Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

Structural changes in US power markets continue to affect absolute prices and price variability, which presents opportunities for both generators and load-serving entities to use hedging to ensure greater cost and revenue stability. This dynamic is especially relevant in ERCOT, where the lack of a capacity market or procurement mandates creates amplified price risks. Moreover, Ascend believes that in ERCOT in 2026, a confluence of factors have led forward markets to price in a perceived scarcity risk that does not align with supply fundamentals. In this environment, generation assets – and especially battery energy storage systems (BESS) – have unique opportunities to use hedges to ensure cash flow stability. Fully maximizing the benefits of hedging, however, requires a dedicated strategy that leverages advanced analytics to minimize risk and maximize returns.

In a recent webinar, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, Dr. Carlos Blanco, Managing Director of Risk Management and ESG, and Tyler Pritchard, Senior Energy Analyst, to discuss how generators and load-serving entities can structure optimal hedges, how they can use hedging to take advantage of the difference between forward prices and realized spot prices, and how current ERCOT market dynamics bring both risk and opportunity.

Though employed in all energy markets, hedging is especially crucial in ERCOT because of how the market is designed. In ERCOT, without scarcity pricing energy market revenues would be nowhere near sufficient to support new entry, so ERCOT relies on scarcity pricing – which is necessary but irregular – in lieu of a capacity market to fill the needed revenue gaps for new entry.

For generators, then, hedging ensures revenue stability over time, which is highly useful both operationally (in ensuring that actual cash flows meet expected cash flows) and in terms of facilitating project finance. For load-serving entities, hedging is an important way to reduce cost variability.

While thermal generators have been employing hedges for decades to smooth regular scarcity conditions into average expected values, storage owners and operators have done so only limitedly. In ERCOT, where forward prices have missed badly during the past two years – and look likely to do so again in 2026 – this brings serious implications for pricing and revenue stability.

