Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Forward power and gas markets remain one of the clearest and most information-dense signals available for understanding where prices are headed and why they're headed in a specific direction. When interpreted correctly, forwards reveal expectations about fundamentals, market-wide risk expectations and appetites, the linkage between gas and power, and structural stresses embedded in specific regions – all of which are key components for an effective power market forecast.

In a recent webinar, Connor Donovan, Forecasting Manager at Ascend Analytics, discussed the essentials of forward markets, why forward markets are so crucial to Ascend forecasts, and how to interpret forward markets through both a fundamental and a risk-based lens.

Forward markets aggregate the views of stakeholders such as utilities, generators, corporates, traders, and investors, all of which are trading in energy markets to hedge portfolios, make investment decisions, make contracting decisions, and more. Because these stakeholders each possess different objectives and risk appetites, the consensus they represent is diverse, economically meaningful, and offers the best risk-adjusted view of the near term.

Forward markets are crucial for signaling when new capacity is needed in a market, or alternatively, when existing capacity is sufficient to meet expected demand. Ultimately, forwards reflect where power and gas are trading today for delivery months or years in the future. Unlike simple historical averages, however, forwards compress two critical dimensions into a single price signal:

Forward power prices are inseparable from gas economics in thermal-dominated markets. Comparing power forwards to gas forwards derives implied heat rates, which indicate what type of generation is expected to set the marginal price.

This linkage is crucial. It reveals what prices might be and which assets are likely on the margin – and under what operating conditions.

In reality, forwards represent risk-adjusted prices, rather than just predictions of future spot prices. Forward markets assign value to low-probability, high-impact events such as extreme weather, fuel disruptions, transmission constraints, or policy shocks. Because of this, forward price distributions are often asymmetric: the mean and the most likely outcome (the mode) are not the same.

The persistent gap between forward prices and realized spot prices represents a risk premium, not a forecasting error.

Every long-term valuation at Ascend starts with the merit order curve, which is a ranking of generation units by marginal cost, paired with the forward market view.

