Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

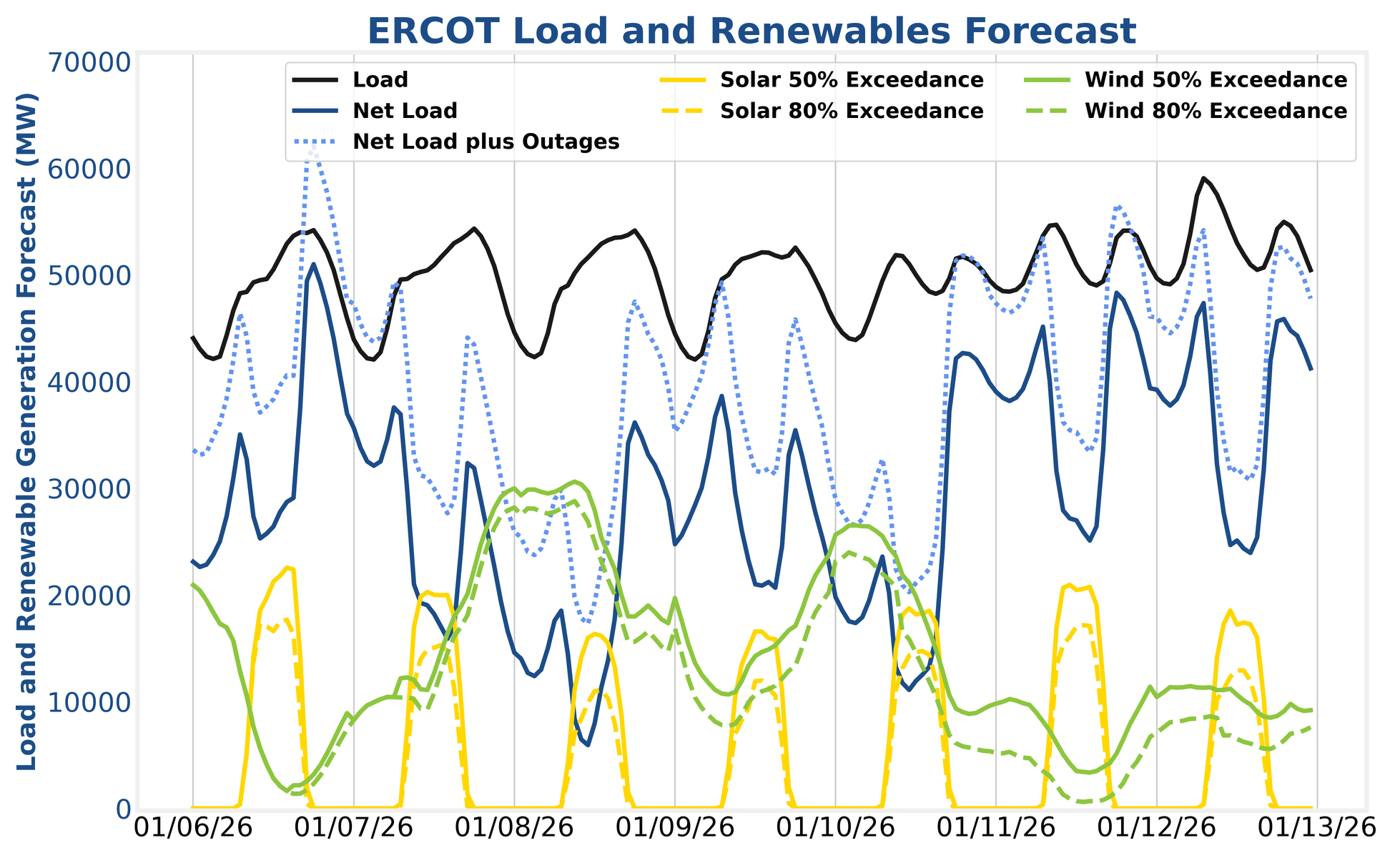

In ERCOT, market conditions will remain mild, and operators should continue to feel comfortable selling day-ahead AS. There are no cold snaps in the foreseeable weather future.

