Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Over the past two years, sweeping shifts in policy, load growth expectations, supply chain constraints, and geopolitical risk have combined to create deep uncertainty in U.S. power markets. For energy mergers and acquisitions (M&A), the market evolved from a 'growth-first' landscape in 2021-2022, in which platform acquisitions and large-scale portfolio transactions were fueled by low interest rates and global capital inflows, to a low-price, low-volatility environment in 2024-25, driven by higher interest rates, interconnection costs, and regional overbuilds. Meanwhile, the elimination of investment tax credits (ITC) and production tax credits (PTC) in the One Big Beautiful Bill Act (OBBBA) had pronounced impacts on solar and wind PPA prices. As the post-OBBBA dust begins to settle, however, a clearer path forward is emerging as investors reprice opportunity and adjust risk appetites.

In a recent webinar, Dr. Michael Fisher, Director of Valuation Services at Ascend Analytics, joined Rahm Orenstein, Managing Director of Ascend Energy Exchange, and Dr. Brandon Mauch, Senior Managing Director of Operations & Strategy, to discuss where to expect M&A activity, PPA price trends, development fees across U.S. energy markets, and more.

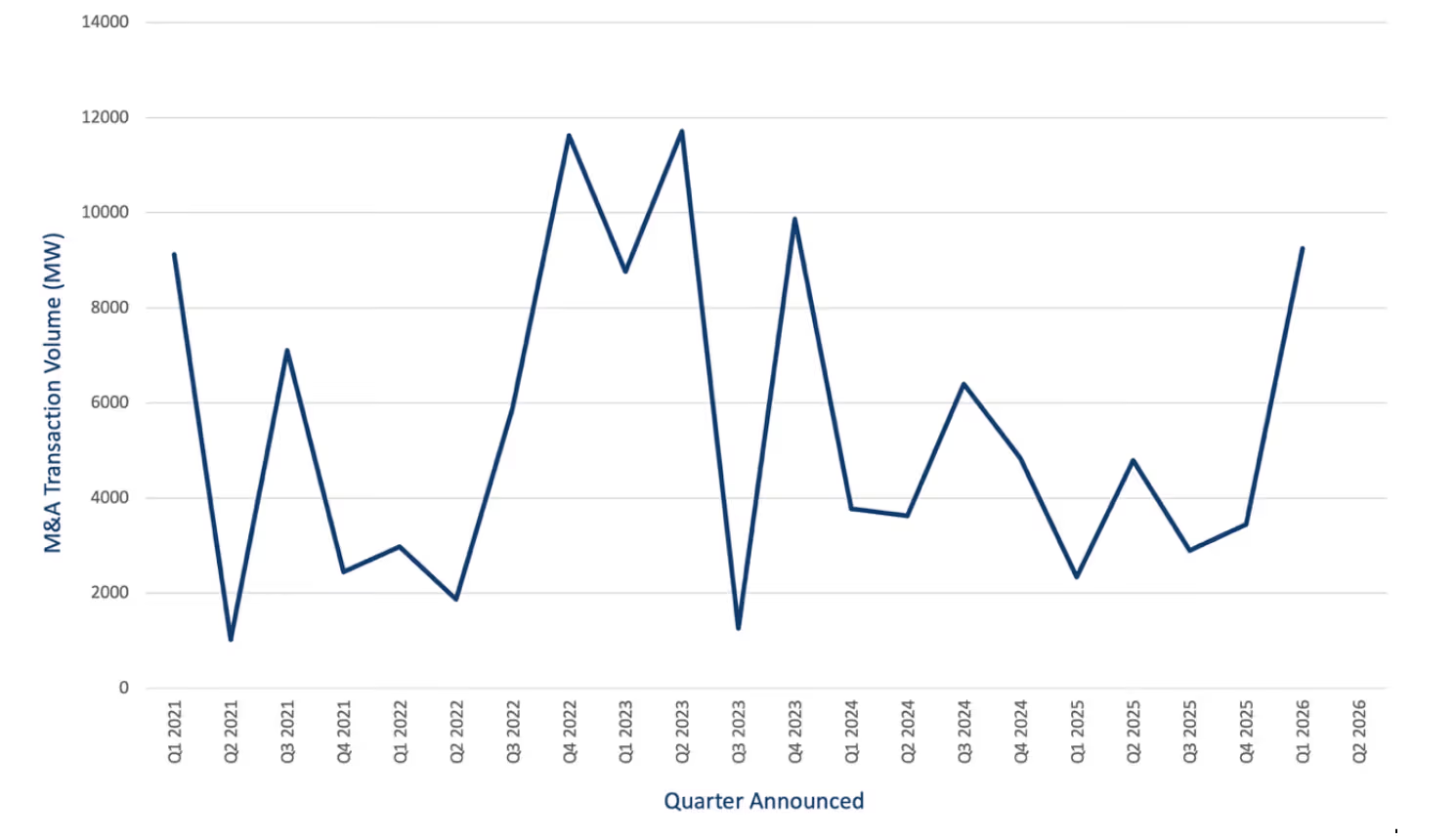

The energy M&A market appears to be recovering. Q1 2026 data tracked by Ascend shows a significant jump in BESS and hybrid asset M&A activity, as seen in Figure 1. Key drivers include greater policy clarity as the post-OBBBA dust settles, a wave of capital realignment as companies restructure portfolios, and data center-driven load growth.

