Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

This publication is the second in a series from Ascend Analytics that considers the implications of rapid load growth on US capacity markets, high capacity prices as the new normal, the risks that new realities create for business-as-usual strategies, and the opportunities that this paradigm shift enables for well-planned new entry resources.

For much of the past two decades, flat load growth left most US power markets oversupplied with capacity, driving low prices both in capacity markets and in bilateral capacity contracts. When combined with low energy market prices driven by cheap natural gas and renewable deployment, low capacity prices led many aging thermal plants to retire, thus tightening supply just as load is being projected to return to robust growth.

However, rising load growth means the entire US has started to (or will soon) see the capacity markets become short for the first time in a generation. Moreover, whereas regulated utilities only recover supply costs, capacity markets pay a market-clearing price to all supply resources. When capacity prices rise to the level required to support new entry, these prices must be paid across the entire supply stack, causing capacity market costs to ratepayers to skyrocket and providing a windfall to existing supply resources.

As tightening conditions have begun pushing up capacity prices in some markets, political pushback and growing sensitivity to energy costs has ensued. Increasingly, stakeholders have been expressing concerns about the future of organized power markets, with some calling to dissolve the markets and re-regulate the power sector. Containing capacity costs without compromising the incentives needed to encourage new unit entry presents a significant challenge, with a limited set of viable solutions.

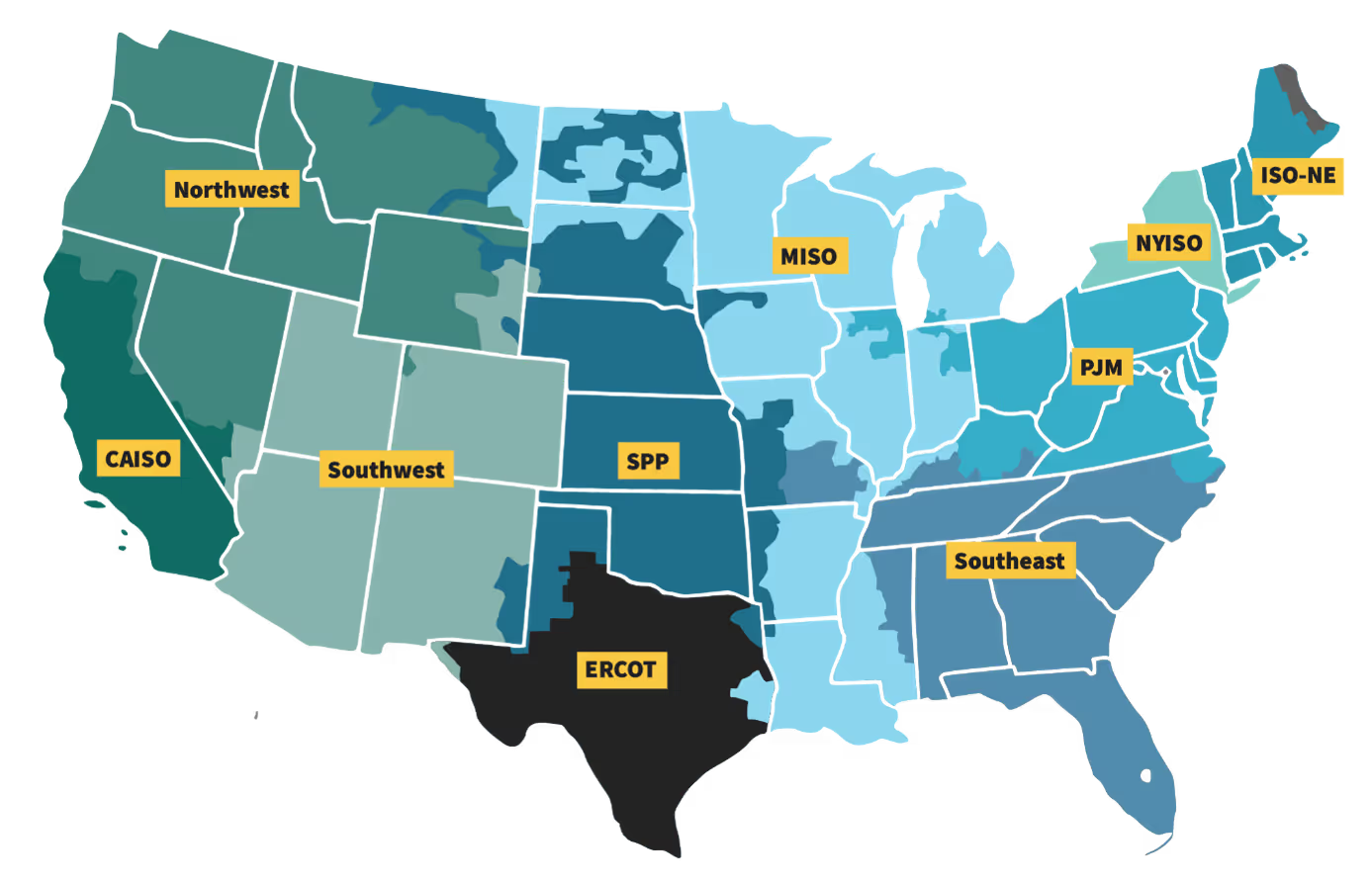

Shown in Figure 1, some parts of the US lack organized markets and instead have fully regulated utilities that receive cost-recovery from captive ratepayers for the costs of supply (primarily the non-California WECC and the Southeast, though some market expansion is coming to these regions).1 The remaining parts of the country have organized electricity markets and independent system operators (ISOs), in which market participants compete to provide the lowest-cost electricity throughout the day. Within these competitive markets, some states still have regulated utilities, including investor-owned utilities, public power entities, and electric co-operatives. Other states have fully deregulated the power sector, with publicly regulated transmission and distribution utilities but competitive retail power suppliers, along with competitive generation produced by Independent Power Producers (IPPs). The primary benefit of deregulated, competitive markets is that the investments risks associated with building power generation are borne by private investors rather than captive ratepayers. In most markets, both IPPs and at least some regulated utilities participate together within the market.

