Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Energy Demand and Supply are Undergoing Structural Change. Energy Market Forecasting Models Must Reflect This New Reality.

In today's rapidly evolving energy markets, choosing the right forecast has never been more critical. Model-driven fundamental forecasts underpin nearly every aspect of energy planning processes and drive important decisions related to optimal dispatch, capacity expansion, resource adequacy, reliability planning, project/portfolio valuation, and investment.

Energy market forecasts serve as foundations for developers, utilities, independent power producers, energy project investors, asset owners and operators, and electric retailers. The right forecasts help maximize investment returns, minimize risks, and optimize project siting, sizing, valuation, origination, and operation. Choosing the right forecast can be the difference between profit and loss, or even risk stranding an asset.

For decades, energy market stakeholders have relied on production cost models to forecast power prices, generation dispatch, capacity expansion, and reliability metrics. This approach worked well in an era where large, weather-insensitive thermal generators set prices while experiencing minimal net load misses in a mostly static energy policy environment.

Today’s power markets, however, are vastly different than they were even five years ago. Many assumptions traditionally used by production cost models no longer hold true. As power markets evolve, and as renewables make up increasingly larger portions of supply stacks in markets across the world, numerous pricing drivers have changed – permanently.

Yet, many production cost model-driven fundamental forecasts still suffer from a backwards-looking paradigm. Legacy models assume perfectly optimized gas units usually set the marginal price, and so inexorably increasing gas prices keep the market price of power rising. In reality, wholesale power prices will be flat or declining as renewables displace thermal supply and renewable curtailment occurs increasingly often.

As renewables continue to make up larger percentages of supply stacks, the dynamics of this shift will only become more pronounced. To thrive in this environment, energy market stakeholders need a sophisticated, high-resolution forecast grounded in the new realities of power markets.

The Ascend Opportunity Cost Forecasting Framework (OCFF) was designed specifically to reflect the new market dynamics of modern power markets, thus ensuring that energy market stakeholders receive accurate, defensible, and bankable forecast outputs. In contrast to legacy production cost models, the OCFF considers that price formation from opportunity cost bidding behavior more accurately reflects true power market prices and price volatility. The OCFF also leverages hourly and sub-hourly analytics, coupled with an economic lens, to provide far more granular and defendable fundamental forecasts than those delivered by traditional models.

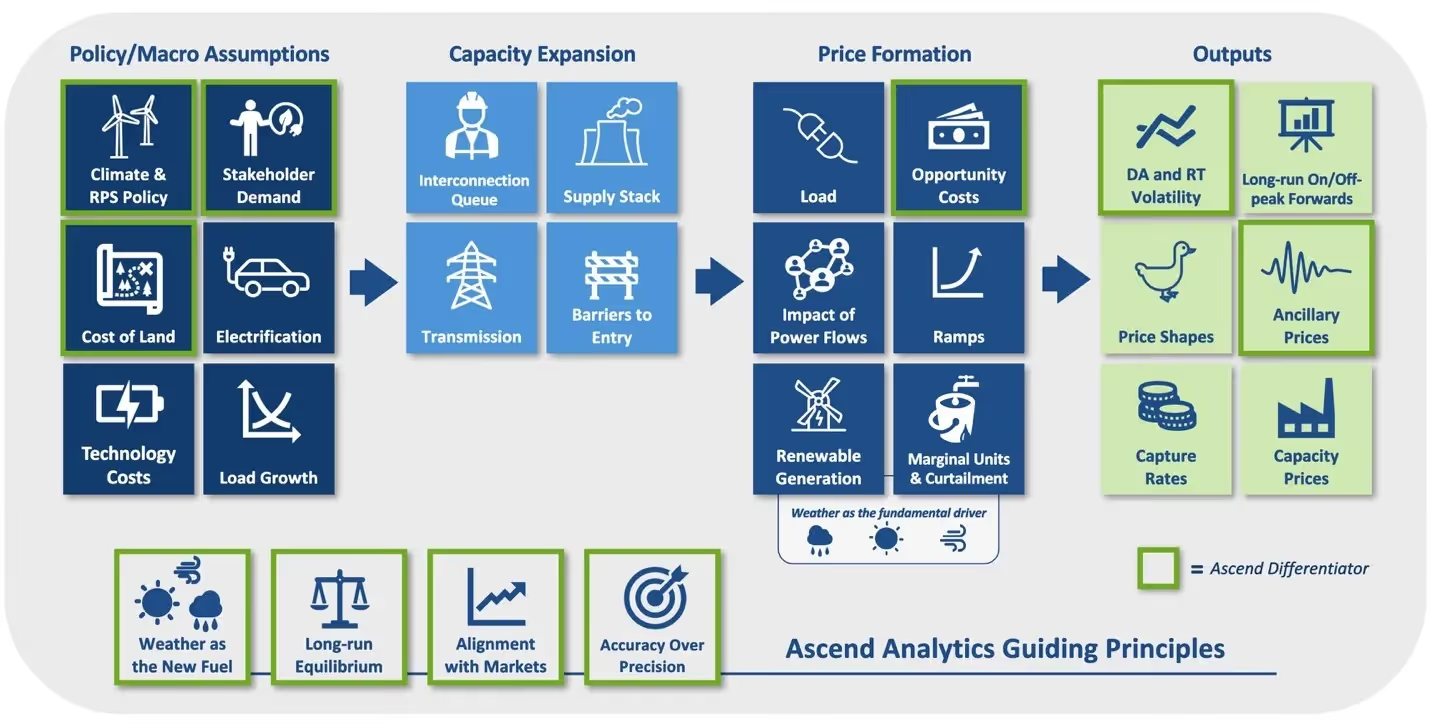

While opportunity cost considerations are an essential part of the OCFF, they are also only one piece of the larger forecasting framework. As shown in Figure 1, the OCFF contains the same core elements as those found in standard energy price formation forecasts, in which macro and policy assumptions drive capacity expansion, which in turn drives price formation and ultimately forecast outputs.

Even though the OCFF shares structural similarities with standard price formation forecasts, it differs from legacy approaches in a number of significant ways. Four crucial differentiators include the guiding principles that Ascend uses, shown at the bottom of Figure 1, to anchor all forecasting.

