Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

This publication is the third in a series from Ascend Analytics that considers the implications of rapid load growth on US capacity markets, high capacity prices as the new normal, the risks that new realities create for business-as-usual strategies, and the opportunities that this paradigm shift enables for well-planned new entry resources.

For much of the past two decades, declining load in many US energy markets diminished the demand for new thermal generation. Economic pressure from low gas prices and renewable deployment drove a wave of retirements among aging thermal plants. Now, however, load growth has returned in a big way, driven by data centers and electrification. This projected load growth is spurring renewed interest in building new thermal generation and is delaying retirements within the existing fleet. In this context, opportunities and risks abound for thermal generators, underscoring the need for a balanced market view that facilitates strategic navigation and prudent investments.

As revenues become increasingly concentrated in capacity markets, the importance of being able to maximize accreditation and generate during times of high system stress will grow. While capacity market accreditation has historically been defined relative to gross peak demand, system operators are increasingly focusing on assessing reliability contributions during those periods of highest scarcity (lowest supply reserves). While high demand is one factor that reduces reserves, the reliability impacts of dynamic changes on the supply side are growing in importance: these impacts include variability in wind and solar production, declining battery state of charge, disruptions to gas fuel supply, and weather-induced correlated forced outages at thermal plants.

Maximizing capacity revenues for thermal generation therefore requires being able to generate when other resources cannot, because if all supply resources could be available then the grid would be unlikely to experience scarcity. In ERCOT, which lacks a capacity market but has scarcity price adders that amplify energy prices when reserves run low, scarcity capture inherently requires being available when other supply resources are not. PJM and ISO-NE both have ‘pay-for-performance’ mechanisms in their capacity markets, in which generation resources that contribute above expected levels during scarcity conditions are given extra capacity compensation while those that perform below expected levels are penalized. As capacity prices rise, the value of overperformance rises and penalties for underperformance become steeper. All other independent system operators (ISOs) other than CAISO accredit (or are proposing to accredit) thermal capacity based on historical performance, thereby reducing the potential capacity value for generation resources that underperform during critical system conditions. Because scarcity conditions also result in the highest wholesale energy prices, the value of being available during these conditions becomes further concentrated.

Consequently, aging thermal generators should postpone retirement as long as they can be kept operational, as capacity prices rise to reflect a cost of new entry that should – in most cases – significantly exceed the cost of keeping existing generation online. Thermal asset owners should also be willing to spend heavily on preventative maintenance to maximize resilience to both hot and cold extreme weather conditions. The importance of resilience during extreme cold conditions is particularly acute: winter storms have driven the biggest reliability risks in recent years in all markets other than CAISO, and many systems are moving to winter peaking as electrification increases. Correlated thermal outages during cold weather will make winter the period of highest reliability risk in most locations even before annual peaks move to the winter.

Thermal plants that are less susceptible to fuel supply disruption or that have onsite fuel storage will be particularly valuable. Additionally, maintenance periods should be strategically planned to account for evolving reliability risk intervals, as reliability risks can arise even in shoulder seasons when unseasonable weather arrives while many other plants are on scheduled outages. Ultimately, with both capacity and energy value concentrating in narrow ranges of conditions, performance during tight conditions grows in importance relative to operations during the remainder of the year.

For those regions that transition toward high renewable penetrations, whether driven by policy or economic factors, renewable curtailment will drive wholesale power prices toward and below zero increasingly often, making generation uneconomic for thermal plants during high renewable output. However, variability in solar and wind supply will drive variability in prices, creating an incentive for generation resources that can be available when prices swing high without having to generate when prices are uneconomic. In such a price environment, flexibility will be the key to revenue maximization. In power markets with high renewable penetrations, large supply changes may occur suddenly, frequently, and briefly. Consequently, negative pricing will occur frequently and persistently, with typically brief swings to high prices when solar and wind generation decline. Maximizing revenue under these conditions requires the ability to turn off when prices are uneconomic and supply is abundant, turn on – and ramp quickly up and down – when prices rise and fall, and turn on and off as often as needed while minimizing startup costs.