Most market participants bid something close to their variable cost of production in daily energy markets. This means that generation resources that are dispatched only on the highest demand days typically only recover their variable costs but still need a way to recover their fixed costs and/or capital expenditures (CapEx). Regulated utilities can recover these costs directly from ratepayers, but IPPs and other market participants need another revenue mechanism to provide this ‘missing money’ that is needed to incentivize these resources to be built in a market and be available when the grid needs supply.

Each market has a different structure for providing these missing revenues. Load-serving entities in SPP and CAISO (roughly 14% of national electric load) must either own or enter into bilateral contracts with sufficient generation to cover their load, though in SPP the requirement comes from the market operator, whereas in California the requirement primarily comes from the state utility commission. ERCOT (roughly 12% of national electric load) has an ‘energy-only’ market but creates just-in-time capacity revenues through a $5,000/MWh price cap and price adders when reserves run scarce. ERCOT also has increased its procurement of ancillary services and created new ancillary services to provide additional revenues to reliability resources.

The remaining markets (roughly 40% of national electric load)all have some form of capacity market structure, in which capacity auctions are held in advance of a given planning year to ensure enough capacity is procured to meet projected demand, and in which all the supply in the market is paid a market-clearing price. MISO consists of mostly regulated utilities, and its capacity auction is optional, with ~90% of load opting out and choosing instead to self-supply capacity through generation owned by the regulated utilities. PJM, ISO-NE, and NYISO have traditional capacity market structures, with lead times ranging from three years (PJM) to one year (ISO-NE and NYISO).

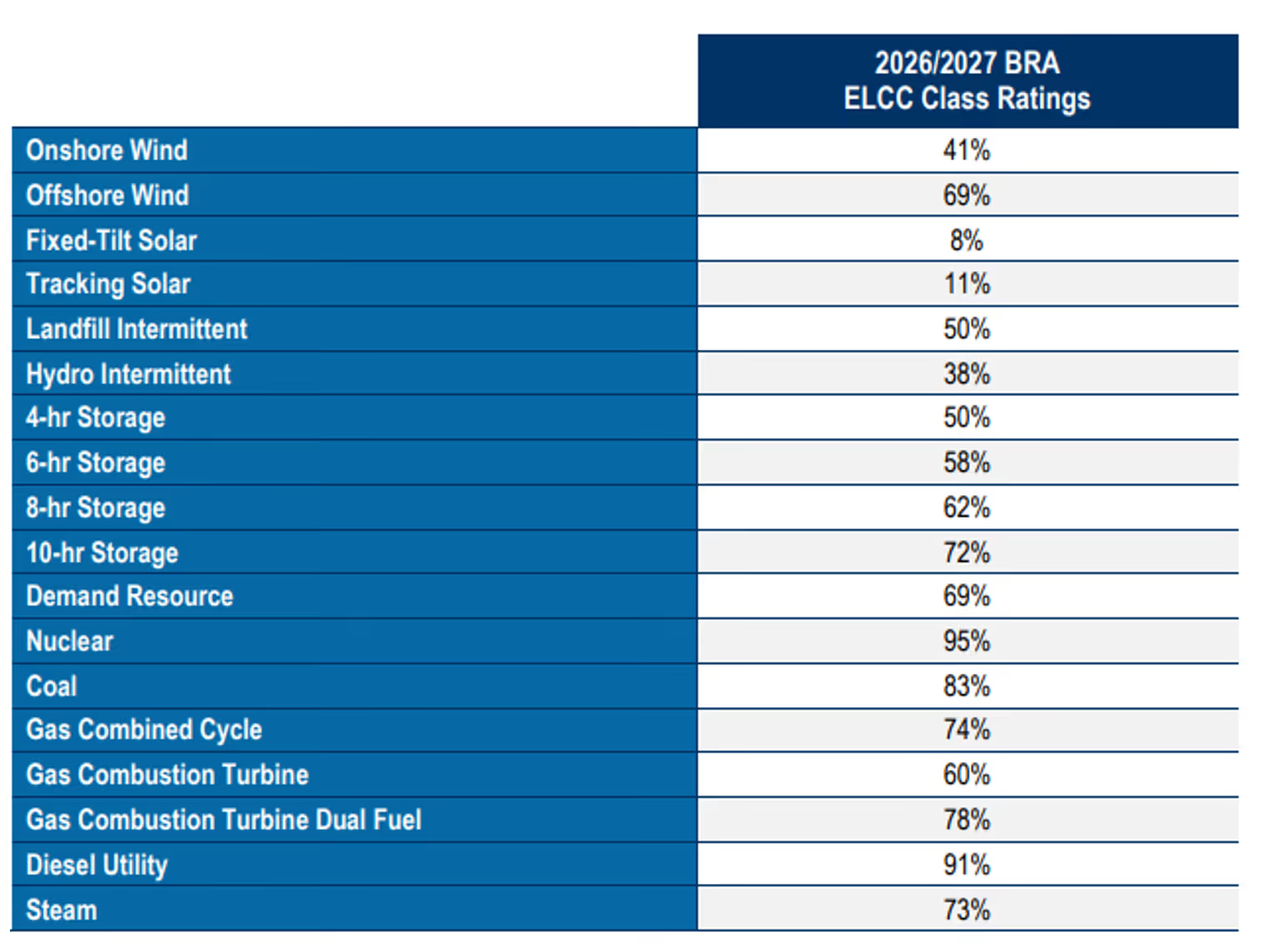

Each generation resource type (e.g. solar, wind, battery, natural gas, etc.) gets accredited at a rate below 100%, meaning that different resources will receive different fractions of the full capacity market price. Conversely, the capacity price set by a given resource will be larger than its missing money by the inverse of its accreditation (i.e. a resource with a 50% accreditation and a capacity revenue need of $30/kW-yr would need to bid a $60/kW-yr capacity market price). Figure 2 shows an example accreditation table from the PJM 2026/2027 capacity market auction.2