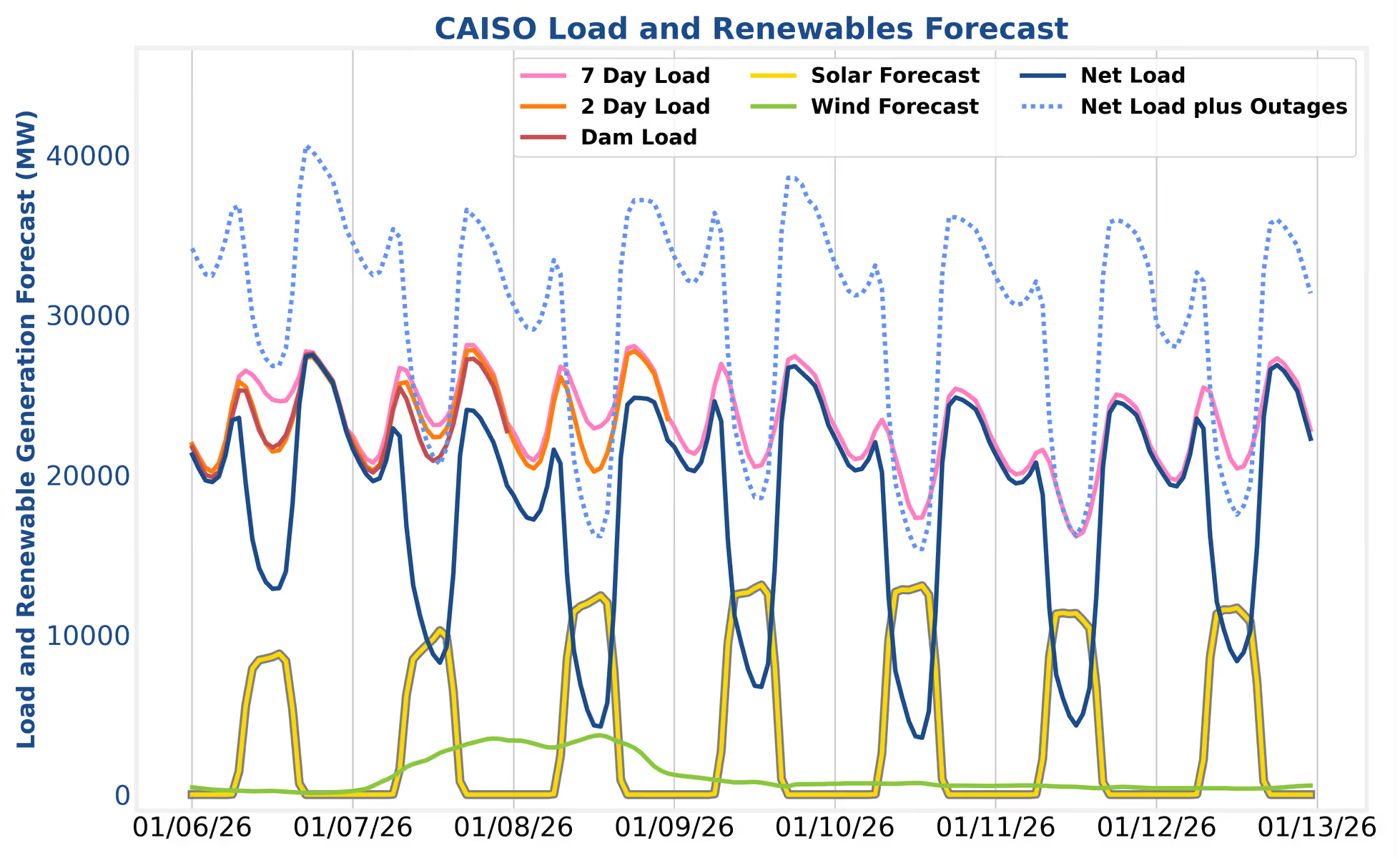

In CAISO, clouds will continue to lift over the solar producing regions of the state, and arbitrage spreads will look a little stronger for the week ahead.