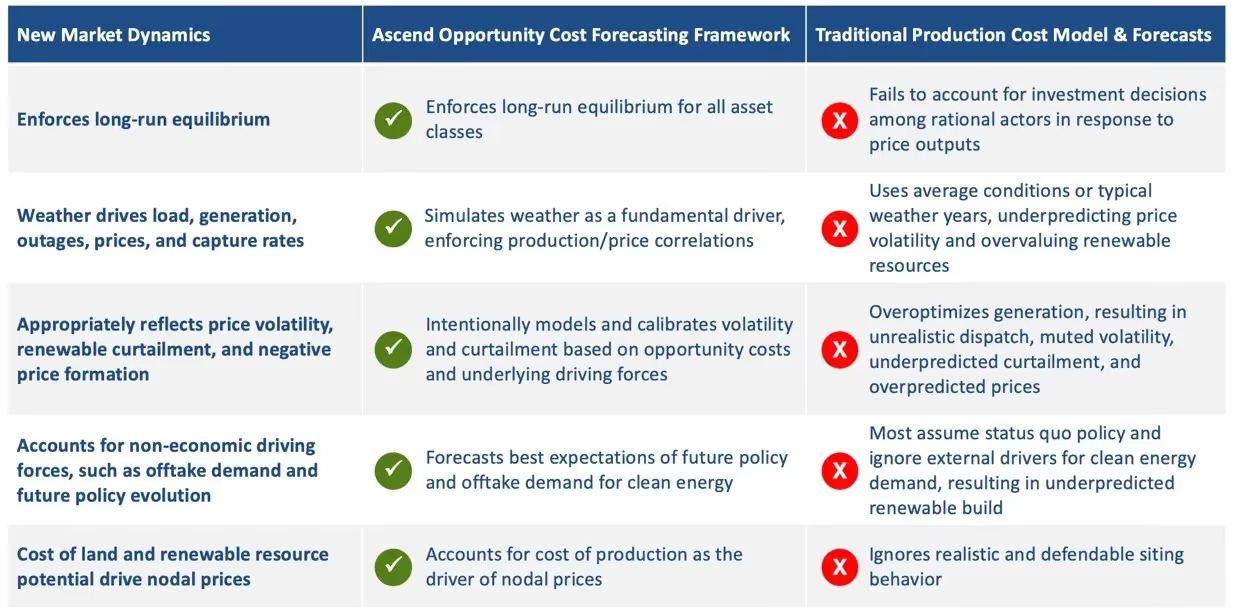

The OCFF also accounts for important power market realities in ways that standard production cost models do not. While many forecasts use purely economic models to guide capacity expansion, Ascend incorporates a granular approach to modeling that captures the fundamental market dynamics – economic and non-economic alike – essential to successfully navigating rapidly evolving energy markets. As summarized in Table 1, these dynamics include the need to enforce long-run equilibrium, weather's profound impact on price formation, volatile pricing dynamics associated with increasing renewable penetrations, projected climate/RPS policy and stakeholder demand for clean energy, as well as considerations related to cost of land and its impact on locational price dynamics.

As load growth surges in energy markets across the world, and numerous project developers compete to provide supply to meet demand, rational investments will converge markets towards an equilibrium between the locational cost of new entry and locational project value. Premium locations cannot stay premium. Thus, all forecasting aspects must align to a world constrained by long-run equilibrium.

Forecasts that fail to account for long-run equilibrium lead to undefendable valuations that are incompatible with the competitive markets that arise from the abundance of project development activity that exists today.

Ascend's forecasts adhere to long-run equilibrium, which ensures that resources can only earn normal returns in the long run, since supernormal returns would drive market entry and subnormal returns would drive retirement or deter entry. Long-run equilibrium modeling shows significant increases in renewable penetration and storage buildout as their costs continue to decline in the medium- to long-term future. In the long run, the OCFF ensures that revenue stacks do not exceed normal returns, with equilibration timing that varies by market. Consequently, Ascend's forecasts ensure that total projected revenue stacks align to capital expenditures (CapEx) for each asset class, including forecasted changes in CapEx over time.

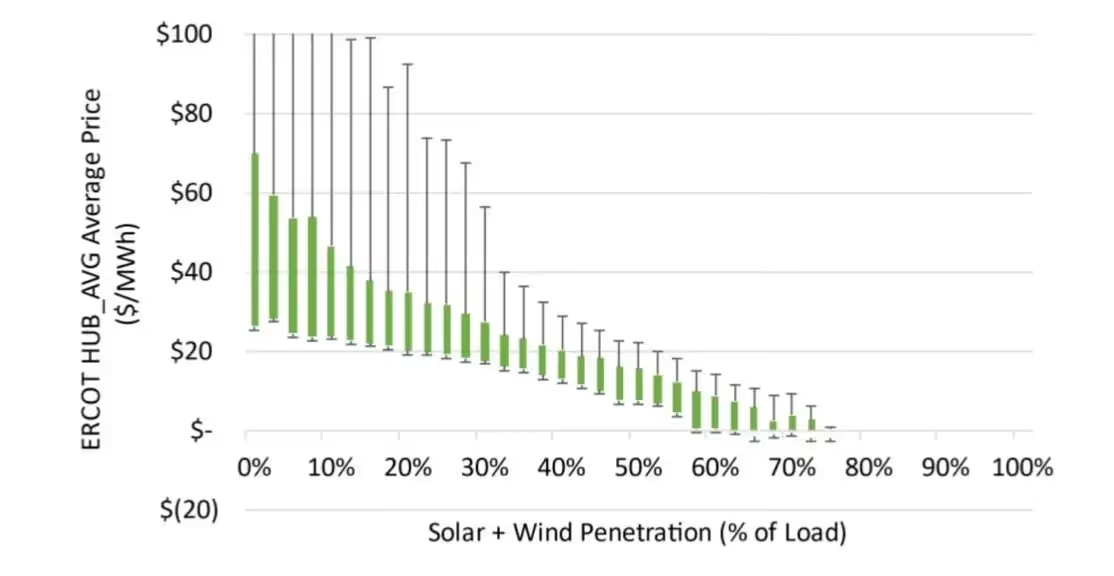

Historically, weather was primarily a factor in energy demand, such as a heat wave driving broad air conditioner use. In today’s energy landscape, weather serves as the essential underlying driver for both demand and supply, and thus plays an increasing role in driving price formation. As renewable penetration increases, energy prices decline, as shown in Figure 2. In markets like CAISO or ERCOT, renewables and storage already set prices in energy, capacity, and ancillary markets. This dynamic will become – and is increasingly becoming – apparent in other US markets as renewable penetration accelerates.

Traditional production cost model-based forecasts often use average conditions or 'typical' weather years. This approach underpredicts price volatility, overvalues renewable resources, and can severely undervalue storage. Models that do not account for underlying weather at an hourly or sub-hourly level can also lead to decoupled price and generation simulations with inflated capture rates that ignore price depression when renewable production is high. Miscorrelating independent price and generation time series can lead to overvaluation of renewable resources: average price and generation shapes are not accurate proxies for generation-weighted prices. In reality, most renewable projects will see declining capture rates as renewable buildout grows. Ultimately, an inflated and biased price forecast will lead to an inflated and biased project valuation.

Uniquely, Ascend simulates weather as the new fuel that drives renewable generation, load, outages, prices, opportunity costs, and capture rates, accounting for the impact of weather on both demand and supply. The Ascend OCFF ensures that prices are represented as a function of net load (load less renewables) in which weather determines both supply and demand while renewable generation displaces higher-cost thermal generation. Price extremes will be driven by renewable generation: the highest highs will occur when renewable production is lowest, and the lowest lows will occur when there is surplus renewable generation. Zero and negative prices will become increasingly common. Ascend's forecasts reflect declining heat rates as renewable penetrations increase, and calibrate negative price formation with observed market behavior to produce price forecasts that align most closely to the realities of energy markets with high renewable penetration.

