Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

In today's increasingly complex western US energy markets, managing a portfolio with significant hydro resources requires moving beyond reactive physical optimization toward proactive strategies, including the use of hedging and other strategic approaches, that explicitly account for shifting physical and financial risks. As uncertainty compounds across systems and markets, the central challenge becomes clear: how can hydro-reliant utilities and asset owners effectively integrate physical and financial decision-making to manage risk and protect value in a rapidly changing power landscape?

In a recent webinar, Dr. Gary Dorris, CEO at Ascend Analytics, Carley Dolch, Managing Director of Energy Risk Solutions, Dr. Dominique Bain, Senior Analyst, Dr. Carlos Blanco, Managing Director of Portfolio and Risk Management and ESG, and Scott Nicholson, Manager of Resource Planning and Valuation, discussed why hydropower must be treated conditionally rather than as a firm planning resource, how initiatives like the Western Energy Imbalance Market (WEIM) and SPP Markets+ will impact price dynamics, and what insights and strategies utilities, asset owners, and counterparties can use to navigate evolving market dynamics.

For utilities – particularly those with significant reliance on hydropower – longstanding objectives of maintaining low and stable costs are becoming harder to achieve as supply-side variability intensifies and operating margins compress. At the same time, growing meteorological volatility is amplifying uncertainty all around: hydrologic conditions directly affect generation availability, while more extreme weather, especially during summer months, drives sharper and less predictable demand peaks.

2026 will offer more of the same. Significant shifts in snowpack, runoff timing, drought frequency, and extreme precipitation are expected to cause hydro shortages in late summer, coupled with higher power prices. To compound the problem, scarcity pricing will cluster in the evening ramp hours, as solar penetration rises and thermal capacity retires. The risk of unusually large rate shocks for customers is materially elevated in 2026 and beyond.

