Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

This publication is the fourth in a series from Ascend Analytics that considers the implications of rapid load growth on US capacity markets, sky-high capacity prices as the new normal, the risks that new realities create for business-as-usual strategies, and the opportunities that this paradigm shift enables for well-planned new entry resources.

For much of the past decade, energy storage has been viewed as a promising but ultimately peripheral player in capacity markets outside of California. Despite being flexible, usually emissions-reducing, and dispatchable, storage had historically struggled to gain traction without state-level procurement mandates. A confluence of forces is now reshaping the capacity opportunities for storage. Load growth, which was once predictable and modest, is now uncertain and aggressively accelerating just as gas capacity is experiencing supply shortages and price increases. In this context, storage is emerging not just as a complementary resource, but as a potential cornerstone of future capacity strategies.

In the absence of substantial load growth, recent markets have generally been oversupplied by legacy thermals, and further supported by the high capacity contribution of early-entrance solar. In this context, there just was not much need for new capacity resources in US power markets, which produced correspondingly low prices in capacity markets. Moving into the mid-2020s, the narrative has shifted dramatically.

A confluence of forces is now reshaping the capacity landscape for storage. Load growth, which was once predictable and modest, is now uncertain and aggressively accelerating. This rapid rise is being driven by data center expansion, electrification, and extreme weather conditions. In previous eras of load growth, the solution was to identify the most cost-effective thermal technology and build gigawatts of that single resource type. During the 1970s, load growth was powered largely by new coal-steam, whereas in the early 2000s growth was largely powered by new natural gas combined cycles.

However, in this new era of load growth, the luxury of choosing a single 'best' resource is fading. ISO interconnection queues are populated with projects that were planning for decarbonization amid minimal peak load growth. Storage and renewables were ideally suited for that scenario, and low expected capacity factors for thermal generation in that world made new gas a more difficult proposition than it appears today. This leaves interconnection queues with few mature thermal projects and has driven a turbine demand surge beyond what manufacturers had planned for.

Moreover, the economics of thermal generation are under pressure from the implications of that demand surge. The cost of a new gas turbine has tripled over the past few years. Gas supply constraints, ongoing regulatory risks related to emissions standards, ongoing stranded asset risks, and capacity factor compression from increasing renewable penetration are all challenging the role for thermal assets in serving capacity needs. Meanwhile, the costs of storage have declined dramatically over the last decade. If storage can enter quickly at a price point competitive with the rapidly rising cost of natural gas turbines, it will find willing and able capacity buyers.

In this context, storage is emerging not just as a complementary resource, but as a potential cornerstone of future capacity strategies. For storage to expand beyond ERCOT and CAISO at scale, however, it must clear several critical hurdles:

From an economic standpoint, storage is increasingly competitive with traditional thermal assets. In all US markets, battery storage can now compete with capacity market bids from new natural gas combined cycle (NGCC) plants, particularly when accounting for rising turbine and fuel costs for thermal developers. More strikingly, storage now underbids simple-cycle natural gas combustion turbines' (NGCTs) capacity revenue needs in every summer-peaking market. While NGCTs have long been the go-to solution for peaking capacity, their shrinking capacity factor and high marginal costs make them less attractive in markets where storage can respond faster, provide ancillary services at lower costs, and monetize the increasing curtailment and wholesale price depression from surplus renewables.

This growing economic edge is reinforced by a steady decline in storage costs, which continues to strengthen the case for storage as a core capacity asset. Since 2022, all-in project costs for battery storage have fallen by roughly 20%, despite persistent inflation in labor and materials, as well as the inflationary impact from rising labor and interest rates. Battery cell prices alone have dropped from $151 per kWh in 2022 to below $100 per kWh in 2025 for the cheapest cells. These cost declines are not just making storage cheaper: they are enabling storage usage in new areas and expanding its capabilities. New storage is no longer only being designed for short-duration arbitrage and ancillary services. Longer-duration systems, including 6-hour and potentially even 8-hour configurations, are now financially viable in some markets, enabling storage to meet both daily peaks and overnight demand profiles.