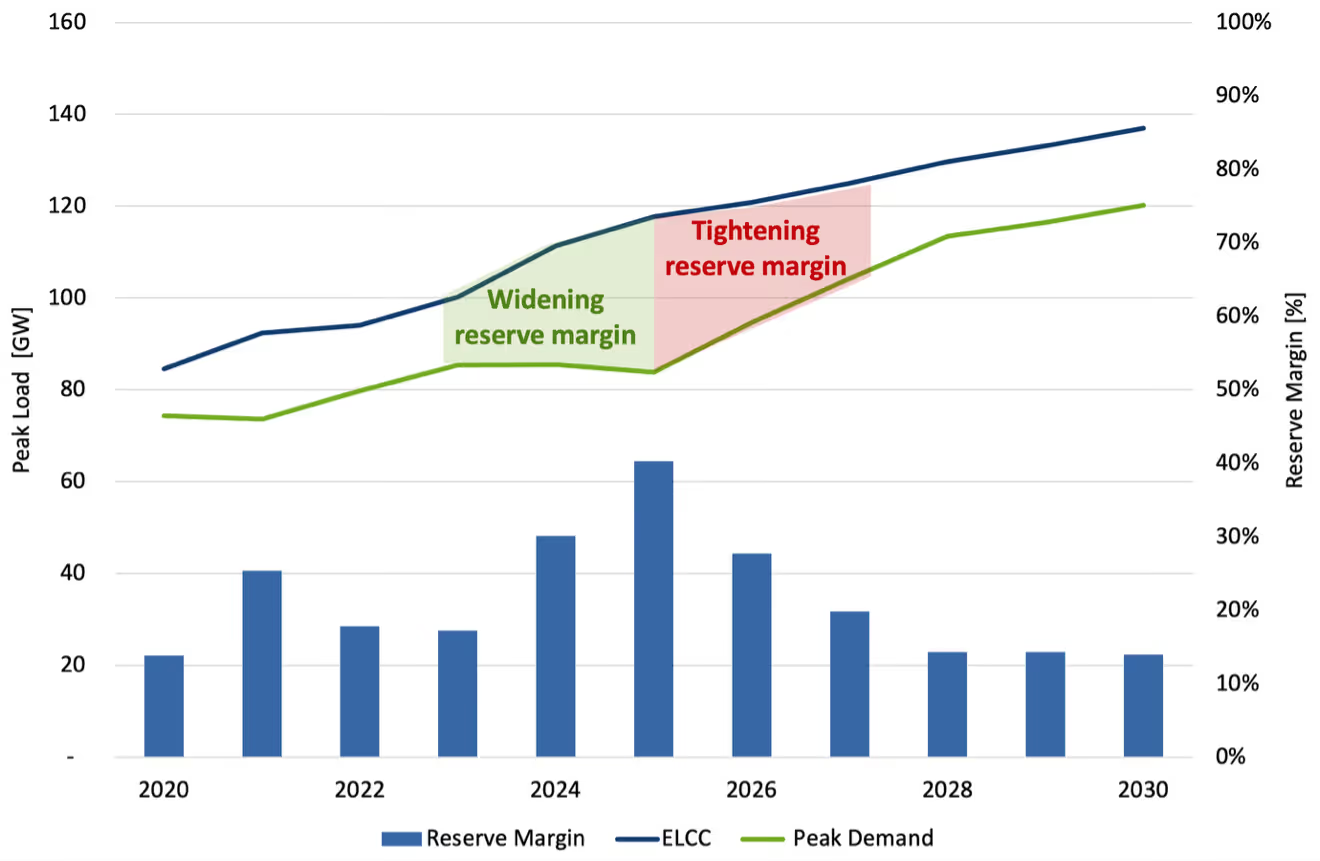

As illustrated in Figure 1, there has been a widening reserve margin in ERCOT during recent years, which has made the market much longer in supply than many people realize. Though the supply/demand situation will start to tighten in 2026 and beyond, there is low potential for scarcity in 2026.

So why are markets pricing 2026 like there is high scarcity potential? As illustrated in Figure 2, ERCOT once possessed an excess quantity of thermal supply to meet peak demand. Currently, however, there exists a deficit of thermal supply relative to peak demand. At the same time, significant amounts of solar and storage have been added to the Texas energy supply during the past several years. If that solar and storage isn't transacting in forward markets, then the forward markets themselves end up with a supply-demand imbalance, even if there is no supply shortage in the actual power market. It is for this reason that Ascend, for the first time ever, created an 'expected case' for ERCOT that does not align to forwards in 2026-2027.

Because hedge risks can vary by year and season, the core of any good strategy begins with a rigorous probabilistic market analysis that accounts for key uncertainties and their correlations. Ascend’s risk analysis, for example, leverages simulations with weather as a fundamental driver, accounting for correlations with load, renewable generation, outages, and fuel prices to illustrate the likelihood and severity of hedge loss events across different operating conditions and periods.

By analyzing the duration and cost of loss events, generators can then optimize hedge sizes using a metric such as Gross Margin at Risk (GMAR). As illustrated in Figure 3 for a battery, GMAR can be used to quantify the revenue downside, and reflects a generator’s ability to cover on-peak contract loss events and the on-peak contract’s ability to supplement generator revenues when prices are depressed. By identifying the optimum hedge size, project revenues become insensitive to market conditions.

As illustrated in Figure 4, however, the optimum hedge position can vary greatly throughout the year. Risk varies from month to month, with winter months characterized by long-duration loss events and higher risk exposure for battery operators. By evaluating monthly risk profiles, operators can avoid overhedging or underhedging battery assets by adjusting hedge sizes accordingly each month.

