Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

For the week of October 8th – 14th: Come see the SmartBidder team in action at the Ascend Summit October 15th – 17th! The analyst team will be leading a technical session on Friday morning that covers forecasting vs. optimization, RTC+B strategies, breakthrough UI enhancements, and more. Register here.

Significant outages in CAISO keep price action interesting while stronger wind and lower load in ERCOT will put a chill on market volatility moving forward.

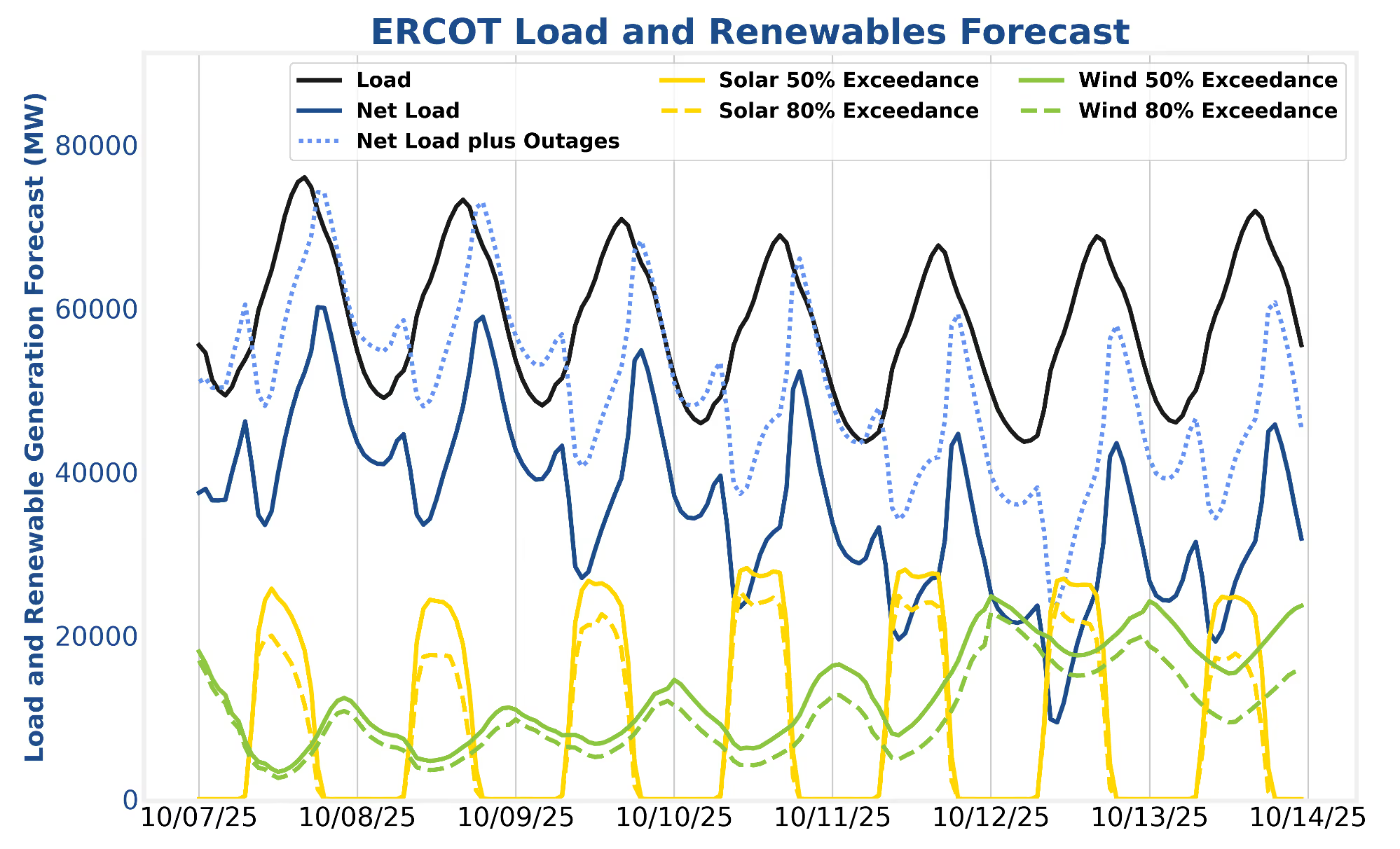

In ERCOT, higher wind production and lower load will progressively haircut net load peaks on a daily basis for the next week. Day-ahead energy discharge prices will not be strong but will likely be stronger than real-time prices, favoring the Mt. Blue Sky Strategy.