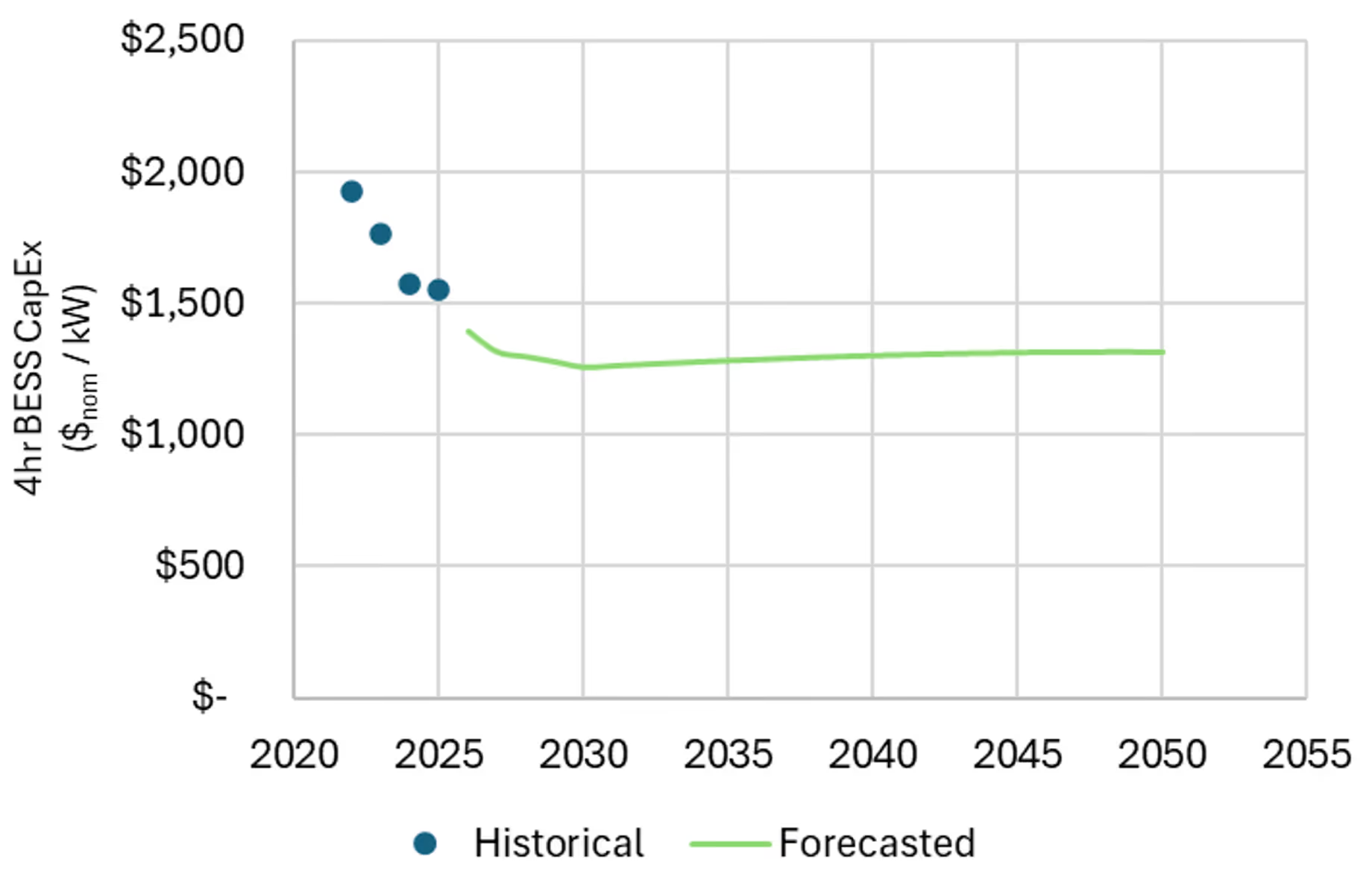

At the same time, policy support remains a critical tailwind as much of the learning curve for storage has been actualized (Figure 1), and storage may struggle to out-innovate new inflationary pressures and supply restrictions. The preservation of the Inflation Reduction Act’s storage ITC in the recently passed One Big Beautiful Bill Act (OBBBA) represents an approximate 26% savings in project Gross Cost of New Entry (CONE) that will persist for projects coming online into the late 2030s. A repeal of that credit, as was proposed in early versions of the bill, would have undone years of learning curve.

While the underlying costs for storage are declining, rising costs for traditional thermal generation are further strengthening the case for storage and are enabling earlier entry of storage into markets with lower renewable penetration. Order books for new gas turbines are filled through the end of the 2020s, and demand from data centers is becoming increasingly insensitive to price in the near term. As a result, the cost of a frame combustion turbine has climbed sharply, with recent projects reaching as high as $2,700 per kW, compared to less than $1,000 per kW just a few years ago, as shown in Figure 2. At the same time, markets are beginning to shorten the expected economic lifespan of these assets. State, utility, and corporate decarbonization goals are increasing the risk of stranded investments and are pushing developers to seek faster payback periods, which in turn drives gross CONE even higher for new gas.

These dynamics are also unfolding within the broader context of deepening renewable penetration, which is fundamentally reshaping the economics of thermal generation. As renewables serve a growing share of load, thermal assets are running at lower capacity factors and with smaller wholesale energy margins, forcing fixed and variable costs to be recovered over a shrinking operational window. The dilution of thermal value is also occurring during system peak gross-load hours. In markets such as ERCOT, solar has contributed as much as 35% of its nameplate capacity during peak load, significantly reducing the need for peaking units and narrowing the summer net-peak to a shorter duration that is increasingly well suited to storage. Markets are also increasingly accounting for winter peak forced outage risks for both turbines and their fuel supply and are reducing capacity accreditation for thermal generation accordingly. This shift is expected to compress margins for traditional peaking turbines and alleviate the decreases in capacity accreditation that storage experiences with growing storage penetration.

In contrast, storage benefits from the integration of renewables. It can access low-, zero-, and negative-cost charging energy during curtailment hours and capture value by discharging during short-lived volatility events created by steep renewable-induced system ramps. The result is a revenue outlook where storage assets can achieve higher merchant net margins than gas assets and can outcompete thermal resources in the capacity market even when gross CONE is comparable. Figure 3 illustrates capacity market revenue needs by asset class for PJM in 2030. While all new resources are more expensive than the previous reference NGCT unit, both 4-hour BESS and 100-hour long-duration storage outcompete new entry NGCTs and are competitive with new entry NGCCs.

The economic rationale behind the inclusion of storage in the next waves of new unit entry is consistent across US markets. However, the starkness of the conclusions depends on the extent to which renewable penetration has eroded thermal value and accentuated the energy arbitrage value of storage.

In California, the case for storage has been and will continue to be clear. CAISO has surplus mid-day solar, a significant carbon allowance cost, a near guarantee of forced thermal retirement, and a load shape that avoids the rapid erosion of capacity accreditation associated with winter peaking. In the Midwest, the supply of strong renewable resources positions some storage to enter SPP, MISO, and western PJM, even without the political support of market-wide 100% clean-energy goals. In NYISO and ISO-NE, however, the economic conclusion for storage is in doubt without policy support. The same challenges that make it difficult and expensive for solar, onshore wind, and offshore wind to enter these markets trickle down to create a corollary challenge to storage economics. Without renewables to create curtailment and arbitrage opportunities for storage, the low storage capacity accreditation (due to wider winter-peak load shapes) puts these markets in a position where they must choose between new expensive fossil fuel and new expensive, but green, long-duration storage capacity.

While storage is becoming increasingly cost-competitive, its ability to scale as a capacity resource depends heavily on market design. The way capacity markets procure, price, and contract for reliability will ultimately determine whether storage can find the long-term revenue certainty that allows it to attract the low-cost capital it needs to be economically competitive.

Long-term capacity offtake agreements are not strictly required to support new entry, but they are a powerful enabling tool. These contracts provide the revenue predictability that developers and financiers need to support capital-intensive projects. However, US capacity markets are moving away from this structure. ISO-NE, which previously offered seven-year price-lock commitments, now provides only one-year contracts due to a FERC ruling that the lock-in process was price-suppressive and discriminatory.1 This exposes new resources to year-over-year uncertainty and volatility in clearing prices, accreditation levels, and the risk of not clearing the market at all. This short contract duration makes it difficult to secure financing, especially as accreditation methodologies change, performance metrics shift, and political interventions can alter market rules midstream. A recent example is PJM’s change in accreditation for storage and gas CTs in response to winter reliability concerns. As shown in Figure 4, accreditation values dropped significantly between two recent auctions. In the subsequent auction, PJM imposed a price cap below the expected clearing level to keep ratepayer costs down, further limiting participants’ ability to recover expected revenues.

For developers and investors, this kind of regulatory uncertainty undermines confidence in the long-term cash flow stability that is needed to service debt. Markets that change the rules midstream not only affect near-term revenues but also reduce trust in the market’s ability to deliver predictable outcomes. This increases the hurdle rate for new entrants and slows the pace of new capacity development. In contrast, CAISO’s bilateral resource adequacy framework allows load serving entities to contract for capacity over longer terms. As a result, most new resources in California enter the market with 10- to 15-year contracts. While similar long-term contracting is possible in other markets, it remains less common despite its value as a hedge in the capacity markets. Expanding this practice could significantly reduce risk and lower the cost of new capacity. As capacity prices rise, the justification for long-term contracts through retail load offtake structures or state subsidies will grow. Calls for this change have already begun in PJM2.

