Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

The Southwest Power Pool (SPP) has long been viewed as an energy market defined by inexpensive energy, surplus capacity, and backlogged interconnection queues. That perception no longer applies. Load growth, driven in part by SPP’s potential as a data center hub, is set to rise. With federal clean energy tax credits phasing out for new projects and existing wind projects nearing the end of their PTC window, SPP power prices are expected to become higher and more stable. For power market stakeholders, SPP has the potential to be the most interesting area of the US in terms of low-cost energy and data center siting. And benefiting from these dynamics requires moving quickly.

In a recent webinar previewing Ascend's latest SPP energy market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, and Dr. Brent Nelson, Managing Director of Markets and Strategy, discussed opportunities, risks, dynamics, and the importance of "striking while the iron is hot" in perhaps the most underappreciated power market in the US.

SPP holds strong opportunities for a variety of energy market stakeholders. From a load perspective, multiple driving forces make SPP attractive. Relatively high renewable penetration, along with high renewable potential, keeps wholesale power prices low. At the same time, gas prices are low and SPP possesses ample gas transmission infrastructure. While SPP has capacity requirements – which are met primarily in the form of bilateral contracts or guaranteed generation capacity – it has no capacity market and thus no skyrocketing capacity market costs such as those seen in PJM and other capacity markets. As a result, retail rates in SPP are significantly below national averages.

SPP also offers plenty of positives for data centers, especially those that need access to gas supply. Abundant gas infrastructure and some fiber pathways exist across SPP, as do large metro areas (often surrounded by cheap, plentiful land) such as Kansas City, Oklahoma City, Wichita, or Omaha.

From a decarbonization standpoint – which remains an important consideration for data centers – SPP offers abundant renewable resource potential. Wind resources in SPP are the strongest, most consistent, and cheapest in the US. Solar offers solid resource potential, too: southern SPP offers solar resources comparable to those found in Florida or Georgia.

On top of that, SPP created the High Impact Large Load (HILL) expedited review process to enable large loads to interconnect within 90 days. HILL includes two subtypes: the High Impact Large Load Generation Assessment (HILLGA) is for load that agrees to bring its own generation, while the Conditional High Impact Large Load (CHILL) pathway is for load that agrees to curtail during tight conditions. This process creates speed to power opportunities for data centers to enter SPP and come online quickly, which marks a significant difference relative to other logjammed US energy markets.