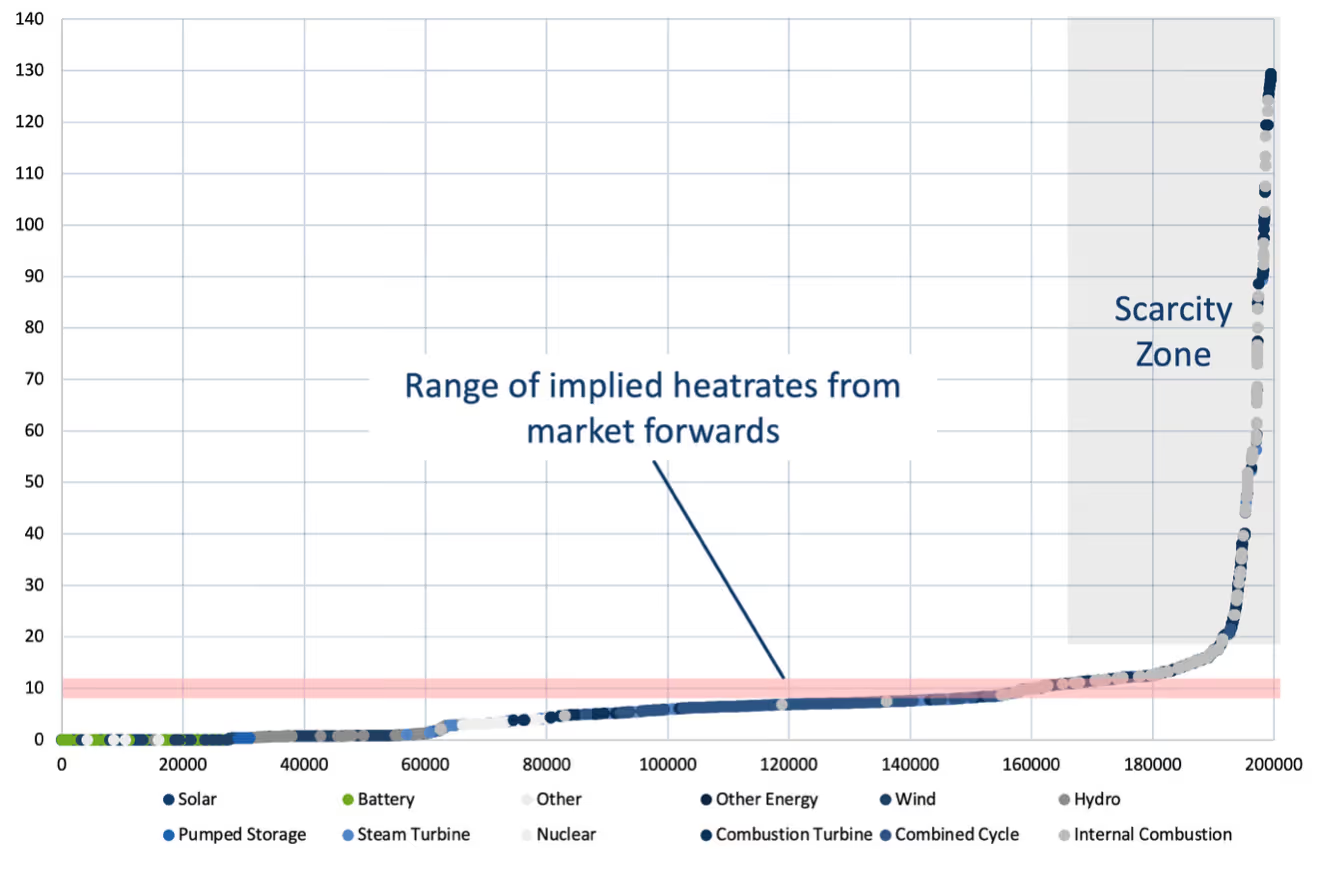

For example, the MISO supply stack includes roughly 160–180 GW of capacity across thousands of units. As illustrated in Figure 1, The curve reveals two regimes:

Recent MISO forwards imply heat rates between roughly 8.5 and 12, signaling that combined cycles, combustion turbines, and hydro are setting prices. The takeaway is straightforward: near-term MISO pricing remains firmly tied to thermal economics.

Comparing implied heat rates across markets highlights where systems are approaching scarcity.

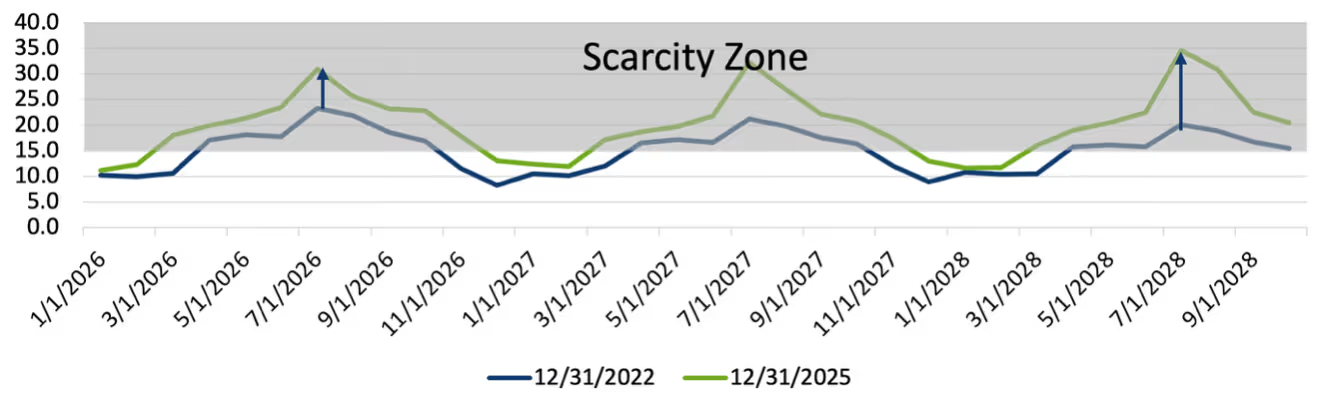

In PJM, for example, the forward curve has shifted decisively into the scarcity zone, as illustrated in Figure 2. This aligns with structural load growth and is reinforced by sharply higher capacity auction clearing prices, which serves as an unambiguous signal that new capacity is needed.