Not all capacity market changes are problematic, though. As grids evolve, it is appropriate to adjust how a resource’s contribution to reliability is measured. Early storage projects deliver more value when the system peak is narrow, while later entrants have diminishing reliability contributions as the net load curve flattens. The decline in peak load contribution sets an economic peak penetration of a given duration of storage. As markets decarbonize or transition to a winter peak-load, there will eventually be an ELCC and project cost where it would be preferential to develop a longer-duration storage facility or a dispatchable natural gas asset instead of multiple 4-hour storage systems, as illustrated in Figure 5, which shows Ascend’s forecasts of 4-hour storage ELCC by market. Further complicating the tradeoffs, cost concentrations in transmission upgrades and power electronics combined with energy arbitrage revenue concentrations in short-duration price spikes make both project cost and project value non-linear with additional duration.

When capacity is only procured one year at a time, developers face uncertainty around when and by how much ELCC will decline, and this uncertainty impacts the design and financeability of projects, contrasting with the stability provided by long-term contracting. While ELCC will naturally decline in steps as markets periodically review accreditation, the timing and magnitude are difficult to predict. MISO’s ELCC evolution illustrates this risk. The modeling currently used by the ISO is inconsistent with other markets, and assuming that MISO is not fundamentally different than other regions, the risk of ELCC re-normalization is both large and probable. Long-term offtake agreements, whether capacity-only or tolling/lease-style, can help bridge this uncertainty. The risk transfer in these contracts allows buyers to lock in favorable terms below the cost of spot capacity prices, while sellers gain the revenue stability needed to finance new projects.

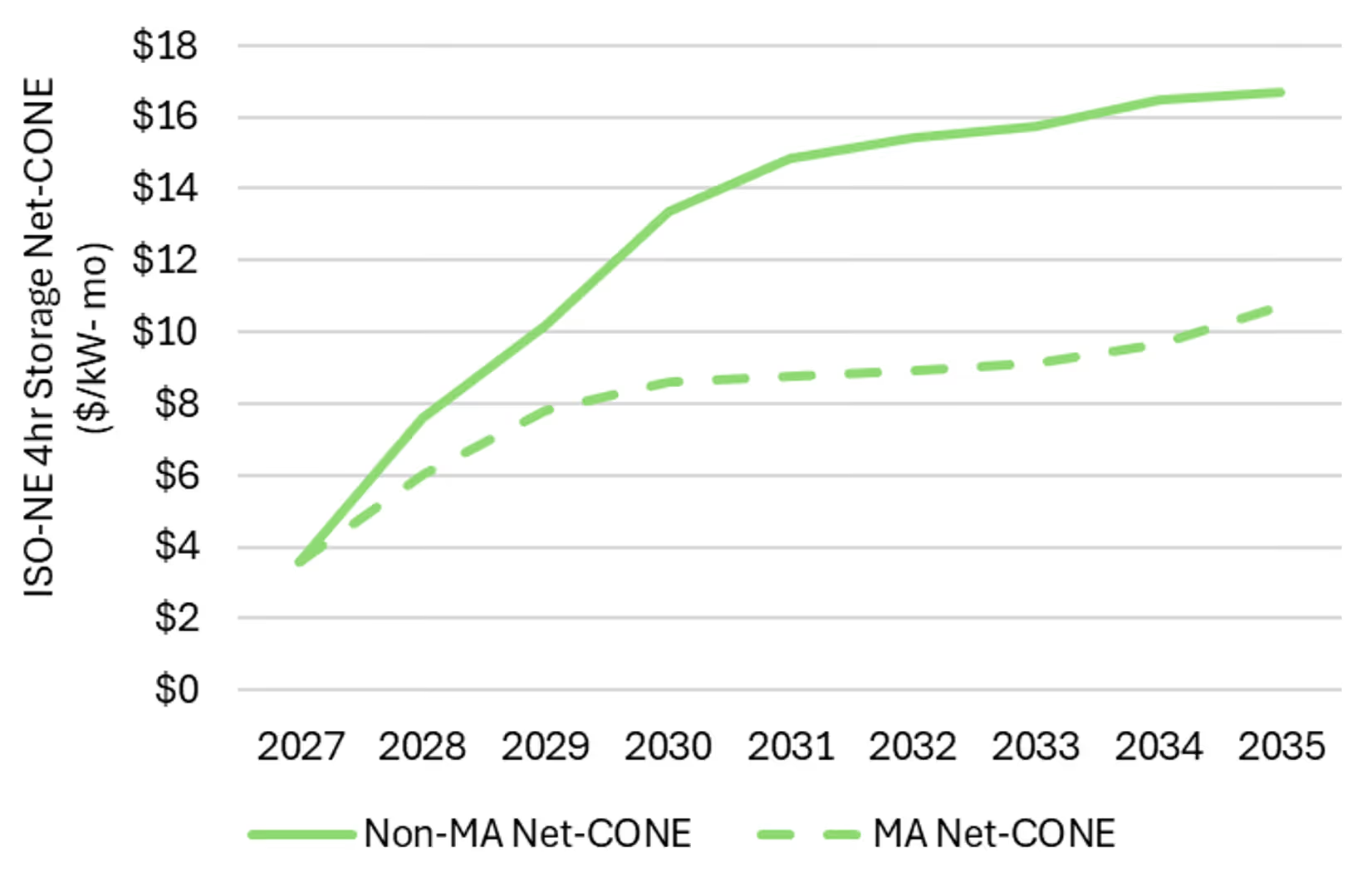

Capacity prices in a market with significant load growth will structurally and necessarily price at the Net Cost of New Entry (Net CONE), which is the gross cost of new entry less any energy and ancillary operating revenues. The forcing functions behind this conclusion are discussed at length in Part I of this capacity market series, but costs to consumers do not necessarily have to skyrocket, as discussed in Part II of this series. Markets, states, utilities, and consumers have the ability to shape outcomes through targeted incentive programs that reduce the Net CONE of new capacity, with a focus on storage in locations with clean energy policies. These programs can shift the economics of new entry without distorting reliability outcomes or providing a windfall to the entire remaining supply stack. For example, the settlement mechanism in New York’s Index Storage Credit turns storage into a capacity market price taker and guarantees that the revenues of a storage project will reach a designated strike price independent of capacity prices or wholesale energy arbitrage results. This design ensures that capacity prices only rise if load growth exceeds the program’s support capacity. Similarly, Massachusetts’ Clean Peak Standard provides a revenue adder for clean energy delivered during peak hours, thus significantly lowering Net CONE for participating clean resources without subsidizing legacy fossil generation. As a result, Net CONE for storage in Massachusetts is materially lower than in the rest of ISO-NE, as shown in Figure 6.

