Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

When ERCOT's Real-Time Co-Optimization plus Batteries (RTC+B) market redesign went live on December 5, 2025, it fundamentally changed how energy storage resources bid into the market and are dispatched. Now that months of post-implementation operating data are available, it is clear that RTC+B worked as intended. It is also clear that some battery energy storage system (BESS) operators are thriving under the new rules, while others are still navigating the learning curve. This raises an important question: what are 'winners' under RTC+B doing differently, and what lessons can be learned from them?

In a recent webinar, Mike Huisenga, Managing Director of Bid Optimization at Ascend Analytics, and Martin Chown, Senior Energy Analyst, discussed the impact of RTC+B, analyzed post-implementation market data, and identified clear lessons for BESS owners and operators in ERCOT.

RTC+B encompasses three interconnected rule changes that together reshape how every battery in ERCOT is modeled, dispatched, and settled. Real-time co-optimization integrated AS awards directly into the Security-Constrained Economic Dispatch (SCED) engine, replacing the legacy Operating Reserve Demand Curve (ORDC) with Ancillary Service Demand Curves (ASDCs). Energy and AS offers are now co-optimized in every 5-minute SCED interval, with real-time AS prices and awards generated simultaneously with Locational Marginal Prices (LMPs).

ERCOT also moved energy storage resources from a combo model, in which batteries were treated as separate charging and discharging assets, to a single, unified representation in ERCOT's core systems, with one set of telemetry, one bid/offer curve, and one settlement structure. New state-of-charge rules introduced explicit MWh accounting into Reliability Unit Commitment and SCED, so that SOC constraints now directly shape both energy and AS awards.

Taken together, these rules require bidding strategies to update dynamically with every SCED run. In practice, this means that ERCOT BESS operators now have a second chance to optimize AS participation in real-time, but only if they have the tools to take advantage of it.

Hub energy prices were essentially undisturbed by the transition, with tight day-ahead to real-time price parity staying mostly steady, outside of Winter Storm Fern in late January 2026.