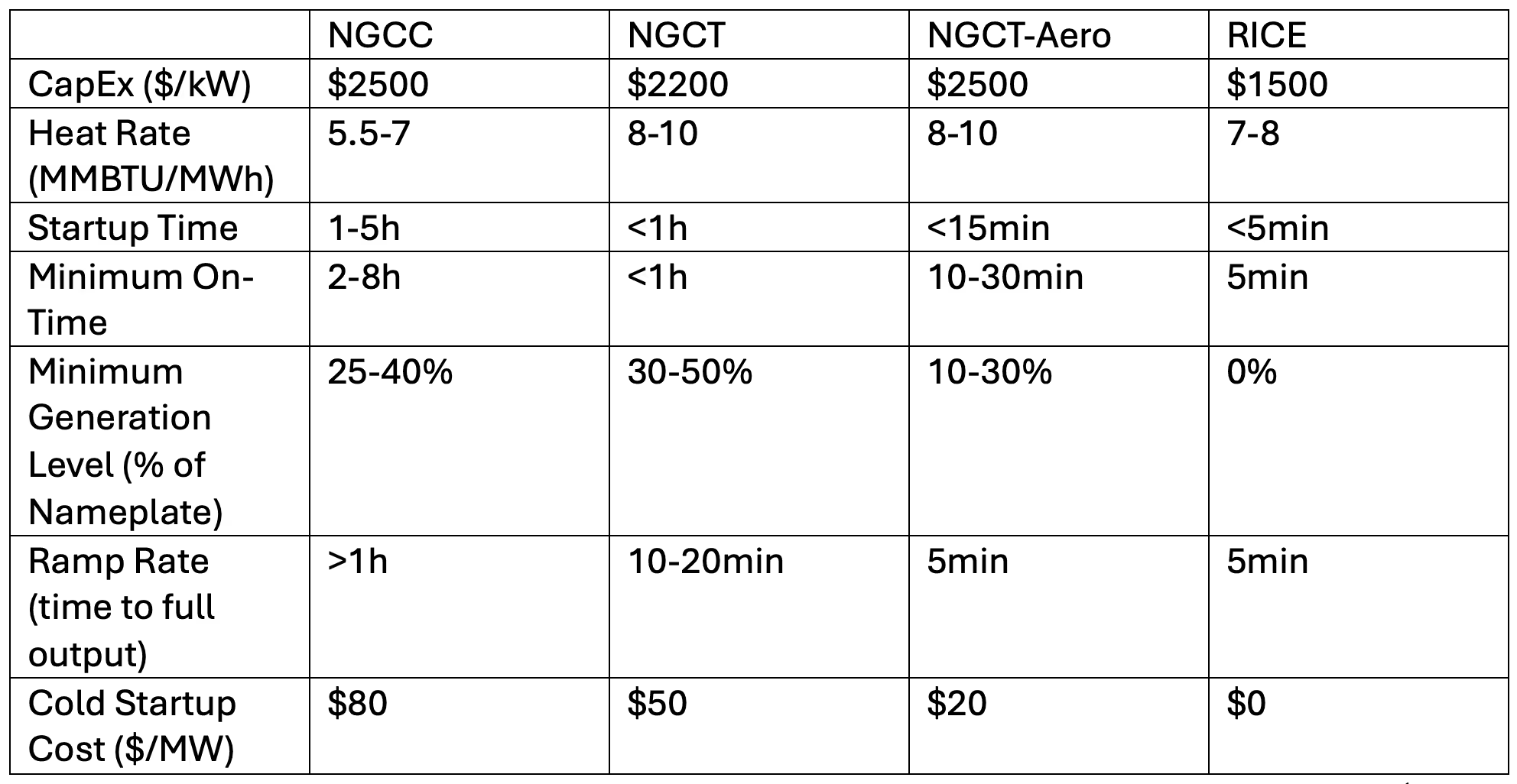

Table 1 shows typical cost and flexibility characteristics for modern Natural Gas Combined Cycle (NGCC), Natural Gas Combustion Turbine (NGCT), NGCT Aeroderivative, and Reciprocating Internal Combustion Engine (RICE) plants.1 While NGCCs are the most efficient, they are also significantly less flexible than the other resources, requiring longer to start, higher minimum generation levels, longer minimum on-times, and slower ramp rates. This reduced flexibility puts NGCCs at a disadvantage in an era of low and volatile power prices. RICE units have historically been more expensive than CCs and CTs, but turbine supply shortages that extend through the late 2020s have led to significant rises in gas turbine costs without corresponding rises for RICE units, leading to RICE now being cheaper, more efficient, and more flexible than an NGCT.

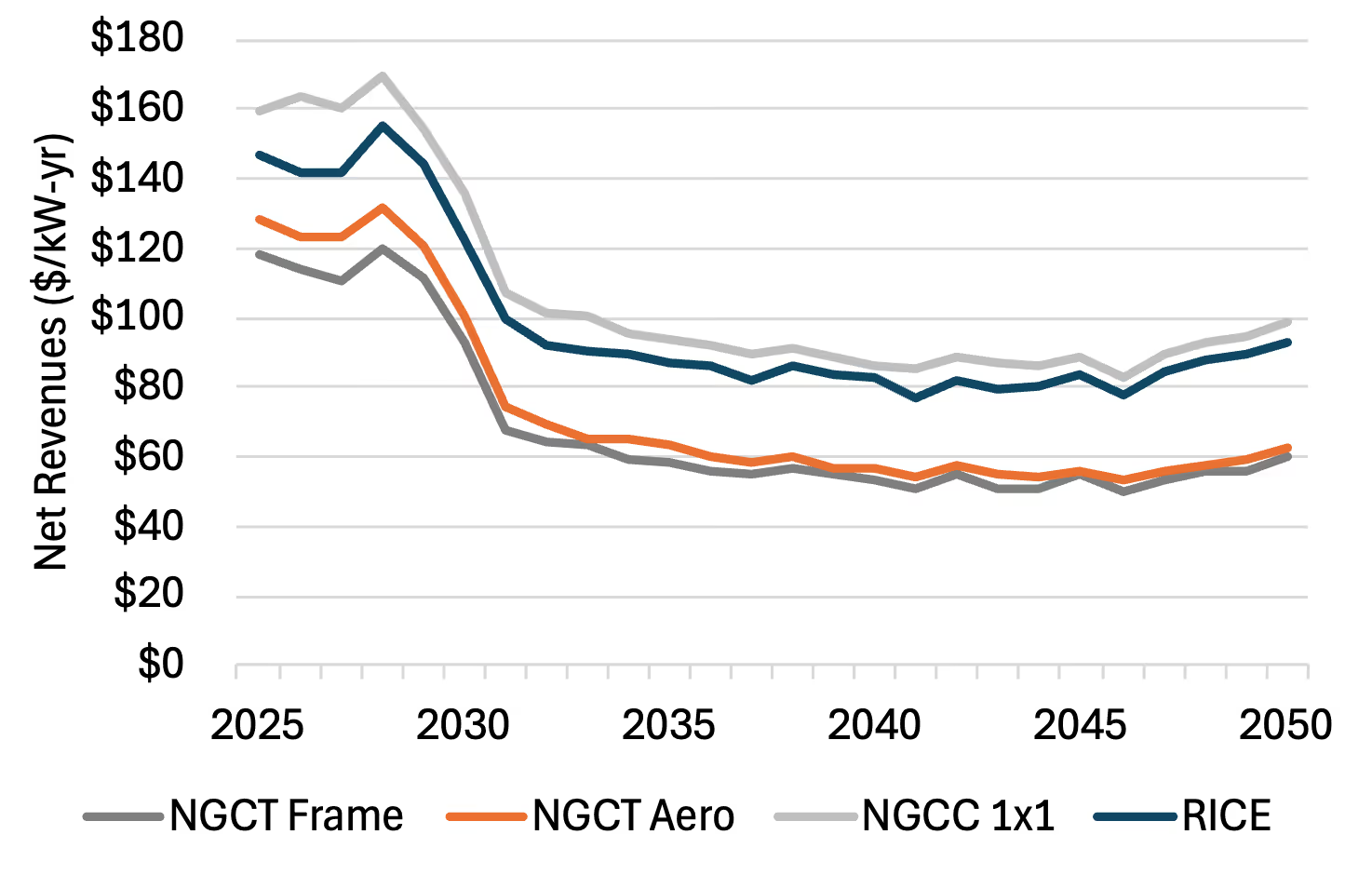

In locations where a substantial portion of energy is supplied by renewables but dispatchable thermal generation still plays a key role for reliability, the best-suited thermal resources will be those that can operate economically at low capacity factors and/or low prices. Figure 1 shows forecasted net revenues for various gas generation configurations through 2050 based on the Ascend 2025 ERCOT Forecast Release 5.2 (excluding scarcity, which is assumed to be similar for each resource type). During this time, renewable penetration is expected to reach 57% in 2035 and 67% in 2050, with average energy prices going from $44/MWh in 2035 to $54/MWh in 2050. As seen in Figure 1, NGCCs (which are the most efficient) earn the highest net revenue while RICE units have nearly as high revenue, owing to their high flexibility and efficiency. RICE units have the added advantage of modularity, which allows them to operate more frequently in their more efficient range and be less likely to experience total outages during valuable time periods. NGCTs have much lower revenues due to their lower efficiency, with the improved flexibility of aeroderivative turbines driving a small increase in revenue relative to frame NGCTs.