Importantly, these subsidies can reduce capacity market costs by significantly more than the cost of the subsidy itself. Every unit that clears the capacity auction is paid the clearing price: therefore, reducing the cost of the marginal new entry unit saves capacity costs (and reduces capacity revenues) not just for the new unit but for the entire remaining capacity supply stack. Moreover, because the missing money for a given capacity resource gets divided by the ELCC to determine its needed capacity price, the impact of subsidies becomes further amplified by the ELCC of the subsidized resource.

Storage, in particular, offers a cost-effective target for subsidy, because of its relatively low ELCC. In PJM, for example, because the 2026-27 auction models a 50% ELCC for 4-hour storage, every dollar of subsidy to storage will reduce the capacity market Net CONE by two dollars, when storage sets the price. A subsidy to an NGCC, which carries an ELCC rating of 78%, by contrast, will reduce its capacity market Net CONE by $1.28 per dollar of subsidy when an NGCC sets the capacity price. Figure 7 shows the implications that a $25/kW-yr strategic subsidy could have on a 2030 capacity market clearing price. Without subsidies, the capacity price will grow to six times its historically normative level. In a scenario where new entry is required to meet load growth that is 50% above current levels, a $25/kW subsidy would reduce total capacity market costs by 28% (including the cost of the subsidy). Breaking that savings down further, the market clearing price (paid by all load) would be reduced by $53/kW-yr though a subsidy that would cost the average ratepayer $12/kW-yr.

Every market in the US will see large-scale deployment of storage between now and the end of the 2020s. Current economics and politics have positioned storage as the most viable solution to serve new load and to manage the impact of new load on ratepayers.

However, the ability of storage to economically enter into a market today does not guarantee that storage will be the long-term definitive solution for a market's future capacity needs. In the same way that high turbine costs, falling Li-Ion battery costs, and rapid load growth have opened a door to storage as a capacity resource, falling turbine costs and flattening net load peaks will close the door to storage over time.

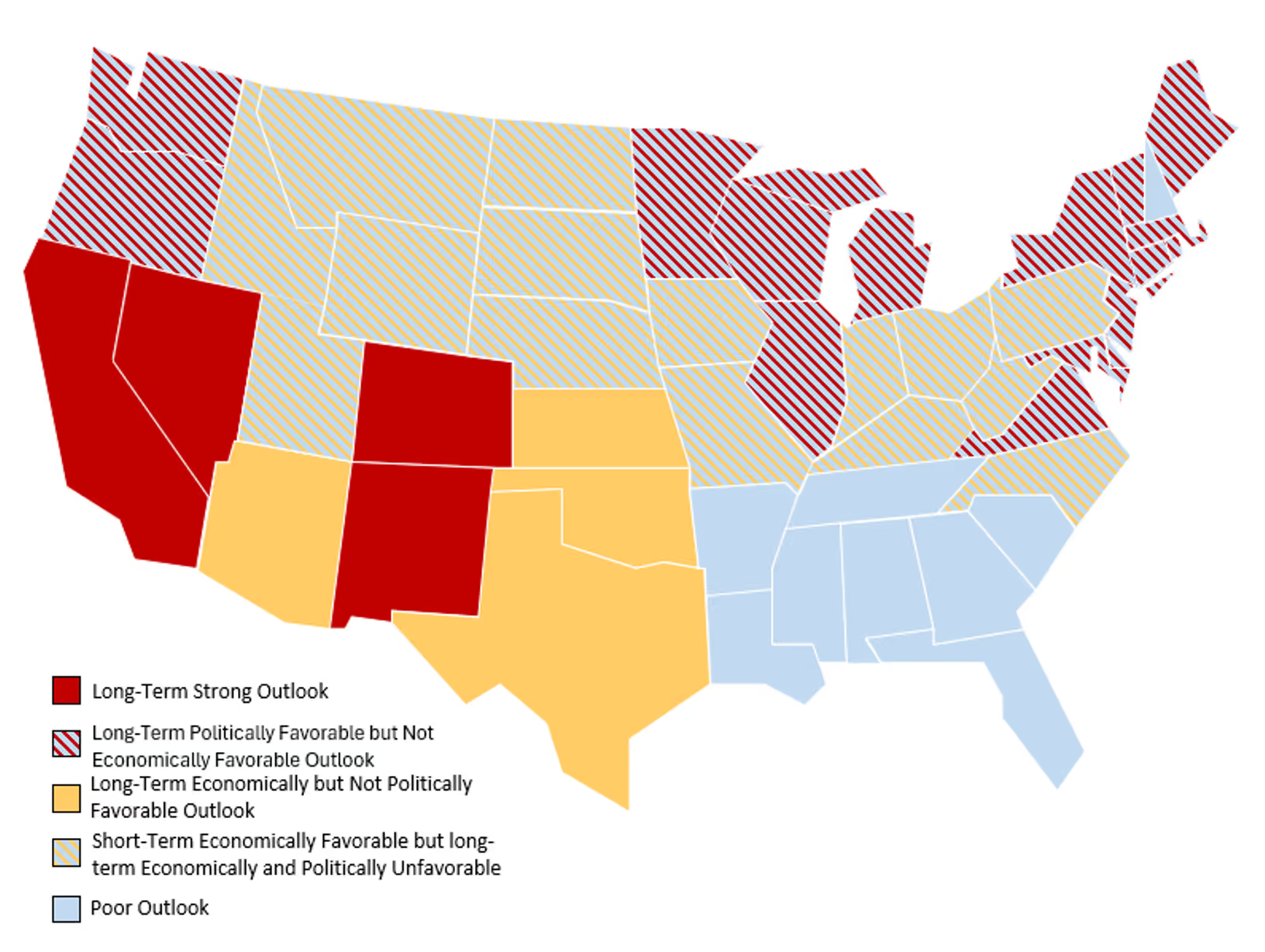

In that context, three factors jointly determine long-term storage prospects:

A summary of how these factors manifest by state is shown in Figure 8 below.

As storage becomes a broadly viable capacity option, navigating the opportunities and risks will require a balanced view that accurately captures the key dynamics shaping energy markets now and in the future.