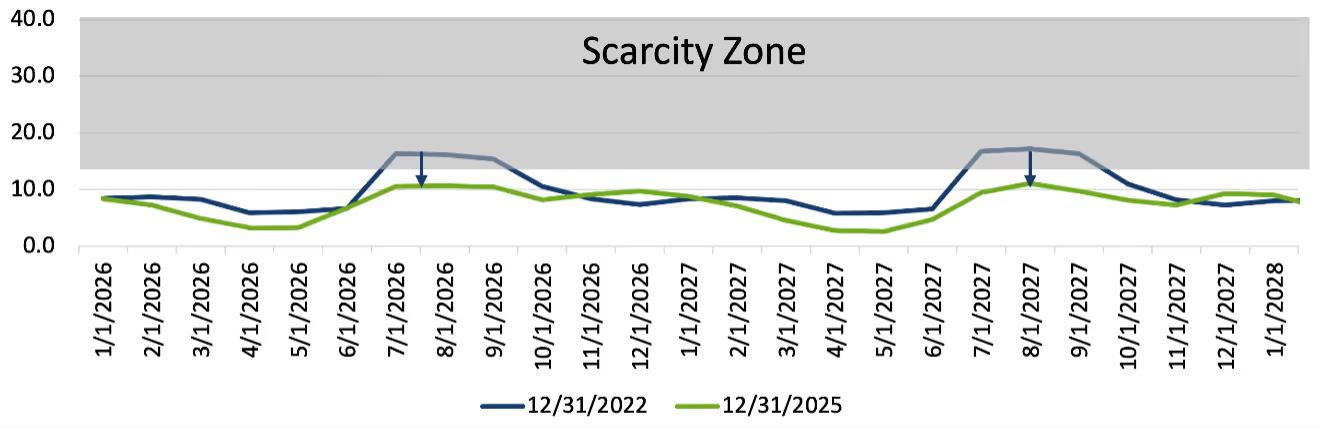

In CAISO, as illustrated in Figure 3, the opposite has occurred. After years of pricing extreme summer risk, forwards have drifted back toward normal thermal conditions, suggesting the system is currently better positioned to meet expected load. These signals are not speculative: they are embedded directly in traded prices.

Yes. Forward price differentials often reveal evolving interregional dynamics, such as those occurring in the California and Mid-Columbia energy markets. Historically, California imported hydropower from the Pacific Northwest. Today, that spread has inverted, with Mid-C forwards pricing well above California during several periods.

This suggests that the Northwest is either retaining more power or seeking imports, reflecting growing uncertainty around hydro conditions, congestion risk, and basis exposure.

Forward markets behave differently near the prompt month versus years out:

As a delivery date draws near, risk premiums should decline as uncertainty resolves and forwards converge toward spot prices.

When forwards fail to converge – even weeks before delivery – it signals something more significant than delayed information.

In ERCOT, for example, summer forwards in 2024 and 2025 retained a premium well into the delivery window, trading at 2-3x the spot price even just two weeks ahead of delivery. This reflected a structural feature of the market: frequent high-impact events that are difficult or impossible to hedge against. In ERCOT, this risk premium represented the market functioning as designed, in which participants in a market known for volatility events were trying to price in a potential blowout that could have, in their estimation, emerged at any point.

Trusted across hundreds of deals and more than $1 billion in transaction value, PowerVAL provides bankable revenue forecasts and nodal-specific valuations for storage, renewables, and hybrid projects under multiple operating strategies across all ISOs. PowerVAL visualizations can be used to work with forward data, and can automatically adjust revenue expectations, and help reveal revenue opportunities associated with locking in inflated forward prices. Please contact us to learn more.

Forward power and gas markets remain one of the clearest and most information-dense signals available for understanding where prices are headed and why they're headed in a specific direction. When interpreted correctly, forwards reveal expectations about fundamentals, market-wide risk expectations and appetites, the linkage between gas and power, and structural stresses embedded in specific regions – all of which are key components for an effective power market forecast.