While load growth creates opportunities for new thermal capacity to come online, investment in thermal resources will still contain several risks that should be carefully considered before making irreversible, long-term investment decisions.

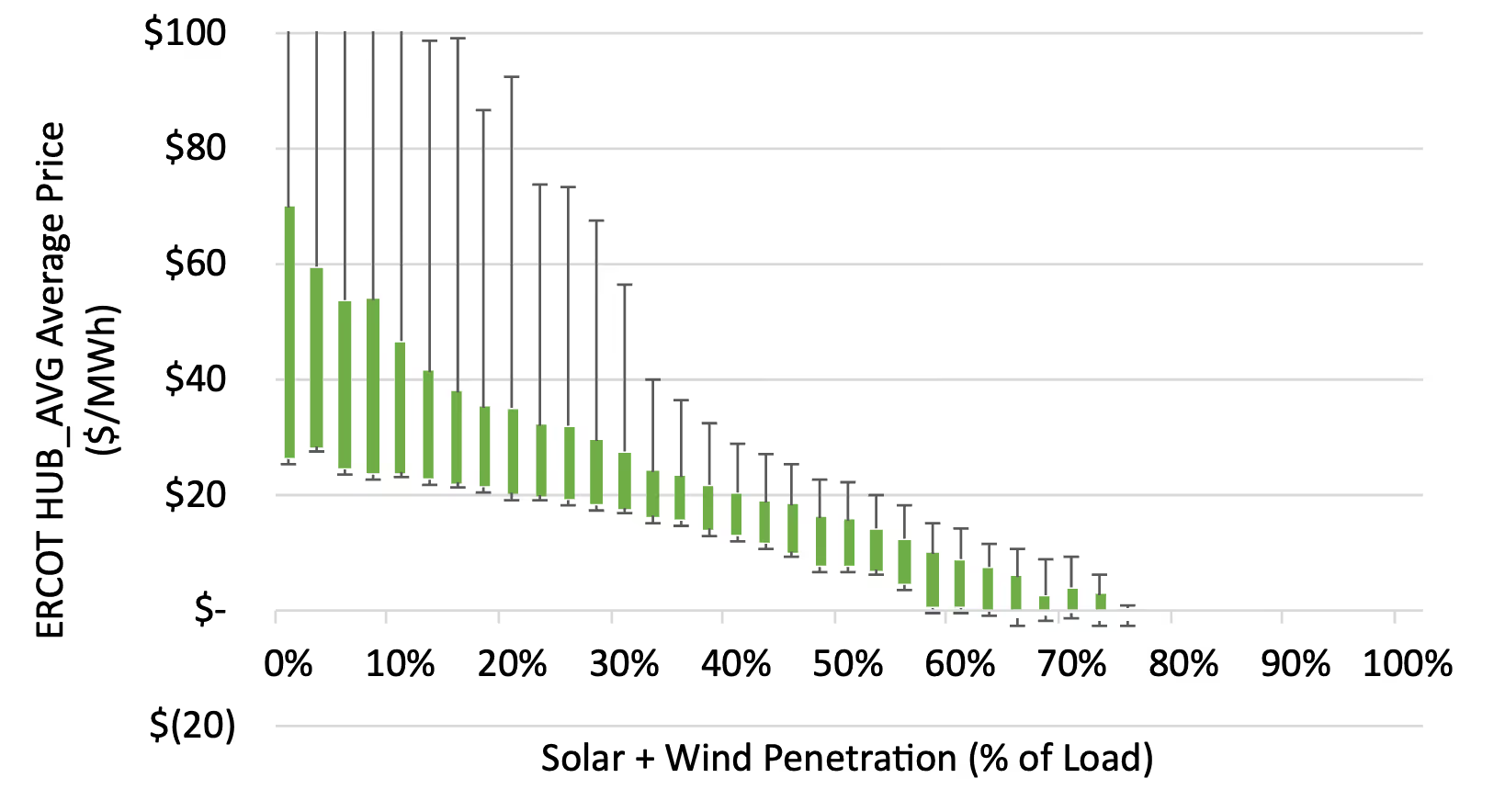

For regions undergoing significant increases in renewable penetration due to state policy, economic forces, or voluntary offtake, thermal generation is likely to see declining capacity factors and declining energy value due to renewable price depression, as shown in Figure 2. Thermal units will also capture minimal ancillary service value as storage displaces thermal generation in the ancillary supply stack. Project valuations that rely on high energy margins or capacity factors to be profitable are likely inflating the anticipated project value. Moreover, as project value becomes increasingly concentrated in capacity revenues, performance during narrow periods will become crucial, thus increasing the sensitivity of project economics to operational risks such as forced outages or fuel supply disruptions.

Even capacity markets carry significant risk, as subsidized or regulated new entry could severely depress capacity prices for remaining generators, as discussed in the market design paper within this series. If this occurs, depressed capacity prices could leave unsubsidized and unregulated new entry unable to recover fixed costs or CapEx. These resources would be forced to seek bilateral contracts and may be unable to find counterparties.

