Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Despite challenges related to demand growth, expensive resource choices, federal opposition to offshore wind development, and increasing winter peaks, solid opportunities exist for renewable and storage development in both the New York Independent System Operator (NYISO) and ISO-New England (ISO-NE) electricity markets. For the moment, favorable state policies and robust subsidy programs for clean energy projects make both ISOs attractive, and the economics of existing generation look good, as well. However, risks remain – especially related to whether Northeast policymakers are willing to tolerate increasingly high energy costs and how their responses affect capacity market prices.

In a recent webinar previewing Ascend's latest NYISO and ISO-NE forecasts, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss why subsidy and procurement programs are essential for Northeast states, how market design impacts capacity prices and new entry, and strategies for maximizing risk-adjusted returns for renewable, storage, and thermal assets.

Meeting clean energy goals on time in New York and in most New England states has become increasingly complicated. During the past two years, offshore wind projects, power purchase agreements (PPAs), and transmission projects have been cancelled due to high costs, while elected officials have frequently voiced concerns about cost sensitivity.

Things haven't gotten better. The Trump administration's opposition to offshore wind has compromised the ability of New England states to meet their goals. New Hampshire is toying with the idea of leaving ISO-NE. Long-duration winter storm peaks diminish the accredited capacity of short-duration storage, but their infrequency means that long-duration storage will see limited utilization. Political and environmental opposition make new gas supply difficult to build – even if turbines were available. The cost and immaturity of renewable fuels and associated distribution systems make new hydrogen expensive to build and operate. And, as with all other US markets, load growth is expected to return.

New entry is needed, and Northeast states face a series of suboptimal choices: to either allow capacity prices to skyrocket, subsidize new entry with diminishing reliability contributions, build new gas generation (and supporting infrastructure), or pay for dispatchable renewable fuel generation.