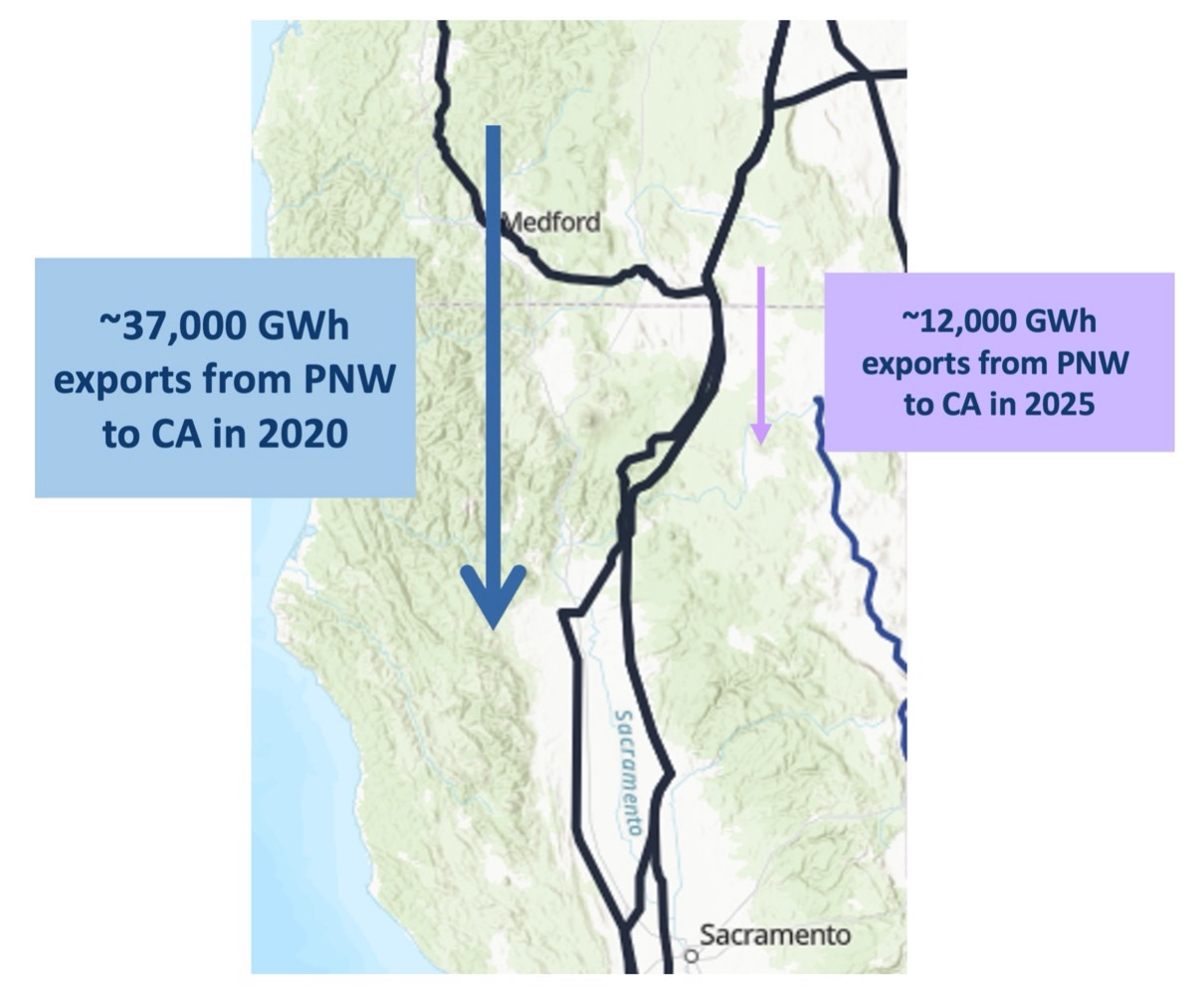

Historically, the hydro-reliant Pacific Northwest (PNW) region has been long on capacity. However, load growth and thermal retirements have tightened supply in recent years, driving elevated and more volatile power prices (though higher near-term prices are expected to decline with future renewable buildout). As a result, hydropower flows have shifted, and are continuing to shift. As shown in Figure 1, hydro exports from the PNW to California have decreased nearly 70% since 2020. The PNW is becoming structurally more expensive as more power remains in the PNW to account for tight supply conditions.

Solar buildout and load growth are also reshaping net load. Deliverability now depends more on interties and scarce flexibility, with volatility concentrating at seams and constrained transmission lines. In addition, limitations on thermal buildout in the PNW means that capacity value migrates toward storage and resources with deliverable flexibility.

Hydro plays a more limited role in California. While hydro serves as the system backbone in the PNW, with prices and scarcity conditions strongly dependent on the water year, annual hydro variability in California makes it hard to rely on. CAISO can see enormous year-to-year variation in hydro generation, with cascading dams increasing the operational complexity. When it comes to price dynamics, solar drives low on-peak prices while gas and carbon pricing drive higher off-peak prices.

For the PNW, connectivity with CAISO is useful for reserve margin management during low hydro years. As illustrated in Figure 2, CAISO can support peak load events without hydro or external imports, given its robust solar resources, solid storage, and moderate load growth. The PNW, however, remains highly reliant on hydro and needs either/both hydro and/or imports to meet peak load events currently and into the future.

Price dynamics within CAISO's Western Energy Imbalance Market (WEIM) will change as SPP Markets+ erodes WEIM participation. Citing concerns about CAISO governance, some notable WEIM participants, including Bonneville Power Authority and Arizona Public Service (APS), will leave the WEIM and join Markets+. This leaves the West fragmented between markets, and Arizona utilities SRP and APS islanded inside the WEIM and Extended Day-Ahead Market (EDAM).

However, the dynamics of the real-time energy imbalance market are expected to continue in a similar manner even as EDAM and SPP Markets+ coalesce into clear shape. The underlying resource, load and transmission infrastructure will not change dramatically. Transmission constraints and market seams will drive highly heterogeneous solar-weighted prices. Physical transmission limits will still impact power flows.

While imports and exports have stayed relatively constant between California and the Desert Southwest states over the past several years, Arizona's joining of SPP Markets+ will reduce this stability. Additionally, some members of the EDAM are pulling out of the Western Resource Adequacy Program (WRAP), thereby compounding the reliability question in Markets+ areas of the PNW.