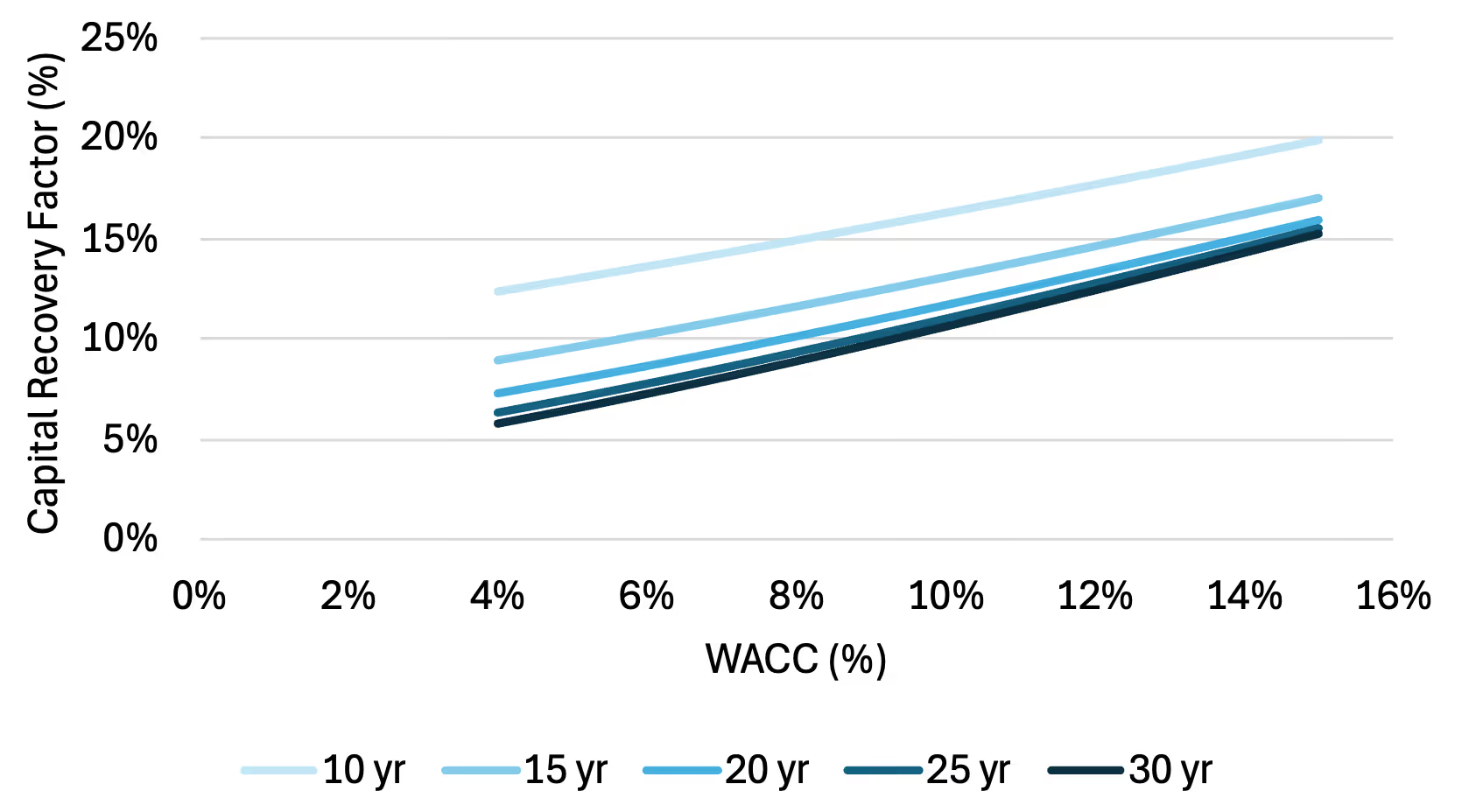

The ongoing potential for new or more aggressive clean energy policy at state and federal levels will create a persistent stranded asset risk for thermal generators that have an expected lifetime that extends beyond when clean energy mandates may come into effect. The potential for further cost declines to renewables and storage (including nascent long-duration storage technologies) adds a further stranded asset risk. Added system stress from increased ramping and start/stop cycles may also reduce thermal plant lifetimes and/or increase maintenance costs. Combined, these factors mean revenue requirements should account for the potential of a shorter operational life for new thermal generation and/or higher rates of return to compensate for the risks. As Figure 3 shows, revenue requirements are relatively insensitive to project lifetimes beyond 20 years, but revenue requirements start to increase dramatically for shorter project lifetimes.

