Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

While many US power markets lack clear paths to bringing generation online quickly enough to serve sudden load growth, the Midcontinent Independent System Operator (MISO) energy market is a bit different. Because it is largely served by vertically integrated regulated utilities that can rate-base new generation, most MISO states can insulate ratepayers from the financial impacts of volatile capacity market dynamics that have driven serious affordability concerns and reform pressures in markets such as PJM. This ‘boring’ dynamic means that MISO offers one of the most stable markets in the US for new generation development – as long as developers can secure offtake deals.

In a recent webinar previewing Ascend’s latest MISO market outlook, Dr. Brent Nelson, Senior Managing Director of Markets and Strategy, and Robert LaFaso, Director of Forecasting and Valuation, discussed why MISO could serve as a model for other US power markets, the implications of regulated utility procurement for new capacity, and what the market's distinctive structure means for developers, investors, and load-serving entities (LSEs).

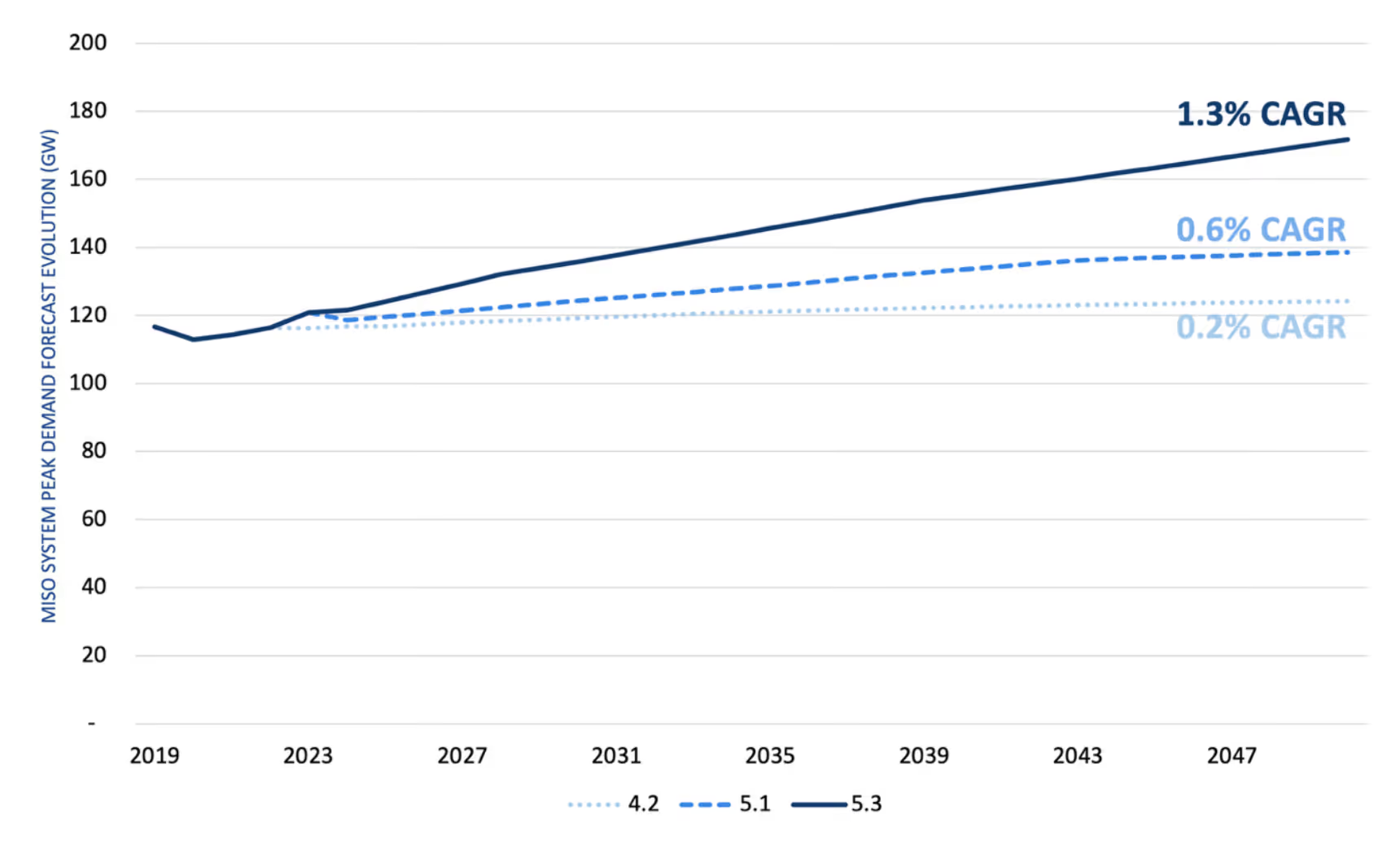

Similar to other US power markets, MISO's load growth trajectory has changed substantially in a short period of time. As shown in Figure 1, MISO has adjusted its internal peak demand forecast from an essentially flat rate of 0.2% CAGR two years ago to a current rate of 1.3% CAGR.

Data center development contributes significantly to the shift in projected peak demand. Unlike projected load growth rates in other ISOs such as ERCOT, there are valid reasons to believe that demand in MISO might actually materialize: the forecast is a much more plausible number and regulated utilities can credibly commit to bringing new generation online on timelines that support large-load interconnection requests. High-profile examples include NIPSCO's agreement to supply 3 GW to Amazon data centers in northern Indiana, as well as Meta's decision to build a $10 billion data center in northeastern Louisiana, in Entergy's service territory. As projects face capacity expansion barriers in other markets, and as GW-scale loads continue to site in MISO, development may even accelerate above and beyond what is currently forecast.

