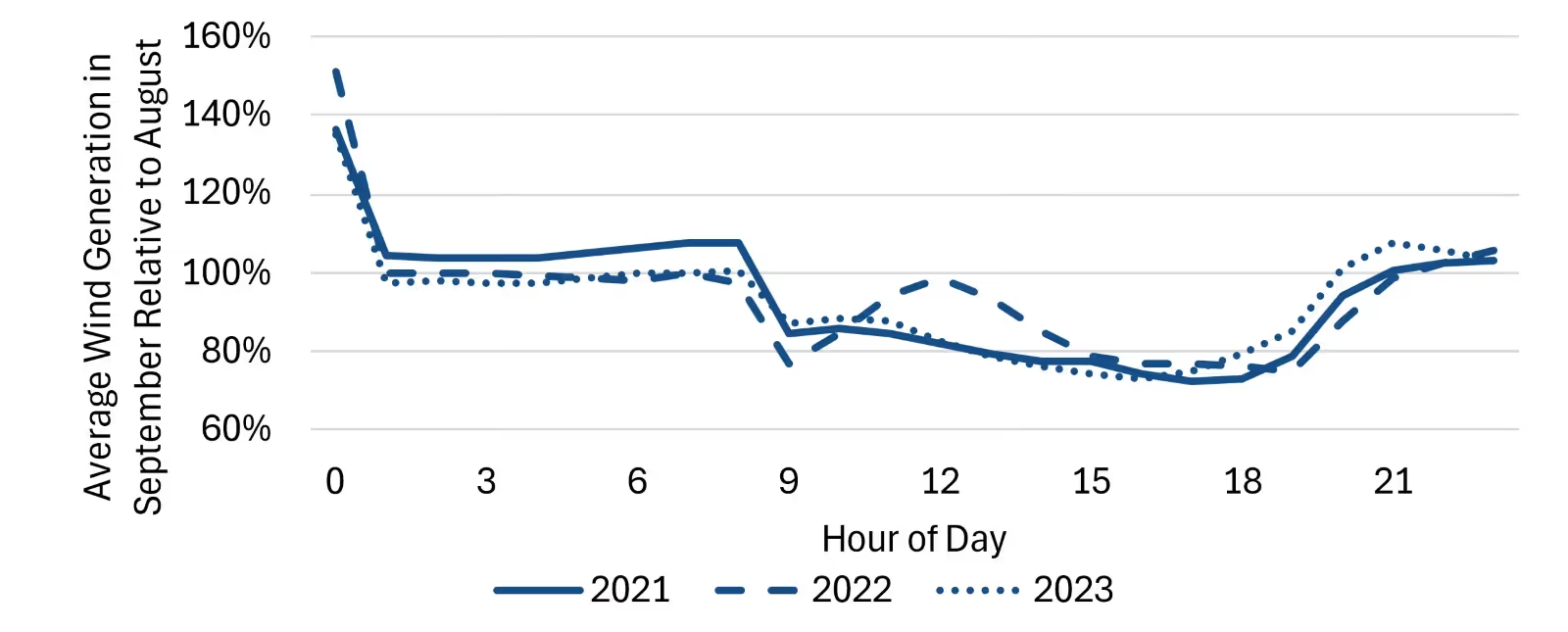

Increasingly, reliability periods are extending into September, as heat-driven demand can push load to levels as high as those seen in August, but with lower solar generation, earlier sunsets, and lower wind generation. These September reliability conditions leave ERCOT’s grid shorter for a longer period before wind generation picks up in the evening, with wind generation during sunset hours about 20% lower in September than in August (Figure 6).

Figure 5: Changes in renewable generation and RT prices in ERCOT North during a heat event, Sept 5-8, 20234

Figure 6: Average wind generation in September relative to August

Historically, the most common extreme weather events in Texas have been heat waves. Although winter demand peaks are less frequent and generally lower than summer peaks, severe cold weather events strain the grid in different ways. Electric heating systems contribute to high heating loads during cold weather events, with peaks expected to grow higher with further electrification of heating and transportation. Winter solar output is reduced by shorter days and the sun lowering in the sky, with a further reduction occurring when snow and ice cover solar panels and cloud cover reduces solar irradiance.