Riding the wind rollercoaster is in, but hitting morning peaks is out so far in January. Mild temperatures will keep morning net load peaks below 50 GW and prices low. Operators should focus on selling day-ahead (DA) ancillary services (AS) to capture the premium that still exists relative to real-time (RT) AS. Those premiums are beginning to go down as more operators become comfortable with DA AS and the RUC implications. Talk to your analyst today about participating in DA AS at your desired RUC risk tolerance. The Mt. Blue Sky strategy with minimal constraints continues to be the top performing SmartBidder strategy in the RTC+B regime.

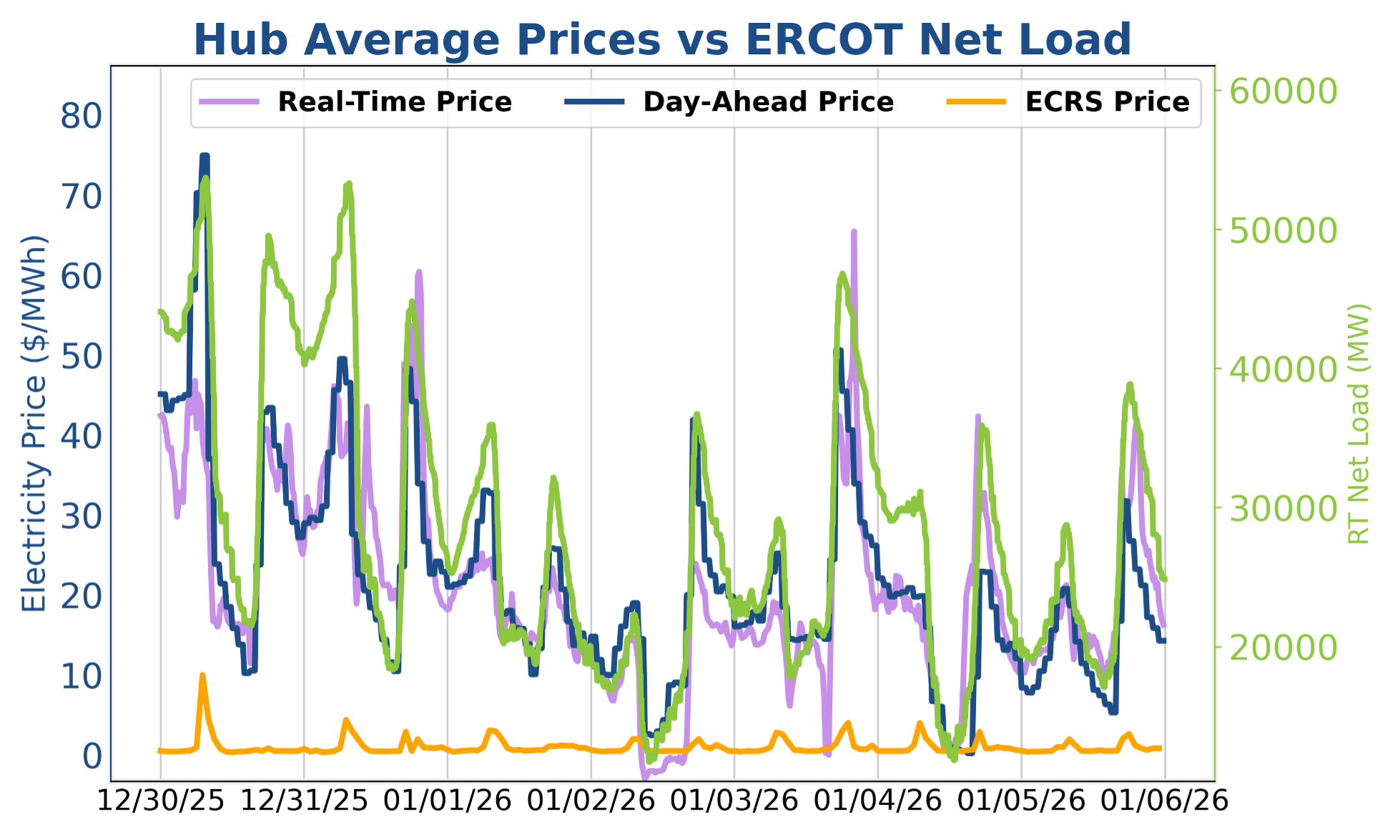

Texas forgot the fireworks for the New Year’s Celebration, and rang in 2026 with a full week without the hub average price cracking $75 in either DA or RT. Some operators are saving cycles, which is likely wise in such an uneventful market regime. Day-ahead ancillaries also continue to have a strong premium to real-time as it appears some storage operators are bidding at the realized day-ahead price in peak hours, pinning the real-time price at or below day-ahead. This dynamic will continue to prevent a negative ancillary DART spread until batteries start running out of SoC. With low energy prices and long flat winter “peaks,” this was not the case last week and the storage fleet largely spent the whole week hitting the snooze button.