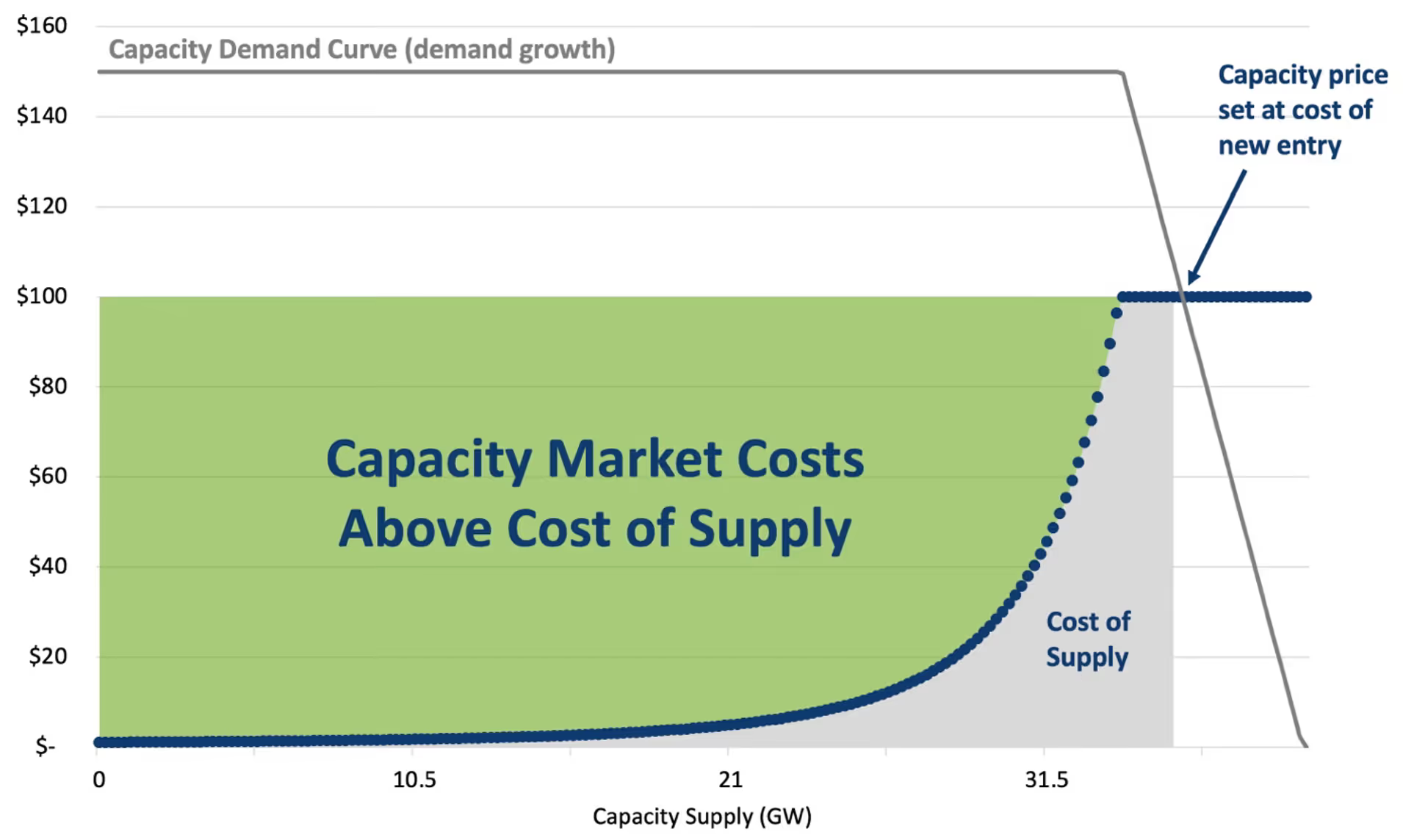

On top of the challenges that Northeast states already face, capacity markets have a cost problem when prices rise to support new entry. If structural change causes capacity markets to clear at the cost of new entry, this cost will flow across the entire supply stack – including to existing thermal generation – regardless of the amount of new entry needed, as illustrated in Figure 1.