_____________________________________

1 FERC Order on New Entrant Rules

2 FERC's Christie calls the need for more gas-fired power 'a rendezvous with reality'

This publication is the fourth in a series from Ascend Analytics that considers the implications of rapid load growth on US capacity markets, sky-high capacity prices as the new normal, the risks that new realities create for business-as-usual strategies, and the opportunities that this paradigm shift enables for well-planned new entry resources.

For much of the past decade, energy storage has been viewed as a promising but ultimately peripheral player in capacity markets outside of California. Despite being flexible, usually emissions-reducing, and dispatchable, storage had historically struggled to gain traction without state-level procurement mandates. A confluence of forces is now reshaping the capacity opportunities for storage. Load growth, which was once predictable and modest, is now uncertain and aggressively accelerating just as gas capacity is experiencing supply shortages and price increases. In this context, storage is emerging not just as a complementary resource, but as a potential cornerstone of future capacity strategies.

In the absence of substantial load growth, recent markets have generally been oversupplied by legacy thermals, and further supported by the high capacity contribution of early-entrance solar. In this context, there just was not much need for new capacity resources in US power markets, which produced correspondingly low prices in capacity markets. Moving into the mid-2020s, the narrative has shifted dramatically.

A confluence of forces is now reshaping the capacity landscape for storage. Load growth, which was once predictable and modest, is now uncertain and aggressively accelerating. This rapid rise is being driven by data center expansion, electrification, and extreme weather conditions. In previous eras of load growth, the solution was to identify the most cost-effective thermal technology and build gigawatts of that single resource type. During the 1970s, load growth was powered largely by new coal-steam, whereas in the early 2000s growth was largely powered by new natural gas combined cycles.

However, in this new era of load growth, the luxury of choosing a single 'best' resource is fading. ISO interconnection queues are populated with projects that were planning for decarbonization amid minimal peak load growth. Storage and renewables were ideally suited for that scenario, and low expected capacity factors for thermal generation in that world made new gas a more difficult proposition than it appears today. This leaves interconnection queues with few mature thermal projects and has driven a turbine demand surge beyond what manufacturers had planned for.

Moreover, the economics of thermal generation are under pressure from the implications of that demand surge. The cost of a new gas turbine has tripled over the past few years. Gas supply constraints, ongoing regulatory risks related to emissions standards, ongoing stranded asset risks, and capacity factor compression from increasing renewable penetration are all challenging the role for thermal assets in serving capacity needs. Meanwhile, the costs of storage have declined dramatically over the last decade. If storage can enter quickly at a price point competitive with the rapidly rising cost of natural gas turbines, it will find willing and able capacity buyers.

In this context, storage is emerging not just as a complementary resource, but as a potential cornerstone of future capacity strategies. For storage to expand beyond ERCOT and CAISO at scale, however, it must clear several critical hurdles:

From an economic standpoint, storage is increasingly competitive with traditional thermal assets. In all US markets, battery storage can now compete with capacity market bids from new natural gas combined cycle (NGCC) plants, particularly when accounting for rising turbine and fuel costs for thermal developers. More strikingly, storage now underbids simple-cycle natural gas combustion turbines' (NGCTs) capacity revenue needs in every summer-peaking market. While NGCTs have long been the go-to solution for peaking capacity, their shrinking capacity factor and high marginal costs make them less attractive in markets where storage can respond faster, provide ancillary services at lower costs, and monetize the increasing curtailment and wholesale price depression from surplus renewables.

This growing economic edge is reinforced by a steady decline in storage costs, which continues to strengthen the case for storage as a core capacity asset. Since 2022, all-in project costs for battery storage have fallen by roughly 20%, despite persistent inflation in labor and materials, as well as the inflationary impact from rising labor and interest rates. Battery cell prices alone have dropped from $151 per kWh in 2022 to below $100 per kWh in 2025 for the cheapest cells. These cost declines are not just making storage cheaper: they are enabling storage usage in new areas and expanding its capabilities. New storage is no longer only being designed for short-duration arbitrage and ancillary services. Longer-duration systems, including 6-hour and potentially even 8-hour configurations, are now financially viable in some markets, enabling storage to meet both daily peaks and overnight demand profiles.

At the same time, policy support remains a critical tailwind as much of the learning curve for storage has been actualized (Figure 1), and storage may struggle to out-innovate new inflationary pressures and supply restrictions. The preservation of the Inflation Reduction Act’s storage ITC in the recently passed One Big Beautiful Bill Act (OBBBA) represents an approximate 26% savings in project Gross Cost of New Entry (CONE) that will persist for projects coming online into the late 2030s. A repeal of that credit, as was proposed in early versions of the bill, would have undone years of learning curve.

While the underlying costs for storage are declining, rising costs for traditional thermal generation are further strengthening the case for storage and are enabling earlier entry of storage into markets with lower renewable penetration. Order books for new gas turbines are filled through the end of the 2020s, and demand from data centers is becoming increasingly insensitive to price in the near term. As a result, the cost of a frame combustion turbine has climbed sharply, with recent projects reaching as high as $2,700 per kW, compared to less than $1,000 per kW just a few years ago, as shown in Figure 2. At the same time, markets are beginning to shorten the expected economic lifespan of these assets. State, utility, and corporate decarbonization goals are increasing the risk of stranded investments and are pushing developers to seek faster payback periods, which in turn drives gross CONE even higher for new gas.

These dynamics are also unfolding within the broader context of deepening renewable penetration, which is fundamentally reshaping the economics of thermal generation. As renewables serve a growing share of load, thermal assets are running at lower capacity factors and with smaller wholesale energy margins, forcing fixed and variable costs to be recovered over a shrinking operational window. The dilution of thermal value is also occurring during system peak gross-load hours. In markets such as ERCOT, solar has contributed as much as 35% of its nameplate capacity during peak load, significantly reducing the need for peaking units and narrowing the summer net-peak to a shorter duration that is increasingly well suited to storage. Markets are also increasingly accounting for winter peak forced outage risks for both turbines and their fuel supply and are reducing capacity accreditation for thermal generation accordingly. This shift is expected to compress margins for traditional peaking turbines and alleviate the decreases in capacity accreditation that storage experiences with growing storage penetration.