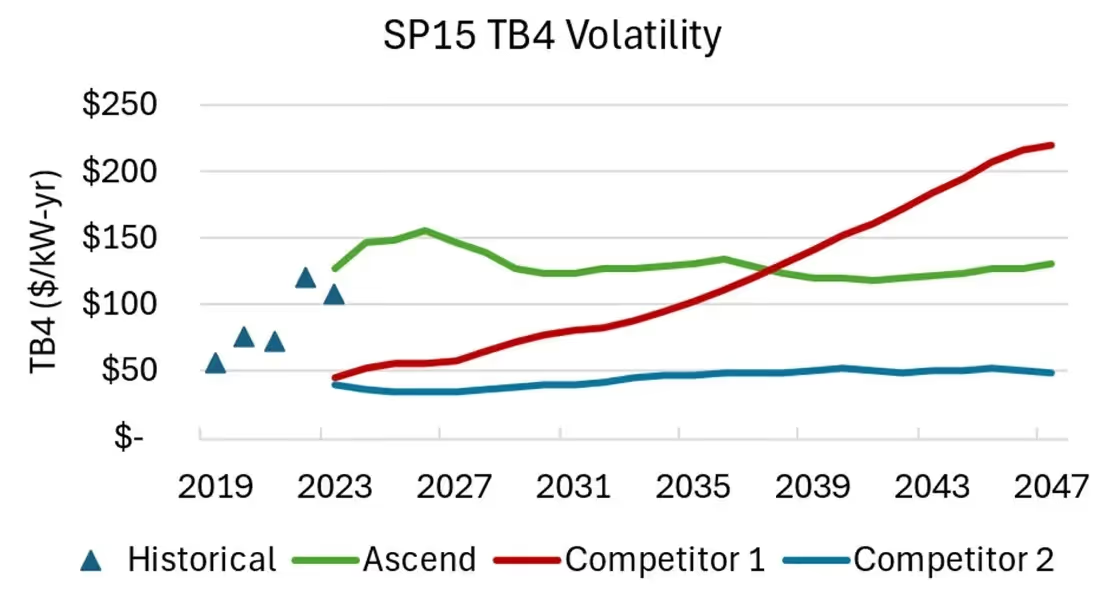

In renewables-heavy markets, unpredictable weather and intermittent resources drive uncertainty and opportunity cost decisions, leading to price volatility that is typically much higher than what traditional production cost models predict. Because storage and other flexible generation resources respond very differently to volatile prices than to flat prices, volatility must be both calibrated and forecasted appropriately in order to properly value these assets. Near-term volatility should be consistent with observed market behavior. Long-term volatility should be forecasted based on fundamental driving forces.

Typical production cost models optimize thermal dispatch around known load and renewable generation profiles. This approach results in over-optimized models with volatility that does not reflect what actually emerges in power markets. Failing to intentionally model volatility leads to models that are inconsistent with the market and irrelevant for valuation of storage and other flexible assets, often undervaluing storage and overvaluing renewables.

Grounded in observed market behavior, the OCFF reflects uncertainty and opportunity costs in price formation. In addition to modeling day-ahead (DA) volatility, Ascend simulates real-time (RT) prices and models the impact of renewable and storage buildout on RT price dynamics and volatility. Thus, Ascend's forecasts often contain price volatility that is higher than that predicted by traditional production cost models, but far more reflective of the realities of the market, as shown in Figure 3.

In power markets across the world, clean energy policy and corporate offtake demand have already emerged as significant driving forces for clean energy deployment.

Yet many forecasts rely on 'status quo policy' assumptions that fail to account for policy evolution and offtake demand, leading to underprediction of renewable buildout, and thus higher prices and lower volatility. Similarly, models that assign a zero value to renewable energy credits (RECs) lead to indefensible forecasts that dismiss or minimize corporate interest in clean energy supply.

Rather than relying on ‘status quo policies,’ which are certain to be incorrect, the Ascend OCFF incorporates assumptions about anticipated state- and federal-level clean energy policy evolution in base case forecasts. Ascend also adds a select amount of non-economic renewable generation into forecasts to reflect anticipated offtake demand and willingness to pay for renewable resources, since corporate offtake demand and ESG factors drive clean energy deployment beyond what an economic model alone would predict. In doing so, Ascend effectively assumes that RECs have a value above zero, reflecting the desire for offtakers to contract with clean energy.

During an energy transition, locational price patterns will be driven by variation in renewable resource quality as well as land cost. Permanent differences in climate and geography create permanent differences in renewable resource potential, population density, and cost of land, which affect the ability to develop projects and the resultant cost of energy, as illustrated in Figure 4. While the alignment between population density and price is not perfect due to differences in solar resource and transmission constraints, more dense and higher-cost areas generally show higher prices relative to less populated areas. New transmission build will only incentivize more project development in lower-cost areas until the price differentials once again reflect the underlying differences in cost of production. High population density and high cost of land create perpetual barriers to new development.

Many production cost models fail to account for locational cost of production, ignoring rational and realistic siting behavior for developers of new projects. This approach leads to underestimates of basis risk and locational premiums.

The OCFF analyzes each market regionally based on geospatial barriers in order to produce granular views of locational price patterns. The Ascend model also enforces compression within self-similar regions over time, as well as maintaining differentiation over time between regions with geospatial barriers between them.

Near-term projections can only be accurate to the extent that the near-term future is knowable. Consequently, Ascend's forecasts intentionally and philosophically align to market-traded forwards, as those reflect the best-known information about the near term. If it were easy to know whether the market was wrong, betting against the market would be free money and a forecaster should be doing so rather than selling forecasts. In the long term, Ascend's forecasts focus on the most important drivers of uncertainty and risk by appropriately modeling the key policy, economic, and physical constraints that govern capacity expansion and dispatch, all while ensuring a view that enforces long-run equilibrium.

Ascend prioritizes accuracy over precision in the long term: while no forecast is perfect, it should be defendable and align to a most probable future that accounts for the likely decisions and motivations of market participants and stakeholders. While forecast accuracy is weather-dependent and can vary widely with accuracy in the traded market forwards, Ascend’s valuation tools and forecasts are continuously calibrated to reflect realizable revenue in operating assets.

In assessing how well the OCFF performs in forecasting the price formation outputs seen in Figure 1, Ascend considers 'directional correctness' to be the most appropriate signal for 'accuracy' (since Ascend's forecasts are necessarily tied to the market, and thus can only be as accurate as the market). Ultimately, the OCFF has consistently proven to be directionally correct in modeling a number of market dynamics, including the evolution of price dynamics for ancillary services, long-run on and off-peak forwards, price shapes, capacity prices, and DA and RT price volatility. The ability to model these market dynamics demonstrates the effectiveness of the model overall, lending fidelity and clarity to the many other analytic models it informs, as well as credibility to efforts around project development, project finance and due diligence, power procurement, and M&A.

Ascend also has consistently and correctly anticipated the evolution of clean energy policy at both the federal level and in numerous American states, illustrating the importance of forecasting based on anticipated changes rather than status quo policy.