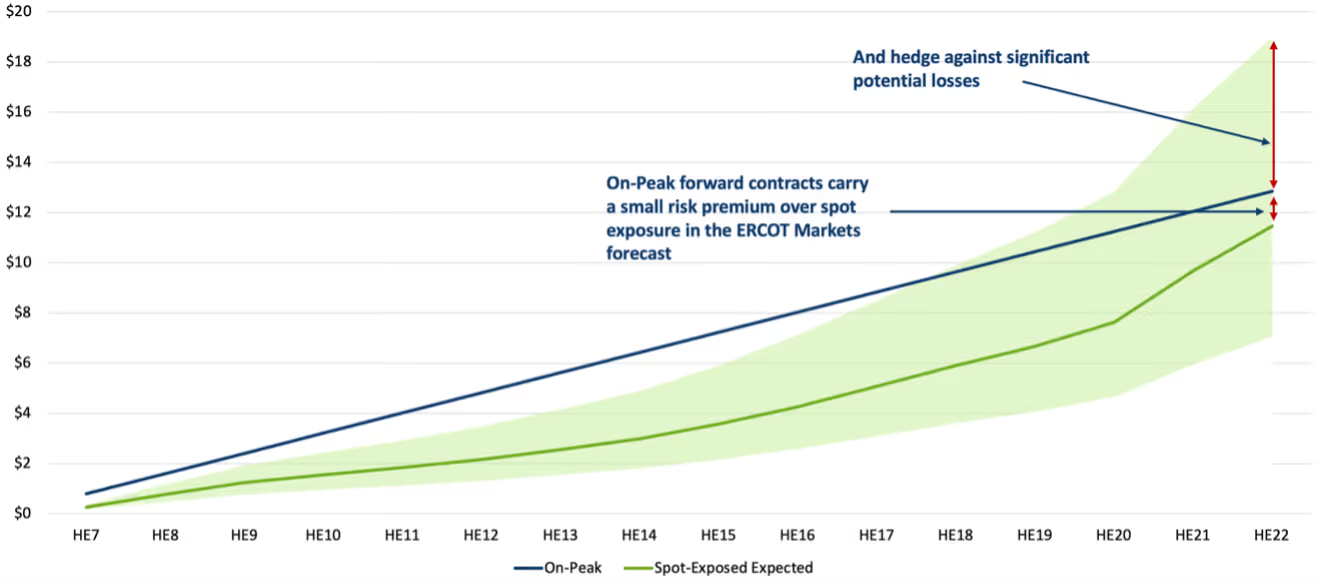

In a forwards-aligned market, it is worthwhile for load-serving entities to purchase on-peak contracts. As seen in the illustrative load profile in Figure 5, the expected value of on-peak hedging generally has a small premium to spot price procurement, but it hedges against very significant potential losses in the evening hours.

