Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

ERCOT’s unique energy market design creates a revenue environment defined by extremes, in which short periods of high volatility, high generator earnings, and high load costs are followed by long stretches of low volatility and prices. Without a true capacity market or centralized planning to smooth out the variability inherent in design, power market stakeholders must ride a roller coaster whose peaks depend on infrequent occurrences such as extreme heat with low wind or deep winter cold coupled with thermal outages. In this context, a critical question emerges: how should developers, IPPs, utilities, retailers, investors, and corporates plan, invest, and hedge in a system built on increasingly infrequent scarcity?

In a webinar previewing Ascend's most recent ERCOT power market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss how ERCOT energy market stakeholders can maximize and stabilize revenue in an inherently unstable market, as well as why structural changes in ERCOT's forward markets have led to near-term price dynamics that are not supported by fundamentals.

Although ERCOT does not technically have a capacity market, its reliance on scarcity pricing makes it functionally similar to one. In practice, ERCOT operates like a traditional capacity market: all resources receive the same clearing price, which creates windfalls for existing generators. ERCOT faces challenges similar to those in other US capacity markets in terms of incentivizing new entry: to do so, prices must go high and stay high. As seen in other capacity markets, this creates political blowback.

A key difference, however, has to do with timing: typical capacity markets procure resources ahead of time to prevent scarcity, while ERCOT's just-in-time structure necessitates scarcity to produce revenues. Thus, ERCOT's scarcity instability is persistent, necessary and variable from year to year, and will remain so unless and until the market design changes.

For energy market participants, the result is a roller coaster market defined by boom-and-bust dynamics. Recent reserve margin patterns illustrate this, as shown in Figure 1. 2023 saw extended periods in the 'danger zone,' while 2024 and 2025 remained mostly stable; 2026 is expected to look similar to 2024 with limited potential for tight conditions.

Scarcity in ERCOT has historically been most pronounced during summer heat waves. A new problem is emerging as the supply stack shifts: winters are bringing larger reliability risks, even though gross load remains higher during summers – about 85 GW compared to around 80 GW during winter. However, plotting net load combined with thermal outages produces peaks that are very similar in winter and summer, which means the overall magnitude in terms of total resources needed to serve either a winter or summer peak is also similar.

A key emerging issue, though is that the ERCOT resource stack is much better suited to serve these net load peaks in summer than in winter peaks. In summer, the gross load peak occurs during the daytime and is well-served by solar generation. Net load has peaks for a few hours around sunset, and thus is well suited to being served by batteries. Winters typically bring long, flat, overnight peaks that cannot be served by solar and are poorly served by batteries with relatively limited duration. Thus, if ERCOT has enough resources to serve a winter peak, then it will have a surplus during the summer. If the market has just enough to serve summer peaks, then Texas will have blackouts during the winter. It is far more likely that ERCOT will have enough capacity to serve winter, and that summer scarcity will diminish as a major reliability issue.

This presents another problem, however, for building new capacity in ERCOT. Summer heat waves are reliable; winter storms are relatively rare. As the associated scarcity 'booms' become rarer, ERCOT may transition to a state where significant pricing events happen only once every five or ten years. For developers looking at projects with 15-year-lives, that rarity of scarcity has serious implications for debt coverage.

On the load side, winter peaking brings a fundamental misalignment between peak demand and supply availability. For electricity retailers or load-serving entities, figuring out how to incentivize peak shifting – whether through demand response programs, energy efficiency measures, rate structures, or other incentives – is more important than ever.

As scarcity – and resulting scarcity revenue – becomes increasingly rare, generators still need stable revenues and a way to cover debt service. Four key options exist for managing ERCOT's boom-and-bust nature.

Subsidized loans are a possibility, though they still carry a default risk and require political support. The Texas Energy Fund (TEF) was created for this purpose and has provided subsidized loans exclusively to new gas. This effort has produced limited results. Nearly all projects that received funds were already in development before the program was created. Thus, the TEF did not actually spur new development as much as it helped to move existing projects across the finish line. Timing is problematic, too. Gas turbines are prohibitively expensive and will be for the near future, and revenue instability continues to pose a major problem. The TEF may be underestimating its own default risk.

Tolling options also exist in ERCOT but are limited. Some of Texas' largest publicly owned utilities have signed a limited number of deals, as have a few other load-serving entities and financial firms. However, the tolling market in ERCOT has shallow depth. Revenue guarantees, such as the type offered by Ascend's EnSurance™, can be powerful tools in making sure that projects retain upside revenue potential while mitigating downside risk. These instruments, however, are limited and require custom arrangements.