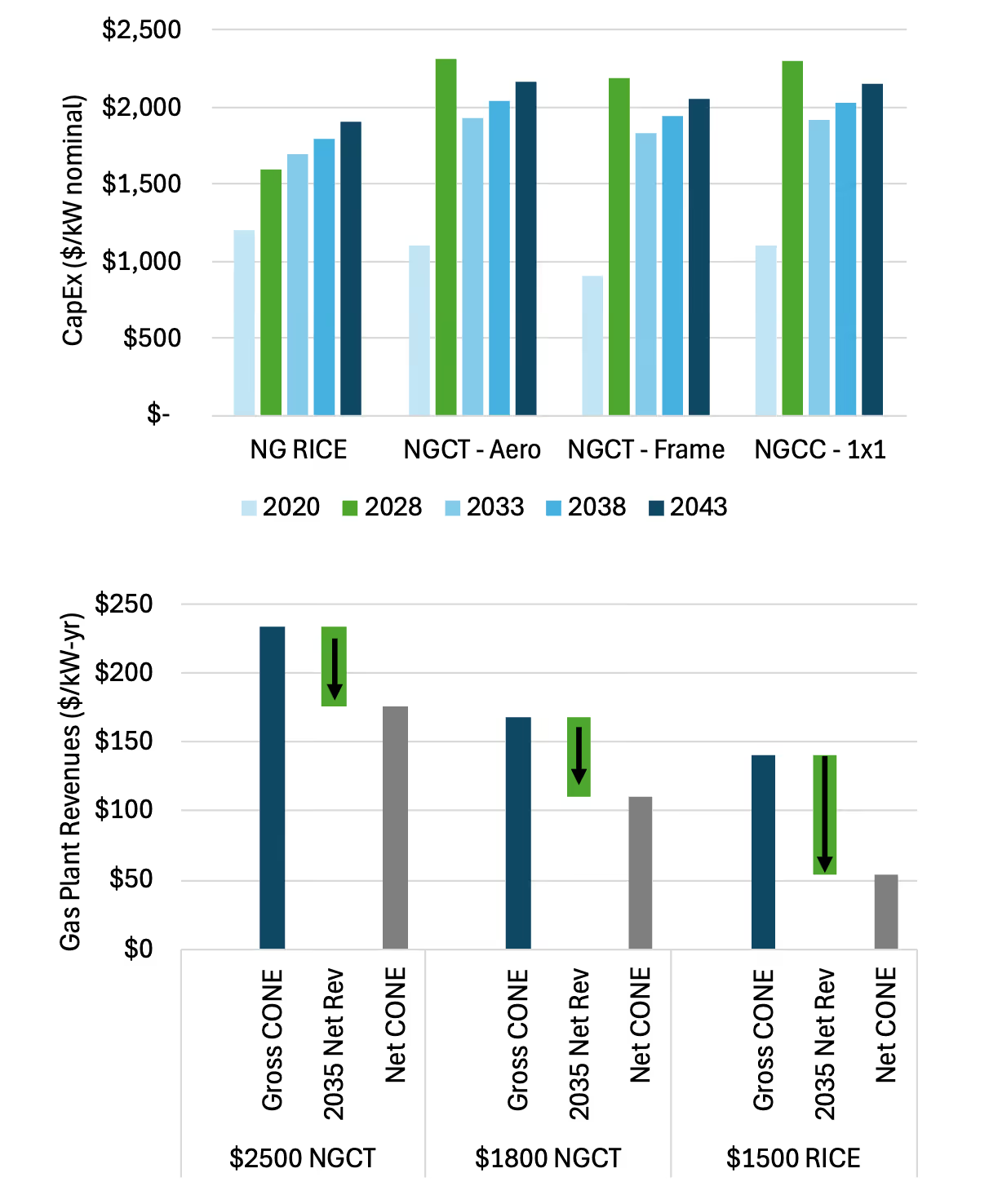

With the current surge in expected load growth amplifying demand for new gas capacity, gas turbine capital costs have risen by 2-3x since 2020, with tariffs adding the potential to increase costs even further. Ascend’s CapEx forecast for gas plants, shown in Figure 4, anticipates some cost normalization through the early 2030s, followed by rising long-run costs with inflation. If supply and demand for new gas capacity come back into balance and prices normalize in the early 2030s, gas turbines built in the early 2030s will have similar performance characteristics to the high-cost units built in the 2020s but a much lower gross CONE revenue requirement, which Figure 4 also shows. If capacity prices reflect the cost of the inflated gas capacity, the equivalent but lower-cost units that come online later will be able to earn supernormal returns. This will drive more new gas online until capacity prices reflect the lower-cost units, displacing the inflated gas capacity and leaving it unable to capture sufficient capacity revenues to cover costs.

Inflated gas turbines will experience the same challenges when competing against RICE units that have not exhibited the same price increases or supply constraints that have occurred for the turbines. Assuming that supply dynamics lead to turbines still setting capacity market prices and revenues, RICE units are positioned to be highly profitable capacity resources, with both lower CapEx and higher net revenues than turbines. While the relative economics of RICE, NGCT, and NGCC will vary by market, the risk of backwardated turbine costs and alternate technologies with fewer supply constraints will remain.

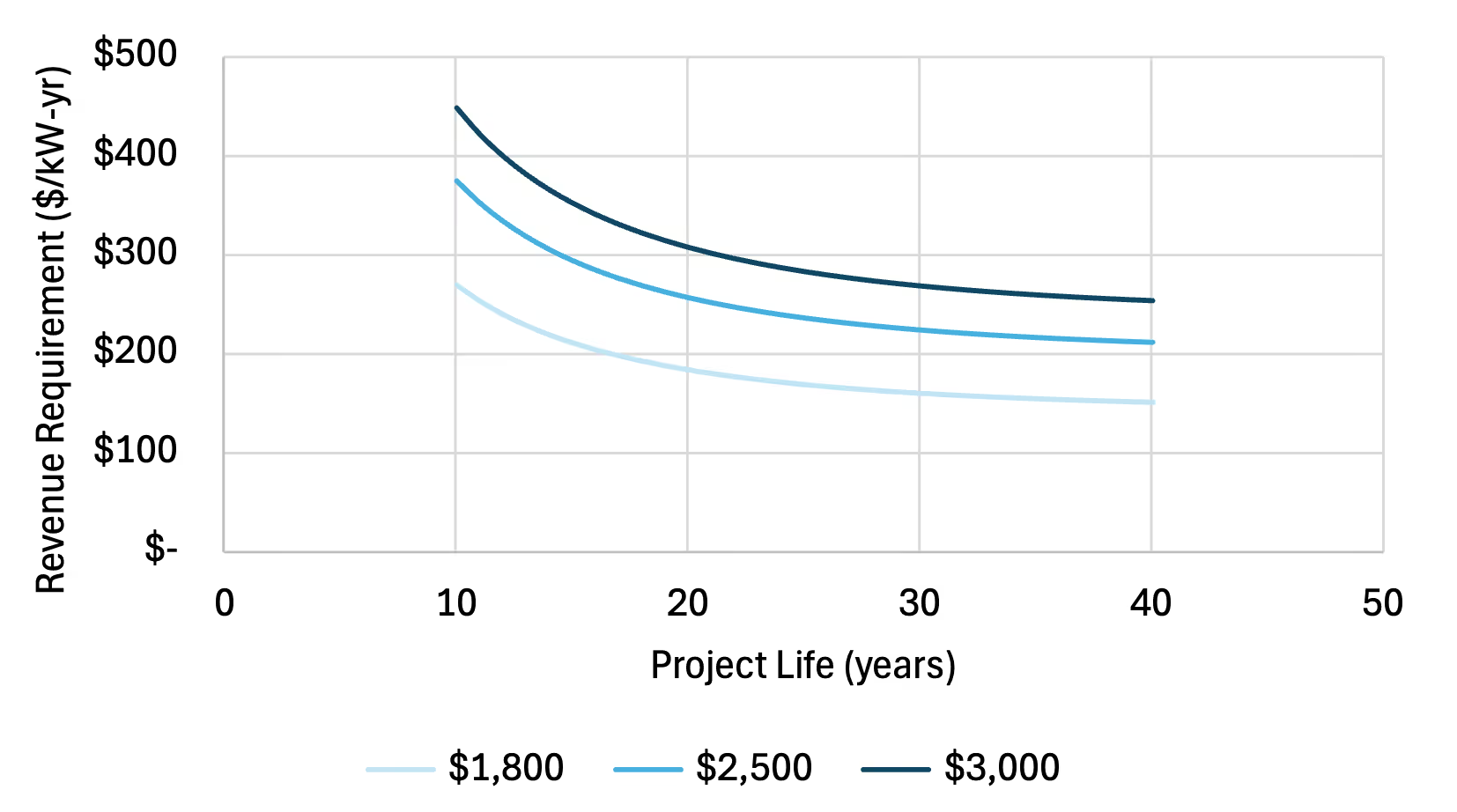

However, the lower revenue requirement of future lower-cost projects will come at the expense of increased stranded asset risk (due to potential policy changes) and missing out on potentially more profitable near-term years before renewable growth depresses wholesale power prices. Thus, later thermal unit entry will face its own risks. Figure 5 shows revenue requirement as a function of project lifetimes for several different capital costs and a fixed 8% WACC. The graph shows that for projects with CapEx of $2,500/kW and $1,800/kW to have the same revenue requirement, the $1,800/kW project would need to have a 10- to 20-year shorter lifetime.

