Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Interconnection queues across the US are no longer just congested: they are overwhelmed. In ERCOT, 198 GW of large load applied for interconnection in the first quarter of 2026 alone, with 86 GW of new load requests under review, which is roughly equal to the current size of ERCOT’s peak load. PJM is grappling with a capacity shortfall that could reach 15 GW by 2030 as new load additions outpace new generation. As load growth continues to soar, it is becoming evident that the rules, infrastructure, and processes governing large load interconnection were designed for a different era, and that market reforms in ISOs across the country are badly needed.

In a recent Ascend Analytics webinar on transmission and market modeling for data center and power project siting, Robert LaFaso, Director of Forecasting and Valuation, Dr. Michael Fisher, Managing Director of Evaluation Services, and Dr. Shalom Goffri, VP of Valuation and Portfolio Management, examined the state of large load interconnection across PJM, ERCOT, and SPP, and discussed what proposed market reforms might mean for developers and hyperscalers competing for grid access.

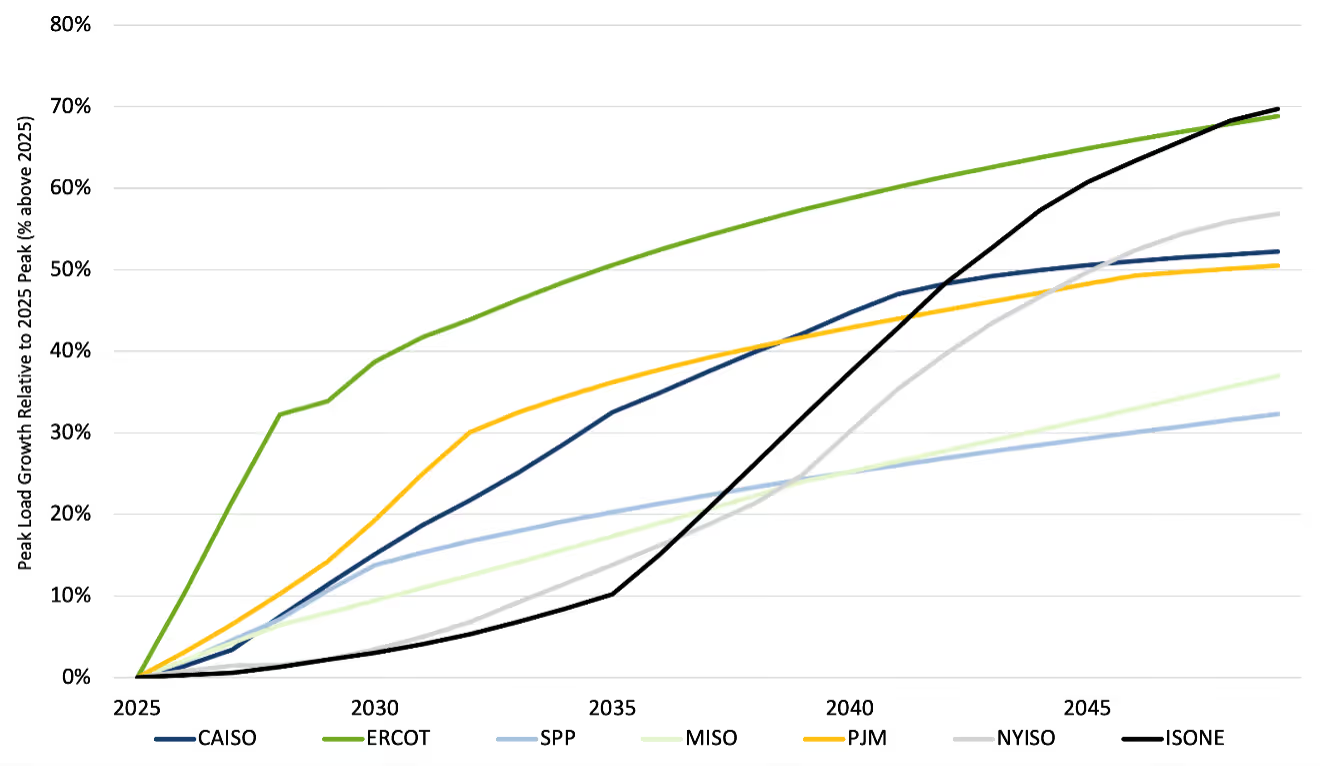

Given the sheer scale of projected load growth in U.S. energy markets, as shown in Figure 1, ISOs are being forced to fundamentally rethink how large loads enter the grid.