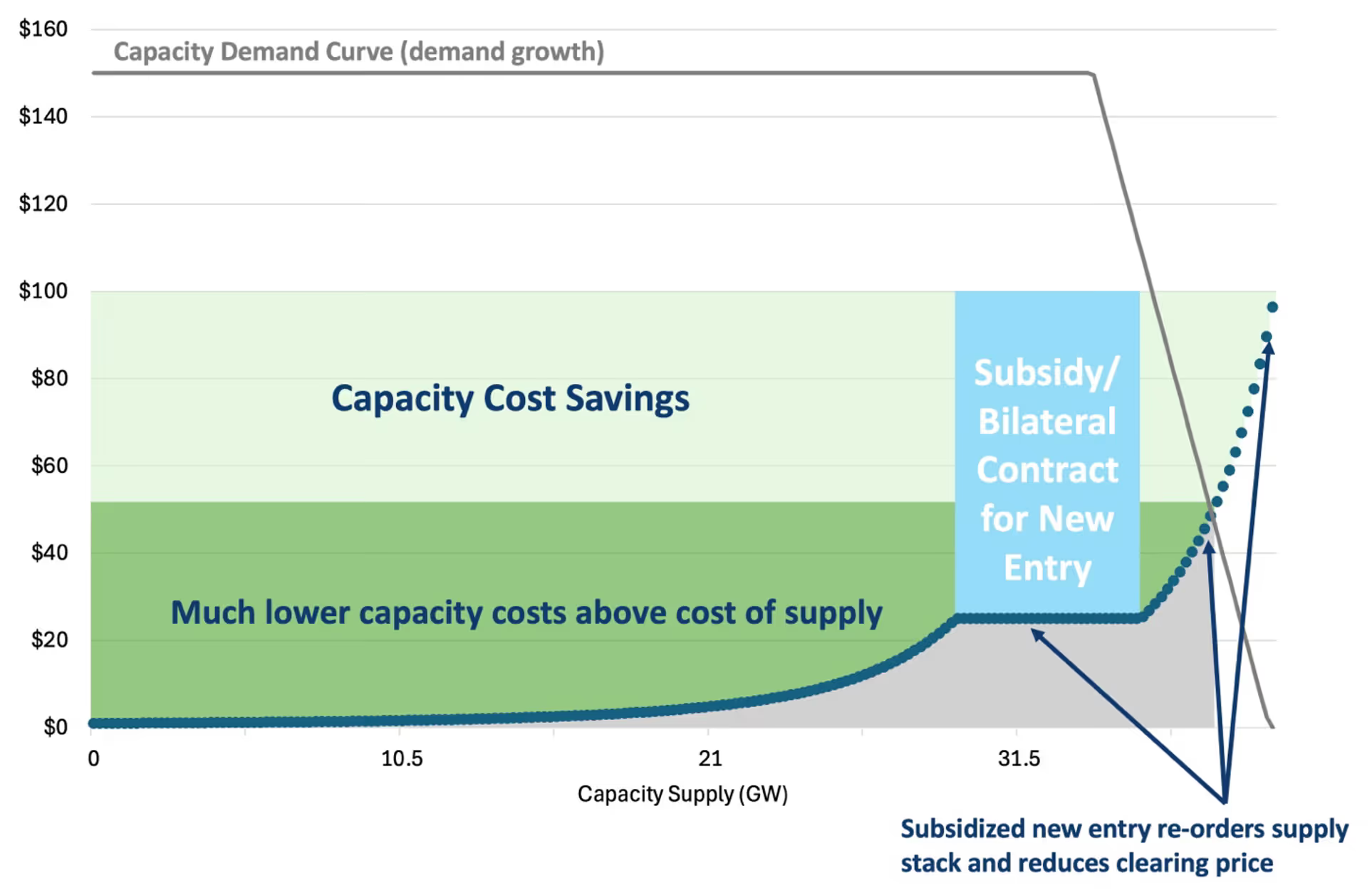

Market design becomes a central consideration when it comes to appropriately tackling soaring capacity prices. Subsidies or bilateral contracts for new entry are essentially the only way to avoid exploding capacity costs and providing windfalls to incumbent fossil generation. As illustrated in Figure 2, the cost of a subsidy can drastically reduce capacity market costs by a significant multiple, depending on the market. For states with clean energy goals, especially, subsidies allow money to flow to new clean entry, and thus to reorder the supply stack and reset the capacity price.

Consequently, several states – most notably, New York and Massachusetts – have introduced programs to subsidize new clean entry. Other Northeast states will need to follow suit in order to support new clean energy resources entering the market.

Formally launched in July 2025, New York's Index Storage Credit (ISC) program aims to accelerate storage buildout while reducing investment risk. As shown in Figure 3, ISC projects must bid a strike price. If a subsequent reference calculation gauges proxy revenues as below the strike price, then then the project receives a payment to make it whole up to the strike price. If proxy revenues are above the strike price, then those get paid back by the project to the state.

With the ISC, additional upside opportunities exist in the form of ancillary revenues, real-time premiums, and nodal premiums. However, those projects on the outside looking in will face significant risk: the ISC will only support 3 GW of utility-scale storage by 2030, with 40% of evaluation based on non-economic factors.

New York's Value of Distributed Energy Resources (VDER) compensation mechanism is also helping to accelerate small-scale renewable deployment. Developed as an alternative to traditional distributed energy resource compensation tariffs that are tied to the retail rate of electricity, VDER provides a multi-pronged revenue stack for ~1.5 GW of sub-5 MW projects , with energy and capacity revenues indexed to wholesale markets. The program also reduces development risks by allowing non-market value stack revenues to be locked in for 10-25 years.

Crucially, VDER allows projects that dispatch at full capacity during a single peak hour to receive full capacity accreditation – which represents an enormous opportunity for storage. Unlike the wholesale market, storage is not subject to effective load carrying capability (ELCC) deration, which means increased capacity revenue potential in VDER compared to utility-scale projects.

Under Massachusetts' Clean Peak Standard (CPS) program, credits are produced by clean generation during defined peak hours, with extra multipliers during different hours, seasons, and locations. Suppliers are required to procure these credits, proportional to load. The state defines bounding parameters, including quantities and price caps.

The CPS represents a strong opportunity for storage and renewable developers. CPS requirements will likely outpace supply for the next decade, leading to prices at the cap and substantial additional revenues for clean projects in Massachusetts. However, there are risks, too. Massachusetts has reduced requirements in the past and has shown growing cost sensitivity. The program may also evolve, redefining what the ‘peak’ period is and favoring longer durations.

Additionally, almost every state in New England is at least exploring a direct procurement program to create functionally contracted revenues for projects. But without contracted revenues, it becomes very difficult for purely merchant projects to compete in Northeast states.

Access the full webinar recording, which offers guidance for where, what, and when to add new capacity resources in NYISO and ISO-NE. The webinar also offers insights related to capacity prices, projected renewable energy buildout, and updated energy demand forecasts.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Despite challenges related to demand growth, expensive resource choices, federal opposition to offshore wind development, and increasing winter peaks, solid opportunities exist for renewable and storage development in both the New York Independent System Operator (NYISO) and ISO-New England (ISO-NE) electricity markets. For the moment, favorable state policies and robust subsidy programs for clean energy projects make both ISOs attractive, and the economics of existing generation look good, as well. However, risks remain – especially related to whether Northeast policymakers are willing to tolerate increasingly high energy costs and how their responses affect capacity market prices.