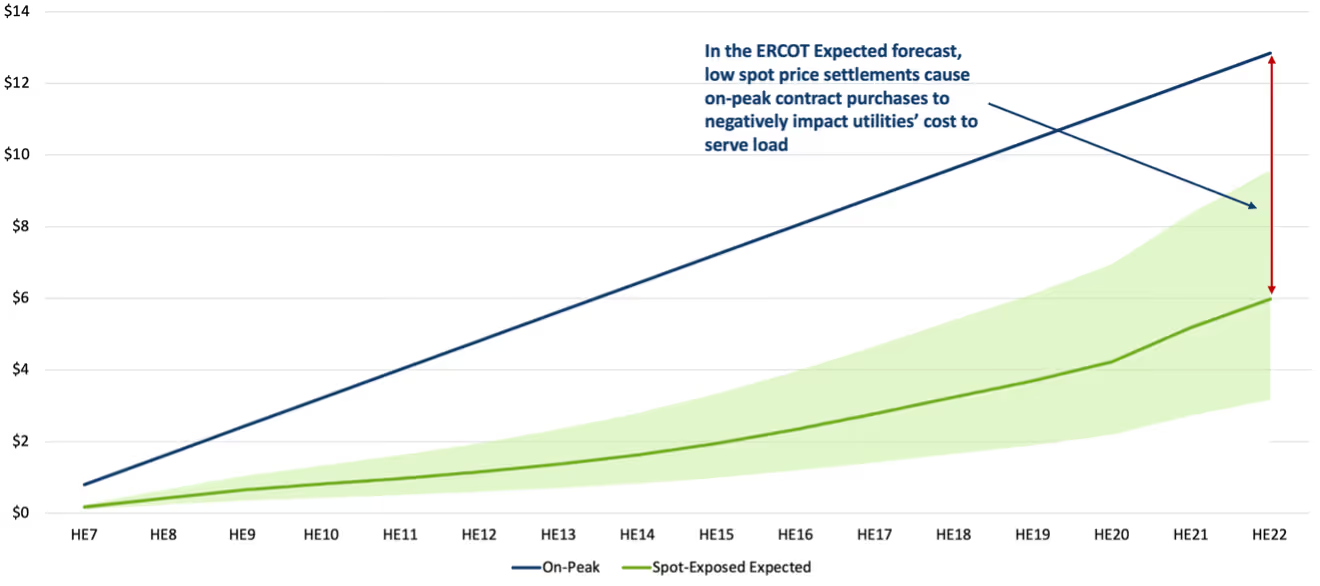

If market forwards are not aligned to expected spot prices, however, then the situation changes. What starts as a small risk premium between the on-peak forward price and the spot price becomes a very significant risk premium in a lower spot price settlement world. As illustrated in Figure 6, in Ascend’s ERCOT ‘expected’ case there are virtually no situations where the spot price procurement will actually settle at a more costly cost-to-serve load than the on-peak hedge. This creates a situation where load-serving entities are overpaying for energy. Developing the optimal strategy for navigating this uncertainty requires understanding the stochastic distributions of spot price settlements across different hours. By limiting exposure to hours with the highest loss potential, load-serving entities can reduce the risk of overpaying for hedged positions.

Additionally, super-peak forward structures, which focus on hours-ending 18-22, can be advantageous to both load and generation when low volatility is expected in ERCOT. While super-peak forwards appear presently overpriced, increased storage participation could increase market efficiency and bring the price down.

For energy asset owners and operators who have rarely or never employed hedging strategies, the following practices are crucial:

Ultimately, significant value creation opportunities exist for forward hedging combined with revenue stacking while maintaining physical market rules and warranty constraints. Portfolio optimization and risk management solutions, such as those offered by Ascend's PowerSIMM™ platform and associated consulting services, can be highly effective in creating optimal hedging strategies for energy assets.

The Ascend PowerSIMM™ suite is an energy analytics platform that captures the new and evolving dynamics of electricity markets. Utilities, public power entities, renewable developers, and community choice aggregators utilize PowerSIMM for optimal energy portfolio management, risk management, resource planning, and project optimization.

Access the full webinar now or contact us to learn more.

Structural changes in US power markets continue to affect absolute prices and price variability, which presents opportunities for both generators and load-serving entities to use hedging to ensure greater cost and revenue stability. This dynamic is especially relevant in ERCOT, where the lack of a capacity market or procurement mandates creates amplified price risks. Moreover, Ascend believes that in ERCOT in 2026, a confluence of factors have led forward markets to price in a perceived scarcity risk that does not align with supply fundamentals. In this environment, generation assets – and especially battery energy storage systems (BESS) – have unique opportunities to use hedges to ensure cash flow stability. Fully maximizing the benefits of hedging, however, requires a dedicated strategy that leverages advanced analytics to minimize risk and maximize returns.

In a recent webinar, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, Dr. Carlos Blanco, Managing Director of Risk Management and ESG, and Tyler Pritchard, Senior Energy Analyst, to discuss how generators and load-serving entities can structure optimal hedges, how they can use hedging to take advantage of the difference between forward prices and realized spot prices, and how current ERCOT market dynamics bring both risk and opportunity.

Though employed in all energy markets, hedging is especially crucial in ERCOT because of how the market is designed. In ERCOT, without scarcity pricing energy market revenues would be nowhere near sufficient to support new entry, so ERCOT relies on scarcity pricing – which is necessary but irregular – in lieu of a capacity market to fill the needed revenue gaps for new entry.

For generators, then, hedging ensures revenue stability over time, which is highly useful both operationally (in ensuring that actual cash flows meet expected cash flows) and in terms of facilitating project finance. For load-serving entities, hedging is an important way to reduce cost variability.