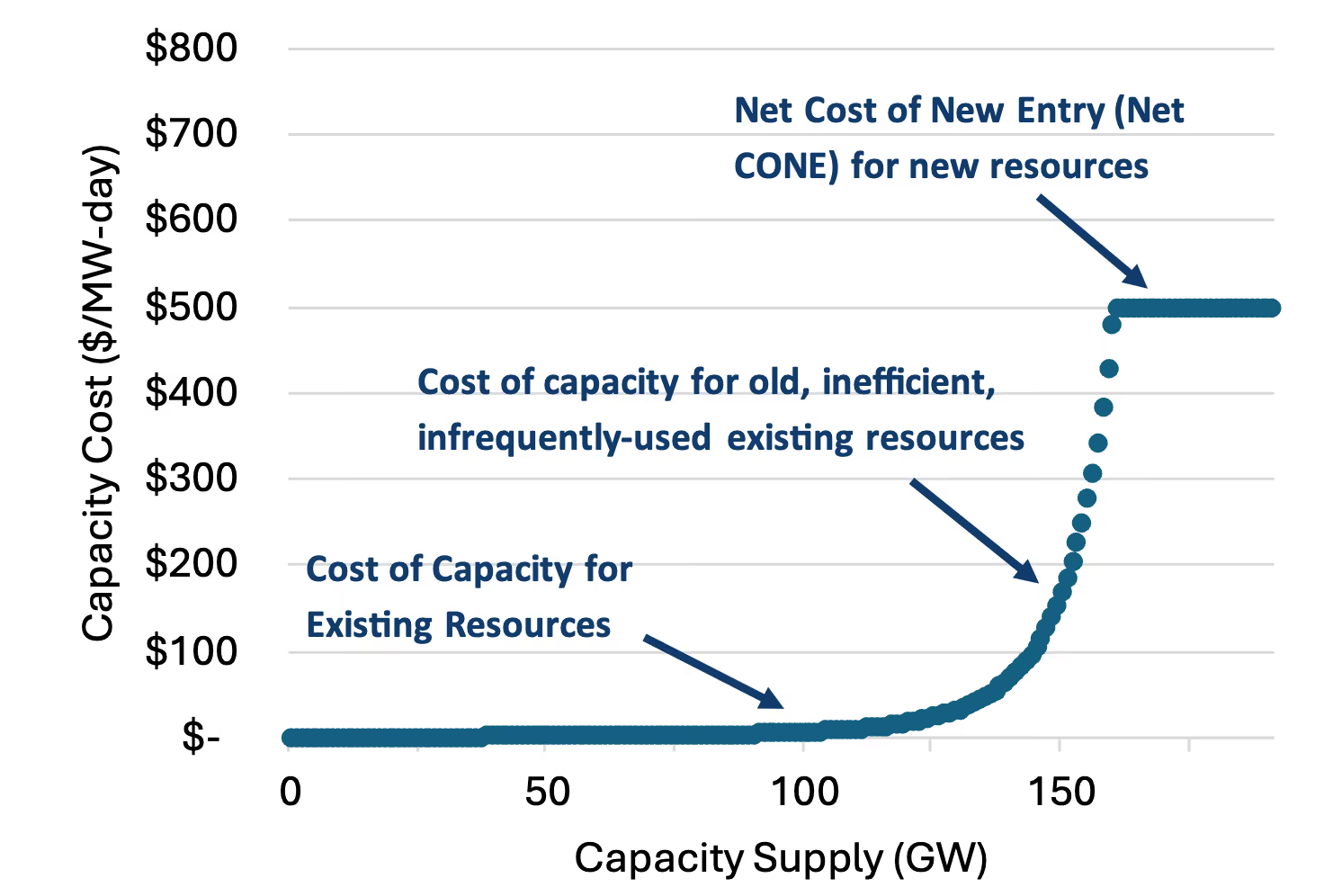

Figure 3 shows an illustrative capacity supply curve for a market like PJM. The lowest-cost resources are those that are already online, are depreciated, and that have relatively low fixed and variable costs. Infrequently-used peaking resources are next, requiring more revenue from the capacity market to compensate low margins in the energy market and higher maintenance costs as they age. Prices top out at the net cost of new entry (Net CONE) for generation resources that must recover their full revenue requirement (including CapEx) minus energy and ancillary revenues in order to justify coming online.