Additionally, winter heating demand is highest overnight and in the early mornings, when solar generation is zero, limiting the extent to which solar capacity can meet winter demand. Extreme cold can also cause correlated unplanned outages on the state’s wind and thermal generation fleet, or even disrupt gas supply as witnessed during Winter Storm Uri in 2021. The duration of cold weather events and their impact on demand and generation profiles create reliability challenges that are more complex than those associated with heat waves, lasting many hours or even days with low solar and wind generation, high thermal outages, and empty batteries.

Several technologies can support the grid during reliability periods, but each has limitations on how it can participate. Combustion turbines (CTs), reciprocating internal combustion engines (RICE), and batteries can all respond to market signals quickly, dispatching energy when the system needs it. Gas assets, such as CTs and RICE, are well-suited to take advantage of reliability periods because they can ramp up generation rapidly and continue providing power as long as they have fuel. Although RICE units have higher capital expenditures than CT units, they are more efficient and have no startup costs, providing ERCOT with highly flexible power that can operate efficiently for long periods as well as ramp quickly in response to changing renewable supply. CT units act well as peaker plants because they are less efficient than RICE, take longer to ramp up generation, and incur startup costs. All gas units are also subject to weather-induced forced outages due to both on-site mechanical issues and gas supply disruptions. Winter Storm Uri, for example, caused forced thermal outages to reach over 32 GW, compared with a historical February average of about 11.5 GW.5 Availability during extreme weather or other reliability events depends on preventative maintenance and the reliable operation of the state’s gas infrastructure.

In contrast to thermal generators, batteries have no fuel costs and can benefit from intraday price volatility, charging at low prices during low net load hours and discharging during peak net load conditions. Short-duration batteries are well-suited to take advantage of the reliability challenges posed by steep but brief sunset net load ramps, as those windows are usually limited to a few evening hours. Already, ERCOT has seen a notable increase in the reserve margin in 2024 relative to recent years, which is largely attributable to recent additions of solar and storage capacity (see Figure 4 above). The growing battery fleet in ERCOT provides reliability benefits, but only as long as the batteries have sufficient state-of-charge. As battery deployment grows, effective peak conditions will become longer, diminishing the value capture of shorter-duration batteries. Scarcity conditions will be associated with sunset/overnight, low wind, and empty batteries, creating opportunities for longer duration storage. However, without an organized capacity market, these projects must optimize their participation in the available revenue streams.

Growing load, accelerating renewable deployment, and changing scarcity conditions in ERCOT will drive a need for more dispatchable capacity that can operate during tight periods to ensure system reliability. The resources that enter the market must consider the physical capabilities needed to perform during scarcity conditions, the change in revenue streams over time, and the relative risk associated with each. Recent changes to the market structure in ERCOT aim to address growing reliability concerns and incentivize the buildout of necessary resources.

Many Regional Transmission Operators (RTOs) have capacity markets or bilaterally-traded capacity requirements that guarantee payments to resources that commit to providing power during a future period. In those RTOs, capacity prices and contracts act as a market signal to incentivize the buildout of new resources when they are needed. If a system is short on capacity, the price will rise to stimulate new buildout. The certainty and stability of capacity revenues makes the projects that receive them easier to finance. In lieu of capacity payments, ERCOT maintains a high cap on energy prices ($5,000/MWh) and provides scarcity price adders, which act as the system’s price signals for new buildout. This energy-only system subjects resources to more risk and variability, and project viability relies on bidding strategies that take advantage of opportunities in energy and ancillary markets to maximize revenues.

Growing renewable capacity in Texas has put downward pressure on power prices, but the added volatility from these intermittent resources creates opportunities for storage via arbitrage potential. Figure 7 shows renewable penetration and price volatility in the real-time market, which have grown together over the past several years. Growing solar generation contributes to volatility by creating ‘ducky’ prices in ERCOT, which provide reliable arbitrage revenues to storage with low midday prices when solar generation is high and a dependable evening price increase when solar generation drops off. Days with coincident evening drops of both solar and wind generation have steep net load ramps and, in turn, larger price spikes. These price spikes reflect the value of a resource's ability to provide power quickly when other resources are unavailable.

