Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

In ERCOT, operators should strongly consider taking on additional day-ahead ancillary services (AS) revenue, as there has been a substantial premium for day-ahead AS so far. This opportunity will remain until market participants begin selling more day-ahead AS.

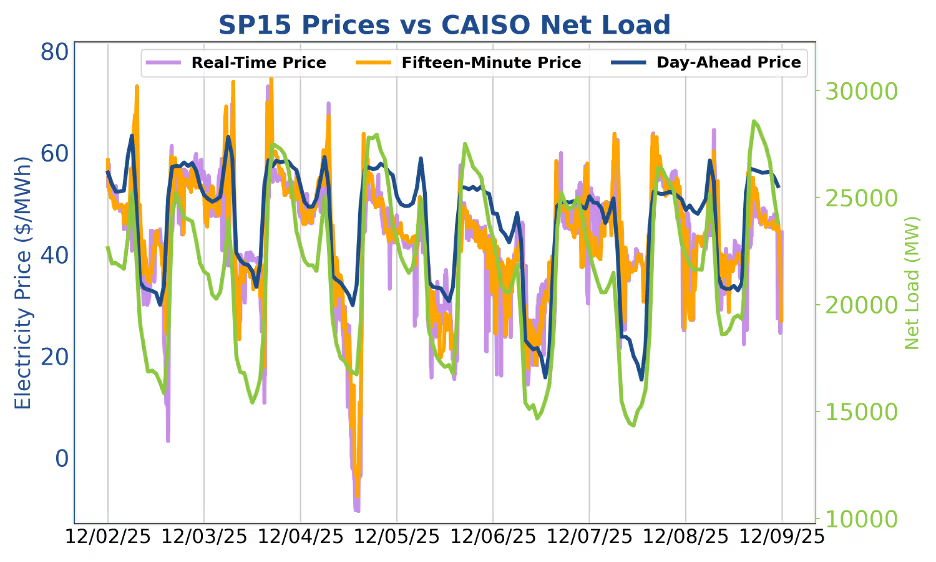

In CAISO, operators should consider day-ahead charging in SP15 but real-time charging in NP15, as there has been minimal path 15 congestion in the real-time markets this December. Discharging in day-ahead energy will generally be more lucrative than real-time energy.