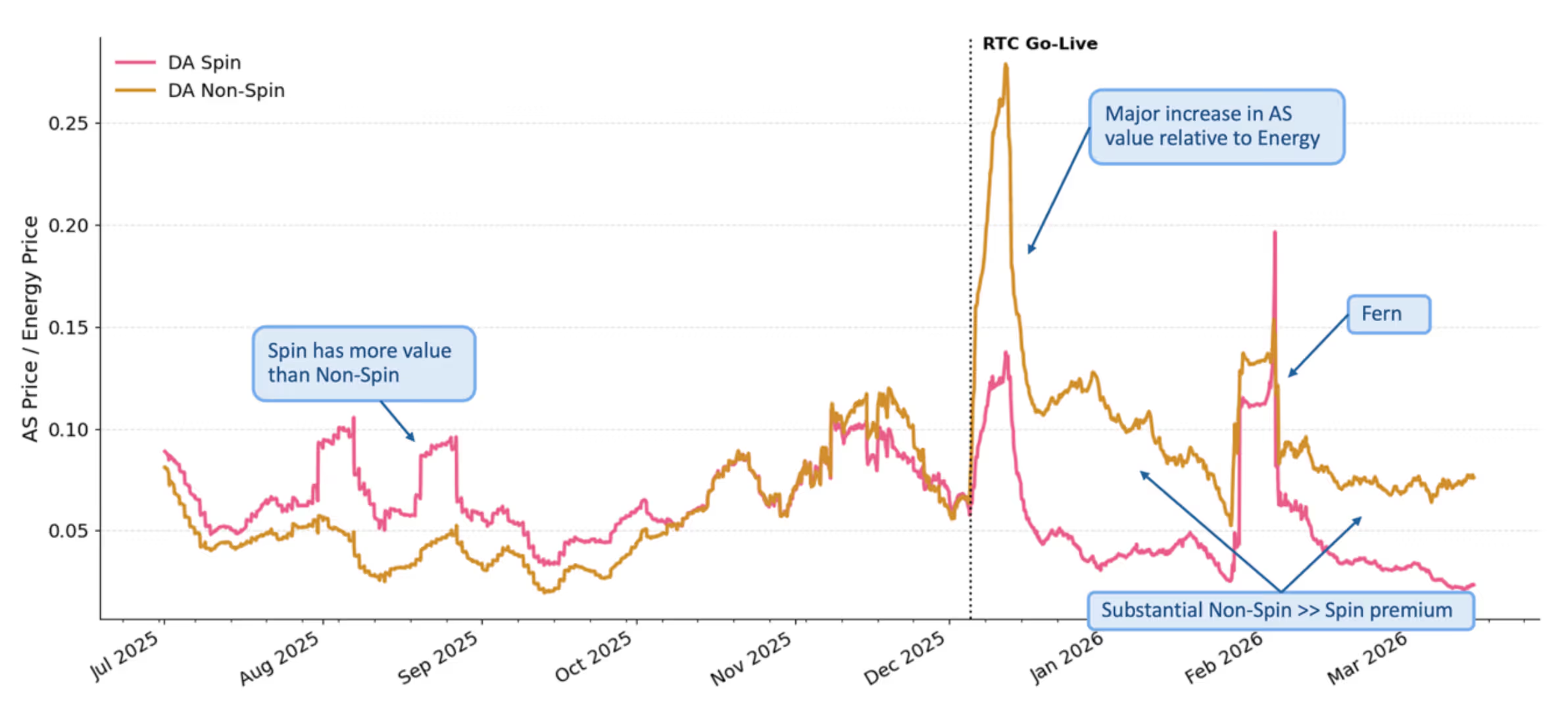

With ancillary services, however, DA prices surged immediately after the December 5 go-live, with the AS-to-energy price ratio spiking sharply before gradually returning to more typical levels, as shown in Figure 1. This surge was not driven primarily by increased AS procurement volumes, but rather reflected a rapid tightening of the Non-Spin supply stack as participants rationalized the increased state of charge (SOC) duration requirements.

Two structural pricing shifts are underway since the transition. First, the DA premium over RT AS prices is eroding. Initially, DA ancillary prices carried a substantial premium over RT prices; that gap is narrowing as the market matures. Second, Non-Spin now commands a persistent premium over Spin, with ECRS falling in between. State-of-charge duration requirements mean that products requiring less SOC commitment carry higher clearing prices, creating a durable price hierarchy – Non-Spin, then ECRS, then Spin – that ERCOT BESS operators need to account for explicitly in their product prioritization.

