Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

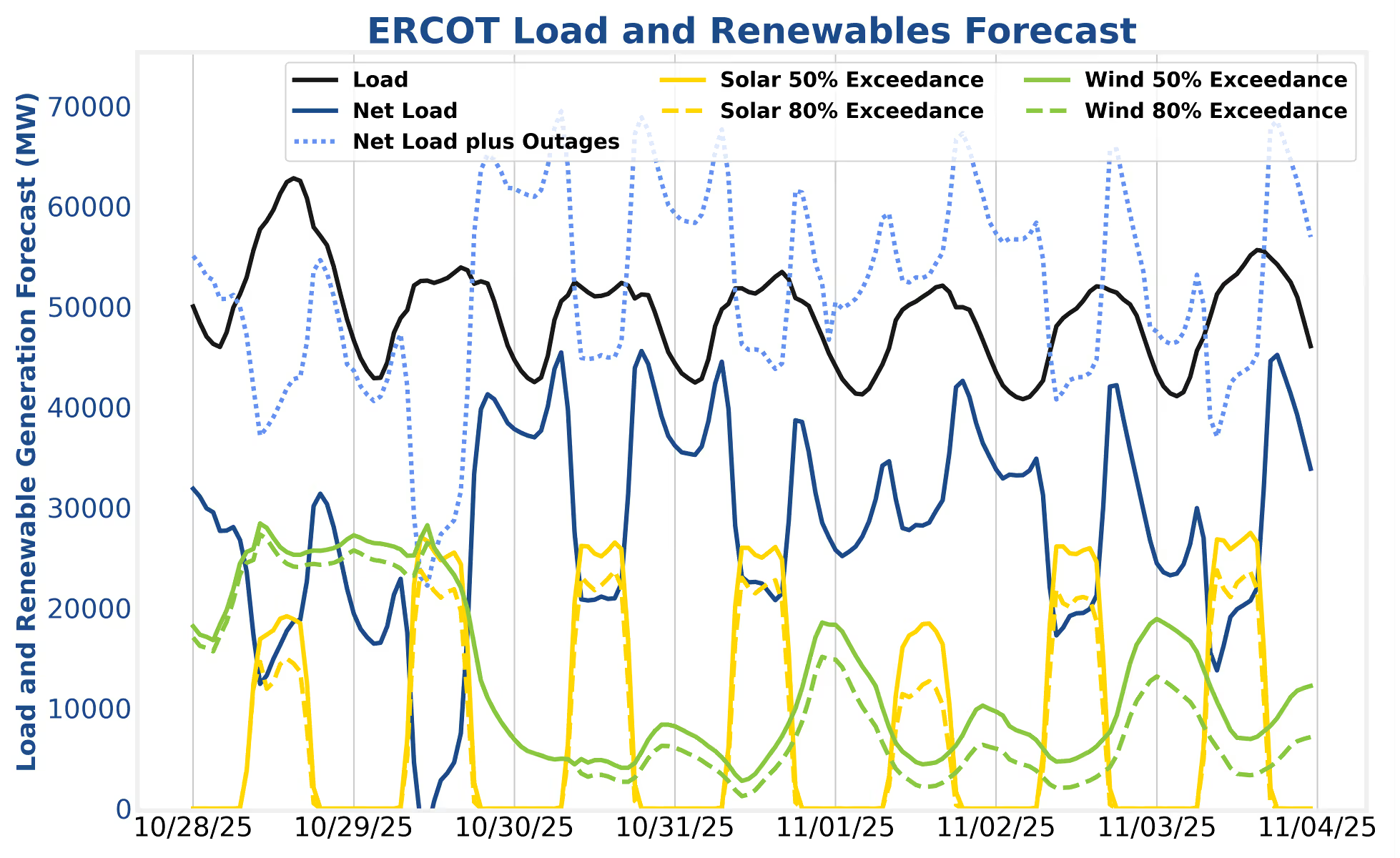

For the week of October 29th – November 4th: Charging dynamics will be interesting, and largely profitable, throughout ERCOT today before a 40 GW net load ramp into this evening. CAISO will continue to rinse and repeat.

In ERCOT, operators should clear their SoC this morning to be able to fully charge over negative prices throughout the western, renewable-heavy portions of the state. The 40 GW net load ramp this evening could induce localized price spikes as the solar and wind fleets ramp down coincidently.