To the extent that carbon emissions are valued by offtakers or priced in by markets, they could either help or hinder gas project economics. In a coal-heavy market, a value or price on carbon can provide a significant boost in valuation for an NGCC through its emissions reductions relative to higher-emissions marginal units. However, in locations where the marginal unit is usually gas or something with even lower emissions, a carbon price (or a carbon price increase) can make new energy storage more economical than new gas in markets where they would otherwise be competitive with each other.

Elevated carbon prices increase both power prices and power price volatility without meaningfully increasing revenues for an NGCT, for which the marginal cost of production correspondingly increases with carbon prices. Higher power prices strengthen the economics for renewable resources, leading to higher levels of renewable build and increasing the supply swings that underpin price volatility. In addition to the underlying supply swings, carbon prices further amplify price volatility by increasing the price spreads both within the thermal portion of the supply stack as well as between the renewable and thermal portions of the supply stack.

This increased price volatility increases the potential energy arbitrage revenue for storage without improving energy margins for new gas, thus favoring new storage over new gas. Any increases in nuclear generation, which is typically operated primarily as must-run, will increase the effective renewable penetration into the remaining portion of the supply stack, which will also depress average prices and increase price volatility, further supporting storage over new gas.

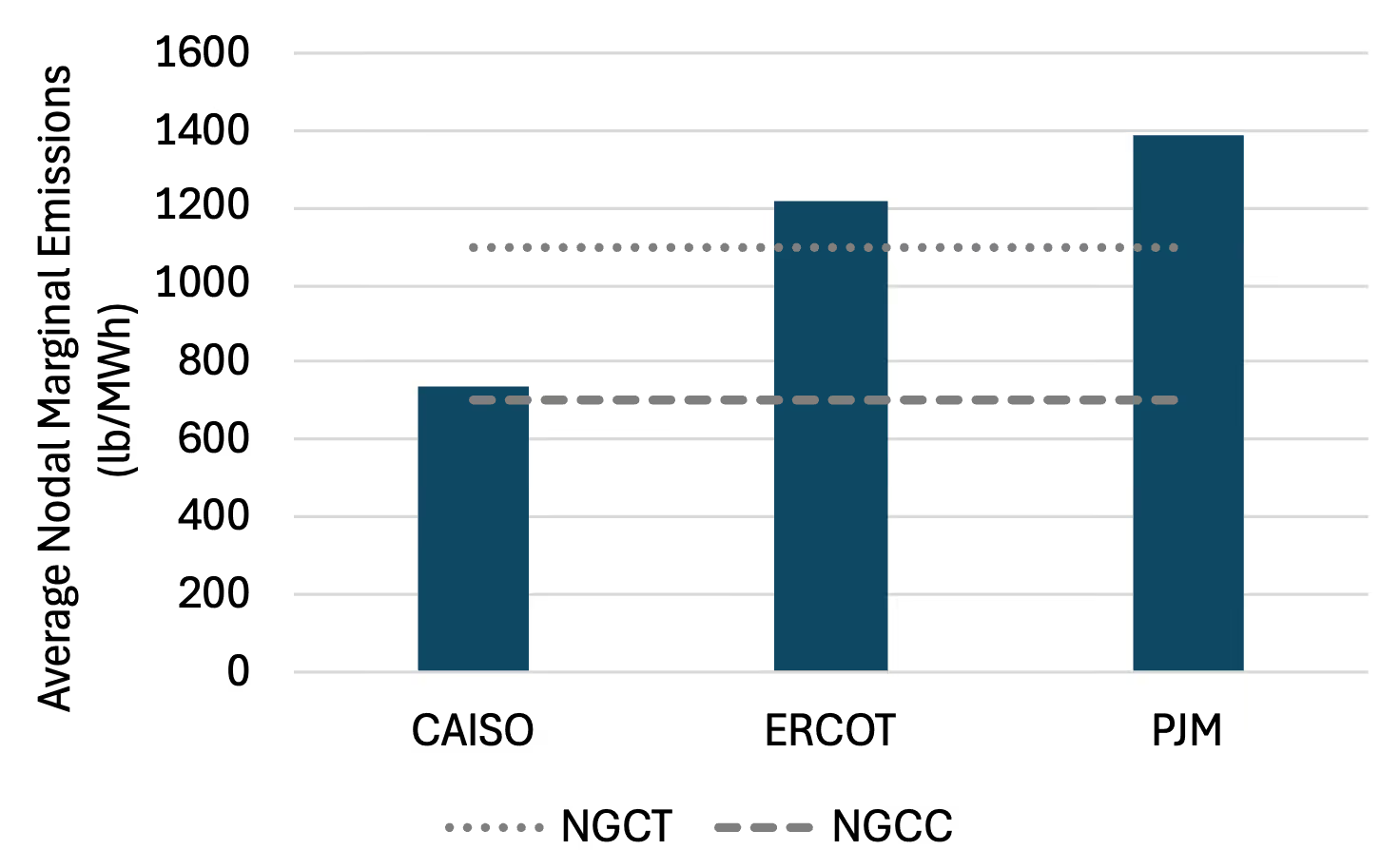

Figure 6 shows Ascend’s estimated average marginal emissions for CAISO, PJM, and ERCOT in 2024, with representative emissions intensities for an NGCT and NGCC included for reference. The graph shows a high degree of variation between markets, demonstrating significant differences in the potential emissions offsets for different gas assets. Whether mandatory or voluntary, a price on carbon will place a value on the potential offsets a given resource can provide and will have a larger effect in markets with higher carbon intensity.