Results from Ascend's own annual M&A survey, conducted across 87 different developers and independent power producers (IPPs), align with this trend. 40% of buyers and 44% of sellers expect higher volumes of transactions in 2026, with many companies that did not transact in 2025 planning to do so in 2026. Ascend's survey also noted that large portfolio sales above 500 MW have more sellers than buyers, suggesting a need to sell multiple projects at smaller deal sizes to a set of buyers.

Across asset types, battery energy storage systems (BESS) generate the highest level of buyer interest. Solar + storage hybrids and standalone solar follow closely, while wind lags behind, which likely reflects both development challenges and an unfavorable federal policy environment.

Project quality continues to be a critical consideration, and not all projects are created equal. Buyers are scrutinizing locational value, interconnection costs, permit status, FEOC exposure, tariff risks, and the path to viable offtake opportunities. Sellers, meanwhile, are absorbing higher development costs and longer timelines, creating a growing valuation gap that can be a source of friction with potential buyers. Development fee expectations also differ by market and project maturity.

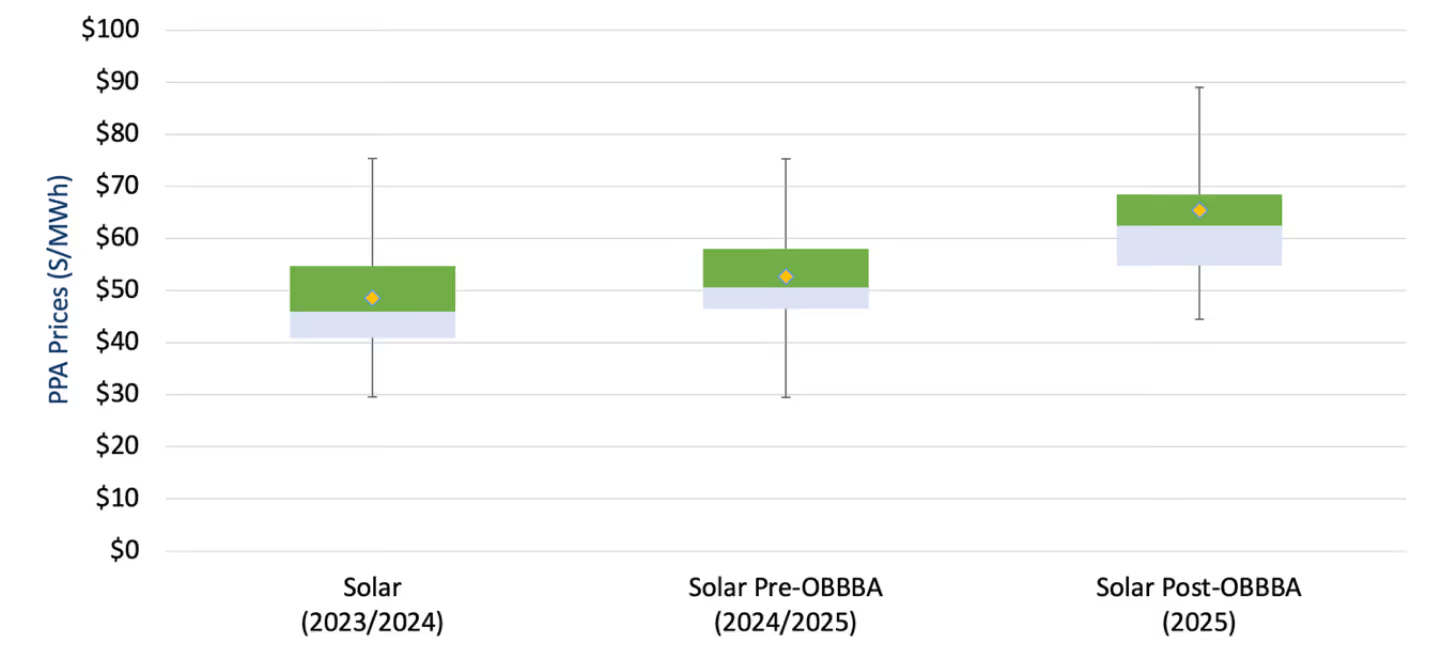

In CAISO, solar PPA prices had already climbed 13% year-over-year before the bill's passage. Post-OBBBA, prices jumped an additional 24%, driven by the accelerated tax credit phaseout timeline and persistent tariff uncertainty around equipment supply chains, as seen in Figure 2.

Pre-OBBBA, solar offers were distributed fairly evenly across 2027-2030 CODs. Post-OBBBA, nearly half of all CAISO solar bids are now clustering around 2029, which is the last year projects can still qualify for the full ITC and PTC, with near-term COD premiums reflecting the combined burden of FEOC compliance risk and tariff exposure.