In a recent webinar, Connor Donovan, Forecasting Manager at Ascend Analytics, discussed the essentials of forward markets, why forward markets are so crucial to Ascend forecasts, and how to interpret forward markets through both a fundamental and a risk-based lens.

Forward markets aggregate the views of stakeholders such as utilities, generators, corporates, traders, and investors, all of which are trading in energy markets to hedge portfolios, make investment decisions, make contracting decisions, and more. Because these stakeholders each possess different objectives and risk appetites, the consensus they represent is diverse, economically meaningful, and offers the best risk-adjusted view of the near term.

Forward markets are crucial for signaling when new capacity is needed in a market, or alternatively, when existing capacity is sufficient to meet expected demand. Ultimately, forwards reflect where power and gas are trading today for delivery months or years in the future. Unlike simple historical averages, however, forwards compress two critical dimensions into a single price signal:

Forward power prices are inseparable from gas economics in thermal-dominated markets. Comparing power forwards to gas forwards derives implied heat rates, which indicate what type of generation is expected to set the marginal price.

This linkage is crucial. It reveals what prices might be and which assets are likely on the margin – and under what operating conditions.

In reality, forwards represent risk-adjusted prices, rather than just predictions of future spot prices. Forward markets assign value to low-probability, high-impact events such as extreme weather, fuel disruptions, transmission constraints, or policy shocks. Because of this, forward price distributions are often asymmetric: the mean and the most likely outcome (the mode) are not the same.

The persistent gap between forward prices and realized spot prices represents a risk premium, not a forecasting error.

Every long-term valuation at Ascend starts with the merit order curve, which is a ranking of generation units by marginal cost, paired with the forward market view.

For example, the MISO supply stack includes roughly 160–180 GW of capacity across thousands of units. As illustrated in Figure 1, The curve reveals two regimes:

Recent MISO forwards imply heat rates between roughly 8.5 and 12, signaling that combined cycles, combustion turbines, and hydro are setting prices. The takeaway is straightforward: near-term MISO pricing remains firmly tied to thermal economics.

Comparing implied heat rates across markets highlights where systems are approaching scarcity.

In PJM, for example, the forward curve has shifted decisively into the scarcity zone, as illustrated in Figure 2. This aligns with structural load growth and is reinforced by sharply higher capacity auction clearing prices, which serves as an unambiguous signal that new capacity is needed.

In CAISO, as illustrated in Figure 3, the opposite has occurred. After years of pricing extreme summer risk, forwards have drifted back toward normal thermal conditions, suggesting the system is currently better positioned to meet expected load. These signals are not speculative: they are embedded directly in traded prices.

Yes. Forward price differentials often reveal evolving interregional dynamics, such as those occurring in the California and Mid-Columbia energy markets. Historically, California imported hydropower from the Pacific Northwest. Today, that spread has inverted, with Mid-C forwards pricing well above California during several periods.

This suggests that the Northwest is either retaining more power or seeking imports, reflecting growing uncertainty around hydro conditions, congestion risk, and basis exposure.

Forward markets behave differently near the prompt month versus years out:

As a delivery date draws near, risk premiums should decline as uncertainty resolves and forwards converge toward spot prices.

When forwards fail to converge – even weeks before delivery – it signals something more significant than delayed information.

In ERCOT, for example, summer forwards in 2024 and 2025 retained a premium well into the delivery window, trading at 2-3x the spot price even just two weeks ahead of delivery. This reflected a structural feature of the market: frequent high-impact events that are difficult or impossible to hedge against. In ERCOT, this risk premium represented the market functioning as designed, in which participants in a market known for volatility events were trying to price in a potential blowout that could have, in their estimation, emerged at any point.

Trusted across hundreds of deals and more than $1 billion in transaction value, PowerVAL provides bankable revenue forecasts and nodal-specific valuations for storage, renewables, and hybrid projects under multiple operating strategies across all ISOs. PowerVAL visualizations can be used to work with forward data, and can automatically adjust revenue expectations, and help reveal revenue opportunities associated with locking in inflated forward prices. Please contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)