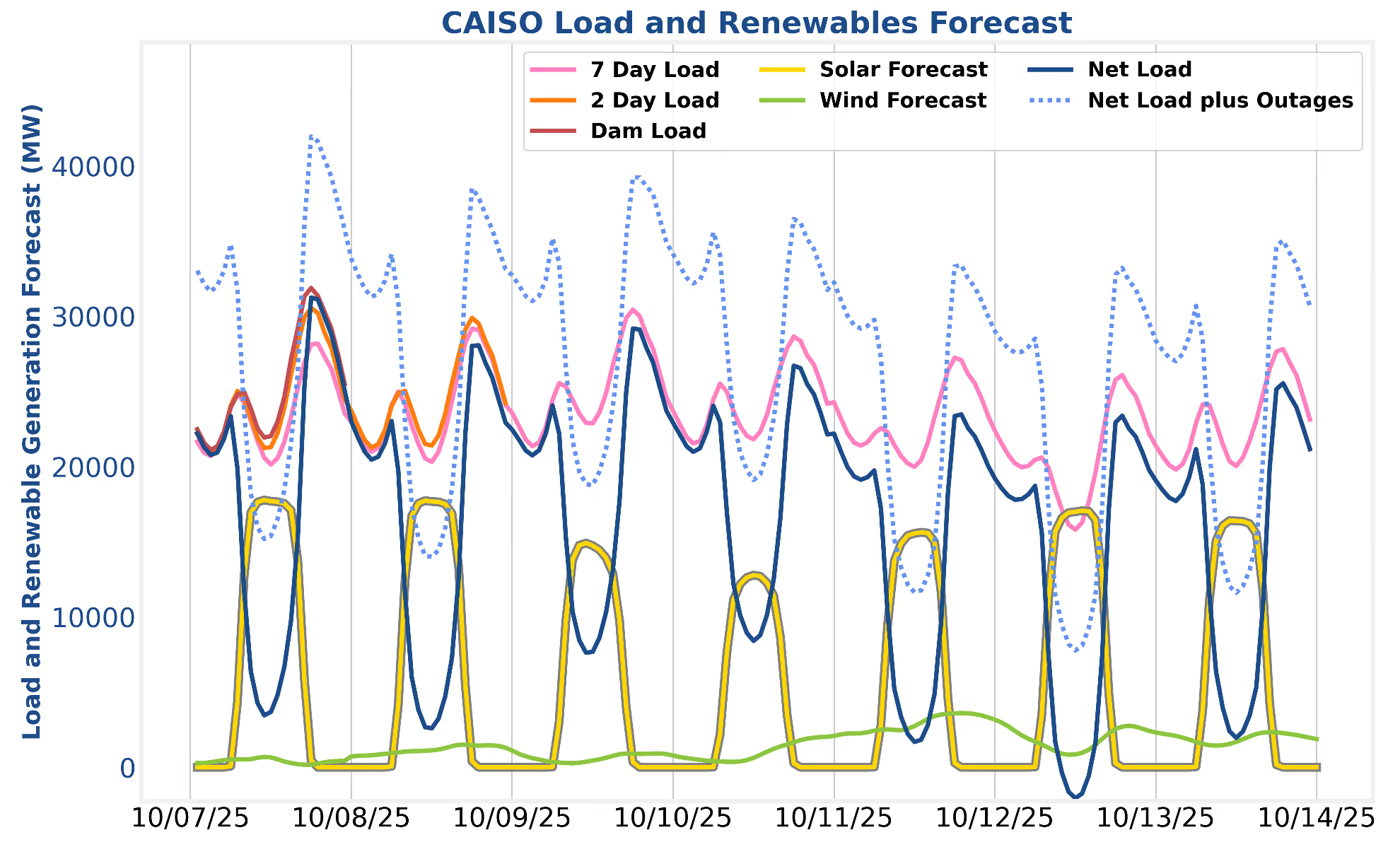

In CAISO, outages around 12 GW are contributing to stronger real-time discharge prices during evening peaks. Operators should consider backing off day-ahead energy participation if this trend continues.

Daily net load peaks currently clocking in around 60 GW will steadily decline to just above 40 GW by the 12th. Real-time energy discharge dominance has faded, and the Mt. Blue Sky strategy should be the top performer this week. The net load trough near 10 GW on the 12th will likely induce negative charging prices at many nodes due to coincidently strong solar and wind production. Operators should consider moving SoC out of their batteries on the evening on the 11th (even though day-ahead discharge prices will be pretty low) depending on how the day-ahead charging prices look on the morning on the 12th. Arbitrage opportunities don’t always have to involve high discharge prices during periods of high renewable generation.