Ultimately, a fragmented west will create new challenges alongside the benefits of market expansion. Market seams will decrease market efficiency, creating price gradients and decreasing access to imports in some places while increasing access in others. As these market seams form, utilities must consider whether previous sources of power and hedging will still be available, and evaluate whether new pricing and operational risks have emerged.

Because PNW portfolios are often hydro-heavy, near-term price risk can be mitigated by monthly forward block contract buys/sales, depending on position length. As illustrated in Figure 3, hedging can significantly narrow the band of expected risk for hydro assets.

Financial hedging addresses price and water risk. Optimal hedges, when added to portfolio, can minimize cost at risk (95th percentile cost minus average cost). Optimal hedges can vary monthly by on- and off-peak, and slice deals are a longer-term option for mitigating volumetric risk for a hydro asset owner by contracting out portions of the capacity to other parties in exchange for more stable power supply. For asset owners and operators, a well-hedged hydro portfolio provides cost and revenue stability regardless of price level while an unhedged portfolio has a gross margin that changes significantly depending on power price.

To mitigate risks associated with hydro-reliant portfolios, a critical first step involves designing and establishing trading risk management policies and procedures that set guardrails around asset operations and hedging strategies. These must account for stakeholder risk tolerance, hedging protocol design, authority delegation, as well as ongoing communication and reporting. These policies and procedures are essential not only for optimizing hedging outcomes but also for providing a robust framework of accountability should the organization’s strategies be scrutinized in the future.

To address the complexities of PNW and CAISO hydro portfolios, organizations must utilize forward hedging and advanced hedge structures. Implementing dynamic hedge protocols allows for more responsive risk management, directly contributing to rate stability and cost control.

Meaningful risk metrics can guide more informed, data-driven also allows for a much clearer way to inform portfolio management decisions.

The Ascend PowerSIMM™ suite is an energy analytics platform that captures the new and evolving dynamics of electricity markets. Utilities, public power entities, renewable developers, and community choice aggregators utilize PowerSIMM for optimal energy portfolio management, risk management, resource planning, and project optimization.

Access the full webinar now or contact us to learn more.

In today's increasingly complex western US energy markets, managing a portfolio with significant hydro resources requires moving beyond reactive physical optimization toward proactive strategies, including the use of hedging and other strategic approaches, that explicitly account for shifting physical and financial risks. As uncertainty compounds across systems and markets, the central challenge becomes clear: how can hydro-reliant utilities and asset owners effectively integrate physical and financial decision-making to manage risk and protect value in a rapidly changing power landscape?

In a recent webinar, Dr. Gary Dorris, CEO at Ascend Analytics, Carley Dolch, Managing Director of Energy Risk Solutions, Dr. Dominique Bain, Senior Analyst, Dr. Carlos Blanco, Managing Director of Portfolio and Risk Management and ESG, and Scott Nicholson, Manager of Resource Planning and Valuation, discussed why hydropower must be treated conditionally rather than as a firm planning resource, how initiatives like the Western Energy Imbalance Market (WEIM) and SPP Markets+ will impact price dynamics, and what insights and strategies utilities, asset owners, and counterparties can use to navigate evolving market dynamics.

For utilities – particularly those with significant reliance on hydropower – longstanding objectives of maintaining low and stable costs are becoming harder to achieve as supply-side variability intensifies and operating margins compress. At the same time, growing meteorological volatility is amplifying uncertainty all around: hydrologic conditions directly affect generation availability, while more extreme weather, especially during summer months, drives sharper and less predictable demand peaks.

2026 will offer more of the same. Significant shifts in snowpack, runoff timing, drought frequency, and extreme precipitation are expected to cause hydro shortages in late summer, coupled with higher power prices. To compound the problem, scarcity pricing will cluster in the evening ramp hours, as solar penetration rises and thermal capacity retires. The risk of unusually large rate shocks for customers is materially elevated in 2026 and beyond.

Historically, the hydro-reliant Pacific Northwest (PNW) region has been long on capacity. However, load growth and thermal retirements have tightened supply in recent years, driving elevated and more volatile power prices (though higher near-term prices are expected to decline with future renewable buildout). As a result, hydropower flows have shifted, and are continuing to shift. As shown in Figure 1, hydro exports from the PNW to California have decreased nearly 70% since 2020. The PNW is becoming structurally more expensive as more power remains in the PNW to account for tight supply conditions.

