Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

-4-Website%20Image%20(4).avif)

Not long ago, the California Independent System Operator (CAISO) was defined by summer scarcity, extreme weather events, high gas prices, and urgent questions about how the system would maintain reliability amid thermal retirements. Today, California's power market is being reshaped by two different – and competing – dynamics: aggressive policy-driven decarbonization efforts and increasing underlying concerns about energy affordability. Understanding how policy, procurement, and market fundamentals intersect in CAISO is therefore critical for utilities, developers, and corporate buyers navigating investment risk and opportunity in California.

In a recent webinar previewing Ascend's latest CAISO energy market forecast, Dr. Brent Nelson, Managing Director of Markets and Strategy for Ascend Analytics, was joined by Robert LaFaso, Director of Forecasting and Valuation, and Connor Donovan, Market Intelligence Manager and Lead CAISO Analyst, to discuss policies, prices, and outlooks for one of the most consequential – and complex – electricity systems in the US.

California has a serious affordability problem. The state has seen a massive recent increase in energy retail rates: for example, Pacific Gas & Electric (PG&E) retail rates have nearly tripled since 2013. This dynamic has significant implications on what the pathway to decarbonization will – or will not – look like. Soaring retail rates also bring serious implications related to where new load does – or does not – locate. There exists a real risk that exceedingly high retail rates will deter new load, even data center-driven load, from going to California.

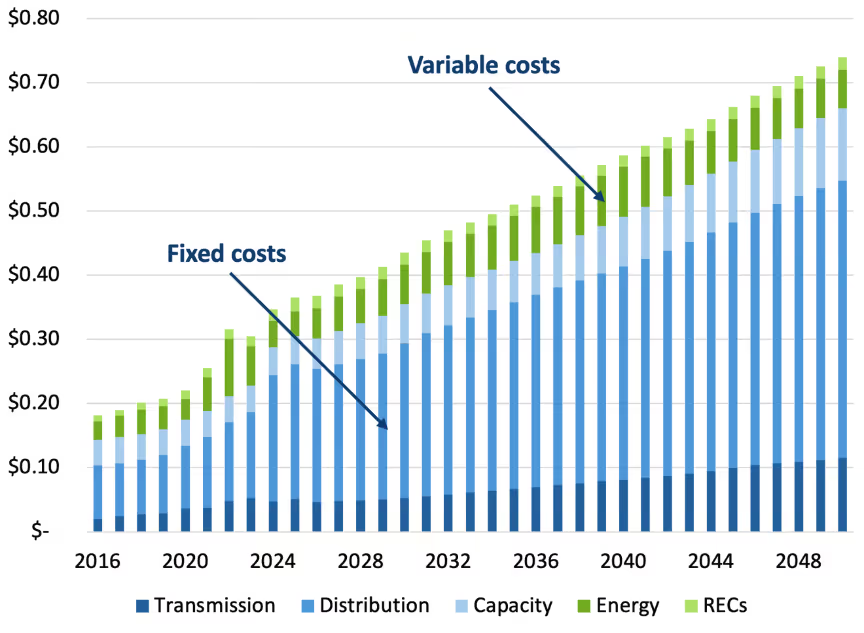

It is vital for key decision makers in California to revisit retail rate design, especially with the continued surge in behind-the-meter (BTM) energy resources. As shown in Figure 1, the vast majority of CAISO system costs are fixed, yet retail rates are largely volumetric. Retail rates can be reduced somewhat with better system utilization. However, California retail rate designs currently lack sufficient incentives to drive meaningful changes to load shapes to improve utilization.

In addition, there may well have to be changes made to existing clean energy mandates – perhaps even to SB100, which requires 100% of retail electricity sales to be zero-carbon by 2045. Even though California policymakers have yet to waver in their public commitment to decarbonization, continued energy affordability concerns might leave them with little choice.