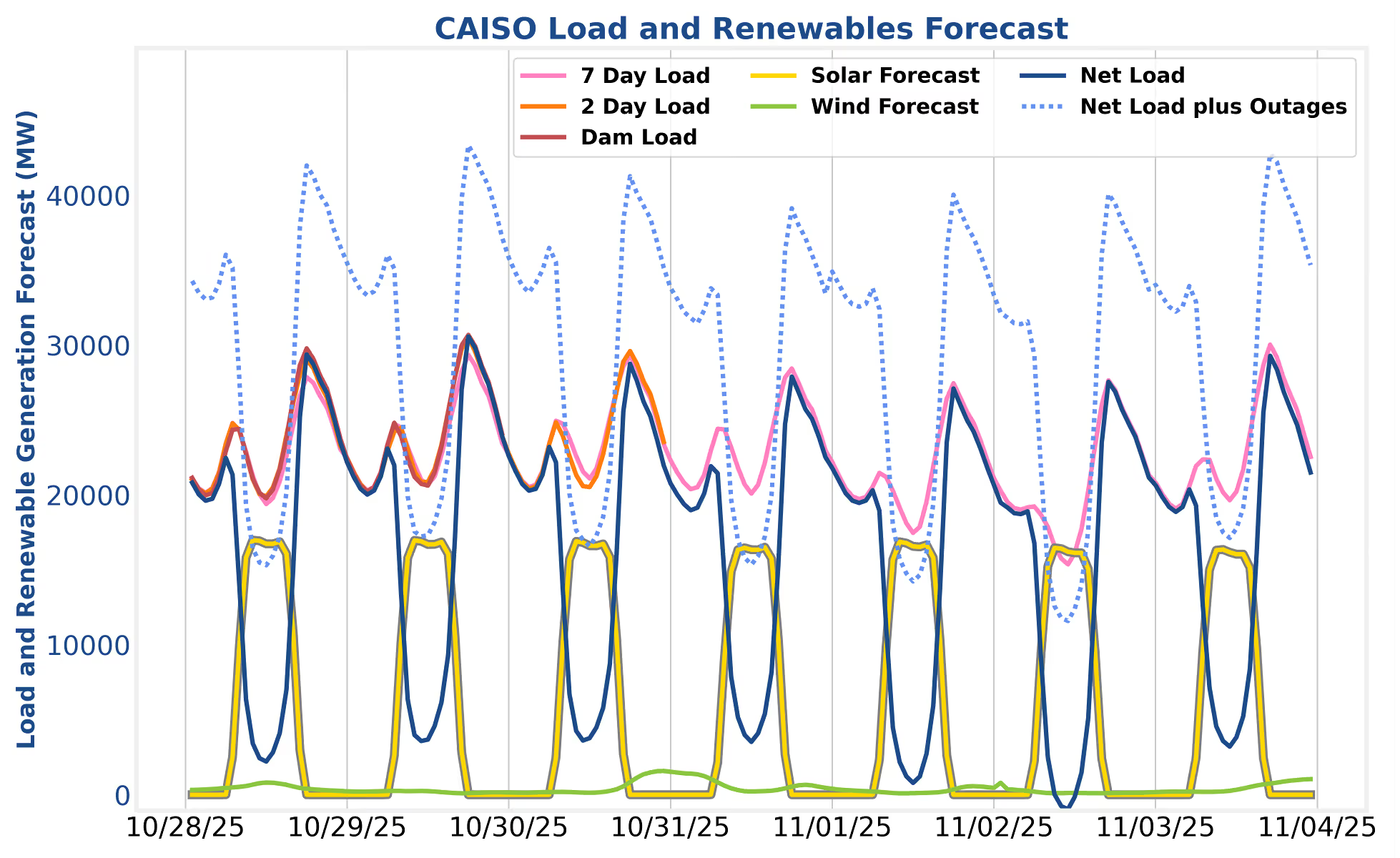

In CAISO, solar production and gross load are projected to be quite steady over the forecastable horizon. Operators should continue to target energy arbitrage and regulation.