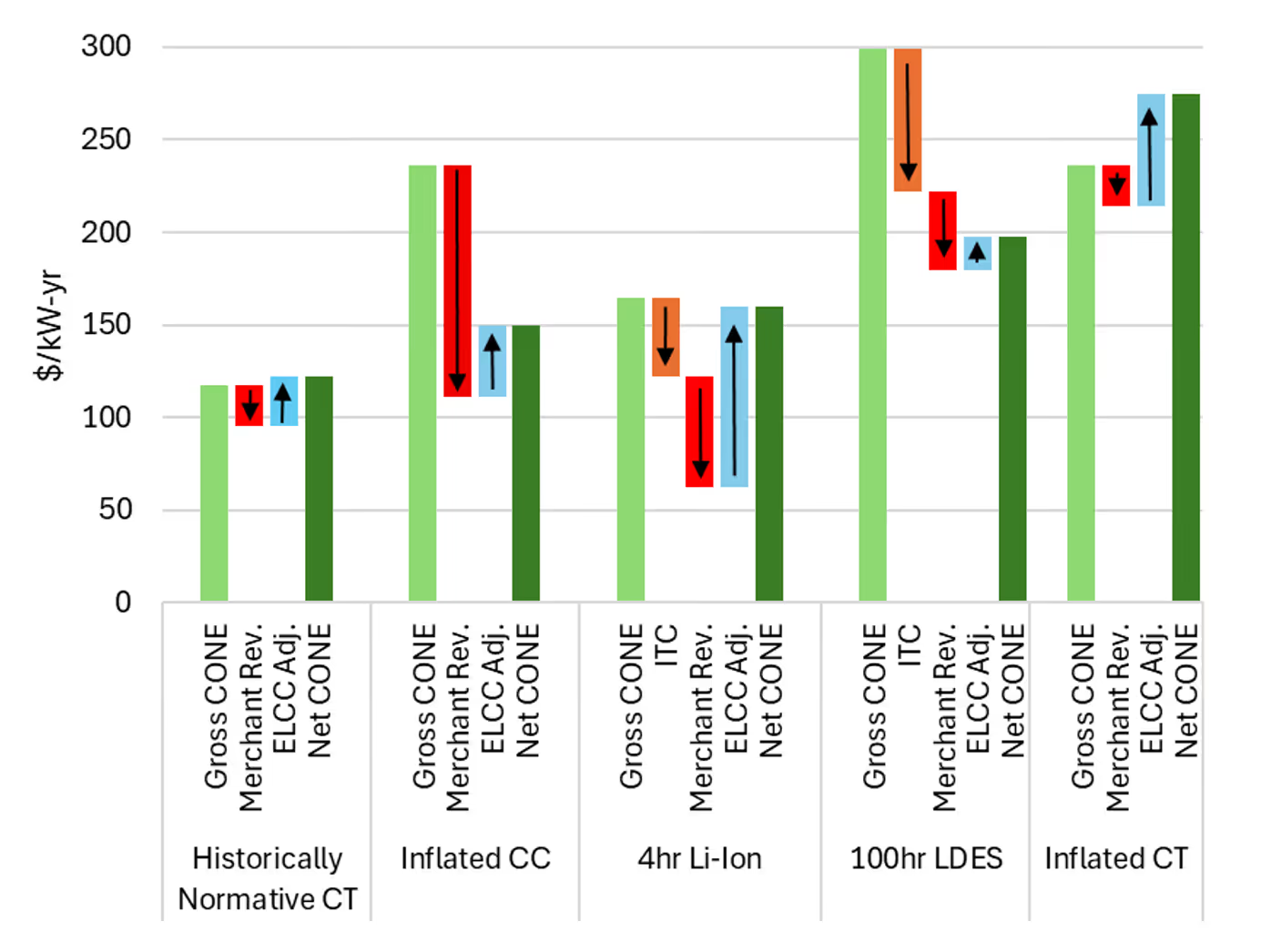

In contrast, storage benefits from the integration of renewables. It can access low-, zero-, and negative-cost charging energy during curtailment hours and capture value by discharging during short-lived volatility events created by steep renewable-induced system ramps. The result is a revenue outlook where storage assets can achieve higher merchant net margins than gas assets and can outcompete thermal resources in the capacity market even when gross CONE is comparable. Figure 3 illustrates capacity market revenue needs by asset class for PJM in 2030. While all new resources are more expensive than the previous reference NGCT unit, both 4-hour BESS and 100-hour long-duration storage outcompete new entry NGCTs and are competitive with new entry NGCCs.

The economic rationale behind the inclusion of storage in the next waves of new unit entry is consistent across US markets. However, the starkness of the conclusions depends on the extent to which renewable penetration has eroded thermal value and accentuated the energy arbitrage value of storage.

In California, the case for storage has been and will continue to be clear. CAISO has surplus mid-day solar, a significant carbon allowance cost, a near guarantee of forced thermal retirement, and a load shape that avoids the rapid erosion of capacity accreditation associated with winter peaking. In the Midwest, the supply of strong renewable resources positions some storage to enter SPP, MISO, and western PJM, even without the political support of market-wide 100% clean-energy goals. In NYISO and ISO-NE, however, the economic conclusion for storage is in doubt without policy support. The same challenges that make it difficult and expensive for solar, onshore wind, and offshore wind to enter these markets trickle down to create a corollary challenge to storage economics. Without renewables to create curtailment and arbitrage opportunities for storage, the low storage capacity accreditation (due to wider winter-peak load shapes) puts these markets in a position where they must choose between new expensive fossil fuel and new expensive, but green, long-duration storage capacity.

While storage is becoming increasingly cost-competitive, its ability to scale as a capacity resource depends heavily on market design. The way capacity markets procure, price, and contract for reliability will ultimately determine whether storage can find the long-term revenue certainty that allows it to attract the low-cost capital it needs to be economically competitive.