PJM’s emerging framework, for example, creates two new types of load. In contrast to historical approaches to reliability planning, PJM will now allow large loads to interconnect without a requirement that the capacity auction furnish resources to serve the load during peak grid-stress events. This category of Non-Capacity-Backed-Load (NCBL) accepts curtailment before traditional load when the market is unavailable to provide energy to serve all loads. In exchange for this risk-taking, the load is able to enter the market without waiting for new generation. PJM’s backstop procurement mechanism will create stable revenue incentives for new generation to close the capacity shortfall in the near term. However, long-term reform of the capacity market structure is still required, and BTM solutions for site power will enable high load-factor service before the backstop auction resolves generation shortfall in the early 2030s.

PJM’s second new category is the transmission corollary to NCBL. Rather than entering early before generation is built, these interim network integration transmission service (NITS) projects are interconnecting before new transmission is built to serve them. Similar to NCBL, these projects take curtailment before traditional load. However, reflecting the key physical nature of transmission limits, interim NITS loads are curtailed before NCBL loads. In the long term, these interim NITS projects will be served by new transmission. However, timelines for the new service are long and uncertain, making interim NITS projects highly dependent on BTM solutions for firm power.

While ERCOT’s approach may be similar to PJM’s in intent, it differs in structure. Without a capacity market, ERCOT has no direct mechanism to guarantee that generation comes online to serve new load. Instead, ERCOT sets a reserve margin target and uses batch study results to determine how much load can enter the system without violating that threshold and without violating transmission line limits. Large loads with BTM generation are treated more favorably in the batch study process. SB6 requires all large loads to curtail during specific emergency conditions; however, loads with BTM generation made available to ERCOT during scarcity events make their integration a much simpler problem. ERCOT’s in-progress reform of its Four Coincident Peak (4CP) program will also shift BTM generation’s function from cost control to grid enablement, which marks a significant change for how developers size and operate their on-site resources.

The Southwest Power Pool (SPP) has recently developed expedited review processes for large loads that create opportunities for data centers to come online quickly, which marks a significant difference relative to other logjammed U.S. energy markets. SPP offers three distinct pathways for large loads:

Under SPP’s framework, a load can be served by a combination of firm service, CHILLS, and HILLGA generation simultaneously. That flexibility allows developers to phase their interconnection strategy, securing some firm capacity while using non-firm bridge arrangements to come online faster, then transitioning toward firmness as transmission upgrades are completed. The 90-day HILLGA study timeline directly addresses the speed-to-power constraint that has driven many projects toward BTM approaches. Critically, however, SPP does not offer a pathway that is equivalent to the NCBL process in PJM.

For data center developers seeking rapid grid access, BTM thermal generation is an understandable near-term solution. When speed to market is the primary consideration, BTM gas can get a facility online quickly and serve as a reliable stopgap until a grid connection is established.