Charging prices will be negative at many nodes across ERCOT today as extremely strong wind production persists through the solar ramp up. Then, wind and solar will ramp down coincidently as thermal and batteries manage a ~40 GW net load ramp over the course of a few hours. It may be a fun afternoon for the ERCOT operators. Gross load will be substantially lower during the peaks beginning on the 29th. Real-time energy exposure has continued to provide the highest revenues in ERCOT as of late. Operators should continue targeting real-time energy and non-spin. Preserving flexibility for morning peaks should be a day-to-day consideration as well. Oftentimes, overnight ancillary services (AS) at $1/MW is not worth missing a morning peak opportunity. Mt. Blue Sky is the recommended SmartBidder strategy.

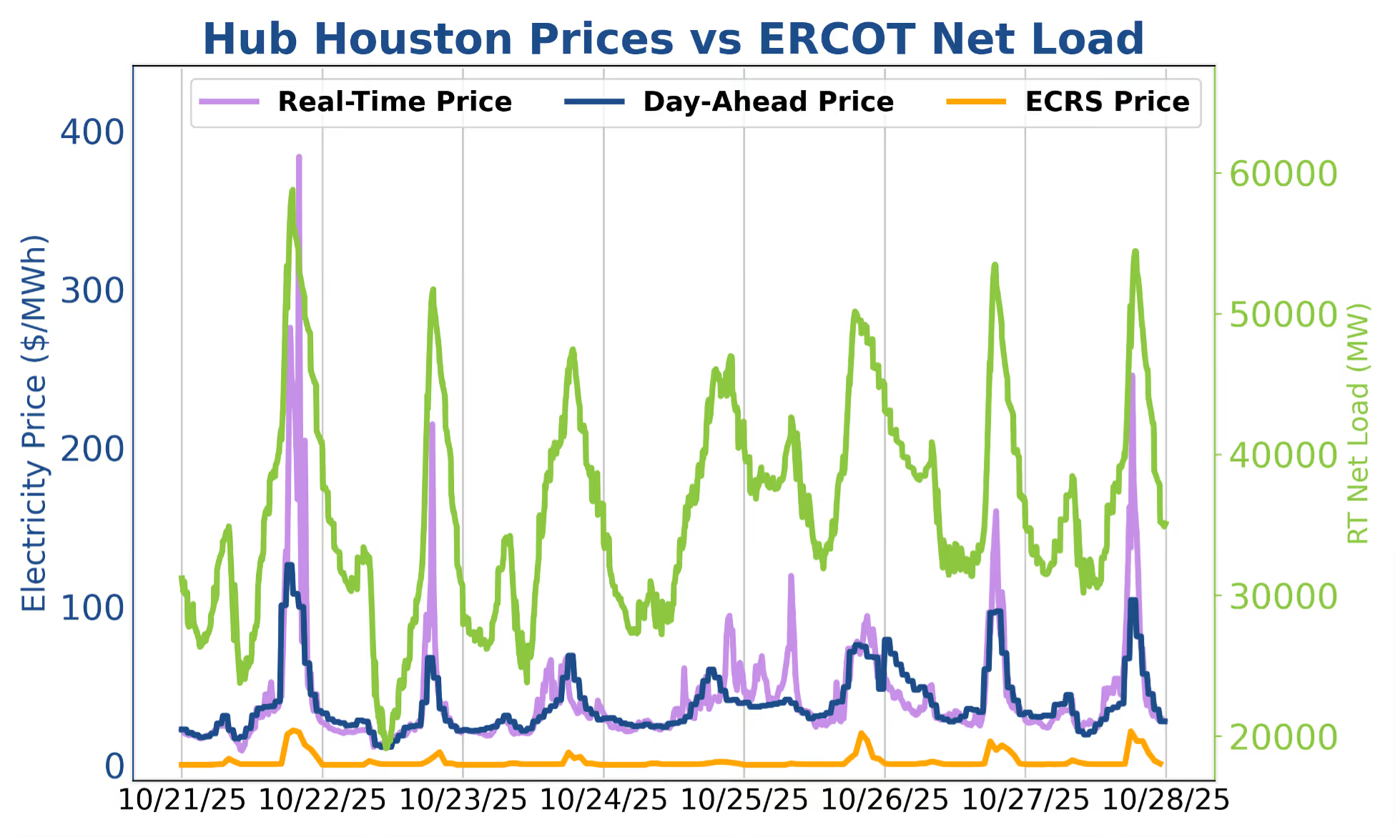

Last week in ERCOT a combination of outages and uncertainty in renewable production led to high real-time prices throughout the week. The largest spike came on the evening of the 21st after renewable production ramped down quickly and outages remained above 20GW, leading to 56GW of net load and sustained real-time prices above $200/MWh. We saw similar (albeit smaller) spikes on the evenings of the 22nd, 25th and 26th when net load came in around 50GW. As temperatures drop and more storms roll through, operators should look to save SOC (or charge with reg-down in the afternoon) for discharge into these evening peaks, while those with stricter cycling constraints can utilize reg-up to gain similar exposure.

