Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

-4-Website%20Image.avif)

Driven by load growth and policy changes, US power markets are experiencing significant structural shifts that are redefining how buyers, sellers, and investors approach energy storage and renewables. For energy M&A, discipline has replaced velocity as a key investing principle, 'patient capital' has returned, and diversification has become more essential than ever. Meanwhile, PPA prices for renewable energy continue to diverge sharply across U.S. regions, reflecting differences in resource quality, land economics, and market maturity.

In a recent webinar, Dr. Michael Fisher, Director of Valuation Services at Ascend Analytics, joined Rahm Orenstein, Managing Director of Ascend Energy Exchange, and Anthony Boukarim, Director of Resource Planning & Power Procurement, to discuss what to expect and how to proceed in an environment of highly competitive PPA procurements and a solidly recovering M&A market.

The U.S. clean energy M&A market has evolved from the high-velocity heights of 2021–2022 to a more disciplined environment in 2025. Early-decade growth was fueled by low interest rates, optimism around federal policy, and an influx of international capital pursuing platform and portfolio-scale deals.

By 2023–2024, higher interest rates, buyer saturation in ERCOT, project scarcity in CAISO, and supply chain bottlenecks – especially for transformers and breakers –slowed transaction volumes and shifted attention toward asset-specific, risk-adjusted dealmaking.

Momentum has since returned. In early 2025, sellers sought to recycle capital while FERC Order 2023 prompted developers unable to fund interconnection deposits to sell earlier. 'Patient capital' investors took advantage of these opportunities, broadening their reach for storage and hybrid acquisitions beyond ERCOT and CAISO into other US power markets.

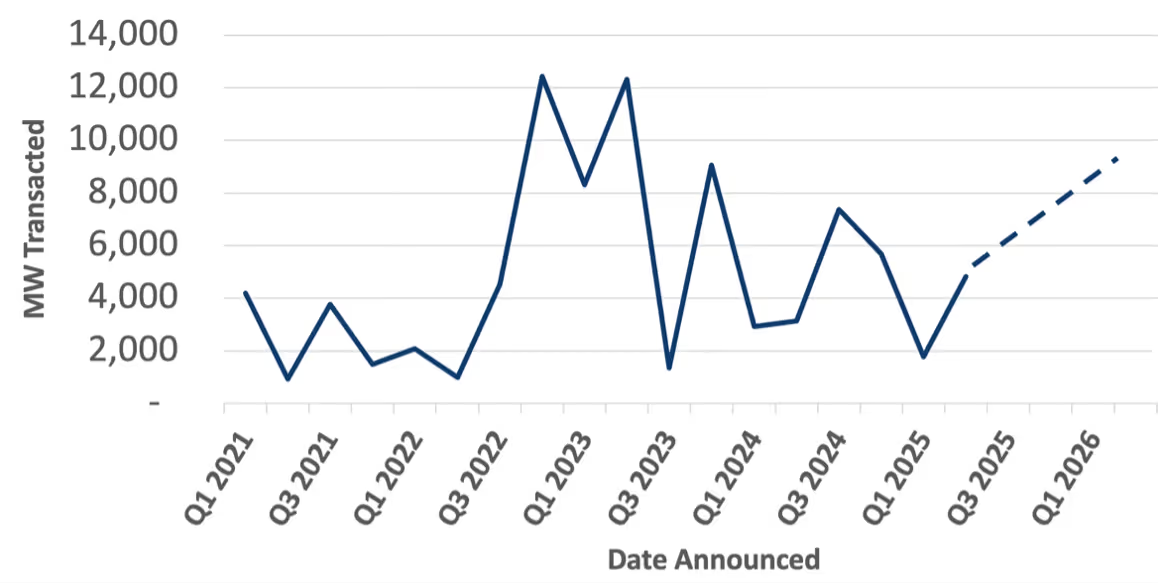

While temporary headwinds in Q2 2025 – from tariff and IRA-related uncertainties to anti-renewable proposals in Texas – slowed activity down, primarily for shovel-ready projects, Ascend is seeing some recovery and is expecting sustained M&A momentum through 2026, as illustrated in Figure 1.

In today’s buyers’ market, not all projects are equal. Risk-adjusted valuations hinge on timing, interconnection and permitting risks and costs, as well as locational value. Sellers face tightening margins, while buyers with the insight to assess nodal dynamics, energy community eligibility, and tariff exposure are well positioned to capture the next wave of opportunity in U.S. clean energy M&A.