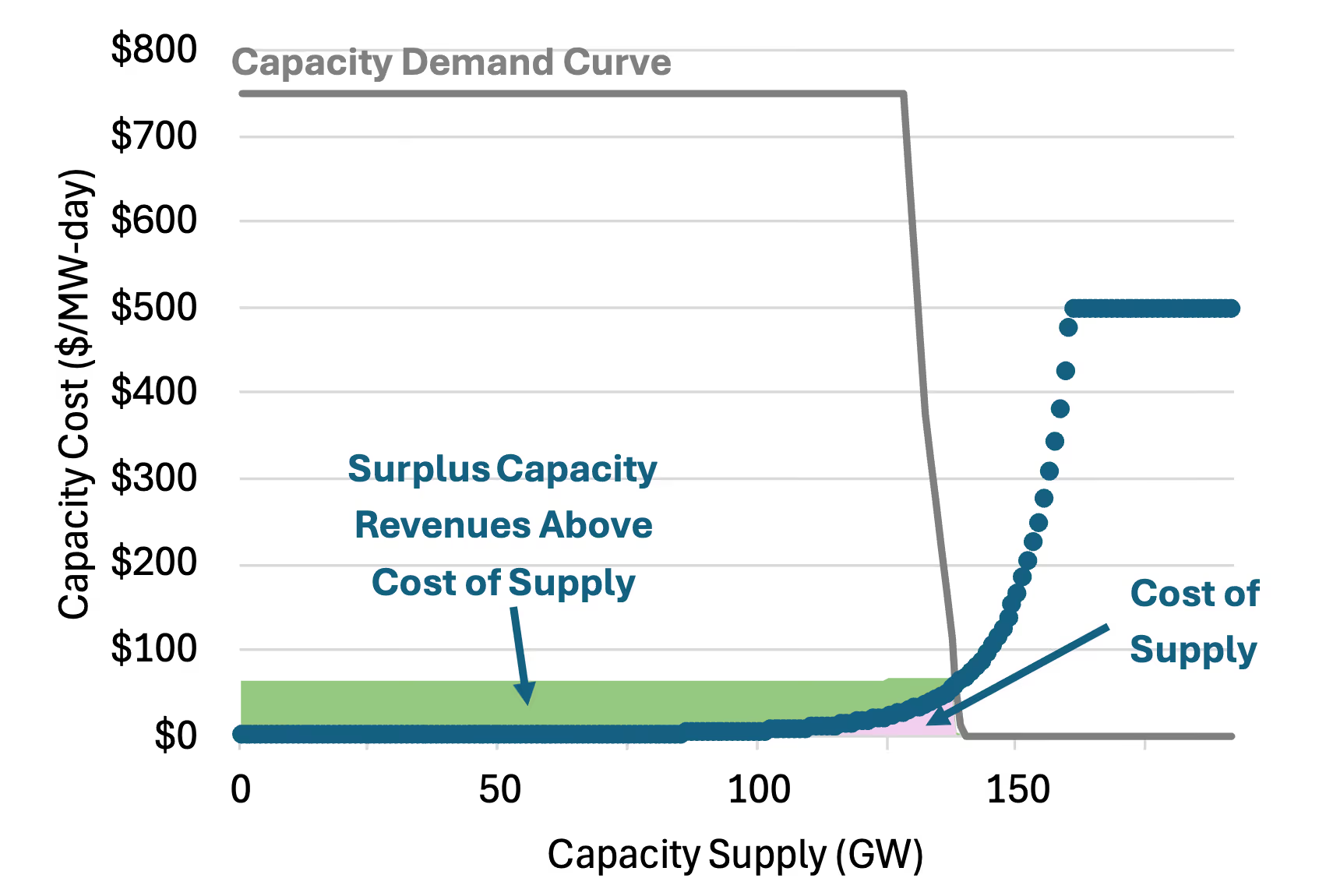

Because capacity markets pay a market clearing price to the entire capacity supply stack, lower-cost resources receive profits above their cost of supply. When the market holds excess supply and the clearing price is similar to the typical cost of capacity, this uplift cost is manageable and of a similar size to the cost of supply, as Figure 4 shows. This uplift in capacity costs beyond the cost of supply in competitive markets has historically been justified by the risk transfer for building new generation from ratepayers to private investors.