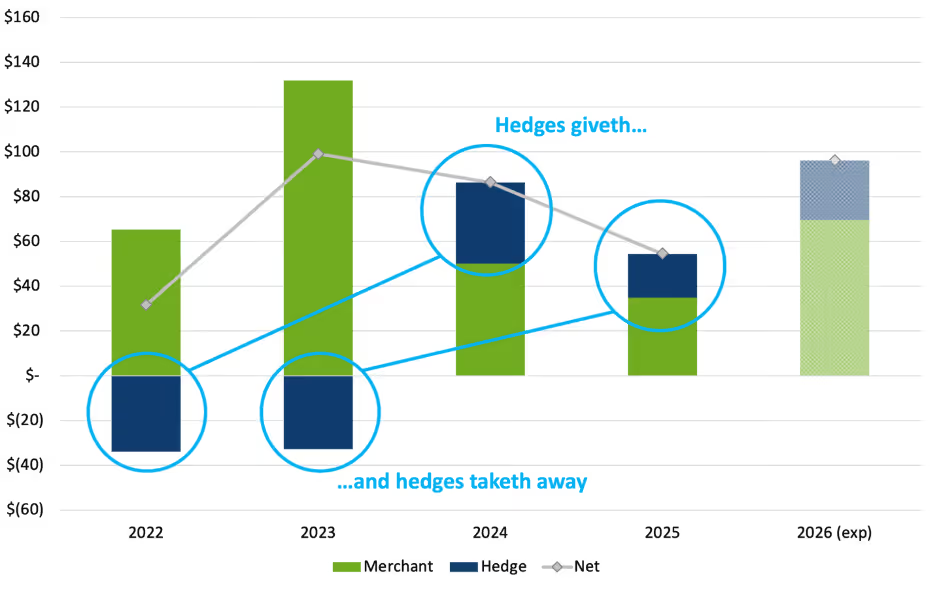

Ultimately, forward market hedging is where generators can best flatten out the revenue instability that comes with riding the ERCOT roller coaster. Forward market hedging allows both load and generation to smooth irregular scarcity conditions into average expected values. As seen in Figure 2, hedging can decrease revenues in windfall years, while adding significant revenue in mild years. Hedges can be optimally sized to minimize revenue uncertainty, with the hedge and merchant revenues carrying offsetting risks. Portfolio optimization and risk management solutions, such as those offered by Ascend's PowerSIMM™ platform and associated consulting services, can be highly effective in creating optimal hedging strategies for energy assets.

Historically, forward markets in ERCOT have been close to correct, on average. A singular problem has emerged recently, however. During 2024 and 2025, forwards missed badly – and high – as markets priced in scarcity events that failed to emerge as reserve margins in ERCOT grew substantially with solar and storage additions. Forwards for 2026 look similar to 2024, but the size of the reserve margins in ERCOT make these forward prices difficult to justify.

Why are forward markets in ERCOT missing so badly? It is Ascend's view that a structural change related to supply and demand in forward markets has occurred, with load-serving entities wanting to hedge more load in the forward markets than there are generators willing to sell forward contracts. On-peak contracts are long in duration, presenting challenges for standalone solar and standalone storage that cannot cover all the hours of an on-peak block even as they serve substantial portions of the ERCOT demand profile. Super-peak and TB4 forward contracts are easier for these resources to cover, but are thinly traded. As a result, the imbalance between buyers and sellers in forward markets is keeping prices high in 2026 despite the widening reserve margin from new solar and batteries that have eased tight conditions. The reserve margin in ERCOT is not expected to tighten until 2027, thus forward market hedges (especially during summer) are likely to provide strong value in 2026 for generators.

Access the full webinar recording, which offers additional insights related to ERCOT forward markets in 2026, optimal hedging strategies for load and generation, a demonstration of Ascend's data visualization tools, and guidance for thermal, renewable, and storage operators in ERCOT.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

ERCOT’s unique energy market design creates a revenue environment defined by extremes, in which short periods of high volatility, high generator earnings, and high load costs are followed by long stretches of low volatility and prices. Without a true capacity market or centralized planning to smooth out the variability inherent in design, power market stakeholders must ride a roller coaster whose peaks depend on infrequent occurrences such as extreme heat with low wind or deep winter cold coupled with thermal outages. In this context, a critical question emerges: how should developers, IPPs, utilities, retailers, investors, and corporates plan, invest, and hedge in a system built on increasingly infrequent scarcity?

In a webinar previewing Ascend's most recent ERCOT power market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss how ERCOT energy market stakeholders can maximize and stabilize revenue in an inherently unstable market, as well as why structural changes in ERCOT's forward markets have led to near-term price dynamics that are not supported by fundamentals.

Although ERCOT does not technically have a capacity market, its reliance on scarcity pricing makes it functionally similar to one. In practice, ERCOT operates like a traditional capacity market: all resources receive the same clearing price, which creates windfalls for existing generators. ERCOT faces challenges similar to those in other US capacity markets in terms of incentivizing new entry: to do so, prices must go high and stay high. As seen in other capacity markets, this creates political blowback.

A key difference, however, has to do with timing: typical capacity markets procure resources ahead of time to prevent scarcity, while ERCOT's just-in-time structure necessitates scarcity to produce revenues. Thus, ERCOT's scarcity instability is persistent, necessary and variable from year to year, and will remain so unless and until the market design changes.