Figure 7: Renewable penetration and volatility in ERCOT South6

The Operating Reserve Demand Curve (ORDC), ERCOT's mechanism to provide an adder to power prices when operating reserves are low, incentivizes resources to be available when the system is scarce and signals the need for new capacity additions to the system. When operating reserves drop below 7,000 MW, a scarcity adder is applied to the power price, and the adder increases as available reserves drop, peaking at $5,000 when reserves drop below 3,000 MW. The ORDC provides an additional revenue stream to resources that are available to provide power when the system is scarce.

In 2023, the Texas legislature approved the Performance Credit Mechanism (PCM), which will create a voluntary forward market for generators to receive performance credits based on their availability during critical grid conditions. The PCM will provide additional revenues to resources that generate during the tightest grid conditions and will impose penalties on resources that commit to the market but are unable to fulfill their obligation. The PCM is expected to be implemented once real-time co-optimization is in place, which ERCOT anticipates achieving in late 2025. This new revenue stream is expected to be more stable than revenues from the ORDC adder because it will set a demand curve that will generate more consistent and reliable adders; however, revenue will still vary with grid conditions in a given year.

System tightness causes most price spikes in ERCOT, but scarcity pricing is infrequent because reserves rarely drop below the ORDC trigger point. Thus, resources that opt to participate in the PCM will have more opportunities to receive the associated revenues, rather than relying on large but infrequent adders during scarcity events. Battery participation in the PCM will be limited by the resource’s duration. Short-duration storage is an effective capacity resource in the near term, but as winter weather events become a larger reliability concern, more of the PCM value will stem from longer-duration events, resulting in more revenue for longer-duration assets. Gas assets are similarly well-suited as a capacity resource because they can ramp up generation quickly and continue producing power as long as grid conditions require, given a stable fuel source.

Ancillary service markets aim to maintain system reliability by quickly addressing system imbalances caused by sudden changes in load and unexpected disruptions to generation. These markets usually require quick response times, so batteries’ ability to charge and discharge nearly instantaneously makes them well-suited to participate in ancillaries. Ancillary prices have historically been a valuable revenue source for batteries, but this is quickly changing as battery deployment grows and batteries become price-setters. As ancillary markets become saturated with batteries, prices quickly decline to the opportunity cost of selling energy.

In 2021 ERCOT increased procurement of non-spin ancillary resources by nearly 4 GW. In 2023 ERCOT introduced the ERCOT Contingency Reserve Service (ECRS), an ancillary product with a market size of about 2 GW. This increase in ancillary procurement was partially offset by a reduction in non-spin procurement of about 1.3 GW. The growth of the ancillary market size has temporarily increased ancillary prices, but Ascend does not expect this trend to persist as rapid storage buildout continues. ERCOT plans to implement the Dispatchable Reliability Reserve Service (DRRS) by the end of 2024, creating a new ancillary product designed to procure quick-responding generation to address sudden fluctuations in demand.

The increase in non-spin and introduction of the ECRS will shorten the available supply stack for energy but will also provide a lifeline to some marginal capacity resources, leading to fewer retirements and thus keeping the supply stack generally longer than would otherwise be the case. ECRS has a two-hour duration requirement while non-spin and DRRS have a four-hour requirement, creating additional runway in ancillary value for batteries with sufficient duration to serve those products. However, continued storage buildout will result in a continued shift away from ancillary market revenues and toward energy arbitrage.

Reliability risks in ERCOT will become more prominent as fundamental grid conditions continue to change. Scarcity conditions will compose a growing portion of the total revenue available to resources in ERCOT, but access to those revenues is limited to resources that are able to generate during critical conditions.