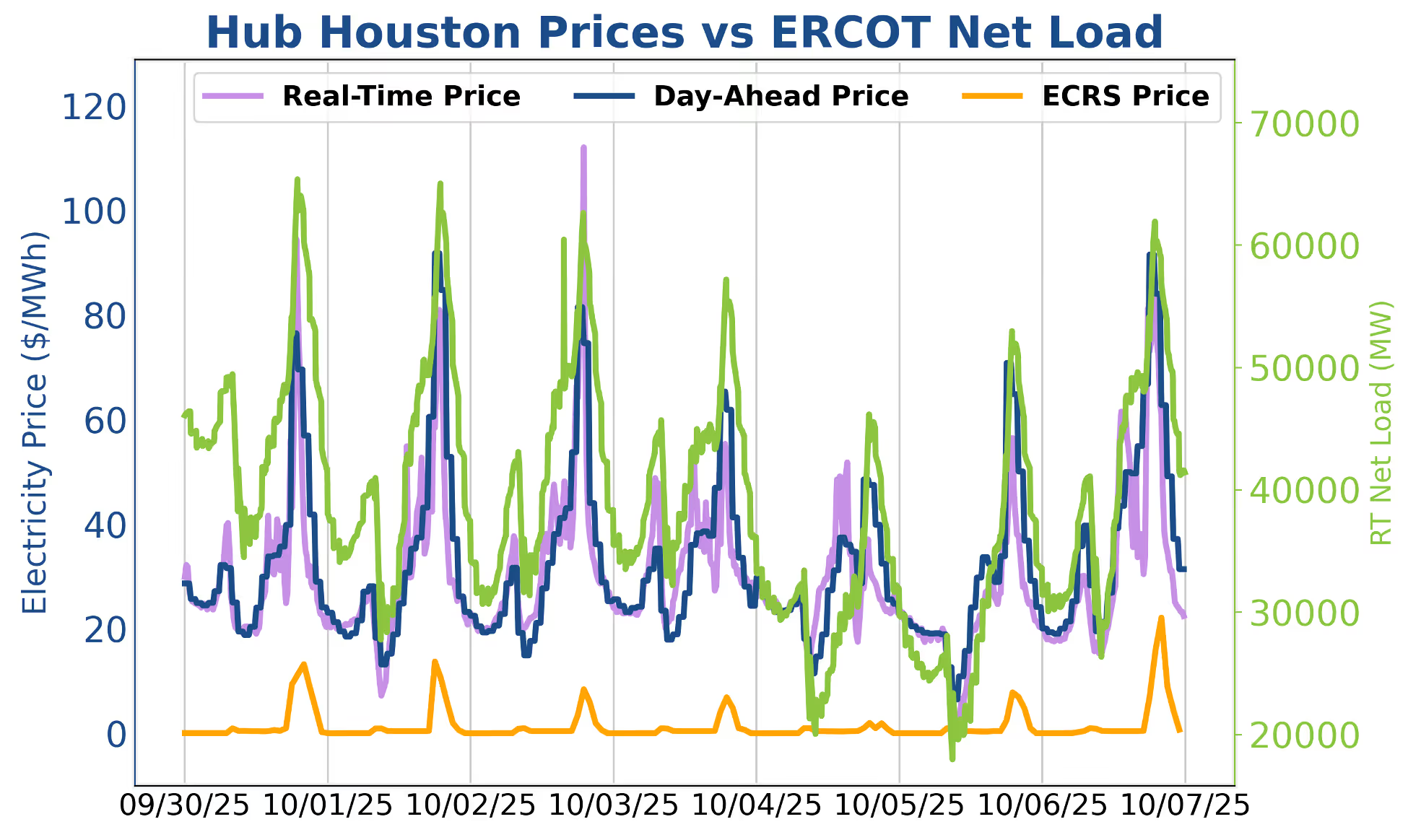

Market conditions were exceedingly normal last week in ERCOT. Real-time LMPs eclipsed $100/MWh during a few intervals, but day-ahead discharge prices were generally higher. Net load troughs were lower on the weekend and sent charging prices towards $0/MWh. Mt. Blue Sky was the top performing SmartBidder strategy.

This week in CAISO, the effects of shoulder season outages are expected to continue, with total outages approaching 12 GW. With this many resources offline, the supply stack will tighten, and operators should anticipate heightened real-time prices during the ramp-up of load as the sun sets, around 17:45–18:00 local time. Cloud cover is projected to reduce solar production on October 9 and 10, which could also lead to relatively elevated real-time prices during mid-day.

Operators should consider a strategy of real-time discharging if systemic large evening forecast misses persist. While the SmartBidder team views this as unlikely, such misses could elevate evening real-time prices. Otherwise, evening discharging in the day-ahead market is the recommended approach. When charging, using regulation down is a reliable way to reduce charging costs. The challenge is layering in the right amount of regulation down to preserve sufficient energy room in case throughput does not materialize. Resources should be cautious with heavy regulation down participation after 1 PM PT to ensure enough time to fully charge before the evening peak. The SmartBidder Mt. Shasta strategy is designed to handle this challenge effectively.