For energy market participants, the result is a roller coaster market defined by boom-and-bust dynamics. Recent reserve margin patterns illustrate this, as shown in Figure 1. 2023 saw extended periods in the 'danger zone,' while 2024 and 2025 remained mostly stable; 2026 is expected to look similar to 2024 with limited potential for tight conditions.

Scarcity in ERCOT has historically been most pronounced during summer heat waves. A new problem is emerging as the supply stack shifts: winters are bringing larger reliability risks, even though gross load remains higher during summers – about 85 GW compared to around 80 GW during winter. However, plotting net load combined with thermal outages produces peaks that are very similar in winter and summer, which means the overall magnitude in terms of total resources needed to serve either a winter or summer peak is also similar.

A key emerging issue, though is that the ERCOT resource stack is much better suited to serve these net load peaks in summer than in winter peaks. In summer, the gross load peak occurs during the daytime and is well-served by solar generation. Net load has peaks for a few hours around sunset, and thus is well suited to being served by batteries. Winters typically bring long, flat, overnight peaks that cannot be served by solar and are poorly served by batteries with relatively limited duration. Thus, if ERCOT has enough resources to serve a winter peak, then it will have a surplus during the summer. If the market has just enough to serve summer peaks, then Texas will have blackouts during the winter. It is far more likely that ERCOT will have enough capacity to serve winter, and that summer scarcity will diminish as a major reliability issue.

This presents another problem, however, for building new capacity in ERCOT. Summer heat waves are reliable; winter storms are relatively rare. As the associated scarcity 'booms' become rarer, ERCOT may transition to a state where significant pricing events happen only once every five or ten years. For developers looking at projects with 15-year-lives, that rarity of scarcity has serious implications for debt coverage.

On the load side, winter peaking brings a fundamental misalignment between peak demand and supply availability. For electricity retailers or load-serving entities, figuring out how to incentivize peak shifting – whether through demand response programs, energy efficiency measures, rate structures, or other incentives – is more important than ever.

As scarcity – and resulting scarcity revenue – becomes increasingly rare, generators still need stable revenues and a way to cover debt service. Four key options exist for managing ERCOT's boom-and-bust nature.

Subsidized loans are a possibility, though they still carry a default risk and require political support. The Texas Energy Fund (TEF) was created for this purpose and has provided subsidized loans exclusively to new gas. This effort has produced limited results. Nearly all projects that received funds were already in development before the program was created. Thus, the TEF did not actually spur new development as much as it helped to move existing projects across the finish line. Timing is problematic, too. Gas turbines are prohibitively expensive and will be for the near future, and revenue instability continues to pose a major problem. The TEF may be underestimating its own default risk.

Tolling options also exist in ERCOT but are limited. Some of Texas' largest publicly owned utilities have signed a limited number of deals, as have a few other load-serving entities and financial firms. However, the tolling market in ERCOT has shallow depth. Revenue guarantees, such as the type offered by Ascend's EnSurance™, can be powerful tools in making sure that projects retain upside revenue potential while mitigating downside risk. These instruments, however, are limited and require custom arrangements.

Ultimately, forward market hedging is where generators can best flatten out the revenue instability that comes with riding the ERCOT roller coaster. Forward market hedging allows both load and generation to smooth irregular scarcity conditions into average expected values. As seen in Figure 2, hedging can decrease revenues in windfall years, while adding significant revenue in mild years. Hedges can be optimally sized to minimize revenue uncertainty, with the hedge and merchant revenues carrying offsetting risks. Portfolio optimization and risk management solutions, such as those offered by Ascend's PowerSIMM™ platform and associated consulting services, can be highly effective in creating optimal hedging strategies for energy assets.

Historically, forward markets in ERCOT have been close to correct, on average. A singular problem has emerged recently, however. During 2024 and 2025, forwards missed badly – and high – as markets priced in scarcity events that failed to emerge as reserve margins in ERCOT grew substantially with solar and storage additions. Forwards for 2026 look similar to 2024, but the size of the reserve margins in ERCOT make these forward prices difficult to justify.

Why are forward markets in ERCOT missing so badly? It is Ascend's view that a structural change related to supply and demand in forward markets has occurred, with load-serving entities wanting to hedge more load in the forward markets than there are generators willing to sell forward contracts. On-peak contracts are long in duration, presenting challenges for standalone solar and standalone storage that cannot cover all the hours of an on-peak block even as they serve substantial portions of the ERCOT demand profile. Super-peak and TB4 forward contracts are easier for these resources to cover, but are thinly traded. As a result, the imbalance between buyers and sellers in forward markets is keeping prices high in 2026 despite the widening reserve margin from new solar and batteries that have eased tight conditions. The reserve margin in ERCOT is not expected to tighten until 2027, thus forward market hedges (especially during summer) are likely to provide strong value in 2026 for generators.

Access the full webinar recording, which offers additional insights related to ERCOT forward markets in 2026, optimal hedging strategies for load and generation, a demonstration of Ascend's data visualization tools, and guidance for thermal, renewable, and storage operators in ERCOT.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)