In a recent webinar previewing Ascend's latest NYISO and ISO-NE forecasts, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss why subsidy and procurement programs are essential for Northeast states, how market design impacts capacity prices and new entry, and strategies for maximizing risk-adjusted returns for renewable, storage, and thermal assets.

Meeting clean energy goals on time in New York and in most New England states has become increasingly complicated. During the past two years, offshore wind projects, power purchase agreements (PPAs), and transmission projects have been cancelled due to high costs, while elected officials have frequently voiced concerns about cost sensitivity.

Things haven't gotten better. The Trump administration's opposition to offshore wind has compromised the ability of New England states to meet their goals. New Hampshire is toying with the idea of leaving ISO-NE. Long-duration winter storm peaks diminish the accredited capacity of short-duration storage, but their infrequency means that long-duration storage will see limited utilization. Political and environmental opposition make new gas supply difficult to build – even if turbines were available. The cost and immaturity of renewable fuels and associated distribution systems make new hydrogen expensive to build and operate. And, as with all other US markets, load growth is expected to return.

New entry is needed, and Northeast states face a series of suboptimal choices: to either allow capacity prices to skyrocket, subsidize new entry with diminishing reliability contributions, build new gas generation (and supporting infrastructure), or pay for dispatchable renewable fuel generation.

On top of the challenges that Northeast states already face, capacity markets have a cost problem when prices rise to support new entry. If structural change causes capacity markets to clear at the cost of new entry, this cost will flow across the entire supply stack – including to existing thermal generation – regardless of the amount of new entry needed, as illustrated in Figure 1.

Market design becomes a central consideration when it comes to appropriately tackling soaring capacity prices. Subsidies or bilateral contracts for new entry are essentially the only way to avoid exploding capacity costs and providing windfalls to incumbent fossil generation. As illustrated in Figure 2, the cost of a subsidy can drastically reduce capacity market costs by a significant multiple, depending on the market. For states with clean energy goals, especially, subsidies allow money to flow to new clean entry, and thus to reorder the supply stack and reset the capacity price.

Consequently, several states – most notably, New York and Massachusetts – have introduced programs to subsidize new clean entry. Other Northeast states will need to follow suit in order to support new clean energy resources entering the market.

Formally launched in July 2025, New York's Index Storage Credit (ISC) program aims to accelerate storage buildout while reducing investment risk. As shown in Figure 3, ISC projects must bid a strike price. If a subsequent reference calculation gauges proxy revenues as below the strike price, then then the project receives a payment to make it whole up to the strike price. If proxy revenues are above the strike price, then those get paid back by the project to the state.

With the ISC, additional upside opportunities exist in the form of ancillary revenues, real-time premiums, and nodal premiums. However, those projects on the outside looking in will face significant risk: the ISC will only support 3 GW of utility-scale storage by 2030, with 40% of evaluation based on non-economic factors.

New York's Value of Distributed Energy Resources (VDER) compensation mechanism is also helping to accelerate small-scale renewable deployment. Developed as an alternative to traditional distributed energy resource compensation tariffs that are tied to the retail rate of electricity, VDER provides a multi-pronged revenue stack for ~1.5 GW of sub-5 MW projects , with energy and capacity revenues indexed to wholesale markets. The program also reduces development risks by allowing non-market value stack revenues to be locked in for 10-25 years.

Crucially, VDER allows projects that dispatch at full capacity during a single peak hour to receive full capacity accreditation – which represents an enormous opportunity for storage. Unlike the wholesale market, storage is not subject to effective load carrying capability (ELCC) deration, which means increased capacity revenue potential in VDER compared to utility-scale projects.

Under Massachusetts' Clean Peak Standard (CPS) program, credits are produced by clean generation during defined peak hours, with extra multipliers during different hours, seasons, and locations. Suppliers are required to procure these credits, proportional to load. The state defines bounding parameters, including quantities and price caps.

The CPS represents a strong opportunity for storage and renewable developers. CPS requirements will likely outpace supply for the next decade, leading to prices at the cap and substantial additional revenues for clean projects in Massachusetts. However, there are risks, too. Massachusetts has reduced requirements in the past and has shown growing cost sensitivity. The program may also evolve, redefining what the ‘peak’ period is and favoring longer durations.

Additionally, almost every state in New England is at least exploring a direct procurement program to create functionally contracted revenues for projects. But without contracted revenues, it becomes very difficult for purely merchant projects to compete in Northeast states.

Access the full webinar recording, which offers guidance for where, what, and when to add new capacity resources in NYISO and ISO-NE. The webinar also offers insights related to capacity prices, projected renewable energy buildout, and updated energy demand forecasts.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)