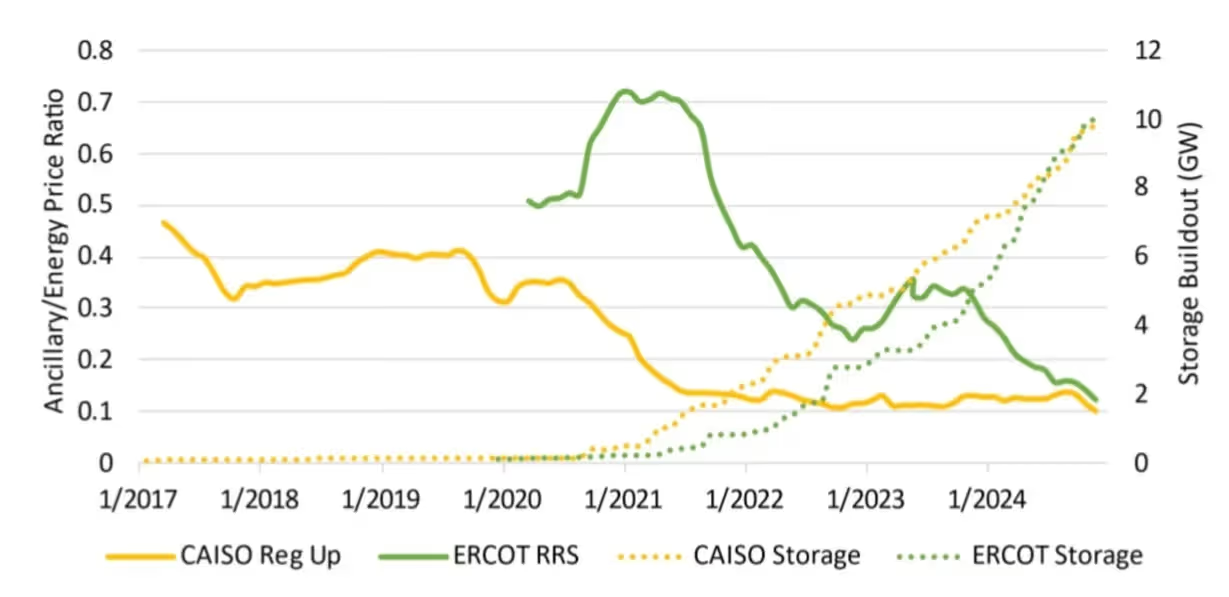

Ascend ancillary service price forecasts explicitly consider that storage resources are so well-suited to providing ancillary services that they will quickly saturate the markets and set energy prices as their deployment grows. Because batteries have many idle hours, opportunity costs in these intervals are close to zero, depressing ancillary prices.

In the near term, Ascend’s ancillary forecasts are informed by ancillary market forwards (where available) and historical pricing dynamics (for markets not yet saturated by storage). As ancillary markets saturate with storage, Ascend expects ancillary service prices to reflect the opportunity cost to storage of not providing real-time energy arbitrage within a given time interval. Thus, prices will be highest during periods of high expected RT price volatility, and lowest during periods of low expected RT price volatility. Providing ancillary services will offer only a slight revenue uplift, offsetting the increased risks and complexity of optimizing battery operations across both energy and ancillary markets.

Using the OCFF, Ascend anticipated (and warned investors about) the declining value of ancillary services in battery-heavy markets. Figure 5 shows the ancillary price saturation that has already occurred in CAISO and ERCOT, which Ascend predicted several years before it happened.

The Ascend approach for forecasting monthly on/off-peak forwards specifically accounts for the two primary ways that renewable penetration drives price depression: by shifting the supply stack, and through negative price formation during surplus renewable generation. As renewable penetration rises, the shifting of the supply stack drives general price depression while reflecting steeper supply stack slopes at periods of high demand than at periods of low demand.

Ascend fundamental modeling accounts for changes to the marginal generation unit as renewable penetration rises. In general, minimal to no curtailment occurs at renewable penetrations below 10-20%, slowly rising curtailment and frequency of negative prices occur as renewable penetrations rise to ~40%, and a rapid increase in curtailment and negative prices occurs at renewable penetrations above ~40%. As renewable curtailment becomes increasingly common at high renewable penetrations, zero/negative prices will accordingly weight the average prices.

Ascend uses relationships derived from market fundamental modeling for these price depression mechanisms to account for heat rate depression and negative price formation. Ascend also incorporates the impact of storage by modeling the ability of storage to absorb surplus renewable generation. Hourly, monthly, and seasonal variation in renewable generation and load shapes provide a more granular basis for forecasting the impacts of renewable curtailment by peak period, month, and year.

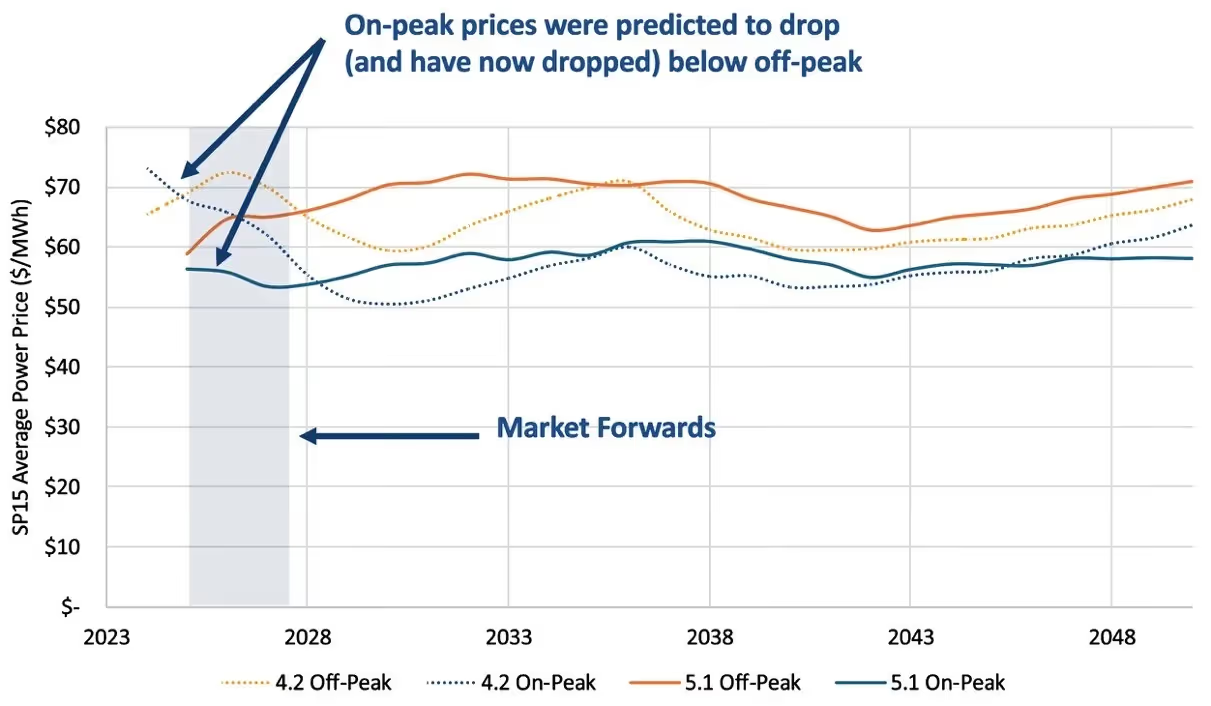

A powerful example of the importance of capturing new market dynamics is reflected in the OCFF model’s ability to accurately forecast that solar deployment would cause CAISO on-peak prices to drop below off-peak prices (and Ascend warned investors about continued declines in solar-weighted prices), as shown in Figure 6. CAISO on-peak prices have been depressed by solar deployment, while off-peak prices remain driven by gas and carbon prices. Ascend has been forecasting the mid-2020s inversion of on- and off-peak prices since 2020, well before the inversion appeared in market forwards. The inversion has moved earlier, with rising gas and carbon prices lifting the off-peak, and rising REC prices driving mid-day prices more negative and reducing the on-peak.