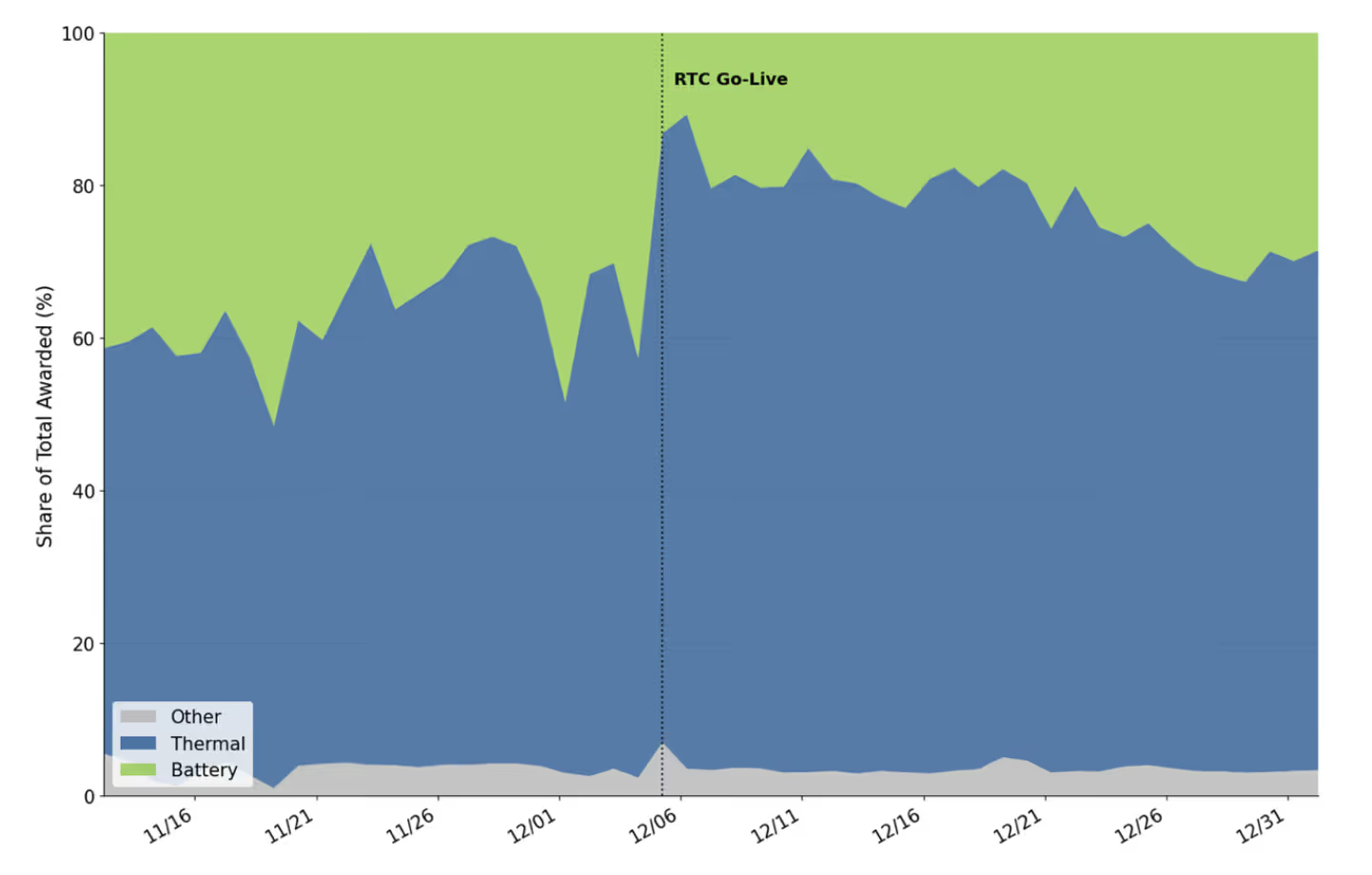

The first weeks after go-live revealed an asymmetry in how quickly different resource types adapted. As shown in Figure 2, thermal generators responded almost immediately to elevated DA AS prices on December 5 with a significant number of Non-Spin offers the next day. Battery operators, by contrast, did not meaningfully increase DA Non-Spin participation until December 21.

The result was that thermal assets captured the majority of the early AS value premium while many battery operators were still adjusting. It was clear that storage operators needed faster feedback loops between observed price signals and offer strategy updates.