When planning projects in ERCOT, developers should consider an asset’s flexibility and availability, as these characteristics maximize value for projects in a world of high price volatility. Flexibility allows generators to respond quickly to price signals and ramp up or down as needed to complement the intermittent nature of the growing renewable fleet. Availability dictates whether a unit is able to generate when needed and how long it is able to generate. Regular maintenance and weatherization can help to ensure availability during reliability events, particularly during extreme weather.

Additionally, developers should move toward longer-duration storage as peak periods and reliability events stretch into longer periods. Monitoring weather conditions will also become increasingly important, particularly as ERCOT adds more renewable capacity to its grid. As grid conditions and revenue opportunities change in ERCOT, generators will rely on bidding strategies that optimize their participation in the ancillary and energy markets. Learn more about Ascend’s proprietary approach to long-term market forecasting and Smartbidder bid optimization strategies here.

1 The average three-hour net load amp in summer 2024 fell due to relatively mild weather, which caused lower gross load and diminished the magnitude of the evening net load ramps

3 Based on load and available capacity reserves between the hours of 5-9 p.m.

4 Change in Renewable Generation’ refers to the change in combined wind and solar output over five-minute intervals. ‘RT Price with Adders’ refers to the ERCOT North Real-time price, including the ORDC.

5 Historical average is based on outage data from 2017-2024

6 Notes: ERCOT exhibited low volatility in 2020 due to the COVID-19 pandemic and depressed load. 2021 values exclude February 13-19 to avoid the distorting effects of Winter Storm Uri. Volatility increased in 20221 in part due to elevated gas prices, and an extended heat dome drove high power prices and volatility in 2023.

Scarcity events in ERCOT have persisted in recent years, and changing grid conditions could lead to an increase in both the severity and duration of these events. Growing population and load, increasing renewable capacity, the isolated nature of the ERCOT grid, and several extreme weather events have continued to test the system’s resilience. The continuation of these trends, coupled with the financial risks associated with building new gas generation beyond the limited quantity subsidized by the Texas Energy Fund, will increase reliability risks on the ERCOT grid.

Currently, critical system conditions are usually constrained to a few hours each year and are typically associated with sunset hours on particularly hot days. In the near term, short-duration batteries are well poised to generate during these brief periods of limited supply and high demand when prices reach their peak. However, as critical conditions stretch into longer peak periods and winter overnights, storage durations will need to increase to ensure grid reliability. These changing conditions in the context of ERCOT’s energy-only market structure bring into question the financial viability of longer-duration storage and other dispatchable assets that operate during infrequent extreme conditions. Evolving grid conditions and new market structures in ERCOT will need to incentivize the buildout of flexible resources that can address reliability risks that are growing in duration and frequency.

Texas produces the most renewable energy of any state in the country, and the share of the state’s electricity coming from renewables has increased significantly in the past several years (Figure 1). Solar capacity alone increased from less than one gigawatt in 2016 to over 32 GW in 2024. During hot summer days, solar generation during daylight hours supplies a significant and growing portion of the system's load when cooling demand is highest. Wind generation usually picks up after sunset, which helps offset the evening sundown ramp.

However, wind generation sometimes stays low or declines at sunset, compounding the evening solar drop-off and leaving the grid scrambling for fast-responding resources to meet the steep net load ramp during these ‘superduck’ events (Figure 2). Growing renewable capacity and changing demand conditions have caused the average three-hour net load ramps to increase in recent years, with seasonal variation in the magnitude of these ramps (Figure 3). For example, summer months regularly see larger evening net load ramps due to the elevated demand for power to cool homes and the significant solar generation that drops off quickly during sunset.1

These extreme ramps create power balancing challenges that are already visible in ERCOT, and upcoming wind and solar capacity additions will continue to exacerbate this phenomenon. Any thermal retirements from coal and older gas plants decrease the amount of dispatchable generation available to the system, although this is partially offset by battery storage additions and new gas incentivized by the Texas Energy Fund.2

Figure 1: Share of generation by fuel in 2016 and 2023

Figure 2: Steep net load ramp from coincident declines of wind and solar on April 20, 2023

Figure 3: Growth in three-hour net load ramps across seasons

Recent population growth has been accompanied by an increase in power-intensive industries such as AI data centers, cryptocurrency data mining facilities, and the electrification of vehicles and heating systems. These demographic and industrial changes drive up demand across all hours of the day, including peak demand hours which are already the most difficult to serve. Extreme weather events create additional risk, leading to tight conditions and sometimes straining the grid. The combination of load growth and extreme weather are changing grid conditions quickly and dramatically.