Some of the newsletter authors spent the holidays in California, and seeing the beautiful weather forecast for the week after vacation added insult to injury after the atmospheric river poured rain all over the state last week. This is good news for storage operators however, as the charging prices will be favorable to cycle again with increasing PV production over the next few days. Discharge prices have yet to get the memo that storage operators made a resolution to make lots of revenue in 2026, but at least there will be a little bit more of a duck curve returning. Operators may want to switch from strategies focused on rainy weather to strategies focused on mild conditions.

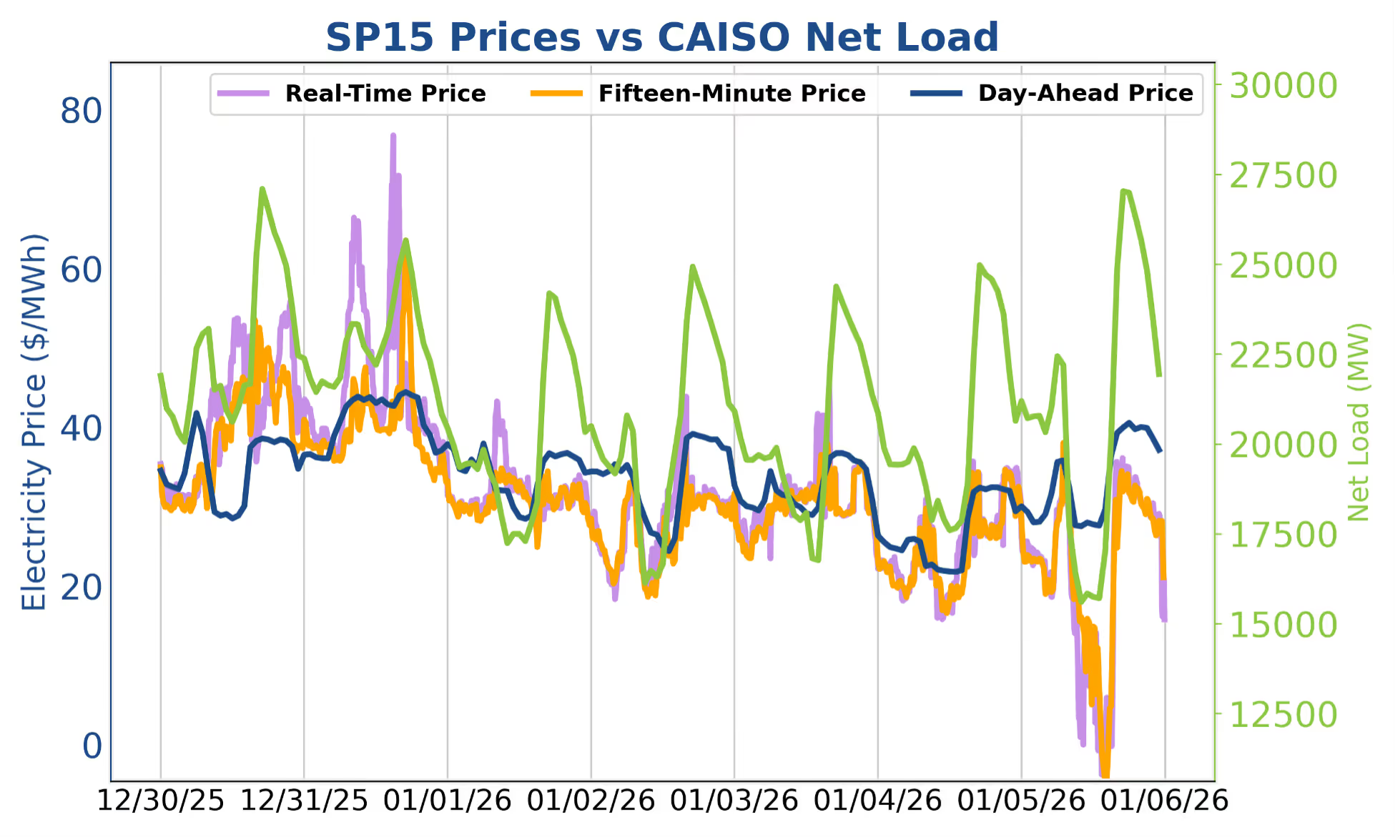

Low solar production led to limited charging opportunities on the final two days of 2025. This dynamic favored operators who charged in the day-ahead market and discharged in real-time to capture the highest prices of the week. Once again, the days following muted solar production featured higher midday DART spreads, possibly due to solar operators maintaining conservative day-ahead commitments and dispatching the remainder of their generation in real-time.

As solar production ramped back up in the new year, pricing dynamics returned to what we have seen throughout 2025 – tight TB4 spreads with little real-time price action above the day-ahead mark. However, a high miss on the net load forecast combined with strong solar production on January 5th pulled real-time prices close to negative territory. This provided a valuable charging opportunity in the real-time market and highlights the importance of capitalizing on such opportunities when the sun re-emerges after long spells of rain.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

In ERCOT, market conditions will remain mild, and operators should continue to feel comfortable selling day-ahead AS. There are no cold snaps in the foreseeable weather future.

In CAISO, clouds will continue to lift over the solar producing regions of the state, and arbitrage spreads will look a little stronger for the week ahead.

Riding the wind rollercoaster is in, but hitting morning peaks is out so far in January. Mild temperatures will keep morning net load peaks below 50 GW and prices low. Operators should focus on selling day-ahead (DA) ancillary services (AS) to capture the premium that still exists relative to real-time (RT) AS. Those premiums are beginning to go down as more operators become comfortable with DA AS and the RUC implications. Talk to your analyst today about participating in DA AS at your desired RUC risk tolerance. The Mt. Blue Sky strategy with minimal constraints continues to be the top performing SmartBidder strategy in the RTC+B regime.