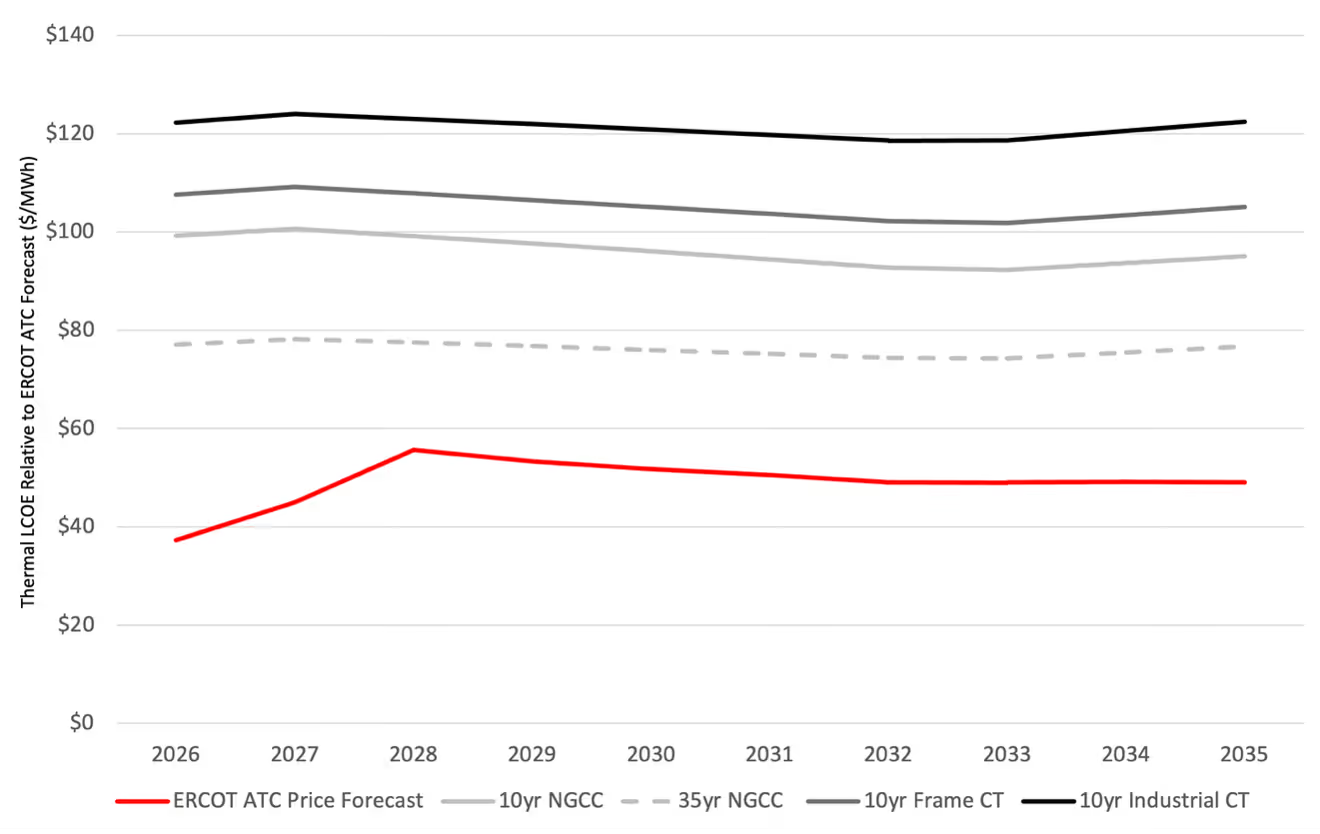

It is an expensive proposition, though. As illustrated in Figure 2, the LCOE for BTM natural gas generation exceeds ERCOT’s projected ATC forward price across every thermal configuration, in many cases by a wide margin. An industrial combustion turbine (CT) running at high capacity-factor carries an LCOE above $120 per megawatt-hour (MWh). Even a natural gas combined cycle (NGCC) plant with a 35-year asset life, which stretches far beyond the decarbonization commitments most hyperscalers have made, still prices above ERCOT’s grid cost forecast.

BTM storage, however, offers multiple advantages. In non-curtailment hours, which make up the vast majority of any given year, the load can take grid power. However, BTM storage can participate in critical peak reduction programs in different ISOs to reduce transmission cost allocation, provide ancillary services, and execute energy arbitrage. Additionally, while ISOs may assign limited accreditation value to duration-limited resources due to concerns over performance during tail events, BTM storage can effectively receive 100% accreditation by reducing on-site peak demand during “critical peak” events that can be relatively easy to predict in certain markets.

The full webinar recording offers additional insights related to large load interconnection reform across PJM, ERCOT, and SPP, flexible interconnection design, and transmission modeling for data center and power project siting.

Trusted across hundreds of deals and more than $1 billion in transaction value, PowerVAL provides bankable revenue forecasts and nodal-specific valuations for storage, renewables, and hybrid projects under multiple operating strategies across all ISOs. Please contact us to learn more.

Interconnection queues across the US are no longer just congested: they are overwhelmed. In ERCOT, 198 GW of large load applied for interconnection in the first quarter of 2026 alone, with 86 GW of new load requests under review, which is roughly equal to the current size of ERCOT’s peak load. PJM is grappling with a capacity shortfall that could reach 15 GW by 2030 as new load additions outpace new generation. As load growth continues to soar, it is becoming evident that the rules, infrastructure, and processes governing large load interconnection were designed for a different era, and that market reforms in ISOs across the country are badly needed.

In a recent Ascend Analytics webinar on transmission and market modeling for data center and power project siting, Robert LaFaso, Director of Forecasting and Valuation, Dr. Michael Fisher, Managing Director of Evaluation Services, and Dr. Shalom Goffri, VP of Valuation and Portfolio Management, examined the state of large load interconnection across PJM, ERCOT, and SPP, and discussed what proposed market reforms might mean for developers and hyperscalers competing for grid access.