In May 2019, the peak demand record was about 60 GW, and the record increased to over 74 GW by the end of that summer. During summer 2022, peak demand again increased to nearly 80 GW. In summer 2023, a heat dome settled over Texas which caused ERCOT to set several new peak demand records, reaching over 85 GW. Most recently, in August 2024, Texas heat pushed demand to just under 86 GW, marking yet another peak demand record for the state. Extreme heat in summer months regularly pushes power demand far higher than in winter months, and this leads to seasonal variation in the system’s reserve margin. Figure 4 shows that the reserve margin is generally at its lowest in August when extreme heat most frequently occurs in Texas.

Figure 4: Seasonal variation in ERCOT's reserve margin during peak hours3

Peak power demand during heat waves usually lasts for several hours in the afternoon when cooling demand is highest. Solar resources generally produce during most of these hours, reducing net load when gross demand is at its highest, but solar generation ramps down quickly at sunset before power demand falls for the evening. These demand and generation profiles push peak net load periods to the evening hours when solar is no longer generating but cooling demand remains high, often leading to price spikes, as shown in Figure 5. These price spikes reflect the value of fast-responding dispatchable generation and illustrate the reliability challenge associated with sundown hours. These windows of high prices are relatively brief, leaving a reliability challenge that offers opportunities for two-hour duration storage.

Increasingly, reliability periods are extending into September, as heat-driven demand can push load to levels as high as those seen in August, but with lower solar generation, earlier sunsets, and lower wind generation. These September reliability conditions leave ERCOT’s grid shorter for a longer period before wind generation picks up in the evening, with wind generation during sunset hours about 20% lower in September than in August (Figure 6).

Figure 5: Changes in renewable generation and RT prices in ERCOT North during a heat event, Sept 5-8, 20234

Figure 6: Average wind generation in September relative to August

Historically, the most common extreme weather events in Texas have been heat waves. Although winter demand peaks are less frequent and generally lower than summer peaks, severe cold weather events strain the grid in different ways. Electric heating systems contribute to high heating loads during cold weather events, with peaks expected to grow higher with further electrification of heating and transportation. Winter solar output is reduced by shorter days and the sun lowering in the sky, with a further reduction occurring when snow and ice cover solar panels and cloud cover reduces solar irradiance.

Additionally, winter heating demand is highest overnight and in the early mornings, when solar generation is zero, limiting the extent to which solar capacity can meet winter demand. Extreme cold can also cause correlated unplanned outages on the state’s wind and thermal generation fleet, or even disrupt gas supply as witnessed during Winter Storm Uri in 2021. The duration of cold weather events and their impact on demand and generation profiles create reliability challenges that are more complex than those associated with heat waves, lasting many hours or even days with low solar and wind generation, high thermal outages, and empty batteries.

Several technologies can support the grid during reliability periods, but each has limitations on how it can participate. Combustion turbines (CTs), reciprocating internal combustion engines (RICE), and batteries can all respond to market signals quickly, dispatching energy when the system needs it. Gas assets, such as CTs and RICE, are well-suited to take advantage of reliability periods because they can ramp up generation rapidly and continue providing power as long as they have fuel. Although RICE units have higher capital expenditures than CT units, they are more efficient and have no startup costs, providing ERCOT with highly flexible power that can operate efficiently for long periods as well as ramp quickly in response to changing renewable supply. CT units act well as peaker plants because they are less efficient than RICE, take longer to ramp up generation, and incur startup costs. All gas units are also subject to weather-induced forced outages due to both on-site mechanical issues and gas supply disruptions. Winter Storm Uri, for example, caused forced thermal outages to reach over 32 GW, compared with a historical February average of about 11.5 GW.5 Availability during extreme weather or other reliability events depends on preventative maintenance and the reliable operation of the state’s gas infrastructure.