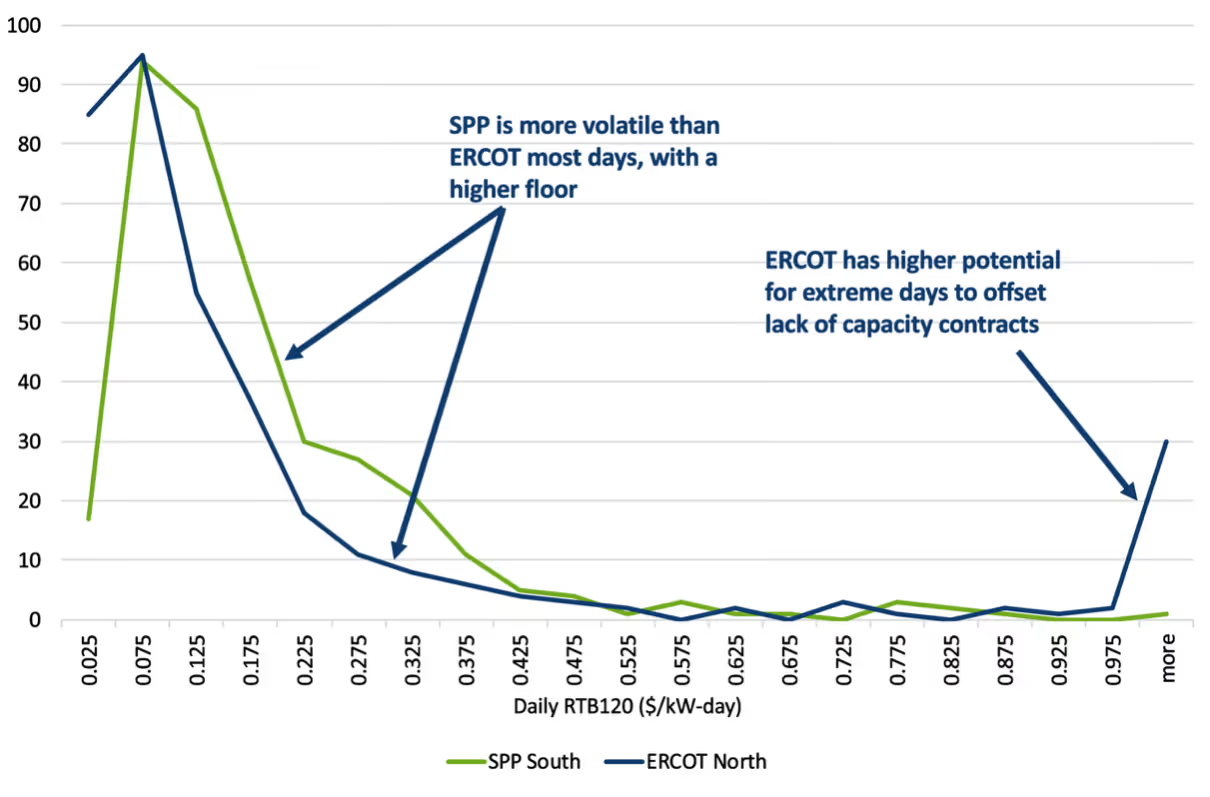

From a storage standpoint, SPP looks attractive for a variety of reasons. It offers year-round volatility and concrete needs for flexible capacity. As illustrated in Figure 1, SPP is actually more volatile than ERCOT most days and has a higher volatility floor during most years, even though ERCOT has more extreme pricing frequency. Extremes in SPP are flattened by the market's capacity construct: utilities must have bilateral contracts or their own generation to cover load, which becomes a stable revenue stream that offsets the inconsistent extreme conditions seen in ERCOT. This is a benefit, though: the ability to maintain a stable revenue structure presents another advantage for SPP relative to ERCOT or locations with capacity markets, which are also unstable.

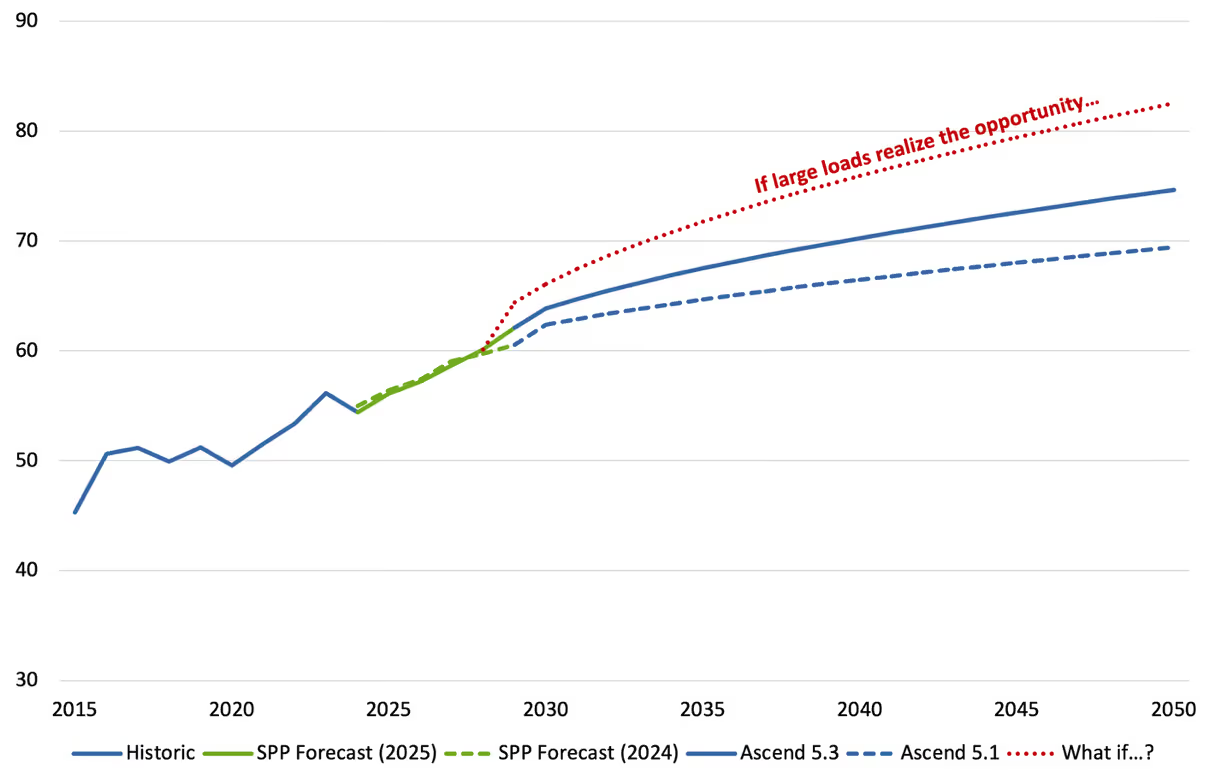

As with power markets everywhere, SPP needs more capacity. As shown in Figure 2, SPP has significantly raised its demand forecast on top of recently increasing its reserve margin requirement, amplifying the need for new capacity. If large loads realize the SPP potential, load could grow much more. This signals a recognition that SPP needs to start paying for capacity, and that a shortage was already materializing even before the data center impact. Two key uncertainties remain, though (which is true for all US energy markets): exactly how much capacity will be needed, and how quickly? \