While thermal generators have been employing hedges for decades to smooth regular scarcity conditions into average expected values, storage owners and operators have done so only limitedly. In ERCOT, where forward prices have missed badly during the past two years – and look likely to do so again in 2026 – this brings serious implications for pricing and revenue stability.

As illustrated in Figure 1, there has been a widening reserve margin in ERCOT during recent years, which has made the market much longer in supply than many people realize. Though the supply/demand situation will start to tighten in 2026 and beyond, there is low potential for scarcity in 2026.

So why are markets pricing 2026 like there is high scarcity potential? As illustrated in Figure 2, ERCOT once possessed an excess quantity of thermal supply to meet peak demand. Currently, however, there exists a deficit of thermal supply relative to peak demand. At the same time, significant amounts of solar and storage have been added to the Texas energy supply during the past several years. If that solar and storage isn't transacting in forward markets, then the forward markets themselves end up with a supply-demand imbalance, even if there is no supply shortage in the actual power market. It is for this reason that Ascend, for the first time ever, created an 'expected case' for ERCOT that does not align to forwards in 2026-2027.

Because hedge risks can vary by year and season, the core of any good strategy begins with a rigorous probabilistic market analysis that accounts for key uncertainties and their correlations. Ascend’s risk analysis, for example, leverages simulations with weather as a fundamental driver, accounting for correlations with load, renewable generation, outages, and fuel prices to illustrate the likelihood and severity of hedge loss events across different operating conditions and periods.

By analyzing the duration and cost of loss events, generators can then optimize hedge sizes using a metric such as Gross Margin at Risk (GMAR). As illustrated in Figure 3 for a battery, GMAR can be used to quantify the revenue downside, and reflects a generator’s ability to cover on-peak contract loss events and the on-peak contract’s ability to supplement generator revenues when prices are depressed. By identifying the optimum hedge size, project revenues become insensitive to market conditions.

As illustrated in Figure 4, however, the optimum hedge position can vary greatly throughout the year. Risk varies from month to month, with winter months characterized by long-duration loss events and higher risk exposure for battery operators. By evaluating monthly risk profiles, operators can avoid overhedging or underhedging battery assets by adjusting hedge sizes accordingly each month.

In a forwards-aligned market, it is worthwhile for load-serving entities to purchase on-peak contracts. As seen in the illustrative load profile in Figure 5, the expected value of on-peak hedging generally has a small premium to spot price procurement, but it hedges against very significant potential losses in the evening hours.

If market forwards are not aligned to expected spot prices, however, then the situation changes. What starts as a small risk premium between the on-peak forward price and the spot price becomes a very significant risk premium in a lower spot price settlement world. As illustrated in Figure 6, in Ascend’s ERCOT ‘expected’ case there are virtually no situations where the spot price procurement will actually settle at a more costly cost-to-serve load than the on-peak hedge. This creates a situation where load-serving entities are overpaying for energy. Developing the optimal strategy for navigating this uncertainty requires understanding the stochastic distributions of spot price settlements across different hours. By limiting exposure to hours with the highest loss potential, load-serving entities can reduce the risk of overpaying for hedged positions.

Additionally, super-peak forward structures, which focus on hours-ending 18-22, can be advantageous to both load and generation when low volatility is expected in ERCOT. While super-peak forwards appear presently overpriced, increased storage participation could increase market efficiency and bring the price down.

For energy asset owners and operators who have rarely or never employed hedging strategies, the following practices are crucial:

Ultimately, significant value creation opportunities exist for forward hedging combined with revenue stacking while maintaining physical market rules and warranty constraints. Portfolio optimization and risk management solutions, such as those offered by Ascend's PowerSIMM™ platform and associated consulting services, can be highly effective in creating optimal hedging strategies for energy assets.

The Ascend PowerSIMM™ suite is an energy analytics platform that captures the new and evolving dynamics of electricity markets. Utilities, public power entities, renewable developers, and community choice aggregators utilize PowerSIMM for optimal energy portfolio management, risk management, resource planning, and project optimization.

Access the full webinar now or contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)