Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

As U.S. power market stakeholders grapple with the effects of increasing renewable penetration, soaring load growth, skyrocketing capacity market prices, and evolving reliability risks, hedging has become a central tool for managing risk and stabilizing returns. Effective hedging in modern energy markets requires the use of sophisticated analytics software solutions that can help align financial strategies with physical asset behavior, market structure, and a range of future outcomes.

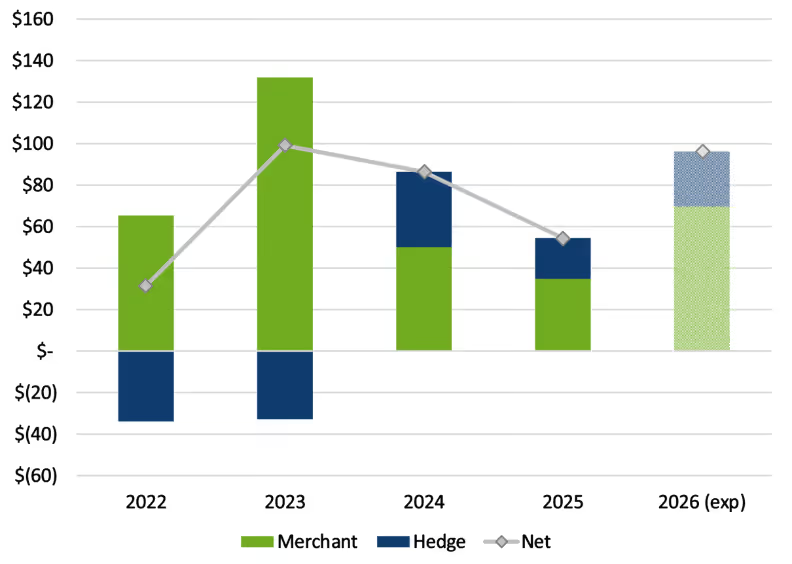

At its core, hedging is about reducing cash flow volatility while preserving upside where possible, as illustrated in Figure 1. For generators, this means ensuring revenue stability over time, both operationally and in terms of facilitating project finance. For load-serving entities (LSEs), hedging can control cost variability in the face of volatile spot prices. For IPPs and developers, hedging can preserve the ability to service debt while retaining as much merchant upside as possible.

Forward market hedging allows both generators and load-serving entities to smooth irregular scarcity conditions into average expected values, transforming a boom-and-bust revenue environment into one that is more predictable and bankable. In so doing, it supports project finance, improves bankability, and enables more confident long-term planning.

Fundamentally, hedging involves optimizing the tradeoff between risk and reward – not just eliminating risk. Overhedging can suppress upside or lead to systematically overpaying for protection, while underhedging can expose portfolios to unacceptable downside risk.

Several structural shifts in power markets are increasing both the need for and the complexity of hedging. These including the following:

These dynamics mean that traditional, static hedging approaches are often insufficient. Instead, market participants must adopt dynamic, analytics-driven strategies that reflect evolving risk profiles.

Hedge optimization requires balancing risk and reward based on an organization’s specific objectives: there is no one-size-fits-all strategy.

The optimal blend of financial and physical hedges depends on the characteristics of the specific market in which an asset operates. The most robust strategies layer financial instruments on top of physical assets, using each to address the limitations of the other. Key considerations include the following:

It is important to note that two hedge structures may offer similar average returns, but the uncertainty around those returns can differ substantially. Thus, using cash flow analysis with uncertainty bands is a valuable tool for benchmarking hedge performance across instrument types.

Successful hedging programs share several characteristics that distinguish them from more reactive or ad hoc approaches. These include:

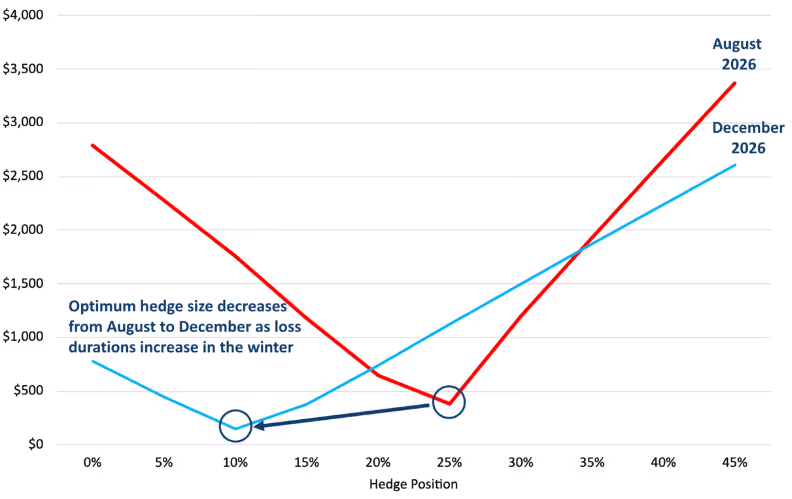

Hedge sizing is one of the most consequential decisions an asset owner or operator can make. Because hedge risks vary by year, season, and hour, finding the 'right' hedge requires the use of a rigorous, data-driven process. Key steps in that process include:

