Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

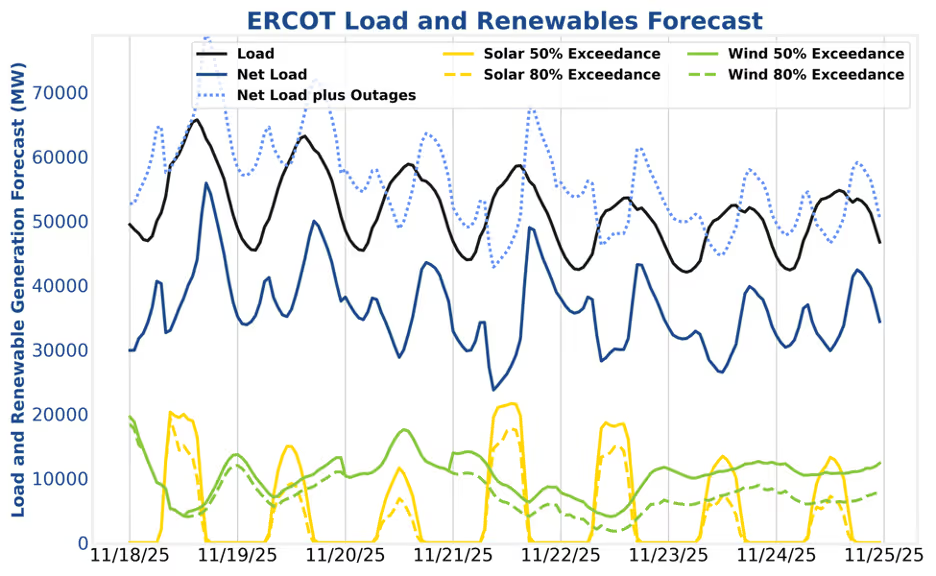

In ERCOT, non-spin and energy discharge is the name of the game on the 7th as higher net load (plus outages) levels will present profitable HE18 opportunities.

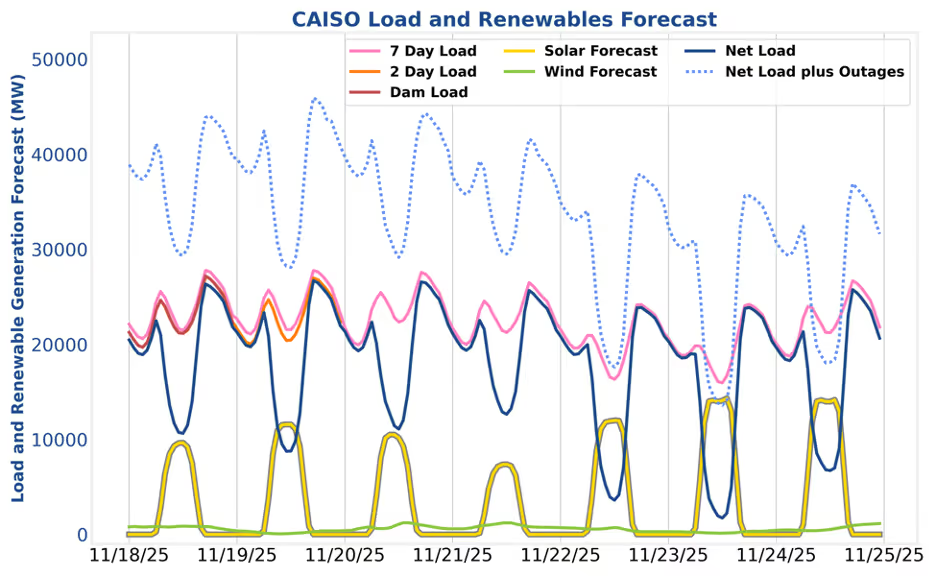

In CAISO, renewable production and temperature will fluctuate throughout the state. Operators should begin paying attention to morning peaks and consider midnight SoC adjustments for day-ahead optimization.

High temperatures are expected to ease this week, steadily reducing gross load levels across the system. Solar output may fluctuate significantly day-to-day while wind production is forecast to remain more stable than usual.

Looking ahead, the evening of the 21st stands out as a period when elevated net load could create opportunities for energy participation. Otherwise, operators should maintain standard low-volatility strategies and prioritize preparation for RTC+B. If you were unable to attend Ascend’s RTC+B webinar last week, please contact your analyst to request a link to the recording.

Last week, ERCOT delivered one of the most straightforward charts we’ve featured in this newsletter. Net load climbed steadily throughout the week, peaking at 53 GW on November 16th when renewable production dropped roughly 10 GW below any other day of the week. Both day-ahead and real-time prices rose in tandem with net load, and with positive average DART spreads each day, the day-ahead market was the clear winner.