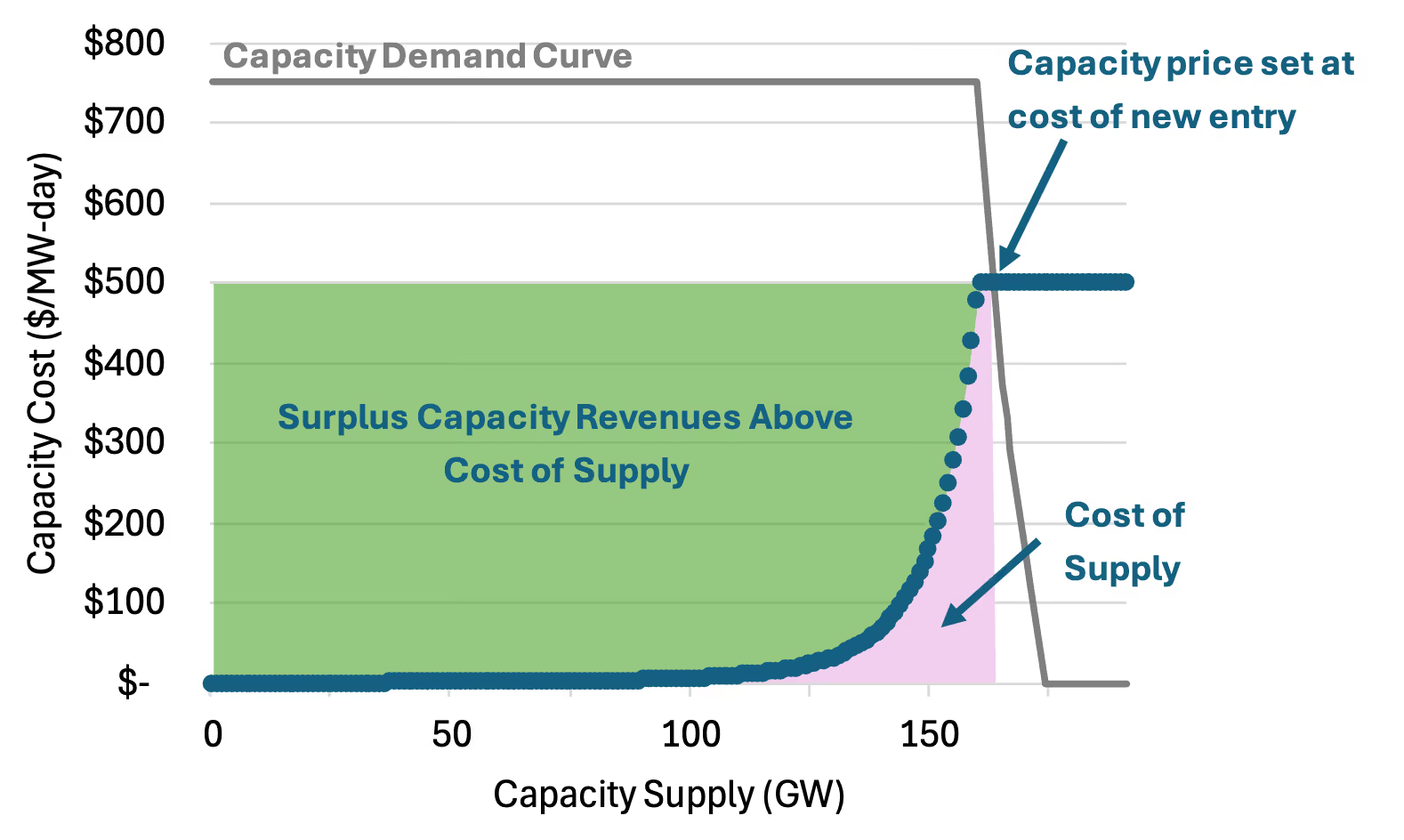

However, when demand growth and/or retirements cause capacity markets to run short on supply, capacity prices must rise to Net CONE (or a market-defined price cap that is some multiple of Net CONE if there is no new supply). When this occurs, the Net CONE price needed to incentivize even a small amount of new entry gets paid across the entire supply stack, leading to massive increases in capacity costs, as Figure 5 illustrates. In a market the size of PJM, for example, this added cost is on the order of $20 billion.

While this example is focused on capacity markets, the same phenomenon also occurs in ERCOT’s energy-only market. To bring new capacity online, sufficient scarcity revenue must be available in the market, but scarcity pricing is also paid across the entire energy supply stack when reserves run short (and not just to the new entry).

As retail electricity prices have risen throughout the country for a variety of reasons, a backlash has been growing among various electricity market stakeholders. This backlash has been most pronounced in deregulated areas, since utility-owned generation acts as a hedge against energy and capacity prices, receiving energy and capacity market revenues that offset the energy and capacity market costs incurred by load. As a result, several deregulated states have shown interest in re-regulating their utilities, with legislation to re-allow utility-owned generation either pending or under discussion.3

As Figure 5 illustrated, when new entry is required in a capacity market, the capacity market costs diverge wildly from the cost of supply that would be incurred in a regulated utility model, creating a strong incentive for states to re-regulate and allow utilities to own generation. If these regulated generation assets are bid into capacity markets as price-takers with a $0 bid, the entire capacity supply curve would shift to the right, allowing the market to increase supply without new entry setting high clearing prices.