In an energy transition, price shapes become increasingly dependent on load and renewable generation profiles that vary with weather. Production cost models that do not account for weather, or that use 'average' weather, will often miss important price dynamics and variability in price shapes.

At Ascend, price shapes are forecasted at the monthly level, providing 24-hour price shapes. The Ascend price shape forecast uses fundamental modeling that incorporates evolution in load shape. Depending on the energy market, this evolution may be driven by such elements as forecasted electric vehicle adoption, building electrification, energy efficiency, behind-the-meter solar and storage deployment, and changes to renewable generation deployment. Additionally, the OCFF accounts for the impact of structural changes in the net load shape (such as the net load ramp rate) that also affect price shapes.

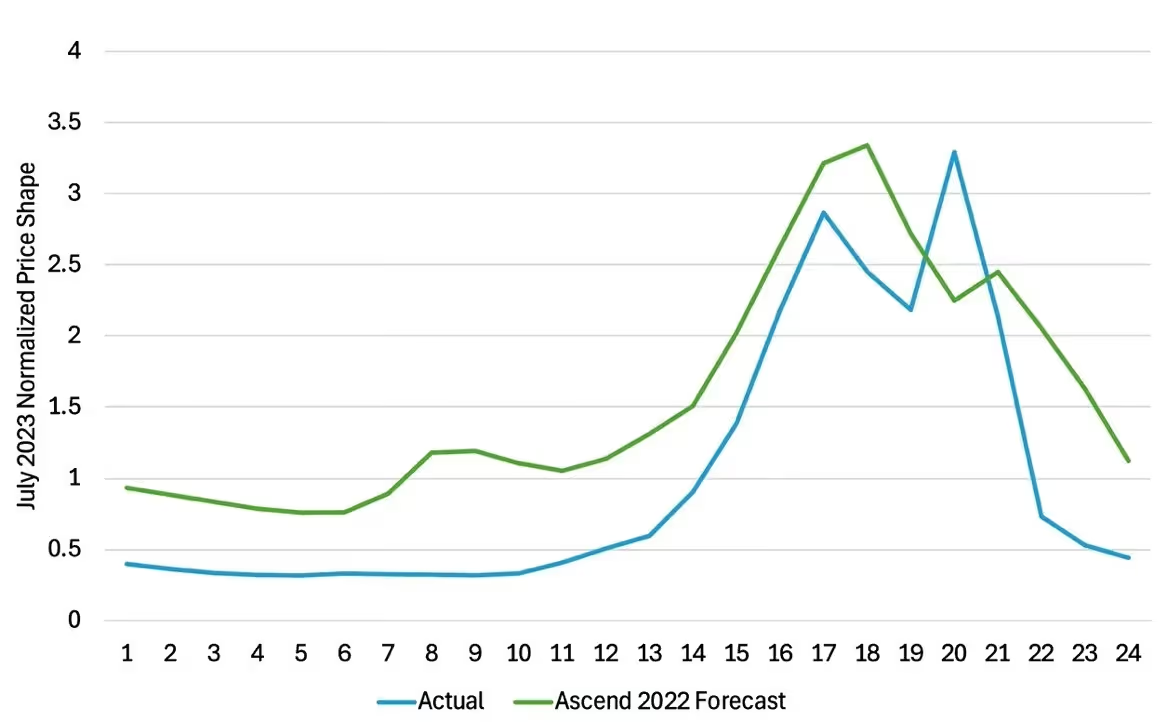

Using the OCFF, Ascend predicted that ERCOT summer price shapes would push the highest prices into sunset hours and exhibit a double-peak in some months, unlike the simpler duck shape in CAISO. As shown in Figure 7, ERCOT developed a double peak in July 2023 with declining load causing an initial price drop from an afternoon peak, followed by a second price peak as solar generation declined, before price declined again as load continued to drop.

Ascend capacity price forecasts assume that the marginal new capacity unit will increasingly be a storage resource. Depending on the market, this assumption is based on renewable policy mandates, stakeholder opposition to the construction of new thermal resources, low capacity values for wind and solar generation, and difficulties in financing or receiving regulatory approval for new thermal capacity due to stranded asset risk.

In the near term, Ascend also considers the impact of expected retirements of thermal capacity due to age and economic pressures as well as the amount of storage in the interconnection queue. In the medium- and long-term future, Ascend forecasts capacity prices based on the expected Net cost of new entry (Net CONE) of new resources while also accounting for increasing duration requirements for storage as storage deployment increases.

Ascend anticipated that storage would become the primary new unit entry for capacity and begin to drive capacity prices, beginning in locations with clean energy mandates. Storage has been driving bilateral capacity prices in California since about 2020, and New York recently designated two-hour storage as the reference unit in its capacity market, aligning to Ascend’s prediction that the Natural Gas Combustion Turbine would be displaced as the reference unit.

While renewables reduce the average price of energy, the intermittency of renewable output drives increased volatility of prices due both to the variability in weather and the uncertainty in renewable production across multiple timescales. In general, growing volatility is observed with growing renewable penetration both in RT and DA markets year-over-year. Ascend uses a variety of custom metrics to forecast RT and DA volatility.

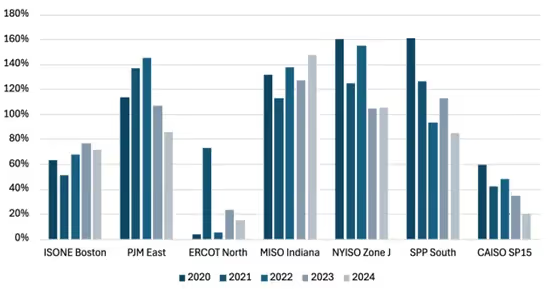

Real-time markets generally have higher volatility than DA markets, with RT prices more volatile because forecast errors must be adapted to on short notice. Higher RT volatility can add 50% more revenue (or more) for batteries and other flexible resources, as seen in Figure 8. Thus, volatility must be modeled accurately at both the DA and RT levels. Ascend forecasts DA and RT volatility based on fundamental driving forces in order to model future value for storage and other flexible resources.

By reflecting uncertainty and opportunity cost in resource bidding and dispatch behavior, as well as by calibrating volatility against historical dynamics, Ascend predicted increasing price volatility in renewables-heavy markets, as shown in Figure 3. Grounded in the realities of the energy transition, Ascend's ability to reflect observed market volatility and forecast it based on underlying driving forces is critical for defendable valuation of flexible assets.