SmartBidder’s Mt. Blue Sky strategy performed best as it bid opportunistically in the day-ahead market to capture the majority of revenues while reserving some SoC for real-time price spikes. Although none materialized this week, the asymmetric upside of discharging into a real-time spike justifies reserving SoC, even if it results in slightly lower discharge prices when spikes fail to materialize.

Adding to an already volatility-starved year, California has now been hit with a streak of cloud cover, and with it the disappearance of charging prices low enough to justify day-ahead arbitrage. Cloudy conditions will dominate over the next several days, with the 21st expected to deliver less than 10 GW of peak solar production. Stronger output should return by the 23rd, at which point TB4 is likely to become a solid strategy once again.

In the meantime, operators stepping back from TB4 due to weak spreads should shift their focus toward real-time energy opportunities and regulation. It remains important to continue placing bids and offers that clear at price levels at which operators are comfortable charging and discharging. Even though the day-ahead market is predictably deficient under the present conditions, the beauty of the real-time market is that it will often present opportunities even when they are not expected. SmartBidder’s Mt. Shasta strategy can be tuned to perform well in these regimes.

Prices in CAISO were largely flat last week. Low solar production pushed midday prices higher, while net load came in below forecast during morning and evening peaks. The day-ahead market remained mostly within the $30–$50/MWh range, and the brief bouts of real-time volatility offered little advantage for participating in one market over the other.

With minimal solar production on the horizon, the day-ahead market will provide the most reliable opportunities to charge at low prices, while the real-time market has more potential for high discharge prices. Lower solar output can also increase midday volatility, making it especially important to place bids throughout the day to capture value whenever it appears.SmartBidder’s opportunity-cost bidding framework is well-suited to this task, allowing operators to take advantage of these fleeting market opportunities.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

In ERCOT, non-spin and energy discharge is the name of the game on the 7th as higher net load (plus outages) levels will present profitable HE18 opportunities.

In CAISO, renewable production and temperature will fluctuate throughout the state. Operators should begin paying attention to morning peaks and consider midnight SoC adjustments for day-ahead optimization.

High temperatures are expected to ease this week, steadily reducing gross load levels across the system. Solar output may fluctuate significantly day-to-day while wind production is forecast to remain more stable than usual.

Looking ahead, the evening of the 21st stands out as a period when elevated net load could create opportunities for energy participation. Otherwise, operators should maintain standard low-volatility strategies and prioritize preparation for RTC+B. If you were unable to attend Ascend’s RTC+B webinar last week, please contact your analyst to request a link to the recording.

Last week, ERCOT delivered one of the most straightforward charts we’ve featured in this newsletter. Net load climbed steadily throughout the week, peaking at 53 GW on November 16th when renewable production dropped roughly 10 GW below any other day of the week. Both day-ahead and real-time prices rose in tandem with net load, and with positive average DART spreads each day, the day-ahead market was the clear winner.

SmartBidder’s Mt. Blue Sky strategy performed best as it bid opportunistically in the day-ahead market to capture the majority of revenues while reserving some SoC for real-time price spikes. Although none materialized this week, the asymmetric upside of discharging into a real-time spike justifies reserving SoC, even if it results in slightly lower discharge prices when spikes fail to materialize.

Adding to an already volatility-starved year, California has now been hit with a streak of cloud cover, and with it the disappearance of charging prices low enough to justify day-ahead arbitrage. Cloudy conditions will dominate over the next several days, with the 21st expected to deliver less than 10 GW of peak solar production. Stronger output should return by the 23rd, at which point TB4 is likely to become a solid strategy once again.

In the meantime, operators stepping back from TB4 due to weak spreads should shift their focus toward real-time energy opportunities and regulation. It remains important to continue placing bids and offers that clear at price levels at which operators are comfortable charging and discharging. Even though the day-ahead market is predictably deficient under the present conditions, the beauty of the real-time market is that it will often present opportunities even when they are not expected. SmartBidder’s Mt. Shasta strategy can be tuned to perform well in these regimes.

Prices in CAISO were largely flat last week. Low solar production pushed midday prices higher, while net load came in below forecast during morning and evening peaks. The day-ahead market remained mostly within the $30–$50/MWh range, and the brief bouts of real-time volatility offered little advantage for participating in one market over the other.

With minimal solar production on the horizon, the day-ahead market will provide the most reliable opportunities to charge at low prices, while the real-time market has more potential for high discharge prices. Lower solar output can also increase midday volatility, making it especially important to place bids throughout the day to capture value whenever it appears.SmartBidder’s opportunity-cost bidding framework is well-suited to this task, allowing operators to take advantage of these fleeting market opportunities.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)