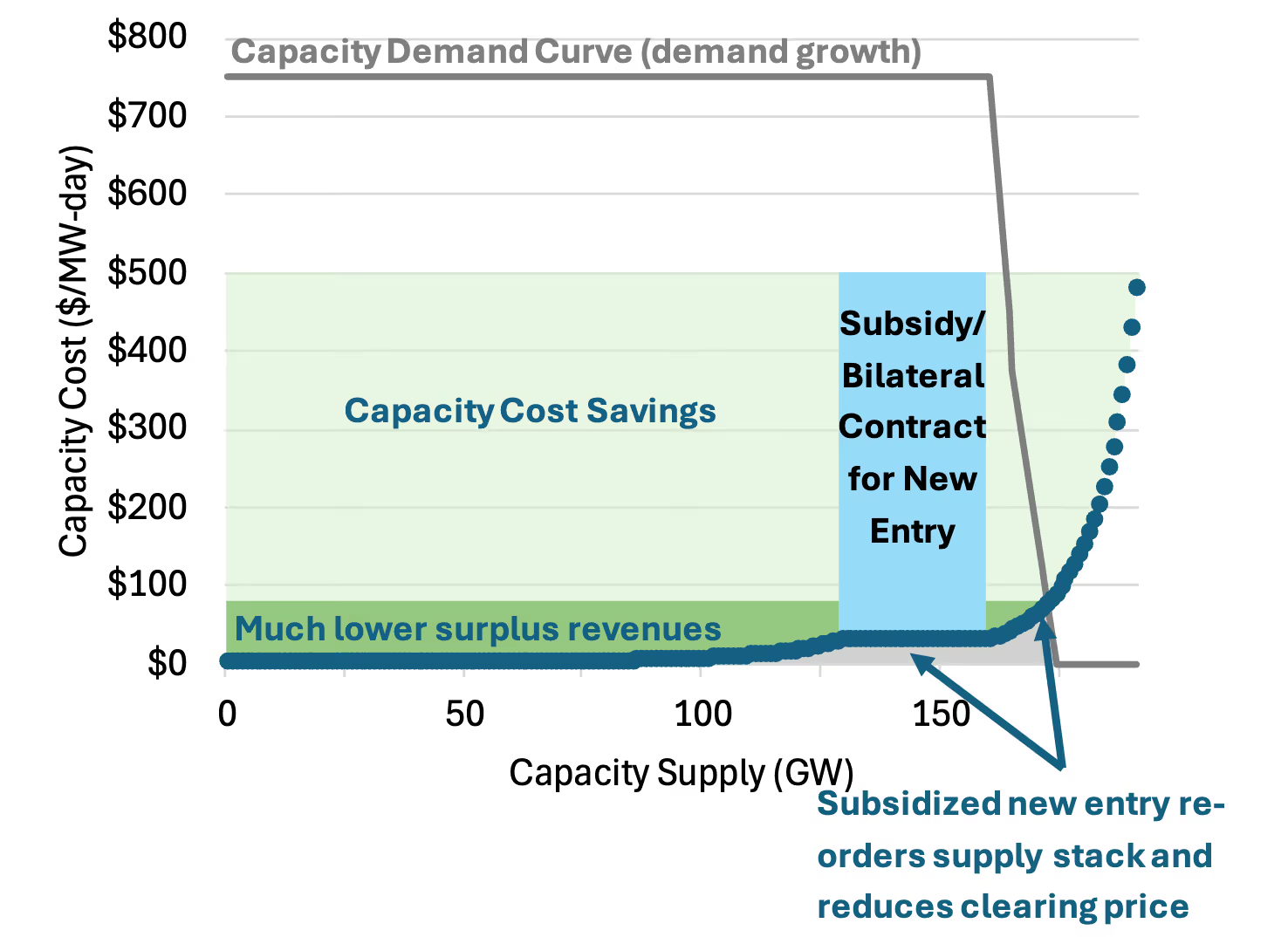

An alternative to re-regulation is for states to directly subsidize new entry and reduce the cost recovery these resources need from the capacity market, re-ordering the supply stack. As illustrated in Figure 6 the subsidized new entry can have a capacity cost similar to the existing resources in the capacity supply stack, thus allowing much lower market clearing prices. Each dollar that a subsidy reduces the missing money of a new entry resource gets further amplified by the accreditation of the resource. For example, a resource accredited at 50% with a capacity revenue need of $100/kW-yr would need a capacity price of $200/kW-yr, but a $40/kW-yr direct subsidy would reduce the revenue need to $60/kW-yr and yield a capacity price of$120/kW-yr, reducing capacity prices by double the size of the subsidy. In a market the size of PJM, a subsidy of a few billion dollars could reduce capacity market costs by around $20 billion dollars.

Subsidizing new entry may be of particular interest for states that have passed clean energy mandates and want to support new (clean)resources coming online without providing windfall profits to legacy fossil fuel generation resources.

Bilateral contracts for new entry can serve a similar role to subsidies, providing additional revenues to new entry and reducing the revenue need from the capacity market. At the 2025 CERAWeek conference, PJM’s CEO Manu Asthana acknowledged the need for such direct support and emphasized that the capacity market is intended to be a residual market rather than a full source of needed revenue, saying “We need to make sure people are transacting outside the market and are using the market as a residual source of balancing.”4

However, bilateral contracts can also result in opaque and inefficient markets that still result in elevated costs across the entire supply stack when legacy generators demand the same contract prices as new entry, as occurred during California’s recent resource adequacy shortage in the early and mid 2020s. New and expanded ancillary service products are another option to offset revenue needs from the capacity market.

Several states are already pursuing some of these approaches, including New York’s Index Storage Credit to subsidize new storage resources, Massachusett’s Clean Peak Standard to incentivize storage and renewables that can generate during peak conditions, California’s procurement orders that require utilities to contract with new clean capacity resources, and various state-level direct procurement programs underway or in development.5 Texas created the Texas Energy Fund to directly subsidize the financing costs of new dispatchable (i.e. natural gas) power plants while also creating a new ancillary service for dispatchable resources.6 Any state that wants to support an energy transition without seeing capacity market costs explode and providing a windfall to fossil fuel generators will also need to follow similar approaches.

Two other possible options exist to reduce capacity market costs: pay-as-bid structures instead of market-clearing prices, and multi-year contracts for new capacity market entrants. However, both have been considered and rejected by market operators and/or FERC.

The primary challenge with pay-as-bid market structures is that market participants will raise their bids to reflect what they anticipate the marginal price to be. In addition to adding extra costs and complexity to bidding, this can also result in inefficient and higher-cost resource selection, as some lower-cost resources will bid above the marginal price, thus re-ordering the supply curve and yielding higher prices than would occur in a market-clearing price model.7 Pay-as-bid structures also disadvantage smaller bidders, which face a higher risk than large bidders of missing out on clearing the market when raising their bids. If these bids are then mitigated back by the market operator, the purpose of having a market at all is severely undermined.

PJM and ISO-NE used to have three-year and seven-year price locks, respectively, in their capacity markets. However, FERC ordered their removal in 2020,8 ruling that price locks created discriminatory pricing, in which different resources would receive different prices for providing the same capacity product. Additionally, price locks distort capacity market prices during the price lock period and may disincentivize new unit entry.

Demand growth requires new unit entry, and supporting new unit entry requires cost recovery not just once but every year for the entire duration of that unit's useful life. If this cost recovery comes from capacity markets, capacity prices must rise to Net CONE. While this would be a boon to power generators, the scale of the escalation in market costs will become politically untenable and markets will risk dissolving. Moreover, states with clean energy mandates will need to replace existing fossil generation with new clean capacity without capacity markets providing a windfall to legacy fossil generation that disincentivizes retirement.

The only way to contain capacity market costs is to utilize mechanisms that funnel revenues solely to new entry without providing these same revenues to existing generation resources that do not need it to stay online. This can be done through re-regulation of utilities with a cost-of-service model or through direct subsidies/procurements/contracts for new capacity resources. State governments in locations without generation-owning regulated utilities should be actively exploring these avenues or else risk sustained high energy costs or market dissolution. Likewise, market operators should actively engage stakeholders to enact market reforms if they hope to keep the markets alive, though reforming without undermining market confidence among generators and investors will present its own challenges.

With power markets undergoing structural change and capacity supply dynamics rapidly changing, risks and opportunities abound for market participants. In this shifting environment, prudent investment requires new ways to look at markets and a balanced view. While potential changes to capacity markets and incentives for new entry are one implication of high capacity prices, Ascend will be covering additional strategic implications in several forthcoming papers.