As noted previously, Ascend incorporates assumptions about anticipated energy policy evolution in base case forecasts, going beyond the unrealistic forecast scenario of only considering currently enacted policies. While policy evolution is uncertain, the least likely future would hold all policy as status quo.

Ascend assesses policy outlooks at both the state and federal level to anticipate the most likely developments for clean energy policy. These assessments could include making clean energy goals more or less aggressive in terms of timelines or absolute targets, extending or sunsetting existing clean energy incentives, offering outlooks for carbon pricing, and accounting for potential tariffs.

Ascend has anticipated tightening clean energy standards in numerous states. Prior to being enacted (or even introduced in state legislatures), for example, Ascend predicted clean energy/zero emission mandates in Illinois, Minnesota, Michigan, Colorado, Oregon, Washington, Vermont, Rhode Island, Delaware, and Maryland. Additionally, Ascend anticipated that California would accelerate its clean energy timelines and adopt more aggressive interim emissions targets. At the federal level, Ascend was already assuming extensions to the clean energy production tax credit and investment tax credit prior to the passage of the Inflation Reduction Act. As a result of these anticipated policies, Ascend’s forecasts were able to retain continuity despite a changing policy environment.

In searching for the right forecast, good and prudent investors should seek out what they don’t want to hear. Not every investment will be a good one, and not everyone can be above average. Investors should also have a clear understanding of the realities of today's energy markets. Prices can’t keep climbing when renewables are setting prices. Projects can’t earn supernormal returns indefinitely when participants respond to incentives and drive equilibrium. Valuations for renewables and storage will often be in opposition: the generation surpluses that drive value for storage suppress value for renewable generation.

While no long-term forecast is perfectly accurate, Ascend’s opportunity cost forecasting framework consistently identifies numerous critical driving forces and market dynamics that inform investment in rapidly changing power markets. The Ascend OCFF provides a powerful, high-resolution analytic lens that produces bankable, defendable energy market forecasts that align to a most probable future.

Trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments, AscendMI™ (Ascend Market Intelligence) leverages the OCFF to deliver proprietary power market forecasts that reflect the new market dynamics driving the energy transition.

Energy Demand and Supply are Undergoing Structural Change. Energy Market Forecasting Models Must Reflect This New Reality.

In today's rapidly evolving energy markets, choosing the right forecast has never been more critical. Model-driven fundamental forecasts underpin nearly every aspect of energy planning processes and drive important decisions related to optimal dispatch, capacity expansion, resource adequacy, reliability planning, project/portfolio valuation, and investment.

Energy market forecasts serve as foundations for developers, utilities, independent power producers, energy project investors, asset owners and operators, and electric retailers. The right forecasts help maximize investment returns, minimize risks, and optimize project siting, sizing, valuation, origination, and operation. Choosing the right forecast can be the difference between profit and loss, or even risk stranding an asset.

For decades, energy market stakeholders have relied on production cost models to forecast power prices, generation dispatch, capacity expansion, and reliability metrics. This approach worked well in an era where large, weather-insensitive thermal generators set prices while experiencing minimal net load misses in a mostly static energy policy environment.

Today’s power markets, however, are vastly different than they were even five years ago. Many assumptions traditionally used by production cost models no longer hold true. As power markets evolve, and as renewables make up increasingly larger portions of supply stacks in markets across the world, numerous pricing drivers have changed – permanently.

Yet, many production cost model-driven fundamental forecasts still suffer from a backwards-looking paradigm. Legacy models assume perfectly optimized gas units usually set the marginal price, and so inexorably increasing gas prices keep the market price of power rising. In reality, wholesale power prices will be flat or declining as renewables displace thermal supply and renewable curtailment occurs increasingly often.

As renewables continue to make up larger percentages of supply stacks, the dynamics of this shift will only become more pronounced. To thrive in this environment, energy market stakeholders need a sophisticated, high-resolution forecast grounded in the new realities of power markets.

The Ascend Opportunity Cost Forecasting Framework (OCFF) was designed specifically to reflect the new market dynamics of modern power markets, thus ensuring that energy market stakeholders receive accurate, defensible, and bankable forecast outputs. In contrast to legacy production cost models, the OCFF considers that price formation from opportunity cost bidding behavior more accurately reflects true power market prices and price volatility. The OCFF also leverages hourly and sub-hourly analytics, coupled with an economic lens, to provide far more granular and defendable fundamental forecasts than those delivered by traditional models.

While opportunity cost considerations are an essential part of the OCFF, they are also only one piece of the larger forecasting framework. As shown in Figure 1, the OCFF contains the same core elements as those found in standard energy price formation forecasts, in which macro and policy assumptions drive capacity expansion, which in turn drives price formation and ultimately forecast outputs.

Even though the OCFF shares structural similarities with standard price formation forecasts, it differs from legacy approaches in a number of significant ways. Four crucial differentiators include the guiding principles that Ascend uses, shown at the bottom of Figure 1, to anchor all forecasting.

The OCFF also accounts for important power market realities in ways that standard production cost models do not. While many forecasts use purely economic models to guide capacity expansion, Ascend incorporates a granular approach to modeling that captures the fundamental market dynamics – economic and non-economic alike – essential to successfully navigating rapidly evolving energy markets. As summarized in Table 1, these dynamics include the need to enforce long-run equilibrium, weather's profound impact on price formation, volatile pricing dynamics associated with increasing renewable penetrations, projected climate/RPS policy and stakeholder demand for clean energy, as well as considerations related to cost of land and its impact on locational price dynamics.

As load growth surges in energy markets across the world, and numerous project developers compete to provide supply to meet demand, rational investments will converge markets towards an equilibrium between the locational cost of new entry and locational project value. Premium locations cannot stay premium. Thus, all forecasting aspects must align to a world constrained by long-run equilibrium.

Forecasts that fail to account for long-run equilibrium lead to undefendable valuations that are incompatible with the competitive markets that arise from the abundance of project development activity that exists today.

Ascend's forecasts adhere to long-run equilibrium, which ensures that resources can only earn normal returns in the long run, since supernormal returns would drive market entry and subnormal returns would drive retirement or deter entry. Long-run equilibrium modeling shows significant increases in renewable penetration and storage buildout as their costs continue to decline in the medium- to long-term future. In the long run, the OCFF ensures that revenue stacks do not exceed normal returns, with equilibration timing that varies by market. Consequently, Ascend's forecasts ensure that total projected revenue stacks align to capital expenditures (CapEx) for each asset class, including forecasted changes in CapEx over time.

Historically, weather was primarily a factor in energy demand, such as a heat wave driving broad air conditioner use. In today’s energy landscape, weather serves as the essential underlying driver for both demand and supply, and thus plays an increasing role in driving price formation. As renewable penetration increases, energy prices decline, as shown in Figure 2. In markets like CAISO or ERCOT, renewables and storage already set prices in energy, capacity, and ancillary markets. This dynamic will become – and is increasingly becoming – apparent in other US markets as renewable penetration accelerates.