In contrast to thermal generators, batteries have no fuel costs and can benefit from intraday price volatility, charging at low prices during low net load hours and discharging during peak net load conditions. Short-duration batteries are well-suited to take advantage of the reliability challenges posed by steep but brief sunset net load ramps, as those windows are usually limited to a few evening hours. Already, ERCOT has seen a notable increase in the reserve margin in 2024 relative to recent years, which is largely attributable to recent additions of solar and storage capacity (see Figure 4 above). The growing battery fleet in ERCOT provides reliability benefits, but only as long as the batteries have sufficient state-of-charge. As battery deployment grows, effective peak conditions will become longer, diminishing the value capture of shorter-duration batteries. Scarcity conditions will be associated with sunset/overnight, low wind, and empty batteries, creating opportunities for longer duration storage. However, without an organized capacity market, these projects must optimize their participation in the available revenue streams.

Growing load, accelerating renewable deployment, and changing scarcity conditions in ERCOT will drive a need for more dispatchable capacity that can operate during tight periods to ensure system reliability. The resources that enter the market must consider the physical capabilities needed to perform during scarcity conditions, the change in revenue streams over time, and the relative risk associated with each. Recent changes to the market structure in ERCOT aim to address growing reliability concerns and incentivize the buildout of necessary resources.

Many Regional Transmission Operators (RTOs) have capacity markets or bilaterally-traded capacity requirements that guarantee payments to resources that commit to providing power during a future period. In those RTOs, capacity prices and contracts act as a market signal to incentivize the buildout of new resources when they are needed. If a system is short on capacity, the price will rise to stimulate new buildout. The certainty and stability of capacity revenues makes the projects that receive them easier to finance. In lieu of capacity payments, ERCOT maintains a high cap on energy prices ($5,000/MWh) and provides scarcity price adders, which act as the system’s price signals for new buildout. This energy-only system subjects resources to more risk and variability, and project viability relies on bidding strategies that take advantage of opportunities in energy and ancillary markets to maximize revenues.

Growing renewable capacity in Texas has put downward pressure on power prices, but the added volatility from these intermittent resources creates opportunities for storage via arbitrage potential. Figure 7 shows renewable penetration and price volatility in the real-time market, which have grown together over the past several years. Growing solar generation contributes to volatility by creating ‘ducky’ prices in ERCOT, which provide reliable arbitrage revenues to storage with low midday prices when solar generation is high and a dependable evening price increase when solar generation drops off. Days with coincident evening drops of both solar and wind generation have steep net load ramps and, in turn, larger price spikes. These price spikes reflect the value of a resource's ability to provide power quickly when other resources are unavailable.

Figure 7: Renewable penetration and volatility in ERCOT South6

The Operating Reserve Demand Curve (ORDC), ERCOT's mechanism to provide an adder to power prices when operating reserves are low, incentivizes resources to be available when the system is scarce and signals the need for new capacity additions to the system. When operating reserves drop below 7,000 MW, a scarcity adder is applied to the power price, and the adder increases as available reserves drop, peaking at $5,000 when reserves drop below 3,000 MW. The ORDC provides an additional revenue stream to resources that are available to provide power when the system is scarce.

In 2023, the Texas legislature approved the Performance Credit Mechanism (PCM), which will create a voluntary forward market for generators to receive performance credits based on their availability during critical grid conditions. The PCM will provide additional revenues to resources that generate during the tightest grid conditions and will impose penalties on resources that commit to the market but are unable to fulfill their obligation. The PCM is expected to be implemented once real-time co-optimization is in place, which ERCOT anticipates achieving in late 2025. This new revenue stream is expected to be more stable than revenues from the ORDC adder because it will set a demand curve that will generate more consistent and reliable adders; however, revenue will still vary with grid conditions in a given year.