By combining assets with different production profiles, market exposures, or geographic locations, portfolios can naturally smooth variability. This approach effectively creates a structural hedge, reducing reliance on financial instruments and improving resilience to market shocks. Key dimensions of diversification include:

Formal governance frameworks are crucial components for successful hedging. They improve decision quality, provide accountability, ensure transparency, and allow reporting at any level of management. Best practices include the following:

Once hedging strategies have been developed, and governance guardrails are in place, hedge execution is the next step. Best practices for disciplined hedging programs include the following:

The Ascend PowerSIMM™ suite is an energy analytics platform that captures the new and evolving dynamics of electricity markets. Utilities, public power entities, renewable developers, and community choice aggregators utilize PowerSIMM for optimal energy portfolio management, risk management, resource planning, and project optimization. Contact us to learn more.

As U.S. power market stakeholders grapple with the effects of increasing renewable penetration, soaring load growth, skyrocketing capacity market prices, and evolving reliability risks, hedging has become a central tool for managing risk and stabilizing returns. Effective hedging in modern energy markets requires the use of sophisticated analytics software solutions that can help align financial strategies with physical asset behavior, market structure, and a range of future outcomes.

At its core, hedging is about reducing cash flow volatility while preserving upside where possible, as illustrated in Figure 1. For generators, this means ensuring revenue stability over time, both operationally and in terms of facilitating project finance. For load-serving entities (LSEs), hedging can control cost variability in the face of volatile spot prices. For IPPs and developers, hedging can preserve the ability to service debt while retaining as much merchant upside as possible.

Forward market hedging allows both generators and load-serving entities to smooth irregular scarcity conditions into average expected values, transforming a boom-and-bust revenue environment into one that is more predictable and bankable. In so doing, it supports project finance, improves bankability, and enables more confident long-term planning.

Fundamentally, hedging involves optimizing the tradeoff between risk and reward – not just eliminating risk. Overhedging can suppress upside or lead to systematically overpaying for protection, while underhedging can expose portfolios to unacceptable downside risk.

Several structural shifts in power markets are increasing both the need for and the complexity of hedging. These including the following:

These dynamics mean that traditional, static hedging approaches are often insufficient. Instead, market participants must adopt dynamic, analytics-driven strategies that reflect evolving risk profiles.

Hedge optimization requires balancing risk and reward based on an organization’s specific objectives: there is no one-size-fits-all strategy.

The optimal blend of financial and physical hedges depends on the characteristics of the specific market in which an asset operates. The most robust strategies layer financial instruments on top of physical assets, using each to address the limitations of the other. Key considerations include the following:

It is important to note that two hedge structures may offer similar average returns, but the uncertainty around those returns can differ substantially. Thus, using cash flow analysis with uncertainty bands is a valuable tool for benchmarking hedge performance across instrument types.

Successful hedging programs share several characteristics that distinguish them from more reactive or ad hoc approaches. These include:

Hedge sizing is one of the most consequential decisions an asset owner or operator can make. Because hedge risks vary by year, season, and hour, finding the 'right' hedge requires the use of a rigorous, data-driven process. Key steps in that process include:

By combining assets with different production profiles, market exposures, or geographic locations, portfolios can naturally smooth variability. This approach effectively creates a structural hedge, reducing reliance on financial instruments and improving resilience to market shocks. Key dimensions of diversification include:

Formal governance frameworks are crucial components for successful hedging. They improve decision quality, provide accountability, ensure transparency, and allow reporting at any level of management. Best practices include the following:

Once hedging strategies have been developed, and governance guardrails are in place, hedge execution is the next step. Best practices for disciplined hedging programs include the following:

The Ascend PowerSIMM™ suite is an energy analytics platform that captures the new and evolving dynamics of electricity markets. Utilities, public power entities, renewable developers, and community choice aggregators utilize PowerSIMM for optimal energy portfolio management, risk management, resource planning, and project optimization. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)