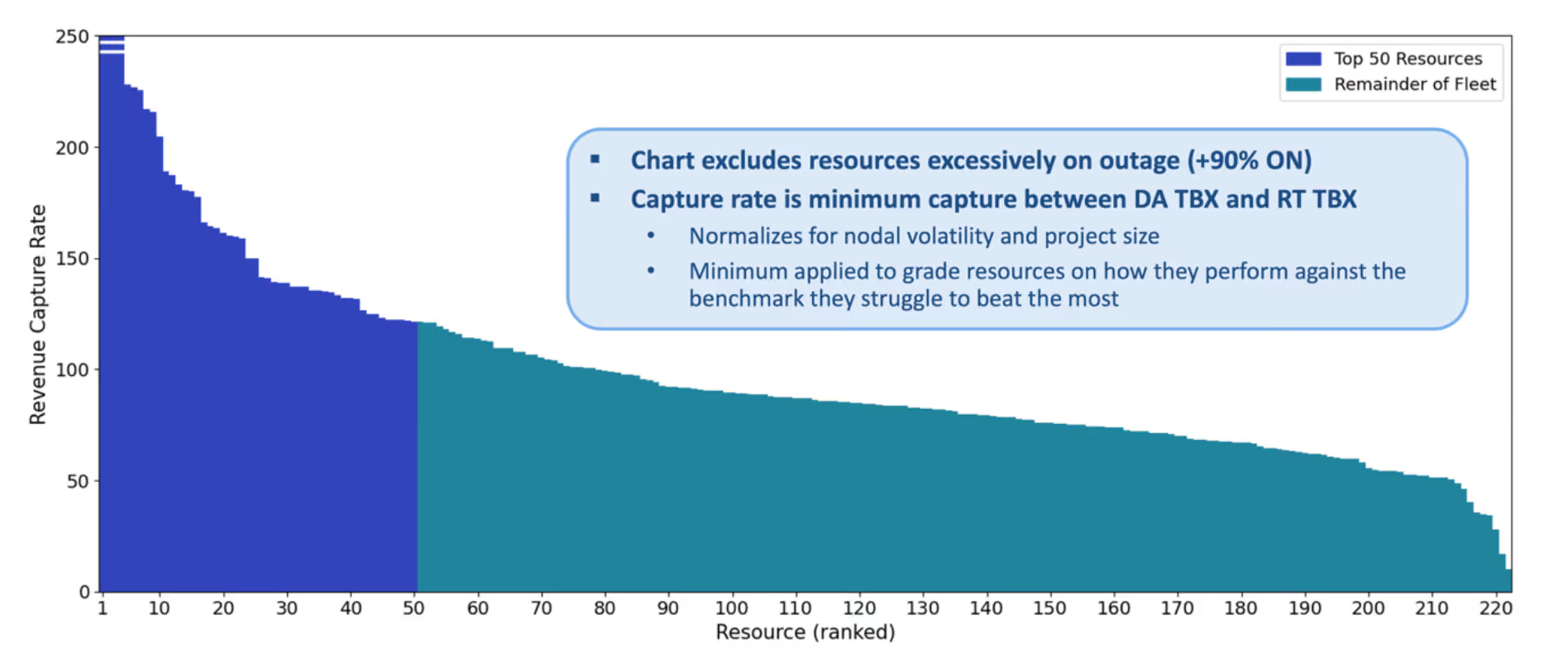

Of approximately 250 batteries operating in ERCOT since RTC+B went live, Ascend’s analysis of settlement and participation data identified around 50 assets consistently beating both day-ahead and real-time TBX benchmarks, as shown in Figure 3. These top performers span all four ERCOT hubs, range from 10 to 200 MW, and represent a variety of owners and optimizers. Thus, the performance gap is not primarily a function of asset size or location, and is instead a function of strategy, risk tolerance, and sophistication.

Here are lessons learned thus far from observing top-performing BESS assets in ERCOT after RTC+B went live:

Post-RTC+B, it is clear that the market is rewarding complexity and penalizing passivity. Operators who remain anchored to pre-RTC+B bidding strategies, such as heavy RT-only AS participation, minimal DA commitments, and static hourly schedules, are leaving significant revenue on the table.

The DA-RT AS price premium that characterized the early post-go-live period will continue to erode as the market matures. The operators who will be best positioned as that window narrows are those who have built genuinely dynamic, interval-by-interval optimization capabilities: adjusting DA offer strategies quickly in response to strong price signals, actively managing real-time positions relative to DA awards, and continuously repricing the relative value of ancillary products in light of SOC constraints.

SmartBidder™ uniquely provides a unified platform for custom bid and offer optimization combined with scheduling services to manage asset performance and operations for storage, renewable, and hybrid assets. SmartBidder maximizes revenue and reduces risk, offering asset owners and operators a 100% increase relative to traditional arbitrage strategies, and a 10-25% improvement over similar competing platforms. The solution enables users to develop their own customized bid strategies based on nodal specific forecasts, asset specific constraints, and risk-based optimization for day-ahead and real-time bids. Contact us to learn more.

When ERCOT's Real-Time Co-Optimization plus Batteries (RTC+B) market redesign went live on December 5, 2025, it fundamentally changed how energy storage resources bid into the market and are dispatched. Now that months of post-implementation operating data are available, it is clear that RTC+B worked as intended. It is also clear that some battery energy storage system (BESS) operators are thriving under the new rules, while others are still navigating the learning curve. This raises an important question: what are 'winners' under RTC+B doing differently, and what lessons can be learned from them?

In a recent webinar, Mike Huisenga, Managing Director of Bid Optimization at Ascend Analytics, and Martin Chown, Senior Energy Analyst, discussed the impact of RTC+B, analyzed post-implementation market data, and identified clear lessons for BESS owners and operators in ERCOT.