System tightness causes most price spikes in ERCOT, but scarcity pricing is infrequent because reserves rarely drop below the ORDC trigger point. Thus, resources that opt to participate in the PCM will have more opportunities to receive the associated revenues, rather than relying on large but infrequent adders during scarcity events. Battery participation in the PCM will be limited by the resource’s duration. Short-duration storage is an effective capacity resource in the near term, but as winter weather events become a larger reliability concern, more of the PCM value will stem from longer-duration events, resulting in more revenue for longer-duration assets. Gas assets are similarly well-suited as a capacity resource because they can ramp up generation quickly and continue producing power as long as grid conditions require, given a stable fuel source.

Ancillary service markets aim to maintain system reliability by quickly addressing system imbalances caused by sudden changes in load and unexpected disruptions to generation. These markets usually require quick response times, so batteries’ ability to charge and discharge nearly instantaneously makes them well-suited to participate in ancillaries. Ancillary prices have historically been a valuable revenue source for batteries, but this is quickly changing as battery deployment grows and batteries become price-setters. As ancillary markets become saturated with batteries, prices quickly decline to the opportunity cost of selling energy.

In 2021 ERCOT increased procurement of non-spin ancillary resources by nearly 4 GW. In 2023 ERCOT introduced the ERCOT Contingency Reserve Service (ECRS), an ancillary product with a market size of about 2 GW. This increase in ancillary procurement was partially offset by a reduction in non-spin procurement of about 1.3 GW. The growth of the ancillary market size has temporarily increased ancillary prices, but Ascend does not expect this trend to persist as rapid storage buildout continues. ERCOT plans to implement the Dispatchable Reliability Reserve Service (DRRS) by the end of 2024, creating a new ancillary product designed to procure quick-responding generation to address sudden fluctuations in demand.

The increase in non-spin and introduction of the ECRS will shorten the available supply stack for energy but will also provide a lifeline to some marginal capacity resources, leading to fewer retirements and thus keeping the supply stack generally longer than would otherwise be the case. ECRS has a two-hour duration requirement while non-spin and DRRS have a four-hour requirement, creating additional runway in ancillary value for batteries with sufficient duration to serve those products. However, continued storage buildout will result in a continued shift away from ancillary market revenues and toward energy arbitrage.

Reliability risks in ERCOT will become more prominent as fundamental grid conditions continue to change. Scarcity conditions will compose a growing portion of the total revenue available to resources in ERCOT, but access to those revenues is limited to resources that are able to generate during critical conditions.

When planning projects in ERCOT, developers should consider an asset’s flexibility and availability, as these characteristics maximize value for projects in a world of high price volatility. Flexibility allows generators to respond quickly to price signals and ramp up or down as needed to complement the intermittent nature of the growing renewable fleet. Availability dictates whether a unit is able to generate when needed and how long it is able to generate. Regular maintenance and weatherization can help to ensure availability during reliability events, particularly during extreme weather.

Additionally, developers should move toward longer-duration storage as peak periods and reliability events stretch into longer periods. Monitoring weather conditions will also become increasingly important, particularly as ERCOT adds more renewable capacity to its grid. As grid conditions and revenue opportunities change in ERCOT, generators will rely on bidding strategies that optimize their participation in the ancillary and energy markets. Learn more about Ascend’s proprietary approach to long-term market forecasting and Smartbidder bid optimization strategies here.

1 The average three-hour net load amp in summer 2024 fell due to relatively mild weather, which caused lower gross load and diminished the magnitude of the evening net load ramps

3 Based on load and available capacity reserves between the hours of 5-9 p.m.

4 Change in Renewable Generation’ refers to the change in combined wind and solar output over five-minute intervals. ‘RT Price with Adders’ refers to the ERCOT North Real-time price, including the ORDC.

5 Historical average is based on outage data from 2017-2024

6 Notes: ERCOT exhibited low volatility in 2020 due to the COVID-19 pandemic and depressed load. 2021 values exclude February 13-19 to avoid the distorting effects of Winter Storm Uri. Volatility increased in 20221 in part due to elevated gas prices, and an extended heat dome drove high power prices and volatility in 2023.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

.avif)

.avif)

%20(1).avif)