In the near term, Ascend expects development fees for late-stage BESS projects in ERCOT to remain depressed, albeit with fundamentals that continue to support load growth, which will drive additional renewable and BESS deployment. This presents strong opportunities for buyers to acquire solid projects at attractive prices. In CAISO, high deal values remain, driven by lucrative resource adequacy and merchant revenue potential, and limited supply due to the hurdles in obtaining interconnection and deliverability. Ascend continues to expect off-taker demand in CAISO into the early 2030s.

In this environment, key paradigm shifts – primarily related to load growth and policy – have also been driving capital realignment. US energy markets have seen a surge in thermal generation investment and M&A, as well as significant capital realignment in renewable and storage platforms.

PPA prices for renewable energy continue to diverge sharply across U.S. regions, reflecting differences in resource quality, land economics, and market maturity. In the Eastern US, renewable project costs remain high due to expensive land, site preparation requirements, and less favorable solar and wind resources. By contrast, the Midwest benefits from superior wind conditions and lower land costs, though solar resource limitations still constrain competitiveness.

In ERCOT and the broader Southwest, abundant solar resources and lower soft costs contribute to the nation’s most competitive PPA pricing. However, wind opportunities outside ERCOT and New Mexico are limited. For emissions-first buyers, project location matters: off-takers focused on carbon abatement often prefer projects in coal-heavy regions, where higher PPA costs in markets like PJM still deliver stronger decarbonization value than lower-cost projects in regions such as ERCOT or SPP.

In increasingly competitive and oversupplied interconnection markets, both renewable PPAs and energy storage tolling agreements are now more reflective of developer cost structures and capital costs than of direct value to the off-taker – pressuring margins and underscoring the need for precise cost benchmarking and market-specific intelligence.

CAISO remains one of the most dynamic and cost-sensitive markets for energy procurement. Over the past year, inflation, supply chain constraints, and procurement mandates – combined with uncertainty surrounding tariffs and tax credits – have driven a sharp escalation in PPA pricing.

Prior to the passage of the One Big Beautiful Bill Act (OBBBA), solar PPA prices had already risen roughly 13% year-over-year. Following OBBBA’s accelerated tax credit phaseout timeline and continued tariff uncertainty, prices increased an additional 24%, marking one of the steepest short-term jumps in recent years.

Storage pricing has proved more resilient. Four-hour standalone storage tolling rates have held relatively steady, while paired storage contracts show modest upward pressure as developers reallocate a portion of rising solar costs. Eight-hour storage tolling prices, meanwhile, have stabilized from early 2024 highs but remain relatively scarce.

As California’s policy and procurement landscape continues to evolve, stakeholders face growing incentives to optimize hybrid configurations, balance duration strategies, and reassess how solar and storage interact under post-OBBBA economics.

Ascend Power Procurement (APP™ ) enables energy buyers to meet climate and reliability goals by conducting automated and highly competitive power procurement processes, totaling more than the U.S. data center load each year. Designed for utilities, community choice aggregators, and corporate renewable energy buyers, APP facilitates the process of executing PPAs by providing an RFP hosting service, shortening the processing time of bids, and evaluating offers with advanced modeling tools and analytics to capture project risks and true economic value.

The Ascend Energy Exchange (AEX™) platform, an exchange for renewable and storage projects, allows buyers to receive access to carefully vetted assets and portfolios, supported by Ascend’s full suite of market-level and project-level valuation, risk assessment, and unique off-take/hedge solutions. Contact us to learn more.

Driven by load growth and policy changes, US power markets are experiencing significant structural shifts that are redefining how buyers, sellers, and investors approach energy storage and renewables. For energy M&A, discipline has replaced velocity as a key investing principle, 'patient capital' has returned, and diversification has become more essential than ever. Meanwhile, PPA prices for renewable energy continue to diverge sharply across U.S. regions, reflecting differences in resource quality, land economics, and market maturity.

In a recent webinar, Dr. Michael Fisher, Director of Valuation Services at Ascend Analytics, joined Rahm Orenstein, Managing Director of Ascend Energy Exchange, and Anthony Boukarim, Director of Resource Planning & Power Procurement, to discuss what to expect and how to proceed in an environment of highly competitive PPA procurements and a solidly recovering M&A market.

The U.S. clean energy M&A market has evolved from the high-velocity heights of 2021–2022 to a more disciplined environment in 2025. Early-decade growth was fueled by low interest rates, optimism around federal policy, and an influx of international capital pursuing platform and portfolio-scale deals.