Solar buildout and load growth are also reshaping net load. Deliverability now depends more on interties and scarce flexibility, with volatility concentrating at seams and constrained transmission lines. In addition, limitations on thermal buildout in the PNW means that capacity value migrates toward storage and resources with deliverable flexibility.

Hydro plays a more limited role in California. While hydro serves as the system backbone in the PNW, with prices and scarcity conditions strongly dependent on the water year, annual hydro variability in California makes it hard to rely on. CAISO can see enormous year-to-year variation in hydro generation, with cascading dams increasing the operational complexity. When it comes to price dynamics, solar drives low on-peak prices while gas and carbon pricing drive higher off-peak prices.

For the PNW, connectivity with CAISO is useful for reserve margin management during low hydro years. As illustrated in Figure 2, CAISO can support peak load events without hydro or external imports, given its robust solar resources, solid storage, and moderate load growth. The PNW, however, remains highly reliant on hydro and needs either/both hydro and/or imports to meet peak load events currently and into the future.

Price dynamics within CAISO's Western Energy Imbalance Market (WEIM) will change as SPP Markets+ erodes WEIM participation. Citing concerns about CAISO governance, some notable WEIM participants, including Bonneville Power Authority and Arizona Public Service (APS), will leave the WEIM and join Markets+. This leaves the West fragmented between markets, and Arizona utilities SRP and APS islanded inside the WEIM and Extended Day-Ahead Market (EDAM).

However, the dynamics of the real-time energy imbalance market are expected to continue in a similar manner even as EDAM and SPP Markets+ coalesce into clear shape. The underlying resource, load and transmission infrastructure will not change dramatically. Transmission constraints and market seams will drive highly heterogeneous solar-weighted prices. Physical transmission limits will still impact power flows.

While imports and exports have stayed relatively constant between California and the Desert Southwest states over the past several years, Arizona's joining of SPP Markets+ will reduce this stability. Additionally, some members of the EDAM are pulling out of the Western Resource Adequacy Program (WRAP), thereby compounding the reliability question in Markets+ areas of the PNW.

Ultimately, a fragmented west will create new challenges alongside the benefits of market expansion. Market seams will decrease market efficiency, creating price gradients and decreasing access to imports in some places while increasing access in others. As these market seams form, utilities must consider whether previous sources of power and hedging will still be available, and evaluate whether new pricing and operational risks have emerged.

Because PNW portfolios are often hydro-heavy, near-term price risk can be mitigated by monthly forward block contract buys/sales, depending on position length. As illustrated in Figure 3, hedging can significantly narrow the band of expected risk for hydro assets.

Financial hedging addresses price and water risk. Optimal hedges, when added to portfolio, can minimize cost at risk (95th percentile cost minus average cost). Optimal hedges can vary monthly by on- and off-peak, and slice deals are a longer-term option for mitigating volumetric risk for a hydro asset owner by contracting out portions of the capacity to other parties in exchange for more stable power supply. For asset owners and operators, a well-hedged hydro portfolio provides cost and revenue stability regardless of price level while an unhedged portfolio has a gross margin that changes significantly depending on power price.

To mitigate risks associated with hydro-reliant portfolios, a critical first step involves designing and establishing trading risk management policies and procedures that set guardrails around asset operations and hedging strategies. These must account for stakeholder risk tolerance, hedging protocol design, authority delegation, as well as ongoing communication and reporting. These policies and procedures are essential not only for optimizing hedging outcomes but also for providing a robust framework of accountability should the organization’s strategies be scrutinized in the future.

To address the complexities of PNW and CAISO hydro portfolios, organizations must utilize forward hedging and advanced hedge structures. Implementing dynamic hedge protocols allows for more responsive risk management, directly contributing to rate stability and cost control.

Meaningful risk metrics can guide more informed, data-driven also allows for a much clearer way to inform portfolio management decisions.

The Ascend PowerSIMM™ suite is an energy analytics platform that captures the new and evolving dynamics of electricity markets. Utilities, public power entities, renewable developers, and community choice aggregators utilize PowerSIMM for optimal energy portfolio management, risk management, resource planning, and project optimization.

Access the full webinar now or contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)