Traditional production cost model-based forecasts often use average conditions or 'typical' weather years. This approach underpredicts price volatility, overvalues renewable resources, and can severely undervalue storage. Models that do not account for underlying weather at an hourly or sub-hourly level can also lead to decoupled price and generation simulations with inflated capture rates that ignore price depression when renewable production is high. Miscorrelating independent price and generation time series can lead to overvaluation of renewable resources: average price and generation shapes are not accurate proxies for generation-weighted prices. In reality, most renewable projects will see declining capture rates as renewable buildout grows. Ultimately, an inflated and biased price forecast will lead to an inflated and biased project valuation.

Uniquely, Ascend simulates weather as the new fuel that drives renewable generation, load, outages, prices, opportunity costs, and capture rates, accounting for the impact of weather on both demand and supply. The Ascend OCFF ensures that prices are represented as a function of net load (load less renewables) in which weather determines both supply and demand while renewable generation displaces higher-cost thermal generation. Price extremes will be driven by renewable generation: the highest highs will occur when renewable production is lowest, and the lowest lows will occur when there is surplus renewable generation. Zero and negative prices will become increasingly common. Ascend's forecasts reflect declining heat rates as renewable penetrations increase, and calibrate negative price formation with observed market behavior to produce price forecasts that align most closely to the realities of energy markets with high renewable penetration.

In renewables-heavy markets, unpredictable weather and intermittent resources drive uncertainty and opportunity cost decisions, leading to price volatility that is typically much higher than what traditional production cost models predict. Because storage and other flexible generation resources respond very differently to volatile prices than to flat prices, volatility must be both calibrated and forecasted appropriately in order to properly value these assets. Near-term volatility should be consistent with observed market behavior. Long-term volatility should be forecasted based on fundamental driving forces.

Typical production cost models optimize thermal dispatch around known load and renewable generation profiles. This approach results in over-optimized models with volatility that does not reflect what actually emerges in power markets. Failing to intentionally model volatility leads to models that are inconsistent with the market and irrelevant for valuation of storage and other flexible assets, often undervaluing storage and overvaluing renewables.

Grounded in observed market behavior, the OCFF reflects uncertainty and opportunity costs in price formation. In addition to modeling day-ahead (DA) volatility, Ascend simulates real-time (RT) prices and models the impact of renewable and storage buildout on RT price dynamics and volatility. Thus, Ascend's forecasts often contain price volatility that is higher than that predicted by traditional production cost models, but far more reflective of the realities of the market, as shown in Figure 3.

In power markets across the world, clean energy policy and corporate offtake demand have already emerged as significant driving forces for clean energy deployment.

Yet many forecasts rely on 'status quo policy' assumptions that fail to account for policy evolution and offtake demand, leading to underprediction of renewable buildout, and thus higher prices and lower volatility. Similarly, models that assign a zero value to renewable energy credits (RECs) lead to indefensible forecasts that dismiss or minimize corporate interest in clean energy supply.

Rather than relying on ‘status quo policies,’ which are certain to be incorrect, the Ascend OCFF incorporates assumptions about anticipated state- and federal-level clean energy policy evolution in base case forecasts. Ascend also adds a select amount of non-economic renewable generation into forecasts to reflect anticipated offtake demand and willingness to pay for renewable resources, since corporate offtake demand and ESG factors drive clean energy deployment beyond what an economic model alone would predict. In doing so, Ascend effectively assumes that RECs have a value above zero, reflecting the desire for offtakers to contract with clean energy.

During an energy transition, locational price patterns will be driven by variation in renewable resource quality as well as land cost. Permanent differences in climate and geography create permanent differences in renewable resource potential, population density, and cost of land, which affect the ability to develop projects and the resultant cost of energy, as illustrated in Figure 4. While the alignment between population density and price is not perfect due to differences in solar resource and transmission constraints, more dense and higher-cost areas generally show higher prices relative to less populated areas. New transmission build will only incentivize more project development in lower-cost areas until the price differentials once again reflect the underlying differences in cost of production. High population density and high cost of land create perpetual barriers to new development.

Many production cost models fail to account for locational cost of production, ignoring rational and realistic siting behavior for developers of new projects. This approach leads to underestimates of basis risk and locational premiums.

The OCFF analyzes each market regionally based on geospatial barriers in order to produce granular views of locational price patterns. The Ascend model also enforces compression within self-similar regions over time, as well as maintaining differentiation over time between regions with geospatial barriers between them.

Near-term projections can only be accurate to the extent that the near-term future is knowable. Consequently, Ascend's forecasts intentionally and philosophically align to market-traded forwards, as those reflect the best-known information about the near term. If it were easy to know whether the market was wrong, betting against the market would be free money and a forecaster should be doing so rather than selling forecasts. In the long term, Ascend's forecasts focus on the most important drivers of uncertainty and risk by appropriately modeling the key policy, economic, and physical constraints that govern capacity expansion and dispatch, all while ensuring a view that enforces long-run equilibrium.

Ascend prioritizes accuracy over precision in the long term: while no forecast is perfect, it should be defendable and align to a most probable future that accounts for the likely decisions and motivations of market participants and stakeholders. While forecast accuracy is weather-dependent and can vary widely with accuracy in the traded market forwards, Ascend’s valuation tools and forecasts are continuously calibrated to reflect realizable revenue in operating assets.

In assessing how well the OCFF performs in forecasting the price formation outputs seen in Figure 1, Ascend considers 'directional correctness' to be the most appropriate signal for 'accuracy' (since Ascend's forecasts are necessarily tied to the market, and thus can only be as accurate as the market). Ultimately, the OCFF has consistently proven to be directionally correct in modeling a number of market dynamics, including the evolution of price dynamics for ancillary services, long-run on and off-peak forwards, price shapes, capacity prices, and DA and RT price volatility. The ability to model these market dynamics demonstrates the effectiveness of the model overall, lending fidelity and clarity to the many other analytic models it informs, as well as credibility to efforts around project development, project finance and due diligence, power procurement, and M&A.

Ascend also has consistently and correctly anticipated the evolution of clean energy policy at both the federal level and in numerous American states, illustrating the importance of forecasting based on anticipated changes rather than status quo policy.

Ascend ancillary service price forecasts explicitly consider that storage resources are so well-suited to providing ancillary services that they will quickly saturate the markets and set energy prices as their deployment grows. Because batteries have many idle hours, opportunity costs in these intervals are close to zero, depressing ancillary prices.

In the near term, Ascend’s ancillary forecasts are informed by ancillary market forwards (where available) and historical pricing dynamics (for markets not yet saturated by storage). As ancillary markets saturate with storage, Ascend expects ancillary service prices to reflect the opportunity cost to storage of not providing real-time energy arbitrage within a given time interval. Thus, prices will be highest during periods of high expected RT price volatility, and lowest during periods of low expected RT price volatility. Providing ancillary services will offer only a slight revenue uplift, offsetting the increased risks and complexity of optimizing battery operations across both energy and ancillary markets.

Using the OCFF, Ascend anticipated (and warned investors about) the declining value of ancillary services in battery-heavy markets. Figure 5 shows the ancillary price saturation that has already occurred in CAISO and ERCOT, which Ascend predicted several years before it happened.