RTC+B encompasses three interconnected rule changes that together reshape how every battery in ERCOT is modeled, dispatched, and settled. Real-time co-optimization integrated AS awards directly into the Security-Constrained Economic Dispatch (SCED) engine, replacing the legacy Operating Reserve Demand Curve (ORDC) with Ancillary Service Demand Curves (ASDCs). Energy and AS offers are now co-optimized in every 5-minute SCED interval, with real-time AS prices and awards generated simultaneously with Locational Marginal Prices (LMPs).

ERCOT also moved energy storage resources from a combo model, in which batteries were treated as separate charging and discharging assets, to a single, unified representation in ERCOT's core systems, with one set of telemetry, one bid/offer curve, and one settlement structure. New state-of-charge rules introduced explicit MWh accounting into Reliability Unit Commitment and SCED, so that SOC constraints now directly shape both energy and AS awards.

Taken together, these rules require bidding strategies to update dynamically with every SCED run. In practice, this means that ERCOT BESS operators now have a second chance to optimize AS participation in real-time, but only if they have the tools to take advantage of it.

Hub energy prices were essentially undisturbed by the transition, with tight day-ahead to real-time price parity staying mostly steady, outside of Winter Storm Fern in late January 2026.

With ancillary services, however, DA prices surged immediately after the December 5 go-live, with the AS-to-energy price ratio spiking sharply before gradually returning to more typical levels, as shown in Figure 1. This surge was not driven primarily by increased AS procurement volumes, but rather reflected a rapid tightening of the Non-Spin supply stack as participants rationalized the increased state of charge (SOC) duration requirements.

Two structural pricing shifts are underway since the transition. First, the DA premium over RT AS prices is eroding. Initially, DA ancillary prices carried a substantial premium over RT prices; that gap is narrowing as the market matures. Second, Non-Spin now commands a persistent premium over Spin, with ECRS falling in between. State-of-charge duration requirements mean that products requiring less SOC commitment carry higher clearing prices, creating a durable price hierarchy – Non-Spin, then ECRS, then Spin – that ERCOT BESS operators need to account for explicitly in their product prioritization.

The first weeks after go-live revealed an asymmetry in how quickly different resource types adapted. As shown in Figure 2, thermal generators responded almost immediately to elevated DA AS prices on December 5 with a significant number of Non-Spin offers the next day. Battery operators, by contrast, did not meaningfully increase DA Non-Spin participation until December 21.

The result was that thermal assets captured the majority of the early AS value premium while many battery operators were still adjusting. It was clear that storage operators needed faster feedback loops between observed price signals and offer strategy updates.

Of approximately 250 batteries operating in ERCOT since RTC+B went live, Ascend’s analysis of settlement and participation data identified around 50 assets consistently beating both day-ahead and real-time TBX benchmarks, as shown in Figure 3. These top performers span all four ERCOT hubs, range from 10 to 200 MW, and represent a variety of owners and optimizers. Thus, the performance gap is not primarily a function of asset size or location, and is instead a function of strategy, risk tolerance, and sophistication.

Here are lessons learned thus far from observing top-performing BESS assets in ERCOT after RTC+B went live:

Post-RTC+B, it is clear that the market is rewarding complexity and penalizing passivity. Operators who remain anchored to pre-RTC+B bidding strategies, such as heavy RT-only AS participation, minimal DA commitments, and static hourly schedules, are leaving significant revenue on the table.

The DA-RT AS price premium that characterized the early post-go-live period will continue to erode as the market matures. The operators who will be best positioned as that window narrows are those who have built genuinely dynamic, interval-by-interval optimization capabilities: adjusting DA offer strategies quickly in response to strong price signals, actively managing real-time positions relative to DA awards, and continuously repricing the relative value of ancillary products in light of SOC constraints.

SmartBidder™ uniquely provides a unified platform for custom bid and offer optimization combined with scheduling services to manage asset performance and operations for storage, renewable, and hybrid assets. SmartBidder maximizes revenue and reduces risk, offering asset owners and operators a 100% increase relative to traditional arbitrage strategies, and a 10-25% improvement over similar competing platforms. The solution enables users to develop their own customized bid strategies based on nodal specific forecasts, asset specific constraints, and risk-based optimization for day-ahead and real-time bids. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)

-4-Website%20Image%20(4).avif)