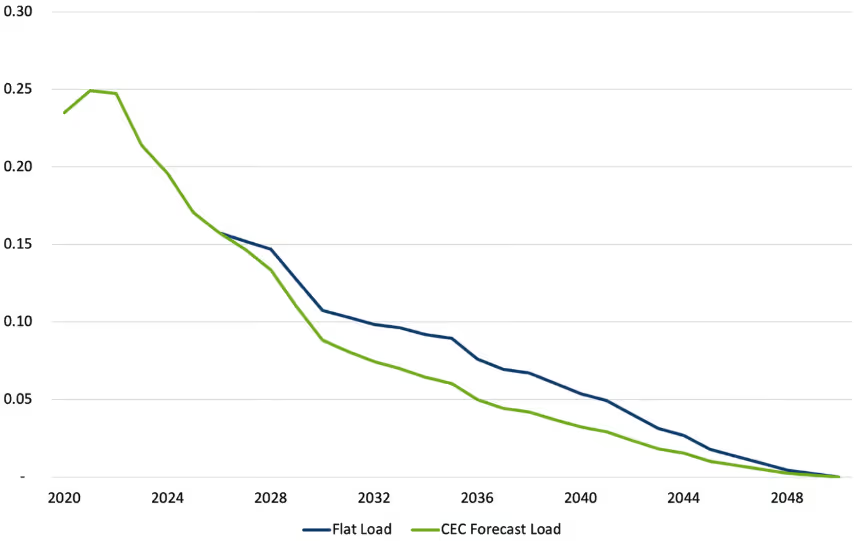

Decarbonization in California was already difficult, especially given California's complex planning dynamics and continued reliability concerns. Load growth only makes decarbonization more difficult. As shown in Figure 2, California carbon emissions mandates are measured in absolute numbers: they are based on reductions from a concrete, defined level – not on grid intensity. Accordingly, increasing load means that California energy must become proportionally cleaner in terms of grid carbon intensity in order to offset the increased load.

On top of that, California's Slice-of-Day (SOD) accounting framework does an inadequate job of incentivizing overnight decarbonization. As currently designed, the SOD framework does not account well for event durations or market needs that last longer than 12 hours, fails to allow vertical slicing, and has an accounting system that is decoupled from both dispatch and deliverability in the hours of SOD accounting. These dynamics lead to inefficiencies that severely hamper California's ability to decarbonize overnight hours.

Affordability challenges will also deter near-term investment in renewable fuels, which will be needed in the long term, especially during extended renewable droughts, to support full decarbonization.

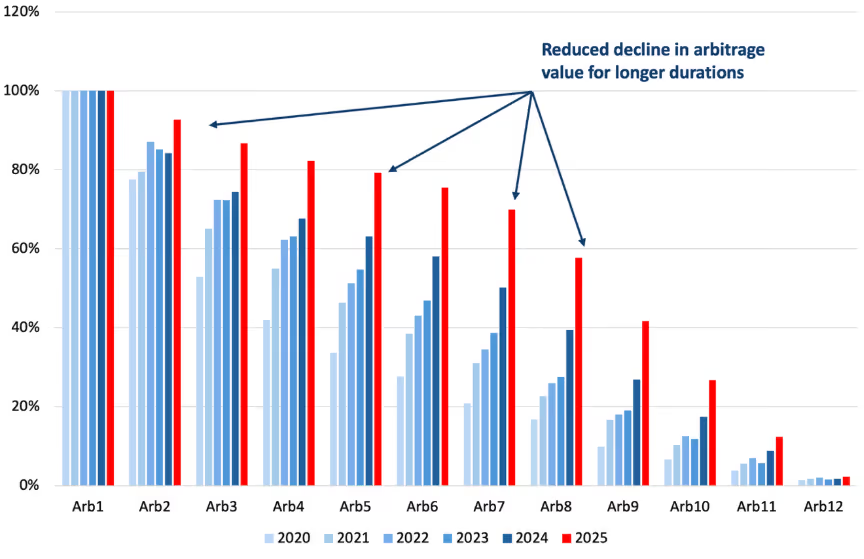

While regulatory incentives are not yet present for long-duration energy storage (LDES), market signals in support of LDES are beginning to emerge. As shown in Figure 3, arbitrage spreads are getting flatter, increasing the value proposition for added storage duration, in addition to the added value for resource adequacy. Higher gas prices also drive arbitrage spread in CAISO, and could amplify arbitrage value.

Though solar will remain a critical resource, especially as LDES becomes more prevalent, other currently undersubscribed carbon-free resources, such as wind (both offshore and on-shore), geothermal, and biomass, will be essential to providing overnight carbon-free energy.

Renewable fuels must also be eventually included in the mix to meet clean energy policy goals, but the loss of federal subsidies for hydrogen presents a near-term headwind. The removal of the hydrogen tax credit will lead to more gas generation, higher grid carbon intensity, and higher carbon costs. Ascend expects California to subsidize renewable fuels using carbon revenues, which will be key to helping California achieve the final stages of decarbonization affordably.