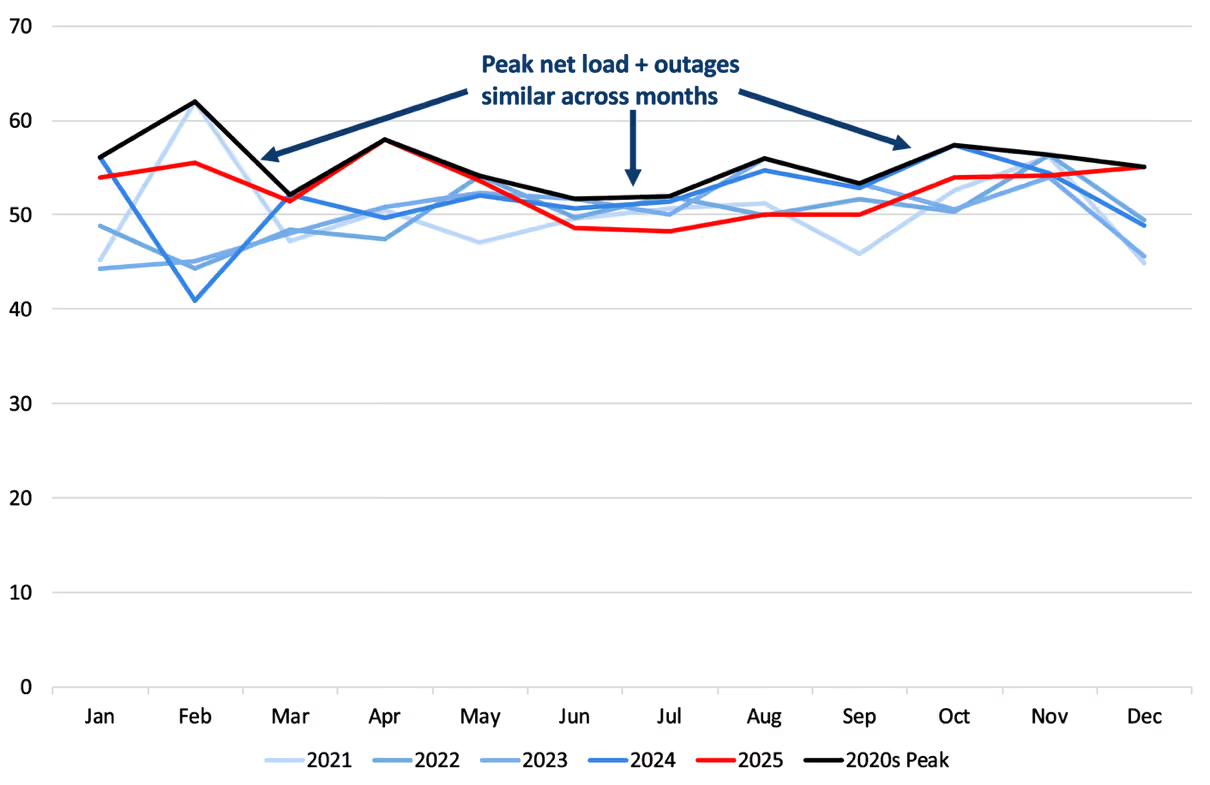

SPP is also somewhat unique in that it needs capacity across all seasons. As shown in Figure 3, SPP capacity needs stay relatively flat throughout the year when outages are included, with peaks slightly higher in the winter. In this context, storage is a well-suited capacity resource at moderate penetrations. Storage shows several GW of capacity value in both summer and winter seasons (once solar deployment grows), before increasing storage buildout erodes ELCC. There is a runway, though, before declines occur in capacity value for storage – thus increasing the value for near-term storage (and providing an associated advantage for those who move quickly to capture that value). Ascend’s modeling indicates that storage is the most economic capacity resource in SPP through the 2020s.

Similar opportunities exist for near-term renewables. PPA prices will rise as tax credits phase out, allowing higher long-run power prices that leave tax credit-eligible renewables highly economic.

From a thermal standpoint, new combustion turbine gas units make little to no economic sense until the mid-2030s, due primarily to supply shortages and currently exorbitant costs for new turbines. Combined cycle (CC) units, however, present a far more economic near-term thermal choice, and have the potential to overtake storage as a low-cost capacity resource by the early 2030s.