Most of last week’s outages are still in place, which could combine with low wind production to inflate prices. The solar production forecast is relatively flat with the best chance to charge at negative prices coming midday on November 2nd. On other days, operators will have to manage and distribute SoC effectively across morning and evening peaks, especially when the net load plus outages is forecasted near 40GW on October 29th and 30th as well as November 3rd. These are also the best days to save SoC for morning and evening price spikes in the real-time market, even though it can be hard to ignore day-ahead prices that consistently come in above $50/MWh. With the potential for high prices on either side of solar hours, now is a great time to work with your analyst to configure a fall/winter strategy that optimizes SoC to capture maximum value in both morning and evening peaks without over cycling.

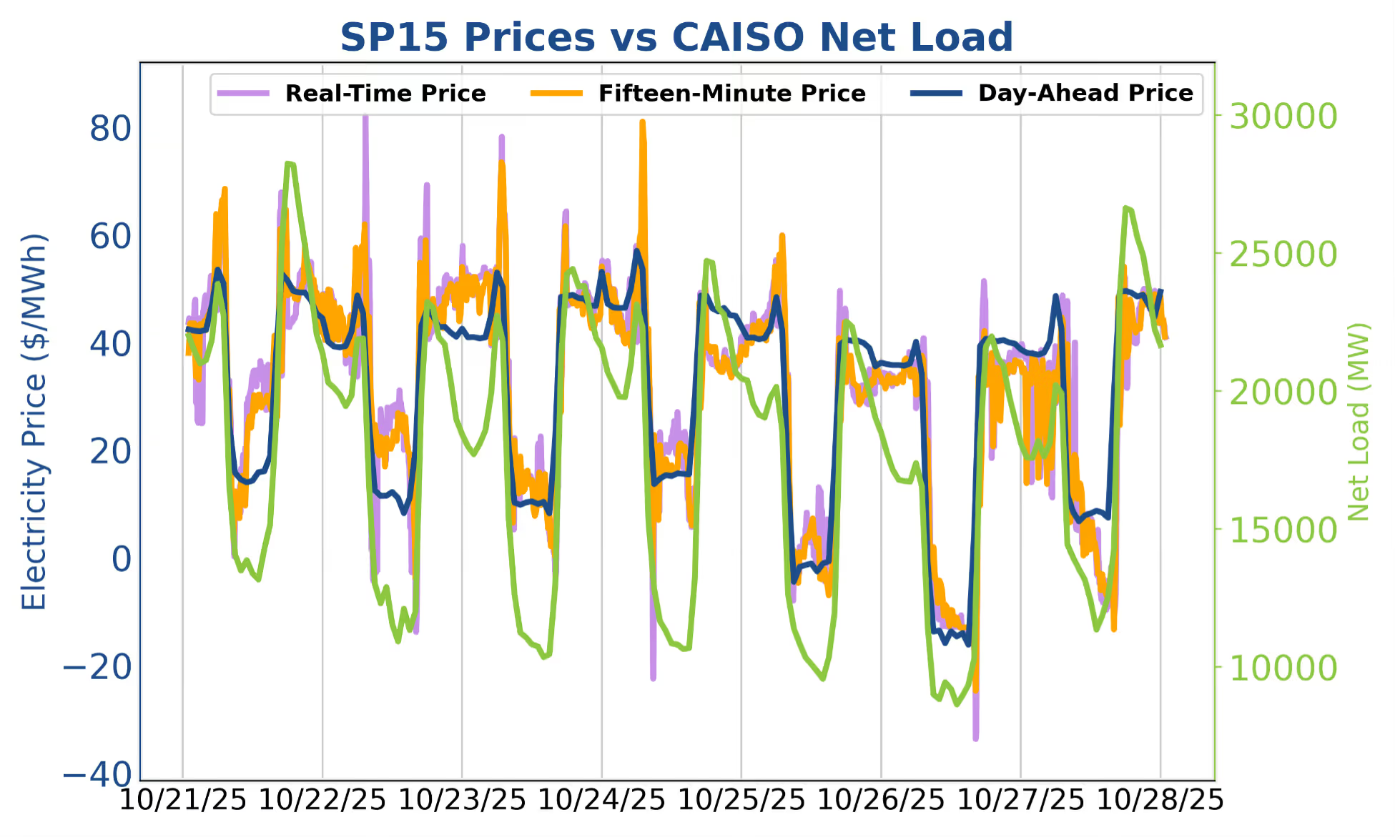

Halloween decorations are popping up everywhere, and CAISO’s morning peaks are right there with them. Last week featured strong morning prices in both the day-ahead and real-time markets, which means there are multiple approaches to maximizing revenue through the end of fall and into the winter season. Operators hoping to capture the full upside of real-time price spikes may want to shift their focus (and SoC) to the early morning hours between 4:00 and 7:00am where we saw spikes of varying magnitudes on the 21st through the 25th. At the same time, days like October 26th, which had predictable negative midday charging prices, offer great opportunities to discharge into both peaks while supplementing revenue and building SoC during solar hours.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of October 29th – November 4th: Charging dynamics will be interesting, and largely profitable, throughout ERCOT today before a 40 GW net load ramp into this evening. CAISO will continue to rinse and repeat.

In ERCOT, operators should clear their SoC this morning to be able to fully charge over negative prices throughout the western, renewable-heavy portions of the state. The 40 GW net load ramp this evening could induce localized price spikes as the solar and wind fleets ramp down coincidently.

In CAISO, solar production and gross load are projected to be quite steady over the forecastable horizon. Operators should continue to target energy arbitrage and regulation.