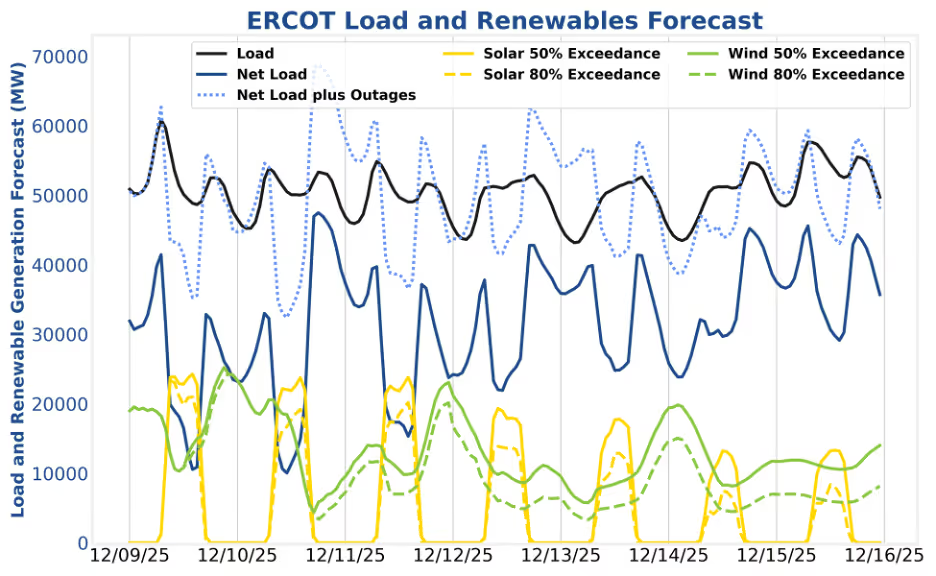

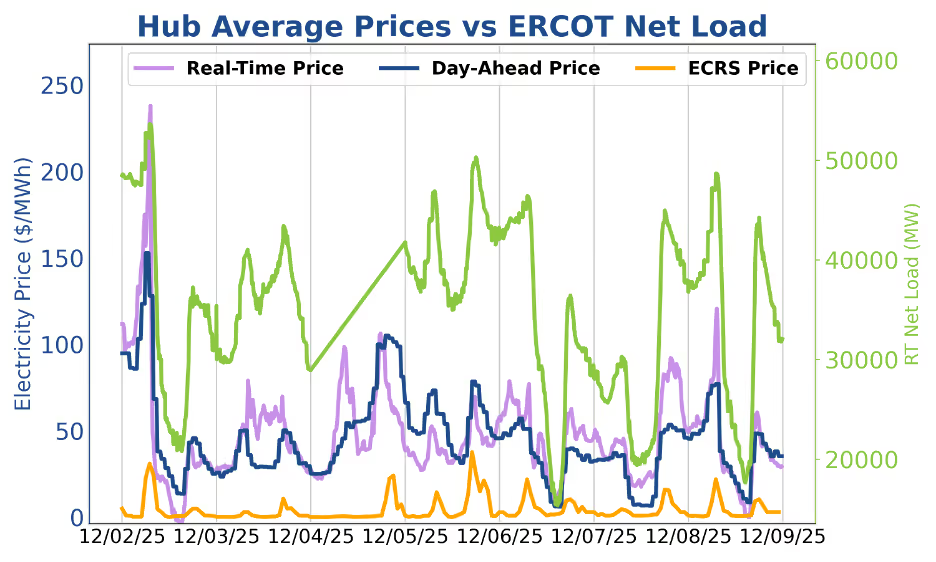

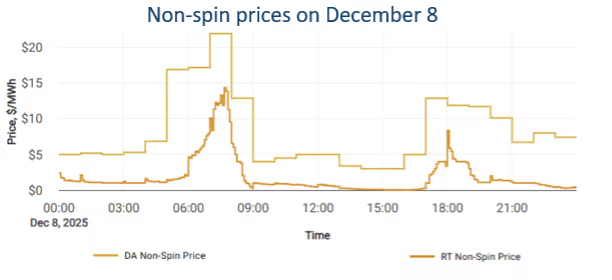

The ERCOT market transitioned to the RTC+B paradigm overnight last Thursday without a hitch. While the energy markets stayed steady throughout the change, the most notable impact has been elevated day-ahead ancillary service prices, particularly non-spin, as many market participants have shifted away from day-ahead AS and towards the “new kid on the block” real-time (RT) AS products. The RT AS products have been driven into the ground primarily due to 1) day-ahead AS participants switched to RT AS and 2) market participants who previously refrained from entertaining the commitment of day-ahead AS feel much more comfortable considering RT AS that they can switch in and out of on a five minute basis.

At the moment, there is a lot of money to be made in day-ahead AS. For operators concerned about honoring RUC SoC and duration requirements, the SmartBidder optimization in day-ahead and real-time is fully capable of handling RUC feasibility and can limit day-ahead AS offers in accordance with RUC requirements. The optimization is also fully capable of covering day-ahead AS awards in real-time. Talk to your analyst about the various options SmartBidder has to participate in day-ahead AS in a risk-adjusted manner to maximize revenue.

Day-ahead AS prices have been the RTC+B winner so far. Importantly, even when real-time energy prices have eclipsed day-ahead energy prices, real-time AS prices have still been far lower than day-ahead AS prices. This signals that there is a current structural inefficiency where market participants are much warier about taking on day-ahead AS relative to RT AS. While this is expected to some degree (proportional to energy spreads), the degree of day-ahead dominance points towards battery operators being overly conservative about taking on day-ahead AS positions. This inefficiency should begin to iron out over the coming weeks as the market reacts. The major caveat is that there has still been no test of how RT AS prices will respond when the battery fleet depletes its SoC fully. Keep an eye out for the first morning/evening when RT energy prices are strong enough for a full discharge.