Given the sheer scale of projected load growth in U.S. energy markets, as shown in Figure 1, ISOs are being forced to fundamentally rethink how large loads enter the grid.

PJM’s emerging framework, for example, creates two new types of load. In contrast to historical approaches to reliability planning, PJM will now allow large loads to interconnect without a requirement that the capacity auction furnish resources to serve the load during peak grid-stress events. This category of Non-Capacity-Backed-Load (NCBL) accepts curtailment before traditional load when the market is unavailable to provide energy to serve all loads. In exchange for this risk-taking, the load is able to enter the market without waiting for new generation. PJM’s backstop procurement mechanism will create stable revenue incentives for new generation to close the capacity shortfall in the near term. However, long-term reform of the capacity market structure is still required, and BTM solutions for site power will enable high load-factor service before the backstop auction resolves generation shortfall in the early 2030s.

PJM’s second new category is the transmission corollary to NCBL. Rather than entering early before generation is built, these interim network integration transmission service (NITS) projects are interconnecting before new transmission is built to serve them. Similar to NCBL, these projects take curtailment before traditional load. However, reflecting the key physical nature of transmission limits, interim NITS loads are curtailed before NCBL loads. In the long term, these interim NITS projects will be served by new transmission. However, timelines for the new service are long and uncertain, making interim NITS projects highly dependent on BTM solutions for firm power.

While ERCOT’s approach may be similar to PJM’s in intent, it differs in structure. Without a capacity market, ERCOT has no direct mechanism to guarantee that generation comes online to serve new load. Instead, ERCOT sets a reserve margin target and uses batch study results to determine how much load can enter the system without violating that threshold and without violating transmission line limits. Large loads with BTM generation are treated more favorably in the batch study process. SB6 requires all large loads to curtail during specific emergency conditions; however, loads with BTM generation made available to ERCOT during scarcity events make their integration a much simpler problem. ERCOT’s in-progress reform of its Four Coincident Peak (4CP) program will also shift BTM generation’s function from cost control to grid enablement, which marks a significant change for how developers size and operate their on-site resources.

The Southwest Power Pool (SPP) has recently developed expedited review processes for large loads that create opportunities for data centers to come online quickly, which marks a significant difference relative to other logjammed U.S. energy markets. SPP offers three distinct pathways for large loads:

Under SPP’s framework, a load can be served by a combination of firm service, CHILLS, and HILLGA generation simultaneously. That flexibility allows developers to phase their interconnection strategy, securing some firm capacity while using non-firm bridge arrangements to come online faster, then transitioning toward firmness as transmission upgrades are completed. The 90-day HILLGA study timeline directly addresses the speed-to-power constraint that has driven many projects toward BTM approaches. Critically, however, SPP does not offer a pathway that is equivalent to the NCBL process in PJM.

For data center developers seeking rapid grid access, BTM thermal generation is an understandable near-term solution. When speed to market is the primary consideration, BTM gas can get a facility online quickly and serve as a reliable stopgap until a grid connection is established.

It is an expensive proposition, though. As illustrated in Figure 2, the LCOE for BTM natural gas generation exceeds ERCOT’s projected ATC forward price across every thermal configuration, in many cases by a wide margin. An industrial combustion turbine (CT) running at high capacity-factor carries an LCOE above $120 per megawatt-hour (MWh). Even a natural gas combined cycle (NGCC) plant with a 35-year asset life, which stretches far beyond the decarbonization commitments most hyperscalers have made, still prices above ERCOT’s grid cost forecast.

BTM storage, however, offers multiple advantages. In non-curtailment hours, which make up the vast majority of any given year, the load can take grid power. However, BTM storage can participate in critical peak reduction programs in different ISOs to reduce transmission cost allocation, provide ancillary services, and execute energy arbitrage. Additionally, while ISOs may assign limited accreditation value to duration-limited resources due to concerns over performance during tail events, BTM storage can effectively receive 100% accreditation by reducing on-site peak demand during “critical peak” events that can be relatively easy to predict in certain markets.

The full webinar recording offers additional insights related to large load interconnection reform across PJM, ERCOT, and SPP, flexible interconnection design, and transmission modeling for data center and power project siting.

Trusted across hundreds of deals and more than $1 billion in transaction value, PowerVAL provides bankable revenue forecasts and nodal-specific valuations for storage, renewables, and hybrid projects under multiple operating strategies across all ISOs. Please contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)