Last week in CAISO we saw something we have not seen in a while: strong real-time prices in both the charging and discharging windows. Early in the week, on September 30 and October 1, it was advantageous for operators to be exclusively in the real-time energy market rather than selling out day-ahead participation. Perhaps the best performing strategy was a combination of regulation down and real-time energy during the midday hours, followed by real-time discharging in the evening. This should not come as a surprise since lower mid-day prices are typical during the shoulder seasons when cooler weather and reduced demand ease pressure on the grid.

What was surprising, however, were the day-ahead load forecast misses that led to particularly strong evening prices on October 1 and 2. Actual demand during those evenings came in more than one gigawatt above day-ahead forecasts, driving prices higher in the real-time supply stack relative to day-ahead settlements. While this trend was especially pronounced early in the week and hinted at similar dynamics developing around October 6, it is still reasonable to expect that day-ahead evening discharging prices will remain the most favorable on most days, with real-time continuing to offer stronger opportunities in the mid-day charging window. Operators who are more risk-tolerant should consider setting a midnight SOC value that enables real-time charging and day-ahead discharging during days with strong solar production. Please reach out to your dedicated analyst if you would like to configure something like this.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of October 8th – 14th: Come see the SmartBidder team in action at the Ascend Summit October 15th – 17th! The analyst team will be leading a technical session on Friday morning that covers forecasting vs. optimization, RTC+B strategies, breakthrough UI enhancements, and more. Register here.

Significant outages in CAISO keep price action interesting while stronger wind and lower load in ERCOT will put a chill on market volatility moving forward.

In ERCOT, higher wind production and lower load will progressively haircut net load peaks on a daily basis for the next week. Day-ahead energy discharge prices will not be strong but will likely be stronger than real-time prices, favoring the Mt. Blue Sky Strategy.

In CAISO, outages around 12 GW are contributing to stronger real-time discharge prices during evening peaks. Operators should consider backing off day-ahead energy participation if this trend continues.

Daily net load peaks currently clocking in around 60 GW will steadily decline to just above 40 GW by the 12th. Real-time energy discharge dominance has faded, and the Mt. Blue Sky strategy should be the top performer this week. The net load trough near 10 GW on the 12th will likely induce negative charging prices at many nodes due to coincidently strong solar and wind production. Operators should consider moving SoC out of their batteries on the evening on the 11th (even though day-ahead discharge prices will be pretty low) depending on how the day-ahead charging prices look on the morning on the 12th. Arbitrage opportunities don’t always have to involve high discharge prices during periods of high renewable generation.

Market conditions were exceedingly normal last week in ERCOT. Real-time LMPs eclipsed $100/MWh during a few intervals, but day-ahead discharge prices were generally higher. Net load troughs were lower on the weekend and sent charging prices towards $0/MWh. Mt. Blue Sky was the top performing SmartBidder strategy.

This week in CAISO, the effects of shoulder season outages are expected to continue, with total outages approaching 12 GW. With this many resources offline, the supply stack will tighten, and operators should anticipate heightened real-time prices during the ramp-up of load as the sun sets, around 17:45–18:00 local time. Cloud cover is projected to reduce solar production on October 9 and 10, which could also lead to relatively elevated real-time prices during mid-day.

Operators should consider a strategy of real-time discharging if systemic large evening forecast misses persist. While the SmartBidder team views this as unlikely, such misses could elevate evening real-time prices. Otherwise, evening discharging in the day-ahead market is the recommended approach. When charging, using regulation down is a reliable way to reduce charging costs. The challenge is layering in the right amount of regulation down to preserve sufficient energy room in case throughput does not materialize. Resources should be cautious with heavy regulation down participation after 1 PM PT to ensure enough time to fully charge before the evening peak. The SmartBidder Mt. Shasta strategy is designed to handle this challenge effectively.

Last week in CAISO we saw something we have not seen in a while: strong real-time prices in both the charging and discharging windows. Early in the week, on September 30 and October 1, it was advantageous for operators to be exclusively in the real-time energy market rather than selling out day-ahead participation. Perhaps the best performing strategy was a combination of regulation down and real-time energy during the midday hours, followed by real-time discharging in the evening. This should not come as a surprise since lower mid-day prices are typical during the shoulder seasons when cooler weather and reduced demand ease pressure on the grid.

What was surprising, however, were the day-ahead load forecast misses that led to particularly strong evening prices on October 1 and 2. Actual demand during those evenings came in more than one gigawatt above day-ahead forecasts, driving prices higher in the real-time supply stack relative to day-ahead settlements. While this trend was especially pronounced early in the week and hinted at similar dynamics developing around October 6, it is still reasonable to expect that day-ahead evening discharging prices will remain the most favorable on most days, with real-time continuing to offer stronger opportunities in the mid-day charging window. Operators who are more risk-tolerant should consider setting a midnight SOC value that enables real-time charging and day-ahead discharging during days with strong solar production. Please reach out to your dedicated analyst if you would like to configure something like this.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)