In the face of rising electricity demand and declining capacity accreditation for renewables and storage, the need for dispatchable, long-duration capacity resources will persist. To meet this need, new gas capacity will be built.

However, investments in new gas should be made cautiously, prudently, and strategically. Thermal generation will remain a risky investment, with stranded asset risks not going away. Investment in new gas capacity at inflated prices through the end of the 2020s also creates a risk of being outcompeted by future projects once prices normalize.

Given the opportunities and risks of investment in thermal generation, the need for a balanced market view is more important than ever.

________________________________

1 Costs and performance characteristics are indicative of current values and not intended to be exact. Information taken from internal sources, manufacturer technical data sheets, and Kumar et al., “Power Plant Cycling Costs”, NREL Technical Monitor, 2012

This publication is the third in a series from Ascend Analytics that considers the implications of rapid load growth on US capacity markets, high capacity prices as the new normal, the risks that new realities create for business-as-usual strategies, and the opportunities that this paradigm shift enables for well-planned new entry resources.

For much of the past two decades, declining load in many US energy markets diminished the demand for new thermal generation. Economic pressure from low gas prices and renewable deployment drove a wave of retirements among aging thermal plants. Now, however, load growth has returned in a big way, driven by data centers and electrification. This projected load growth is spurring renewed interest in building new thermal generation and is delaying retirements within the existing fleet. In this context, opportunities and risks abound for thermal generators, underscoring the need for a balanced market view that facilitates strategic navigation and prudent investments.

As revenues become increasingly concentrated in capacity markets, the importance of being able to maximize accreditation and generate during times of high system stress will grow. While capacity market accreditation has historically been defined relative to gross peak demand, system operators are increasingly focusing on assessing reliability contributions during those periods of highest scarcity (lowest supply reserves). While high demand is one factor that reduces reserves, the reliability impacts of dynamic changes on the supply side are growing in importance: these impacts include variability in wind and solar production, declining battery state of charge, disruptions to gas fuel supply, and weather-induced correlated forced outages at thermal plants.

Maximizing capacity revenues for thermal generation therefore requires being able to generate when other resources cannot, because if all supply resources could be available then the grid would be unlikely to experience scarcity. In ERCOT, which lacks a capacity market but has scarcity price adders that amplify energy prices when reserves run low, scarcity capture inherently requires being available when other supply resources are not. PJM and ISO-NE both have ‘pay-for-performance’ mechanisms in their capacity markets, in which generation resources that contribute above expected levels during scarcity conditions are given extra capacity compensation while those that perform below expected levels are penalized. As capacity prices rise, the value of overperformance rises and penalties for underperformance become steeper. All other independent system operators (ISOs) other than CAISO accredit (or are proposing to accredit) thermal capacity based on historical performance, thereby reducing the potential capacity value for generation resources that underperform during critical system conditions. Because scarcity conditions also result in the highest wholesale energy prices, the value of being available during these conditions becomes further concentrated.

Consequently, aging thermal generators should postpone retirement as long as they can be kept operational, as capacity prices rise to reflect a cost of new entry that should – in most cases – significantly exceed the cost of keeping existing generation online. Thermal asset owners should also be willing to spend heavily on preventative maintenance to maximize resilience to both hot and cold extreme weather conditions. The importance of resilience during extreme cold conditions is particularly acute: winter storms have driven the biggest reliability risks in recent years in all markets other than CAISO, and many systems are moving to winter peaking as electrification increases. Correlated thermal outages during cold weather will make winter the period of highest reliability risk in most locations even before annual peaks move to the winter.

Thermal plants that are less susceptible to fuel supply disruption or that have onsite fuel storage will be particularly valuable. Additionally, maintenance periods should be strategically planned to account for evolving reliability risk intervals, as reliability risks can arise even in shoulder seasons when unseasonable weather arrives while many other plants are on scheduled outages. Ultimately, with both capacity and energy value concentrating in narrow ranges of conditions, performance during tight conditions grows in importance relative to operations during the remainder of the year.

For those regions that transition toward high renewable penetrations, whether driven by policy or economic factors, renewable curtailment will drive wholesale power prices toward and below zero increasingly often, making generation uneconomic for thermal plants during high renewable output. However, variability in solar and wind supply will drive variability in prices, creating an incentive for generation resources that can be available when prices swing high without having to generate when prices are uneconomic. In such a price environment, flexibility will be the key to revenue maximization. In power markets with high renewable penetrations, large supply changes may occur suddenly, frequently, and briefly. Consequently, negative pricing will occur frequently and persistently, with typically brief swings to high prices when solar and wind generation decline. Maximizing revenue under these conditions requires the ability to turn off when prices are uneconomic and supply is abundant, turn on – and ramp quickly up and down – when prices rise and fall, and turn on and off as often as needed while minimizing startup costs.

Table 1 shows typical cost and flexibility characteristics for modern Natural Gas Combined Cycle (NGCC), Natural Gas Combustion Turbine (NGCT), NGCT Aeroderivative, and Reciprocating Internal Combustion Engine (RICE) plants.1 While NGCCs are the most efficient, they are also significantly less flexible than the other resources, requiring longer to start, higher minimum generation levels, longer minimum on-times, and slower ramp rates. This reduced flexibility puts NGCCs at a disadvantage in an era of low and volatile power prices. RICE units have historically been more expensive than CCs and CTs, but turbine supply shortages that extend through the late 2020s have led to significant rises in gas turbine costs without corresponding rises for RICE units, leading to RICE now being cheaper, more efficient, and more flexible than an NGCT.

In locations where a substantial portion of energy is supplied by renewables but dispatchable thermal generation still plays a key role for reliability, the best-suited thermal resources will be those that can operate economically at low capacity factors and/or low prices. Figure 1 shows forecasted net revenues for various gas generation configurations through 2050 based on the Ascend 2025 ERCOT Forecast Release 5.2 (excluding scarcity, which is assumed to be similar for each resource type). During this time, renewable penetration is expected to reach 57% in 2035 and 67% in 2050, with average energy prices going from $44/MWh in 2035 to $54/MWh in 2050. As seen in Figure 1, NGCCs (which are the most efficient) earn the highest net revenue while RICE units have nearly as high revenue, owing to their high flexibility and efficiency. RICE units have the added advantage of modularity, which allows them to operate more frequently in their more efficient range and be less likely to experience total outages during valuable time periods. NGCTs have much lower revenues due to their lower efficiency, with the improved flexibility of aeroderivative turbines driving a small increase in revenue relative to frame NGCTs.