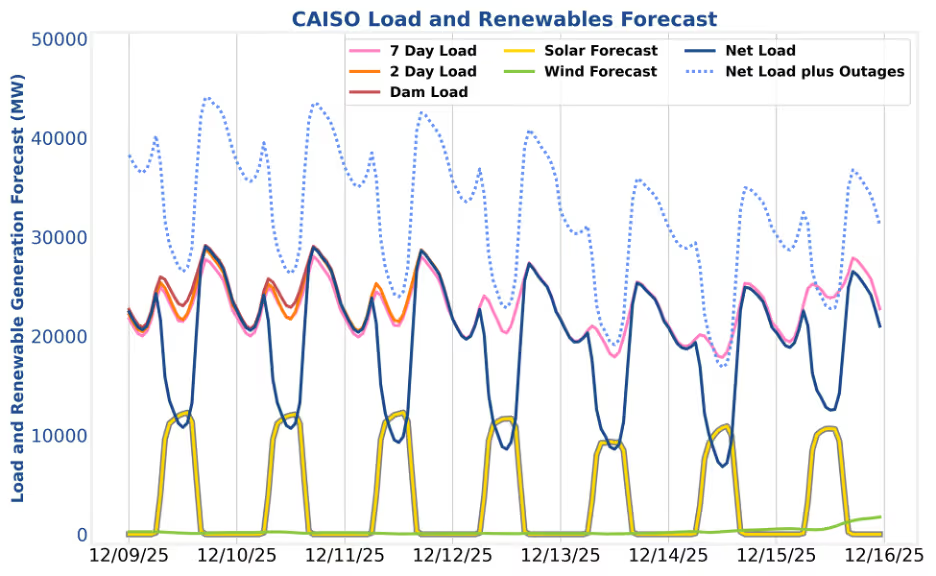

Expect this week in CAISO to be like the previous two. Peak net loads are not forecast to break 30GW, and solar generation remains consistent throughout. Energy arbitrage is once again the best way to maximize revenue utilizing TB4 as a solid base strategy. Capture more upside by opportunistically trading in both the day-ahead and real-time markets when the DART spread is positive in charging hours and negative in discharging hours. SmartBidder’s Mt. Shasta strategy accounts for all of these dynamics. Additionally, look for increased congestion along Path 15 to provide cheap day-ahead charging opportunities for SP15 operators. This emerging dynamic is described in more detail below.

Market conditions have been quiet in CAISO as net load levels have been low and congestion has been limited, partially due to more limited winter solar production. The day-ahead market is pricing in more congestion than the real-time market. If this continues, expect lower real-time prices in NP15 relative to higher real-time prices in NP15 (relative to day-ahead pricing thresholds). Operators should focus on energy arbitrage and regulation down to grind out additional revenue for the rest of 2025.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

In ERCOT, operators should strongly consider taking on additional day-ahead ancillary services (AS) revenue, as there has been a substantial premium for day-ahead AS so far. This opportunity will remain until market participants begin selling more day-ahead AS.

In CAISO, operators should consider day-ahead charging in SP15 but real-time charging in NP15, as there has been minimal path 15 congestion in the real-time markets this December. Discharging in day-ahead energy will generally be more lucrative than real-time energy.

The ERCOT market transitioned to the RTC+B paradigm overnight last Thursday without a hitch. While the energy markets stayed steady throughout the change, the most notable impact has been elevated day-ahead ancillary service prices, particularly non-spin, as many market participants have shifted away from day-ahead AS and towards the “new kid on the block” real-time (RT) AS products. The RT AS products have been driven into the ground primarily due to 1) day-ahead AS participants switched to RT AS and 2) market participants who previously refrained from entertaining the commitment of day-ahead AS feel much more comfortable considering RT AS that they can switch in and out of on a five minute basis.

At the moment, there is a lot of money to be made in day-ahead AS. For operators concerned about honoring RUC SoC and duration requirements, the SmartBidder optimization in day-ahead and real-time is fully capable of handling RUC feasibility and can limit day-ahead AS offers in accordance with RUC requirements. The optimization is also fully capable of covering day-ahead AS awards in real-time. Talk to your analyst about the various options SmartBidder has to participate in day-ahead AS in a risk-adjusted manner to maximize revenue.

Day-ahead AS prices have been the RTC+B winner so far. Importantly, even when real-time energy prices have eclipsed day-ahead energy prices, real-time AS prices have still been far lower than day-ahead AS prices. This signals that there is a current structural inefficiency where market participants are much warier about taking on day-ahead AS relative to RT AS. While this is expected to some degree (proportional to energy spreads), the degree of day-ahead dominance points towards battery operators being overly conservative about taking on day-ahead AS positions. This inefficiency should begin to iron out over the coming weeks as the market reacts. The major caveat is that there has still been no test of how RT AS prices will respond when the battery fleet depletes its SoC fully. Keep an eye out for the first morning/evening when RT energy prices are strong enough for a full discharge.

Expect this week in CAISO to be like the previous two. Peak net loads are not forecast to break 30GW, and solar generation remains consistent throughout. Energy arbitrage is once again the best way to maximize revenue utilizing TB4 as a solid base strategy. Capture more upside by opportunistically trading in both the day-ahead and real-time markets when the DART spread is positive in charging hours and negative in discharging hours. SmartBidder’s Mt. Shasta strategy accounts for all of these dynamics. Additionally, look for increased congestion along Path 15 to provide cheap day-ahead charging opportunities for SP15 operators. This emerging dynamic is described in more detail below.

Market conditions have been quiet in CAISO as net load levels have been low and congestion has been limited, partially due to more limited winter solar production. The day-ahead market is pricing in more congestion than the real-time market. If this continues, expect lower real-time prices in NP15 relative to higher real-time prices in NP15 (relative to day-ahead pricing thresholds). Operators should focus on energy arbitrage and regulation down to grind out additional revenue for the rest of 2025.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)