The post-OBBBA effect on storage price levels appears modest. Overall, prices for standalone storage show no signs of significant change due to the OBBBA. However, levels are slightly higher in general for nearer term CODs and slightly lower in general for later CODs. Storage pricing post-OBBBA reflects the continuation of the ITC for storage resources, tempered by FEOC concerns as well as tariff uncertainties.

The Ascend Energy Exchange (AEX™) platform, an exchange for renewable and storage projects, allows buyers to receive access to carefully vetted assets and portfolios, supported by Ascend's full suite of market-level and project-level valuation, risk assessment, and unique off-take/hedge solutions.

Ascend Power Procurement (APP™) enables energy buyers to meet climate and reliability goals by conducting automated and highly competitive power procurement processes, totaling more than the U.S. data center load each year. Designed for utilities, community choice aggregators, and corporate renewable energy buyers, APP facilitates the process of executing PPAs by providing an RFP hosting service, shortening the processing time of bids, and evaluating offers with advanced modeling tools and analytics to capture project risks and true economic value. Contact us to learn more.

Over the past two years, sweeping shifts in policy, load growth expectations, supply chain constraints, and geopolitical risk have combined to create deep uncertainty in U.S. power markets. For energy mergers and acquisitions (M&A), the market evolved from a 'growth-first' landscape in 2021-2022, in which platform acquisitions and large-scale portfolio transactions were fueled by low interest rates and global capital inflows, to a low-price, low-volatility environment in 2024-25, driven by higher interest rates, interconnection costs, and regional overbuilds. Meanwhile, the elimination of investment tax credits (ITC) and production tax credits (PTC) in the One Big Beautiful Bill Act (OBBBA) had pronounced impacts on solar and wind PPA prices. As the post-OBBBA dust begins to settle, however, a clearer path forward is emerging as investors reprice opportunity and adjust risk appetites.

In a recent webinar, Dr. Michael Fisher, Director of Valuation Services at Ascend Analytics, joined Rahm Orenstein, Managing Director of Ascend Energy Exchange, and Dr. Brandon Mauch, Senior Managing Director of Operations & Strategy, to discuss where to expect M&A activity, PPA price trends, development fees across U.S. energy markets, and more.

The energy M&A market appears to be recovering. Q1 2026 data tracked by Ascend shows a significant jump in BESS and hybrid asset M&A activity, as seen in Figure 1. Key drivers include greater policy clarity as the post-OBBBA dust settles, a wave of capital realignment as companies restructure portfolios, and data center-driven load growth.

Results from Ascend's own annual M&A survey, conducted across 87 different developers and independent power producers (IPPs), align with this trend. 40% of buyers and 44% of sellers expect higher volumes of transactions in 2026, with many companies that did not transact in 2025 planning to do so in 2026. Ascend's survey also noted that large portfolio sales above 500 MW have more sellers than buyers, suggesting a need to sell multiple projects at smaller deal sizes to a set of buyers.

Across asset types, battery energy storage systems (BESS) generate the highest level of buyer interest. Solar + storage hybrids and standalone solar follow closely, while wind lags behind, which likely reflects both development challenges and an unfavorable federal policy environment.

Project quality continues to be a critical consideration, and not all projects are created equal. Buyers are scrutinizing locational value, interconnection costs, permit status, FEOC exposure, tariff risks, and the path to viable offtake opportunities. Sellers, meanwhile, are absorbing higher development costs and longer timelines, creating a growing valuation gap that can be a source of friction with potential buyers. Development fee expectations also differ by market and project maturity.

In CAISO, solar PPA prices had already climbed 13% year-over-year before the bill's passage. Post-OBBBA, prices jumped an additional 24%, driven by the accelerated tax credit phaseout timeline and persistent tariff uncertainty around equipment supply chains, as seen in Figure 2.

Pre-OBBBA, solar offers were distributed fairly evenly across 2027-2030 CODs. Post-OBBBA, nearly half of all CAISO solar bids are now clustering around 2029, which is the last year projects can still qualify for the full ITC and PTC, with near-term COD premiums reflecting the combined burden of FEOC compliance risk and tariff exposure.

The post-OBBBA effect on storage price levels appears modest. Overall, prices for standalone storage show no signs of significant change due to the OBBBA. However, levels are slightly higher in general for nearer term CODs and slightly lower in general for later CODs. Storage pricing post-OBBBA reflects the continuation of the ITC for storage resources, tempered by FEOC concerns as well as tariff uncertainties.

The Ascend Energy Exchange (AEX™) platform, an exchange for renewable and storage projects, allows buyers to receive access to carefully vetted assets and portfolios, supported by Ascend's full suite of market-level and project-level valuation, risk assessment, and unique off-take/hedge solutions.

Ascend Power Procurement (APP™) enables energy buyers to meet climate and reliability goals by conducting automated and highly competitive power procurement processes, totaling more than the U.S. data center load each year. Designed for utilities, community choice aggregators, and corporate renewable energy buyers, APP facilitates the process of executing PPAs by providing an RFP hosting service, shortening the processing time of bids, and evaluating offers with advanced modeling tools and analytics to capture project risks and true economic value. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)

-4-Website%20Image%20(4).avif)