Texas forgot the fireworks for the New Year’s Celebration, and rang in 2026 with a full week without the hub average price cracking $75 in either DA or RT. Some operators are saving cycles, which is likely wise in such an uneventful market regime. Day-ahead ancillaries also continue to have a strong premium to real-time as it appears some storage operators are bidding at the realized day-ahead price in peak hours, pinning the real-time price at or below day-ahead. This dynamic will continue to prevent a negative ancillary DART spread until batteries start running out of SoC. With low energy prices and long flat winter “peaks,” this was not the case last week and the storage fleet largely spent the whole week hitting the snooze button.

Some of the newsletter authors spent the holidays in California, and seeing the beautiful weather forecast for the week after vacation added insult to injury after the atmospheric river poured rain all over the state last week. This is good news for storage operators however, as the charging prices will be favorable to cycle again with increasing PV production over the next few days. Discharge prices have yet to get the memo that storage operators made a resolution to make lots of revenue in 2026, but at least there will be a little bit more of a duck curve returning. Operators may want to switch from strategies focused on rainy weather to strategies focused on mild conditions.

Low solar production led to limited charging opportunities on the final two days of 2025. This dynamic favored operators who charged in the day-ahead market and discharged in real-time to capture the highest prices of the week. Once again, the days following muted solar production featured higher midday DART spreads, possibly due to solar operators maintaining conservative day-ahead commitments and dispatching the remainder of their generation in real-time.

As solar production ramped back up in the new year, pricing dynamics returned to what we have seen throughout 2025 – tight TB4 spreads with little real-time price action above the day-ahead mark. However, a high miss on the net load forecast combined with strong solar production on January 5th pulled real-time prices close to negative territory. This provided a valuable charging opportunity in the real-time market and highlights the importance of capitalizing on such opportunities when the sun re-emerges after long spells of rain.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)