___________________________

This publication is the second in a series from Ascend Analytics that considers the implications of rapid load growth on US capacity markets, high capacity prices as the new normal, the risks that new realities create for business-as-usual strategies, and the opportunities that this paradigm shift enables for well-planned new entry resources.

For much of the past two decades, flat load growth left most US power markets oversupplied with capacity, driving low prices both in capacity markets and in bilateral capacity contracts. When combined with low energy market prices driven by cheap natural gas and renewable deployment, low capacity prices led many aging thermal plants to retire, thus tightening supply just as load is being projected to return to robust growth.

However, rising load growth means the entire US has started to (or will soon) see the capacity markets become short for the first time in a generation. Moreover, whereas regulated utilities only recover supply costs, capacity markets pay a market-clearing price to all supply resources. When capacity prices rise to the level required to support new entry, these prices must be paid across the entire supply stack, causing capacity market costs to ratepayers to skyrocket and providing a windfall to existing supply resources.

As tightening conditions have begun pushing up capacity prices in some markets, political pushback and growing sensitivity to energy costs has ensued. Increasingly, stakeholders have been expressing concerns about the future of organized power markets, with some calling to dissolve the markets and re-regulate the power sector. Containing capacity costs without compromising the incentives needed to encourage new unit entry presents a significant challenge, with a limited set of viable solutions.

Shown in Figure 1, some parts of the US lack organized markets and instead have fully regulated utilities that receive cost-recovery from captive ratepayers for the costs of supply (primarily the non-California WECC and the Southeast, though some market expansion is coming to these regions).1 The remaining parts of the country have organized electricity markets and independent system operators (ISOs), in which market participants compete to provide the lowest-cost electricity throughout the day. Within these competitive markets, some states still have regulated utilities, including investor-owned utilities, public power entities, and electric co-operatives. Other states have fully deregulated the power sector, with publicly regulated transmission and distribution utilities but competitive retail power suppliers, along with competitive generation produced by Independent Power Producers (IPPs). The primary benefit of deregulated, competitive markets is that the investments risks associated with building power generation are borne by private investors rather than captive ratepayers. In most markets, both IPPs and at least some regulated utilities participate together within the market.

Most market participants bid something close to their variable cost of production in daily energy markets. This means that generation resources that are dispatched only on the highest demand days typically only recover their variable costs but still need a way to recover their fixed costs and/or capital expenditures (CapEx). Regulated utilities can recover these costs directly from ratepayers, but IPPs and other market participants need another revenue mechanism to provide this ‘missing money’ that is needed to incentivize these resources to be built in a market and be available when the grid needs supply.

Each market has a different structure for providing these missing revenues. Load-serving entities in SPP and CAISO (roughly 14% of national electric load) must either own or enter into bilateral contracts with sufficient generation to cover their load, though in SPP the requirement comes from the market operator, whereas in California the requirement primarily comes from the state utility commission. ERCOT (roughly 12% of national electric load) has an ‘energy-only’ market but creates just-in-time capacity revenues through a $5,000/MWh price cap and price adders when reserves run scarce. ERCOT also has increased its procurement of ancillary services and created new ancillary services to provide additional revenues to reliability resources.

The remaining markets (roughly 40% of national electric load)all have some form of capacity market structure, in which capacity auctions are held in advance of a given planning year to ensure enough capacity is procured to meet projected demand, and in which all the supply in the market is paid a market-clearing price. MISO consists of mostly regulated utilities, and its capacity auction is optional, with ~90% of load opting out and choosing instead to self-supply capacity through generation owned by the regulated utilities. PJM, ISO-NE, and NYISO have traditional capacity market structures, with lead times ranging from three years (PJM) to one year (ISO-NE and NYISO).

Each generation resource type (e.g. solar, wind, battery, natural gas, etc.) gets accredited at a rate below 100%, meaning that different resources will receive different fractions of the full capacity market price. Conversely, the capacity price set by a given resource will be larger than its missing money by the inverse of its accreditation (i.e. a resource with a 50% accreditation and a capacity revenue need of $30/kW-yr would need to bid a $60/kW-yr capacity market price). Figure 2 shows an example accreditation table from the PJM 2026/2027 capacity market auction.2

Figure 3 shows an illustrative capacity supply curve for a market like PJM. The lowest-cost resources are those that are already online, are depreciated, and that have relatively low fixed and variable costs. Infrequently-used peaking resources are next, requiring more revenue from the capacity market to compensate low margins in the energy market and higher maintenance costs as they age. Prices top out at the net cost of new entry (Net CONE) for generation resources that must recover their full revenue requirement (including CapEx) minus energy and ancillary revenues in order to justify coming online.

Because capacity markets pay a market clearing price to the entire capacity supply stack, lower-cost resources receive profits above their cost of supply. When the market holds excess supply and the clearing price is similar to the typical cost of capacity, this uplift cost is manageable and of a similar size to the cost of supply, as Figure 4 shows. This uplift in capacity costs beyond the cost of supply in competitive markets has historically been justified by the risk transfer for building new generation from ratepayers to private investors.

However, when demand growth and/or retirements cause capacity markets to run short on supply, capacity prices must rise to Net CONE (or a market-defined price cap that is some multiple of Net CONE if there is no new supply). When this occurs, the Net CONE price needed to incentivize even a small amount of new entry gets paid across the entire supply stack, leading to massive increases in capacity costs, as Figure 5 illustrates. In a market the size of PJM, for example, this added cost is on the order of $20 billion.

While this example is focused on capacity markets, the same phenomenon also occurs in ERCOT’s energy-only market. To bring new capacity online, sufficient scarcity revenue must be available in the market, but scarcity pricing is also paid across the entire energy supply stack when reserves run short (and not just to the new entry).