The Ascend approach for forecasting monthly on/off-peak forwards specifically accounts for the two primary ways that renewable penetration drives price depression: by shifting the supply stack, and through negative price formation during surplus renewable generation. As renewable penetration rises, the shifting of the supply stack drives general price depression while reflecting steeper supply stack slopes at periods of high demand than at periods of low demand.

Ascend fundamental modeling accounts for changes to the marginal generation unit as renewable penetration rises. In general, minimal to no curtailment occurs at renewable penetrations below 10-20%, slowly rising curtailment and frequency of negative prices occur as renewable penetrations rise to ~40%, and a rapid increase in curtailment and negative prices occurs at renewable penetrations above ~40%. As renewable curtailment becomes increasingly common at high renewable penetrations, zero/negative prices will accordingly weight the average prices.

Ascend uses relationships derived from market fundamental modeling for these price depression mechanisms to account for heat rate depression and negative price formation. Ascend also incorporates the impact of storage by modeling the ability of storage to absorb surplus renewable generation. Hourly, monthly, and seasonal variation in renewable generation and load shapes provide a more granular basis for forecasting the impacts of renewable curtailment by peak period, month, and year.

A powerful example of the importance of capturing new market dynamics is reflected in the OCFF model’s ability to accurately forecast that solar deployment would cause CAISO on-peak prices to drop below off-peak prices (and Ascend warned investors about continued declines in solar-weighted prices), as shown in Figure 6. CAISO on-peak prices have been depressed by solar deployment, while off-peak prices remain driven by gas and carbon prices. Ascend has been forecasting the mid-2020s inversion of on- and off-peak prices since 2020, well before the inversion appeared in market forwards. The inversion has moved earlier, with rising gas and carbon prices lifting the off-peak, and rising REC prices driving mid-day prices more negative and reducing the on-peak.

In an energy transition, price shapes become increasingly dependent on load and renewable generation profiles that vary with weather. Production cost models that do not account for weather, or that use 'average' weather, will often miss important price dynamics and variability in price shapes.

At Ascend, price shapes are forecasted at the monthly level, providing 24-hour price shapes. The Ascend price shape forecast uses fundamental modeling that incorporates evolution in load shape. Depending on the energy market, this evolution may be driven by such elements as forecasted electric vehicle adoption, building electrification, energy efficiency, behind-the-meter solar and storage deployment, and changes to renewable generation deployment. Additionally, the OCFF accounts for the impact of structural changes in the net load shape (such as the net load ramp rate) that also affect price shapes.

Using the OCFF, Ascend predicted that ERCOT summer price shapes would push the highest prices into sunset hours and exhibit a double-peak in some months, unlike the simpler duck shape in CAISO. As shown in Figure 7, ERCOT developed a double peak in July 2023 with declining load causing an initial price drop from an afternoon peak, followed by a second price peak as solar generation declined, before price declined again as load continued to drop.

Ascend capacity price forecasts assume that the marginal new capacity unit will increasingly be a storage resource. Depending on the market, this assumption is based on renewable policy mandates, stakeholder opposition to the construction of new thermal resources, low capacity values for wind and solar generation, and difficulties in financing or receiving regulatory approval for new thermal capacity due to stranded asset risk.

In the near term, Ascend also considers the impact of expected retirements of thermal capacity due to age and economic pressures as well as the amount of storage in the interconnection queue. In the medium- and long-term future, Ascend forecasts capacity prices based on the expected Net cost of new entry (Net CONE) of new resources while also accounting for increasing duration requirements for storage as storage deployment increases.

Ascend anticipated that storage would become the primary new unit entry for capacity and begin to drive capacity prices, beginning in locations with clean energy mandates. Storage has been driving bilateral capacity prices in California since about 2020, and New York recently designated two-hour storage as the reference unit in its capacity market, aligning to Ascend’s prediction that the Natural Gas Combustion Turbine would be displaced as the reference unit.

While renewables reduce the average price of energy, the intermittency of renewable output drives increased volatility of prices due both to the variability in weather and the uncertainty in renewable production across multiple timescales. In general, growing volatility is observed with growing renewable penetration both in RT and DA markets year-over-year. Ascend uses a variety of custom metrics to forecast RT and DA volatility.

Real-time markets generally have higher volatility than DA markets, with RT prices more volatile because forecast errors must be adapted to on short notice. Higher RT volatility can add 50% more revenue (or more) for batteries and other flexible resources, as seen in Figure 8. Thus, volatility must be modeled accurately at both the DA and RT levels. Ascend forecasts DA and RT volatility based on fundamental driving forces in order to model future value for storage and other flexible resources.

By reflecting uncertainty and opportunity cost in resource bidding and dispatch behavior, as well as by calibrating volatility against historical dynamics, Ascend predicted increasing price volatility in renewables-heavy markets, as shown in Figure 3. Grounded in the realities of the energy transition, Ascend's ability to reflect observed market volatility and forecast it based on underlying driving forces is critical for defendable valuation of flexible assets.

As noted previously, Ascend incorporates assumptions about anticipated energy policy evolution in base case forecasts, going beyond the unrealistic forecast scenario of only considering currently enacted policies. While policy evolution is uncertain, the least likely future would hold all policy as status quo.

Ascend assesses policy outlooks at both the state and federal level to anticipate the most likely developments for clean energy policy. These assessments could include making clean energy goals more or less aggressive in terms of timelines or absolute targets, extending or sunsetting existing clean energy incentives, offering outlooks for carbon pricing, and accounting for potential tariffs.

Ascend has anticipated tightening clean energy standards in numerous states. Prior to being enacted (or even introduced in state legislatures), for example, Ascend predicted clean energy/zero emission mandates in Illinois, Minnesota, Michigan, Colorado, Oregon, Washington, Vermont, Rhode Island, Delaware, and Maryland. Additionally, Ascend anticipated that California would accelerate its clean energy timelines and adopt more aggressive interim emissions targets. At the federal level, Ascend was already assuming extensions to the clean energy production tax credit and investment tax credit prior to the passage of the Inflation Reduction Act. As a result of these anticipated policies, Ascend’s forecasts were able to retain continuity despite a changing policy environment.

In searching for the right forecast, good and prudent investors should seek out what they don’t want to hear. Not every investment will be a good one, and not everyone can be above average. Investors should also have a clear understanding of the realities of today's energy markets. Prices can’t keep climbing when renewables are setting prices. Projects can’t earn supernormal returns indefinitely when participants respond to incentives and drive equilibrium. Valuations for renewables and storage will often be in opposition: the generation surpluses that drive value for storage suppress value for renewable generation.

While no long-term forecast is perfectly accurate, Ascend’s opportunity cost forecasting framework consistently identifies numerous critical driving forces and market dynamics that inform investment in rapidly changing power markets. The Ascend OCFF provides a powerful, high-resolution analytic lens that produces bankable, defendable energy market forecasts that align to a most probable future.

Trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments, AscendMI™ (Ascend Market Intelligence) leverages the OCFF to deliver proprietary power market forecasts that reflect the new market dynamics driving the energy transition.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

.avif)

.avif)

-1-ercot%20image.avif)

%20(1).avif)