While load growth creates opportunities for new thermal capacity to come online, investment in thermal resources will still contain several risks that should be carefully considered before making irreversible, long-term investment decisions.

For regions undergoing significant increases in renewable penetration due to state policy, economic forces, or voluntary offtake, thermal generation is likely to see declining capacity factors and declining energy value due to renewable price depression, as shown in Figure 2. Thermal units will also capture minimal ancillary service value as storage displaces thermal generation in the ancillary supply stack. Project valuations that rely on high energy margins or capacity factors to be profitable are likely inflating the anticipated project value. Moreover, as project value becomes increasingly concentrated in capacity revenues, performance during narrow periods will become crucial, thus increasing the sensitivity of project economics to operational risks such as forced outages or fuel supply disruptions.

Even capacity markets carry significant risk, as subsidized or regulated new entry could severely depress capacity prices for remaining generators, as discussed in the market design paper within this series. If this occurs, depressed capacity prices could leave unsubsidized and unregulated new entry unable to recover fixed costs or CapEx. These resources would be forced to seek bilateral contracts and may be unable to find counterparties.

The ongoing potential for new or more aggressive clean energy policy at state and federal levels will create a persistent stranded asset risk for thermal generators that have an expected lifetime that extends beyond when clean energy mandates may come into effect. The potential for further cost declines to renewables and storage (including nascent long-duration storage technologies) adds a further stranded asset risk. Added system stress from increased ramping and start/stop cycles may also reduce thermal plant lifetimes and/or increase maintenance costs. Combined, these factors mean revenue requirements should account for the potential of a shorter operational life for new thermal generation and/or higher rates of return to compensate for the risks. As Figure 3 shows, revenue requirements are relatively insensitive to project lifetimes beyond 20 years, but revenue requirements start to increase dramatically for shorter project lifetimes.

With the current surge in expected load growth amplifying demand for new gas capacity, gas turbine capital costs have risen by 2-3x since 2020, with tariffs adding the potential to increase costs even further. Ascend’s CapEx forecast for gas plants, shown in Figure 4, anticipates some cost normalization through the early 2030s, followed by rising long-run costs with inflation. If supply and demand for new gas capacity come back into balance and prices normalize in the early 2030s, gas turbines built in the early 2030s will have similar performance characteristics to the high-cost units built in the 2020s but a much lower gross CONE revenue requirement, which Figure 4 also shows. If capacity prices reflect the cost of the inflated gas capacity, the equivalent but lower-cost units that come online later will be able to earn supernormal returns. This will drive more new gas online until capacity prices reflect the lower-cost units, displacing the inflated gas capacity and leaving it unable to capture sufficient capacity revenues to cover costs.

Inflated gas turbines will experience the same challenges when competing against RICE units that have not exhibited the same price increases or supply constraints that have occurred for the turbines. Assuming that supply dynamics lead to turbines still setting capacity market prices and revenues, RICE units are positioned to be highly profitable capacity resources, with both lower CapEx and higher net revenues than turbines. While the relative economics of RICE, NGCT, and NGCC will vary by market, the risk of backwardated turbine costs and alternate technologies with fewer supply constraints will remain.

However, the lower revenue requirement of future lower-cost projects will come at the expense of increased stranded asset risk (due to potential policy changes) and missing out on potentially more profitable near-term years before renewable growth depresses wholesale power prices. Thus, later thermal unit entry will face its own risks. Figure 5 shows revenue requirement as a function of project lifetimes for several different capital costs and a fixed 8% WACC. The graph shows that for projects with CapEx of $2,500/kW and $1,800/kW to have the same revenue requirement, the $1,800/kW project would need to have a 10- to 20-year shorter lifetime.

To the extent that carbon emissions are valued by offtakers or priced in by markets, they could either help or hinder gas project economics. In a coal-heavy market, a value or price on carbon can provide a significant boost in valuation for an NGCC through its emissions reductions relative to higher-emissions marginal units. However, in locations where the marginal unit is usually gas or something with even lower emissions, a carbon price (or a carbon price increase) can make new energy storage more economical than new gas in markets where they would otherwise be competitive with each other.

Elevated carbon prices increase both power prices and power price volatility without meaningfully increasing revenues for an NGCT, for which the marginal cost of production correspondingly increases with carbon prices. Higher power prices strengthen the economics for renewable resources, leading to higher levels of renewable build and increasing the supply swings that underpin price volatility. In addition to the underlying supply swings, carbon prices further amplify price volatility by increasing the price spreads both within the thermal portion of the supply stack as well as between the renewable and thermal portions of the supply stack.

This increased price volatility increases the potential energy arbitrage revenue for storage without improving energy margins for new gas, thus favoring new storage over new gas. Any increases in nuclear generation, which is typically operated primarily as must-run, will increase the effective renewable penetration into the remaining portion of the supply stack, which will also depress average prices and increase price volatility, further supporting storage over new gas.

Figure 6 shows Ascend’s estimated average marginal emissions for CAISO, PJM, and ERCOT in 2024, with representative emissions intensities for an NGCT and NGCC included for reference. The graph shows a high degree of variation between markets, demonstrating significant differences in the potential emissions offsets for different gas assets. Whether mandatory or voluntary, a price on carbon will place a value on the potential offsets a given resource can provide and will have a larger effect in markets with higher carbon intensity.

In the face of rising electricity demand and declining capacity accreditation for renewables and storage, the need for dispatchable, long-duration capacity resources will persist. To meet this need, new gas capacity will be built.

However, investments in new gas should be made cautiously, prudently, and strategically. Thermal generation will remain a risky investment, with stranded asset risks not going away. Investment in new gas capacity at inflated prices through the end of the 2020s also creates a risk of being outcompeted by future projects once prices normalize.

Given the opportunities and risks of investment in thermal generation, the need for a balanced market view is more important than ever.

________________________________

1 Costs and performance characteristics are indicative of current values and not intended to be exact. Information taken from internal sources, manufacturer technical data sheets, and Kumar et al., “Power Plant Cycling Costs”, NREL Technical Monitor, 2012

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

.avif)

.avif)

-1-ercot%20image.avif)

%20(1).avif)