Charging prices will be negative at many nodes across ERCOT today as extremely strong wind production persists through the solar ramp up. Then, wind and solar will ramp down coincidently as thermal and batteries manage a ~40 GW net load ramp over the course of a few hours. It may be a fun afternoon for the ERCOT operators. Gross load will be substantially lower during the peaks beginning on the 29th. Real-time energy exposure has continued to provide the highest revenues in ERCOT as of late. Operators should continue targeting real-time energy and non-spin. Preserving flexibility for morning peaks should be a day-to-day consideration as well. Oftentimes, overnight ancillary services (AS) at $1/MW is not worth missing a morning peak opportunity. Mt. Blue Sky is the recommended SmartBidder strategy.

Last week in ERCOT a combination of outages and uncertainty in renewable production led to high real-time prices throughout the week. The largest spike came on the evening of the 21st after renewable production ramped down quickly and outages remained above 20GW, leading to 56GW of net load and sustained real-time prices above $200/MWh. We saw similar (albeit smaller) spikes on the evenings of the 22nd, 25th and 26th when net load came in around 50GW. As temperatures drop and more storms roll through, operators should look to save SOC (or charge with reg-down in the afternoon) for discharge into these evening peaks, while those with stricter cycling constraints can utilize reg-up to gain similar exposure.

Most of last week’s outages are still in place, which could combine with low wind production to inflate prices. The solar production forecast is relatively flat with the best chance to charge at negative prices coming midday on November 2nd. On other days, operators will have to manage and distribute SoC effectively across morning and evening peaks, especially when the net load plus outages is forecasted near 40GW on October 29th and 30th as well as November 3rd. These are also the best days to save SoC for morning and evening price spikes in the real-time market, even though it can be hard to ignore day-ahead prices that consistently come in above $50/MWh. With the potential for high prices on either side of solar hours, now is a great time to work with your analyst to configure a fall/winter strategy that optimizes SoC to capture maximum value in both morning and evening peaks without over cycling.

Halloween decorations are popping up everywhere, and CAISO’s morning peaks are right there with them. Last week featured strong morning prices in both the day-ahead and real-time markets, which means there are multiple approaches to maximizing revenue through the end of fall and into the winter season. Operators hoping to capture the full upside of real-time price spikes may want to shift their focus (and SoC) to the early morning hours between 4:00 and 7:00am where we saw spikes of varying magnitudes on the 21st through the 25th. At the same time, days like October 26th, which had predictable negative midday charging prices, offer great opportunities to discharge into both peaks while supplementing revenue and building SoC during solar hours.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)