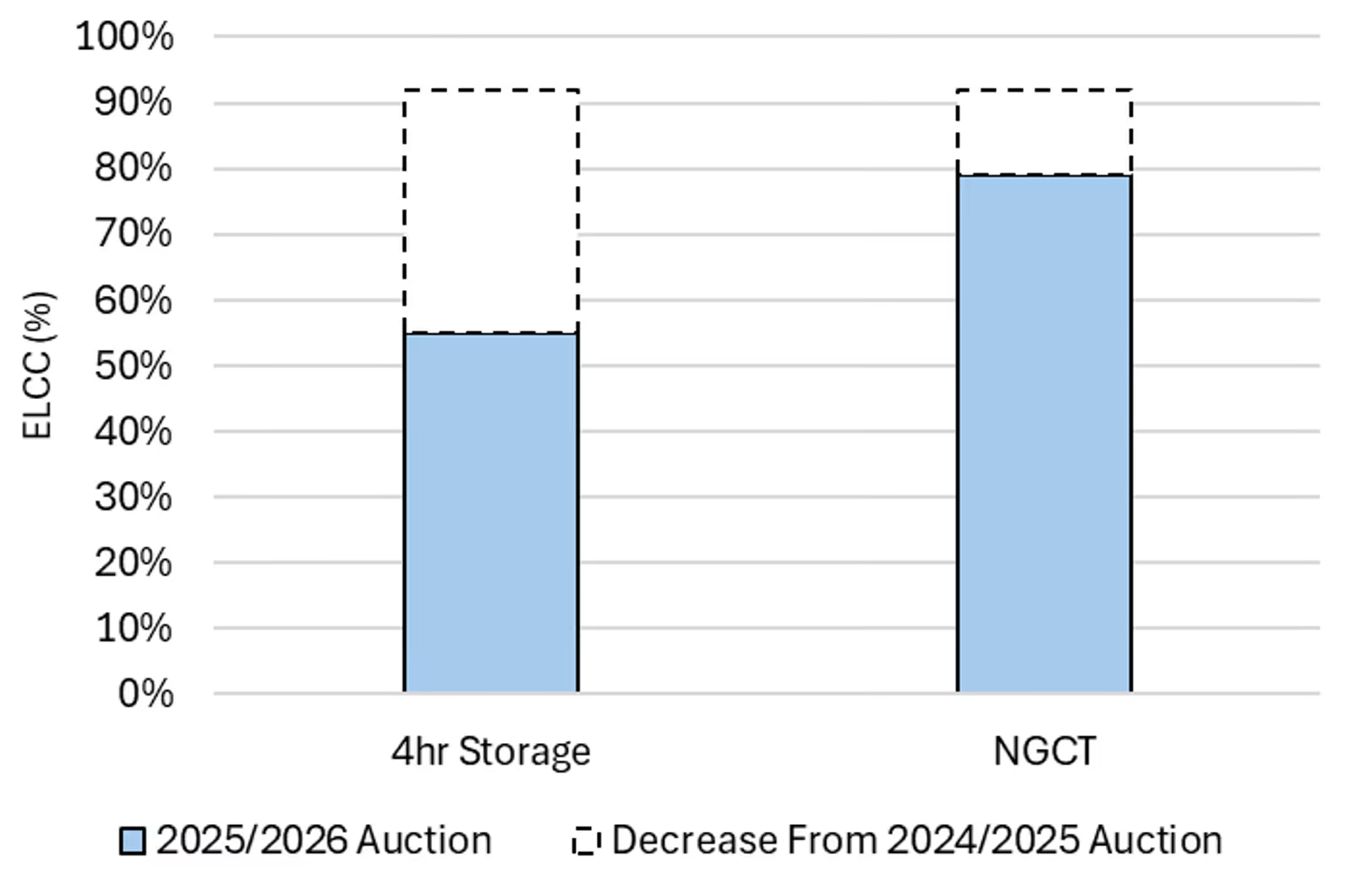

Long-term capacity offtake agreements are not strictly required to support new entry, but they are a powerful enabling tool. These contracts provide the revenue predictability that developers and financiers need to support capital-intensive projects. However, US capacity markets are moving away from this structure. ISO-NE, which previously offered seven-year price-lock commitments, now provides only one-year contracts due to a FERC ruling that the lock-in process was price-suppressive and discriminatory.1 This exposes new resources to year-over-year uncertainty and volatility in clearing prices, accreditation levels, and the risk of not clearing the market at all. This short contract duration makes it difficult to secure financing, especially as accreditation methodologies change, performance metrics shift, and political interventions can alter market rules midstream. A recent example is PJM’s change in accreditation for storage and gas CTs in response to winter reliability concerns. As shown in Figure 4, accreditation values dropped significantly between two recent auctions. In the subsequent auction, PJM imposed a price cap below the expected clearing level to keep ratepayer costs down, further limiting participants’ ability to recover expected revenues.

For developers and investors, this kind of regulatory uncertainty undermines confidence in the long-term cash flow stability that is needed to service debt. Markets that change the rules midstream not only affect near-term revenues but also reduce trust in the market’s ability to deliver predictable outcomes. This increases the hurdle rate for new entrants and slows the pace of new capacity development. In contrast, CAISO’s bilateral resource adequacy framework allows load serving entities to contract for capacity over longer terms. As a result, most new resources in California enter the market with 10- to 15-year contracts. While similar long-term contracting is possible in other markets, it remains less common despite its value as a hedge in the capacity markets. Expanding this practice could significantly reduce risk and lower the cost of new capacity. As capacity prices rise, the justification for long-term contracts through retail load offtake structures or state subsidies will grow. Calls for this change have already begun in PJM2.