As retail electricity prices have risen throughout the country for a variety of reasons, a backlash has been growing among various electricity market stakeholders. This backlash has been most pronounced in deregulated areas, since utility-owned generation acts as a hedge against energy and capacity prices, receiving energy and capacity market revenues that offset the energy and capacity market costs incurred by load. As a result, several deregulated states have shown interest in re-regulating their utilities, with legislation to re-allow utility-owned generation either pending or under discussion.3

As Figure 5 illustrated, when new entry is required in a capacity market, the capacity market costs diverge wildly from the cost of supply that would be incurred in a regulated utility model, creating a strong incentive for states to re-regulate and allow utilities to own generation. If these regulated generation assets are bid into capacity markets as price-takers with a $0 bid, the entire capacity supply curve would shift to the right, allowing the market to increase supply without new entry setting high clearing prices.

An alternative to re-regulation is for states to directly subsidize new entry and reduce the cost recovery these resources need from the capacity market, re-ordering the supply stack. As illustrated in Figure 6 the subsidized new entry can have a capacity cost similar to the existing resources in the capacity supply stack, thus allowing much lower market clearing prices. Each dollar that a subsidy reduces the missing money of a new entry resource gets further amplified by the accreditation of the resource. For example, a resource accredited at 50% with a capacity revenue need of $100/kW-yr would need a capacity price of $200/kW-yr, but a $40/kW-yr direct subsidy would reduce the revenue need to $60/kW-yr and yield a capacity price of$120/kW-yr, reducing capacity prices by double the size of the subsidy. In a market the size of PJM, a subsidy of a few billion dollars could reduce capacity market costs by around $20 billion dollars.

Subsidizing new entry may be of particular interest for states that have passed clean energy mandates and want to support new (clean)resources coming online without providing windfall profits to legacy fossil fuel generation resources.

Bilateral contracts for new entry can serve a similar role to subsidies, providing additional revenues to new entry and reducing the revenue need from the capacity market. At the 2025 CERAWeek conference, PJM’s CEO Manu Asthana acknowledged the need for such direct support and emphasized that the capacity market is intended to be a residual market rather than a full source of needed revenue, saying “We need to make sure people are transacting outside the market and are using the market as a residual source of balancing.”4

However, bilateral contracts can also result in opaque and inefficient markets that still result in elevated costs across the entire supply stack when legacy generators demand the same contract prices as new entry, as occurred during California’s recent resource adequacy shortage in the early and mid 2020s. New and expanded ancillary service products are another option to offset revenue needs from the capacity market.

Several states are already pursuing some of these approaches, including New York’s Index Storage Credit to subsidize new storage resources, Massachusett’s Clean Peak Standard to incentivize storage and renewables that can generate during peak conditions, California’s procurement orders that require utilities to contract with new clean capacity resources, and various state-level direct procurement programs underway or in development.5 Texas created the Texas Energy Fund to directly subsidize the financing costs of new dispatchable (i.e. natural gas) power plants while also creating a new ancillary service for dispatchable resources.6 Any state that wants to support an energy transition without seeing capacity market costs explode and providing a windfall to fossil fuel generators will also need to follow similar approaches.

Two other possible options exist to reduce capacity market costs: pay-as-bid structures instead of market-clearing prices, and multi-year contracts for new capacity market entrants. However, both have been considered and rejected by market operators and/or FERC.

The primary challenge with pay-as-bid market structures is that market participants will raise their bids to reflect what they anticipate the marginal price to be. In addition to adding extra costs and complexity to bidding, this can also result in inefficient and higher-cost resource selection, as some lower-cost resources will bid above the marginal price, thus re-ordering the supply curve and yielding higher prices than would occur in a market-clearing price model.7 Pay-as-bid structures also disadvantage smaller bidders, which face a higher risk than large bidders of missing out on clearing the market when raising their bids. If these bids are then mitigated back by the market operator, the purpose of having a market at all is severely undermined.

PJM and ISO-NE used to have three-year and seven-year price locks, respectively, in their capacity markets. However, FERC ordered their removal in 2020,8 ruling that price locks created discriminatory pricing, in which different resources would receive different prices for providing the same capacity product. Additionally, price locks distort capacity market prices during the price lock period and may disincentivize new unit entry.

Demand growth requires new unit entry, and supporting new unit entry requires cost recovery not just once but every year for the entire duration of that unit's useful life. If this cost recovery comes from capacity markets, capacity prices must rise to Net CONE. While this would be a boon to power generators, the scale of the escalation in market costs will become politically untenable and markets will risk dissolving. Moreover, states with clean energy mandates will need to replace existing fossil generation with new clean capacity without capacity markets providing a windfall to legacy fossil generation that disincentivizes retirement.

The only way to contain capacity market costs is to utilize mechanisms that funnel revenues solely to new entry without providing these same revenues to existing generation resources that do not need it to stay online. This can be done through re-regulation of utilities with a cost-of-service model or through direct subsidies/procurements/contracts for new capacity resources. State governments in locations without generation-owning regulated utilities should be actively exploring these avenues or else risk sustained high energy costs or market dissolution. Likewise, market operators should actively engage stakeholders to enact market reforms if they hope to keep the markets alive, though reforming without undermining market confidence among generators and investors will present its own challenges.

With power markets undergoing structural change and capacity supply dynamics rapidly changing, risks and opportunities abound for market participants. In this shifting environment, prudent investment requires new ways to look at markets and a balanced view. While potential changes to capacity markets and incentives for new entry are one implication of high capacity prices, Ascend will be covering additional strategic implications in several forthcoming papers.

___________________________

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

.avif)

-1-ercot%20image.avif)

%20(1).avif)