By 2023–2024, higher interest rates, buyer saturation in ERCOT, project scarcity in CAISO, and supply chain bottlenecks – especially for transformers and breakers –slowed transaction volumes and shifted attention toward asset-specific, risk-adjusted dealmaking.

Momentum has since returned. In early 2025, sellers sought to recycle capital while FERC Order 2023 prompted developers unable to fund interconnection deposits to sell earlier. 'Patient capital' investors took advantage of these opportunities, broadening their reach for storage and hybrid acquisitions beyond ERCOT and CAISO into other US power markets.

While temporary headwinds in Q2 2025 – from tariff and IRA-related uncertainties to anti-renewable proposals in Texas – slowed activity down, primarily for shovel-ready projects, Ascend is seeing some recovery and is expecting sustained M&A momentum through 2026, as illustrated in Figure 1.

In today’s buyers’ market, not all projects are equal. Risk-adjusted valuations hinge on timing, interconnection and permitting risks and costs, as well as locational value. Sellers face tightening margins, while buyers with the insight to assess nodal dynamics, energy community eligibility, and tariff exposure are well positioned to capture the next wave of opportunity in U.S. clean energy M&A.

In the near term, Ascend expects development fees for late-stage BESS projects in ERCOT to remain depressed, albeit with fundamentals that continue to support load growth, which will drive additional renewable and BESS deployment. This presents strong opportunities for buyers to acquire solid projects at attractive prices. In CAISO, high deal values remain, driven by lucrative resource adequacy and merchant revenue potential, and limited supply due to the hurdles in obtaining interconnection and deliverability. Ascend continues to expect off-taker demand in CAISO into the early 2030s.

In this environment, key paradigm shifts – primarily related to load growth and policy – have also been driving capital realignment. US energy markets have seen a surge in thermal generation investment and M&A, as well as significant capital realignment in renewable and storage platforms.

PPA prices for renewable energy continue to diverge sharply across U.S. regions, reflecting differences in resource quality, land economics, and market maturity. In the Eastern US, renewable project costs remain high due to expensive land, site preparation requirements, and less favorable solar and wind resources. By contrast, the Midwest benefits from superior wind conditions and lower land costs, though solar resource limitations still constrain competitiveness.

In ERCOT and the broader Southwest, abundant solar resources and lower soft costs contribute to the nation’s most competitive PPA pricing. However, wind opportunities outside ERCOT and New Mexico are limited. For emissions-first buyers, project location matters: off-takers focused on carbon abatement often prefer projects in coal-heavy regions, where higher PPA costs in markets like PJM still deliver stronger decarbonization value than lower-cost projects in regions such as ERCOT or SPP.

In increasingly competitive and oversupplied interconnection markets, both renewable PPAs and energy storage tolling agreements are now more reflective of developer cost structures and capital costs than of direct value to the off-taker – pressuring margins and underscoring the need for precise cost benchmarking and market-specific intelligence.

CAISO remains one of the most dynamic and cost-sensitive markets for energy procurement. Over the past year, inflation, supply chain constraints, and procurement mandates – combined with uncertainty surrounding tariffs and tax credits – have driven a sharp escalation in PPA pricing.

Prior to the passage of the One Big Beautiful Bill Act (OBBBA), solar PPA prices had already risen roughly 13% year-over-year. Following OBBBA’s accelerated tax credit phaseout timeline and continued tariff uncertainty, prices increased an additional 24%, marking one of the steepest short-term jumps in recent years.

Storage pricing has proved more resilient. Four-hour standalone storage tolling rates have held relatively steady, while paired storage contracts show modest upward pressure as developers reallocate a portion of rising solar costs. Eight-hour storage tolling prices, meanwhile, have stabilized from early 2024 highs but remain relatively scarce.

As California’s policy and procurement landscape continues to evolve, stakeholders face growing incentives to optimize hybrid configurations, balance duration strategies, and reassess how solar and storage interact under post-OBBBA economics.

Ascend Power Procurement (APP™ ) enables energy buyers to meet climate and reliability goals by conducting automated and highly competitive power procurement processes, totaling more than the U.S. data center load each year. Designed for utilities, community choice aggregators, and corporate renewable energy buyers, APP facilitates the process of executing PPAs by providing an RFP hosting service, shortening the processing time of bids, and evaluating offers with advanced modeling tools and analytics to capture project risks and true economic value.

The Ascend Energy Exchange (AEX™) platform, an exchange for renewable and storage projects, allows buyers to receive access to carefully vetted assets and portfolios, supported by Ascend’s full suite of market-level and project-level valuation, risk assessment, and unique off-take/hedge solutions. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)