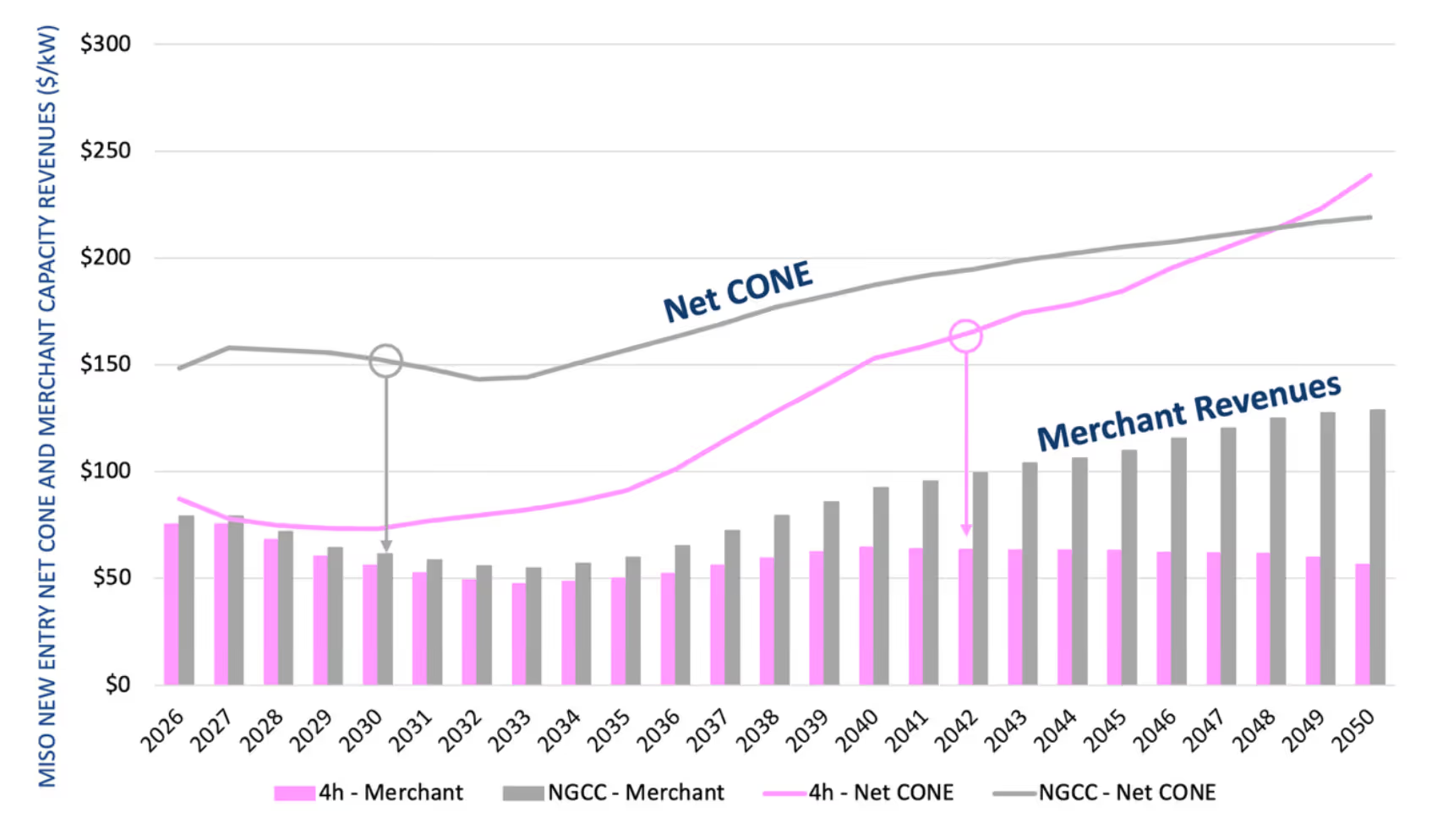

When load growth requires new entry to meet reliability obligations in capacity markets, capacity prices must rise to the net cost of new entry (Net CONE) to make a merchant investment in new supply viable. In markets such as PJM, this means that the new generator is not the only resource paid at that elevated clearing price; every generator on the supply stack receives the same price. This dynamic drives up retail rates and creates the kinds of political pressures that have made capacity market reform a persistent feature of the PJM policy landscape.

Because MISO is served primarily by vertically integrated regulated utilities that often opt out of the capacity market entirely, it largely avoids these capacity market issues. In MISO, it is expected that regulated utilities will contract with or own new generation that can be rate-based, thus allowing cost recovery to flow directly through regulated rates rather than through capacity market clearing prices. The capacity market is therefore used primarily as a true-up and as an efficient retirement signal, rather than as a device to support the bulk of capacity procurement.

For developers, this means that MISO presents fundamentally different new entry opportunities than those that exist in merchant-dominated markets. Those developers who can find a long-term tolling agreement or capacity offtake with a regulated utility will secure revenue certainty. However, as shown in Figure 2, merchant revenues alone will be insufficient to support new entry in MISO. Without offtake, new projects have little to no chance of penciling.

In states with meaningful RPS targets and vertically integrated utilities, including Michigan and Minnesota, the regulated utilities function as offtakers for both energy and RECs from renewable energy developers. For corporate buyers pursuing voluntary clean energy goals, the utility structure also enables sleeve-through arrangements, in which a regulated utility serves as an intermediary between a corporate buyer and renewable developer.

These dynamics are already present in MISO. For example, AES has structured agreements to deliver carbon-free power in support of Microsoft operations within MISO, while Google and Xcel Energy recently announced a large-scale agreement to power a Minnesota data center with clean energy. These examples illustrate the structural advantage MISO offers for clean energy developers relative to fully deregulated markets: creditworthy regulated offtakers with both the mandate and the rate-recovery mechanism to make long-term renewable energy procurement commitments viable.