Access the full webinar recording, which offers additional insights related to CAISO power prices, resource mixes, carbon prices, and volatility projections, as well as opportunities for where and when to invest in energy projects in CAISO.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Not long ago, the California Independent System Operator (CAISO) was defined by summer scarcity, extreme weather events, high gas prices, and urgent questions about how the system would maintain reliability amid thermal retirements. Today, California's power market is being reshaped by two different – and competing – dynamics: aggressive policy-driven decarbonization efforts and increasing underlying concerns about energy affordability. Understanding how policy, procurement, and market fundamentals intersect in CAISO is therefore critical for utilities, developers, and corporate buyers navigating investment risk and opportunity in California.

In a recent webinar previewing Ascend's latest CAISO energy market forecast, Dr. Brent Nelson, Managing Director of Markets and Strategy for Ascend Analytics, was joined by Robert LaFaso, Director of Forecasting and Valuation, and Connor Donovan, Market Intelligence Manager and Lead CAISO Analyst, to discuss policies, prices, and outlooks for one of the most consequential – and complex – electricity systems in the US.

California has a serious affordability problem. The state has seen a massive recent increase in energy retail rates: for example, Pacific Gas & Electric (PG&E) retail rates have nearly tripled since 2013. This dynamic has significant implications on what the pathway to decarbonization will – or will not – look like. Soaring retail rates also bring serious implications related to where new load does – or does not – locate. There exists a real risk that exceedingly high retail rates will deter new load, even data center-driven load, from going to California.

It is vital for key decision makers in California to revisit retail rate design, especially with the continued surge in behind-the-meter (BTM) energy resources. As shown in Figure 1, the vast majority of CAISO system costs are fixed, yet retail rates are largely volumetric. Retail rates can be reduced somewhat with better system utilization. However, California retail rate designs currently lack sufficient incentives to drive meaningful changes to load shapes to improve utilization.

In addition, there may well have to be changes made to existing clean energy mandates – perhaps even to SB100, which requires 100% of retail electricity sales to be zero-carbon by 2045. Even though California policymakers have yet to waver in their public commitment to decarbonization, continued energy affordability concerns might leave them with little choice.

Decarbonization in California was already difficult, especially given California's complex planning dynamics and continued reliability concerns. Load growth only makes decarbonization more difficult. As shown in Figure 2, California carbon emissions mandates are measured in absolute numbers: they are based on reductions from a concrete, defined level – not on grid intensity. Accordingly, increasing load means that California energy must become proportionally cleaner in terms of grid carbon intensity in order to offset the increased load.

On top of that, California's Slice-of-Day (SOD) accounting framework does an inadequate job of incentivizing overnight decarbonization. As currently designed, the SOD framework does not account well for event durations or market needs that last longer than 12 hours, fails to allow vertical slicing, and has an accounting system that is decoupled from both dispatch and deliverability in the hours of SOD accounting. These dynamics lead to inefficiencies that severely hamper California's ability to decarbonize overnight hours.

Affordability challenges will also deter near-term investment in renewable fuels, which will be needed in the long term, especially during extended renewable droughts, to support full decarbonization.

While regulatory incentives are not yet present for long-duration energy storage (LDES), market signals in support of LDES are beginning to emerge. As shown in Figure 3, arbitrage spreads are getting flatter, increasing the value proposition for added storage duration, in addition to the added value for resource adequacy. Higher gas prices also drive arbitrage spread in CAISO, and could amplify arbitrage value.

Though solar will remain a critical resource, especially as LDES becomes more prevalent, other currently undersubscribed carbon-free resources, such as wind (both offshore and on-shore), geothermal, and biomass, will be essential to providing overnight carbon-free energy.

Renewable fuels must also be eventually included in the mix to meet clean energy policy goals, but the loss of federal subsidies for hydrogen presents a near-term headwind. The removal of the hydrogen tax credit will lead to more gas generation, higher grid carbon intensity, and higher carbon costs. Ascend expects California to subsidize renewable fuels using carbon revenues, which will be key to helping California achieve the final stages of decarbonization affordably.

Access the full webinar recording, which offers additional insights related to CAISO power prices, resource mixes, carbon prices, and volatility projections, as well as opportunities for where and when to invest in energy projects in CAISO.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)