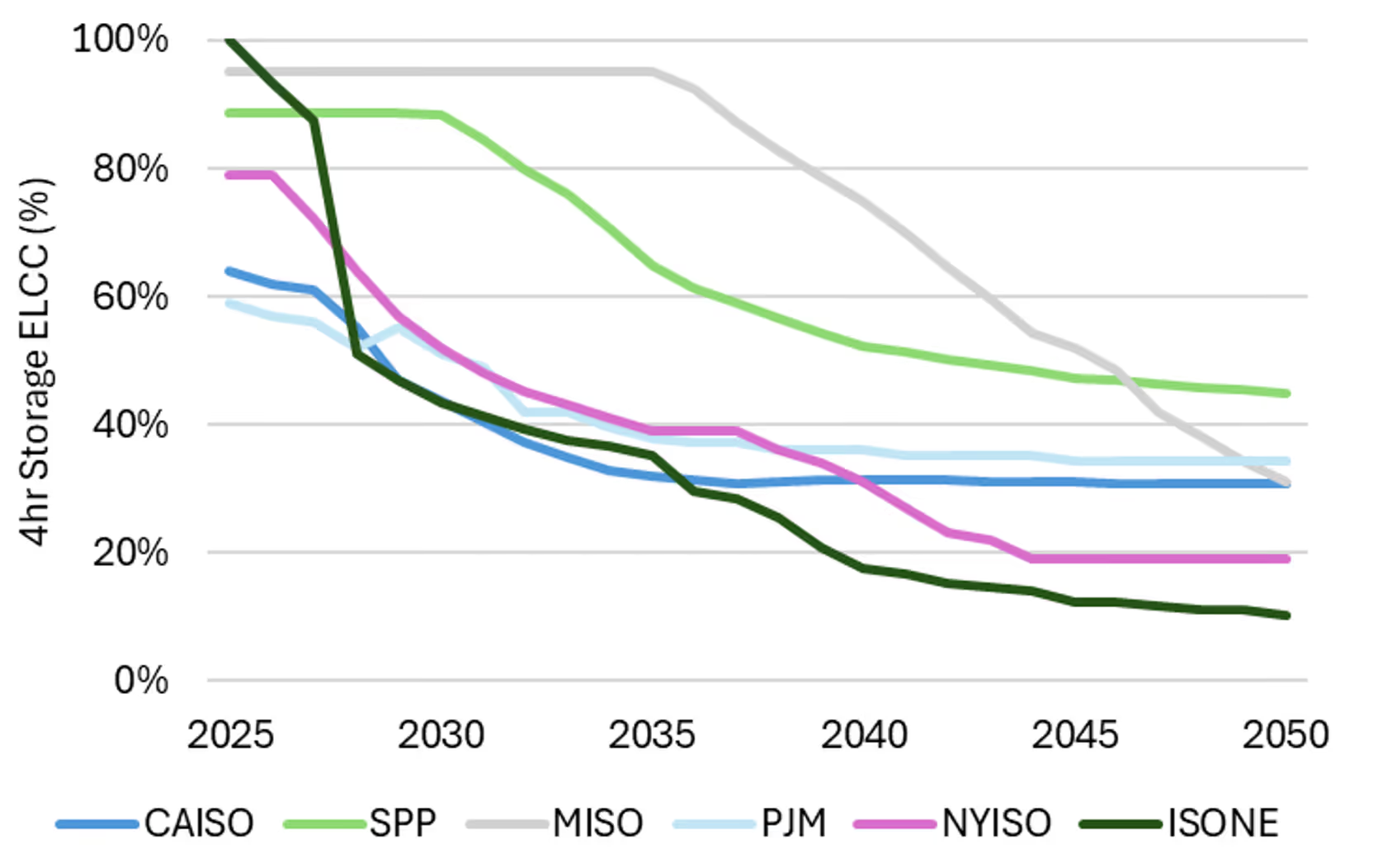

Not all capacity market changes are problematic, though. As grids evolve, it is appropriate to adjust how a resource’s contribution to reliability is measured. Early storage projects deliver more value when the system peak is narrow, while later entrants have diminishing reliability contributions as the net load curve flattens. The decline in peak load contribution sets an economic peak penetration of a given duration of storage. As markets decarbonize or transition to a winter peak-load, there will eventually be an ELCC and project cost where it would be preferential to develop a longer-duration storage facility or a dispatchable natural gas asset instead of multiple 4-hour storage systems, as illustrated in Figure 5, which shows Ascend’s forecasts of 4-hour storage ELCC by market. Further complicating the tradeoffs, cost concentrations in transmission upgrades and power electronics combined with energy arbitrage revenue concentrations in short-duration price spikes make both project cost and project value non-linear with additional duration.

When capacity is only procured one year at a time, developers face uncertainty around when and by how much ELCC will decline, and this uncertainty impacts the design and financeability of projects, contrasting with the stability provided by long-term contracting. While ELCC will naturally decline in steps as markets periodically review accreditation, the timing and magnitude are difficult to predict. MISO’s ELCC evolution illustrates this risk. The modeling currently used by the ISO is inconsistent with other markets, and assuming that MISO is not fundamentally different than other regions, the risk of ELCC re-normalization is both large and probable. Long-term offtake agreements, whether capacity-only or tolling/lease-style, can help bridge this uncertainty. The risk transfer in these contracts allows buyers to lock in favorable terms below the cost of spot capacity prices, while sellers gain the revenue stability needed to finance new projects.

Capacity prices in a market with significant load growth will structurally and necessarily price at the Net Cost of New Entry (Net CONE), which is the gross cost of new entry less any energy and ancillary operating revenues. The forcing functions behind this conclusion are discussed at length in Part I of this capacity market series, but costs to consumers do not necessarily have to skyrocket, as discussed in Part II of this series. Markets, states, utilities, and consumers have the ability to shape outcomes through targeted incentive programs that reduce the Net CONE of new capacity, with a focus on storage in locations with clean energy policies. These programs can shift the economics of new entry without distorting reliability outcomes or providing a windfall to the entire remaining supply stack. For example, the settlement mechanism in New York’s Index Storage Credit turns storage into a capacity market price taker and guarantees that the revenues of a storage project will reach a designated strike price independent of capacity prices or wholesale energy arbitrage results. This design ensures that capacity prices only rise if load growth exceeds the program’s support capacity. Similarly, Massachusetts’ Clean Peak Standard provides a revenue adder for clean energy delivered during peak hours, thus significantly lowering Net CONE for participating clean resources without subsidizing legacy fossil generation. As a result, Net CONE for storage in Massachusetts is materially lower than in the rest of ISO-NE, as shown in Figure 6.

Importantly, these subsidies can reduce capacity market costs by significantly more than the cost of the subsidy itself. Every unit that clears the capacity auction is paid the clearing price: therefore, reducing the cost of the marginal new entry unit saves capacity costs (and reduces capacity revenues) not just for the new unit but for the entire remaining capacity supply stack. Moreover, because the missing money for a given capacity resource gets divided by the ELCC to determine its needed capacity price, the impact of subsidies becomes further amplified by the ELCC of the subsidized resource.

Storage, in particular, offers a cost-effective target for subsidy, because of its relatively low ELCC. In PJM, for example, because the 2026-27 auction models a 50% ELCC for 4-hour storage, every dollar of subsidy to storage will reduce the capacity market Net CONE by two dollars, when storage sets the price. A subsidy to an NGCC, which carries an ELCC rating of 78%, by contrast, will reduce its capacity market Net CONE by $1.28 per dollar of subsidy when an NGCC sets the capacity price. Figure 7 shows the implications that a $25/kW-yr strategic subsidy could have on a 2030 capacity market clearing price. Without subsidies, the capacity price will grow to six times its historically normative level. In a scenario where new entry is required to meet load growth that is 50% above current levels, a $25/kW subsidy would reduce total capacity market costs by 28% (including the cost of the subsidy). Breaking that savings down further, the market clearing price (paid by all load) would be reduced by $53/kW-yr though a subsidy that would cost the average ratepayer $12/kW-yr.

Every market in the US will see large-scale deployment of storage between now and the end of the 2020s. Current economics and politics have positioned storage as the most viable solution to serve new load and to manage the impact of new load on ratepayers.

However, the ability of storage to economically enter into a market today does not guarantee that storage will be the long-term definitive solution for a market's future capacity needs. In the same way that high turbine costs, falling Li-Ion battery costs, and rapid load growth have opened a door to storage as a capacity resource, falling turbine costs and flattening net load peaks will close the door to storage over time.

In that context, three factors jointly determine long-term storage prospects:

A summary of how these factors manifest by state is shown in Figure 8 below.

As storage becomes a broadly viable capacity option, navigating the opportunities and risks will require a balanced view that accurately captures the key dynamics shaping energy markets now and in the future.

_____________________________________

1 FERC Order on New Entrant Rules

2 FERC's Christie calls the need for more gas-fired power 'a rendezvous with reality'

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

.avif)

.avif)

-1-ercot%20image.avif)

%20(1).avif)