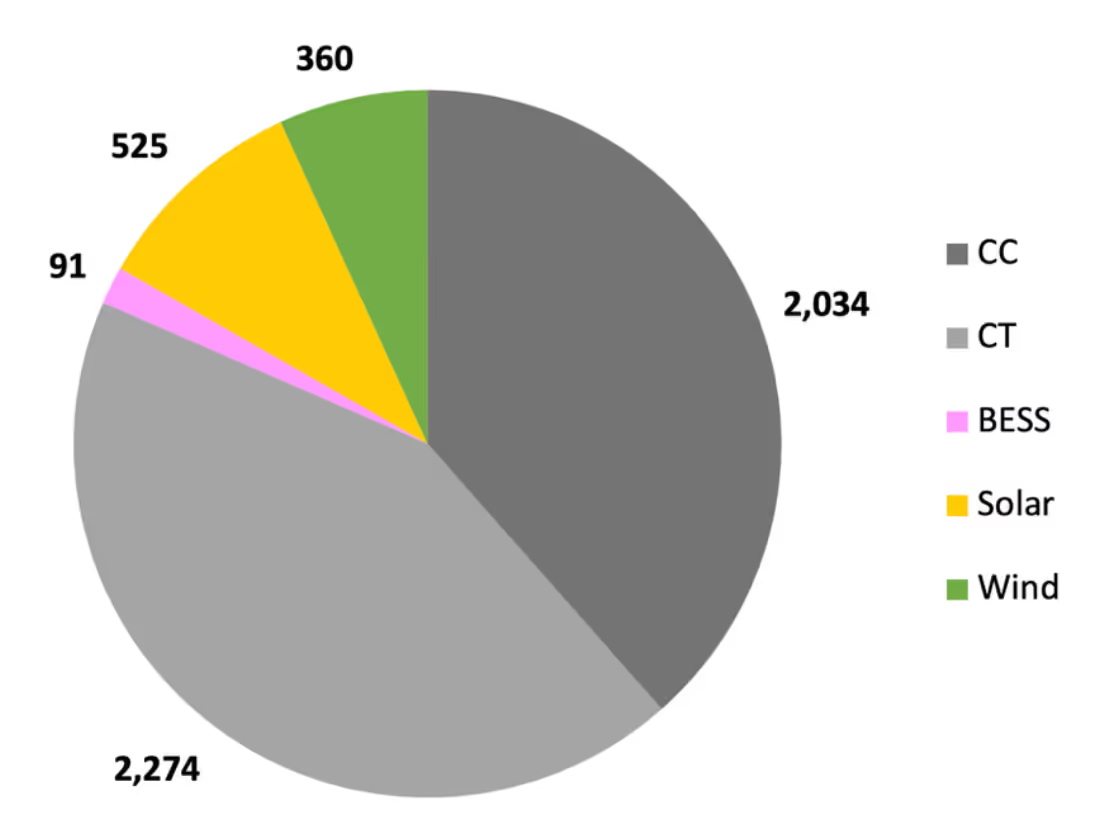

However, technology preference varies significantly throughout MISO. During the 2025 Expedited Resource Addition Study (ERAS), most MISO states without meaningful clean energy mandates demonstrated a strong preference for gas, as shown in Figure 3. Renewable energy developers pursuing offtake in those states should expect a more difficult path than in RPS-driven states.

Access the full webinar recording, which offers additional insights related to MISO’s recent market evolution, ELCC risks for developers, evolving technology costs, investment considerations by asset class, price forecasts, and more.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over 300 gigawatts and $25 billion in project assessments. Please contact us to learn more.

While many US power markets lack clear paths to bringing generation online quickly enough to serve sudden load growth, the Midcontinent Independent System Operator (MISO) energy market is a bit different. Because it is largely served by vertically integrated regulated utilities that can rate-base new generation, most MISO states can insulate ratepayers from the financial impacts of volatile capacity market dynamics that have driven serious affordability concerns and reform pressures in markets such as PJM. This ‘boring’ dynamic means that MISO offers one of the most stable markets in the US for new generation development – as long as developers can secure offtake deals.