Access the full webinar recording, which offers additional insights related to SPP power prices, capacity prices, volatility projections, and emissions offset potential, as opportunities for where and when to invest in energy projects in SPP.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

The Southwest Power Pool (SPP) has long been viewed as an energy market defined by inexpensive energy, surplus capacity, and backlogged interconnection queues. That perception no longer applies. Load growth, driven in part by SPP’s potential as a data center hub, is set to rise. With federal clean energy tax credits phasing out for new projects and existing wind projects nearing the end of their PTC window, SPP power prices are expected to become higher and more stable. For power market stakeholders, SPP has the potential to be the most interesting area of the US in terms of low-cost energy and data center siting. And benefiting from these dynamics requires moving quickly.

In a recent webinar previewing Ascend's latest SPP energy market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, and Dr. Brent Nelson, Managing Director of Markets and Strategy, discussed opportunities, risks, dynamics, and the importance of "striking while the iron is hot" in perhaps the most underappreciated power market in the US.

SPP holds strong opportunities for a variety of energy market stakeholders. From a load perspective, multiple driving forces make SPP attractive. Relatively high renewable penetration, along with high renewable potential, keeps wholesale power prices low. At the same time, gas prices are low and SPP possesses ample gas transmission infrastructure. While SPP has capacity requirements – which are met primarily in the form of bilateral contracts or guaranteed generation capacity – it has no capacity market and thus no skyrocketing capacity market costs such as those seen in PJM and other capacity markets. As a result, retail rates in SPP are significantly below national averages.

SPP also offers plenty of positives for data centers, especially those that need access to gas supply. Abundant gas infrastructure and some fiber pathways exist across SPP, as do large metro areas (often surrounded by cheap, plentiful land) such as Kansas City, Oklahoma City, Wichita, or Omaha.

From a decarbonization standpoint – which remains an important consideration for data centers – SPP offers abundant renewable resource potential. Wind resources in SPP are the strongest, most consistent, and cheapest in the US. Solar offers solid resource potential, too: southern SPP offers solar resources comparable to those found in Florida or Georgia.

On top of that, SPP created the High Impact Large Load (HILL) expedited review process to enable large loads to interconnect within 90 days. HILL includes two subtypes: the High Impact Large Load Generation Assessment (HILLGA) is for load that agrees to bring its own generation, while the Conditional High Impact Large Load (CHILL) pathway is for load that agrees to curtail during tight conditions. This process creates speed to power opportunities for data centers to enter SPP and come online quickly, which marks a significant difference relative to other logjammed US energy markets.

From a storage standpoint, SPP looks attractive for a variety of reasons. It offers year-round volatility and concrete needs for flexible capacity. As illustrated in Figure 1, SPP is actually more volatile than ERCOT most days and has a higher volatility floor during most years, even though ERCOT has more extreme pricing frequency. Extremes in SPP are flattened by the market's capacity construct: utilities must have bilateral contracts or their own generation to cover load, which becomes a stable revenue stream that offsets the inconsistent extreme conditions seen in ERCOT. This is a benefit, though: the ability to maintain a stable revenue structure presents another advantage for SPP relative to ERCOT or locations with capacity markets, which are also unstable.

As with power markets everywhere, SPP needs more capacity. As shown in Figure 2, SPP has significantly raised its demand forecast on top of recently increasing its reserve margin requirement, amplifying the need for new capacity. If large loads realize the SPP potential, load could grow much more. This signals a recognition that SPP needs to start paying for capacity, and that a shortage was already materializing even before the data center impact. Two key uncertainties remain, though (which is true for all US energy markets): exactly how much capacity will be needed, and how quickly? \

SPP is also somewhat unique in that it needs capacity across all seasons. As shown in Figure 3, SPP capacity needs stay relatively flat throughout the year when outages are included, with peaks slightly higher in the winter. In this context, storage is a well-suited capacity resource at moderate penetrations. Storage shows several GW of capacity value in both summer and winter seasons (once solar deployment grows), before increasing storage buildout erodes ELCC. There is a runway, though, before declines occur in capacity value for storage – thus increasing the value for near-term storage (and providing an associated advantage for those who move quickly to capture that value). Ascend’s modeling indicates that storage is the most economic capacity resource in SPP through the 2020s.

Similar opportunities exist for near-term renewables. PPA prices will rise as tax credits phase out, allowing higher long-run power prices that leave tax credit-eligible renewables highly economic.

From a thermal standpoint, new combustion turbine gas units make little to no economic sense until the mid-2030s, due primarily to supply shortages and currently exorbitant costs for new turbines. Combined cycle (CC) units, however, present a far more economic near-term thermal choice, and have the potential to overtake storage as a low-cost capacity resource by the early 2030s.

Access the full webinar recording, which offers additional insights related to SPP power prices, capacity prices, volatility projections, and emissions offset potential, as opportunities for where and when to invest in energy projects in SPP.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)