In a recent webinar previewing Ascend’s latest MISO market outlook, Dr. Brent Nelson, Senior Managing Director of Markets and Strategy, and Robert LaFaso, Director of Forecasting and Valuation, discussed why MISO could serve as a model for other US power markets, the implications of regulated utility procurement for new capacity, and what the market's distinctive structure means for developers, investors, and load-serving entities (LSEs).

Similar to other US power markets, MISO's load growth trajectory has changed substantially in a short period of time. As shown in Figure 1, MISO has adjusted its internal peak demand forecast from an essentially flat rate of 0.2% CAGR two years ago to a current rate of 1.3% CAGR.

Data center development contributes significantly to the shift in projected peak demand. Unlike projected load growth rates in other ISOs such as ERCOT, there are valid reasons to believe that demand in MISO might actually materialize: the forecast is a much more plausible number and regulated utilities can credibly commit to bringing new generation online on timelines that support large-load interconnection requests. High-profile examples include NIPSCO's agreement to supply 3 GW to Amazon data centers in northern Indiana, as well as Meta's decision to build a $10 billion data center in northeastern Louisiana, in Entergy's service territory. As projects face capacity expansion barriers in other markets, and as GW-scale loads continue to site in MISO, development may even accelerate above and beyond what is currently forecast.

When load growth requires new entry to meet reliability obligations in capacity markets, capacity prices must rise to the net cost of new entry (Net CONE) to make a merchant investment in new supply viable. In markets such as PJM, this means that the new generator is not the only resource paid at that elevated clearing price; every generator on the supply stack receives the same price. This dynamic drives up retail rates and creates the kinds of political pressures that have made capacity market reform a persistent feature of the PJM policy landscape.

Because MISO is served primarily by vertically integrated regulated utilities that often opt out of the capacity market entirely, it largely avoids these capacity market issues. In MISO, it is expected that regulated utilities will contract with or own new generation that can be rate-based, thus allowing cost recovery to flow directly through regulated rates rather than through capacity market clearing prices. The capacity market is therefore used primarily as a true-up and as an efficient retirement signal, rather than as a device to support the bulk of capacity procurement.

For developers, this means that MISO presents fundamentally different new entry opportunities than those that exist in merchant-dominated markets. Those developers who can find a long-term tolling agreement or capacity offtake with a regulated utility will secure revenue certainty. However, as shown in Figure 2, merchant revenues alone will be insufficient to support new entry in MISO. Without offtake, new projects have little to no chance of penciling.

In states with meaningful RPS targets and vertically integrated utilities, including Michigan and Minnesota, the regulated utilities function as offtakers for both energy and RECs from renewable energy developers. For corporate buyers pursuing voluntary clean energy goals, the utility structure also enables sleeve-through arrangements, in which a regulated utility serves as an intermediary between a corporate buyer and renewable developer.

These dynamics are already present in MISO. For example, AES has structured agreements to deliver carbon-free power in support of Microsoft operations within MISO, while Google and Xcel Energy recently announced a large-scale agreement to power a Minnesota data center with clean energy. These examples illustrate the structural advantage MISO offers for clean energy developers relative to fully deregulated markets: creditworthy regulated offtakers with both the mandate and the rate-recovery mechanism to make long-term renewable energy procurement commitments viable.

However, technology preference varies significantly throughout MISO. During the 2025 Expedited Resource Addition Study (ERAS), most MISO states without meaningful clean energy mandates demonstrated a strong preference for gas, as shown in Figure 3. Renewable energy developers pursuing offtake in those states should expect a more difficult path than in RPS-driven states.

Access the full webinar recording, which offers additional insights related to MISO’s recent market evolution, ELCC risks for developers, evolving technology costs, investment considerations by asset class, price forecasts, and more.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over 300 gigawatts and $25 billion in project assessments. Please contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

-4-Website%20Image%20(4).avif)