Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

For the week of June 12th – 17th, ERCOT and CAISO will both experience middling revenue opportunities as summer energy prices stay well in check.

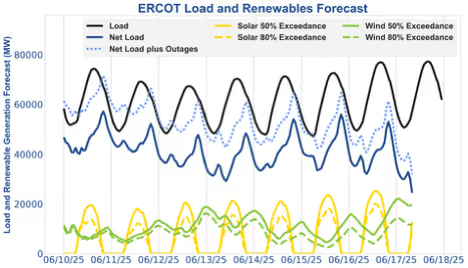

In ERCOT, Heat will show up again on the 16th and 17th next week. Currently, the strong wind forecast is expected to keep net load at manageable levels. Operators should align for evening peak discharge in a mixture of day-ahead (DA) and real-time (RT) energy, augmenting with dispatch conducive ancillary services (AS) products.

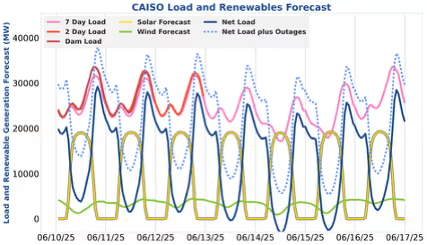

In CAISO, slightly improved arbitrage spreads from warmer weather will dissipate into the weekend as strong solar production and low gross load bring the net load peak down to below 24 GW on the 14th. Operators should continue picking up AS revenue in addition to energy arbitrage.

Wind, solar, and gross load will all fluctuate around average levels this week in ERCOT. Revenue opportunities will remain elusive, barring unforeseen congestion or major forecasting misses. While warmer weather is on the horizon beginning on the 16th, with wind production around 20 GW, temperatures will need to climb well above100 Fahrenheit to push net load up to structural reserve margin tipping points.

In terms of BESS optimization strategy, traders should target energy arbitrage while preserving upside to capture any unexpected real-time volatility through full SoC, reg-up, and non-spin throughout the day. Peak strategies should also enable assets to fully empty between HE20 and HE22, with shorter duration assets picking up more AS awards and longer duration assets leaving more room for fuller energy base points. SmartBidder’s Mt Blue Sky strategy is fully capable of dialing up hedged mixtures of DA AS and energy while targeting 0% SoC at the start of HE23 within the opportunity cost framework. Talk to your analyst about configuring custom heat wave strategies for later this summer.

In addition to some mediocre evening peak action on the 7th and 9th, the most notable day in ERCOT last week was the 5th, as Houston experienced another bout of midday congestion. Reg-up throughput was strong throughout these $1,000/MWh prices that lasted about 30 minutes. Houston area assets should evaluate their midday AS strategies as summer, congestion-induced price spikes are starting to become a pattern. On the structural volatility side of the coin, net load peaked near 60 GW on the 7th and 9th, producing prices ranging between $100/MWh and $200/MWh in the energy markets.This will be an important benchmark later this summer when heat begins to arrive in force.

Hearty wind and solar production are projected to continue to reach the grid this week, with net loads remaining fairly muted despite warming temperatures. The 14th and 15th are the only days where projected net loads are expected to be below zero. Expect a continued trend of monotone renewable curtailment, similar to what was persistent in May. Continuing to operate in a more day-ahead heavy strategy is the recommended approach.

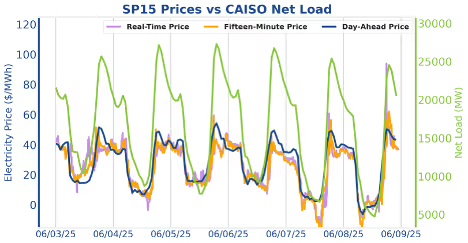

Evening peaks are the name of the game as we transition into the warmer months. Earlier in the week, day-ahead evening discharge prices consistently cleared above real-time, with real-time surpassing day-ahead only on the evenings of the 7th and 8th. Charging prices in CAISO remain mixed. While there are periods—prevalent almost daily—when real-time charging prices dip below day-ahead levels, these windows are typically fleeting given current market conditions. Only on the 7th did the lowest four real-time prices come in below the lowest four day-ahead prices. Charging in real-time energy continues to be the riskier strategy, as forecasting which hours will experience negative price spikes remains unreliable. For example, the first half of HE18 on the 6th offered the best charging prices of the day, while on the 9th, HE18 prices averaged higher than HE21. Operators relying more heavily on day-ahead energy will continue to miss out on real-time price spikes in both directions, but may opt for more consistent returns. Days like the 3rd—where real-time prices fell flat during both charging and discharging windows—have not been uncommon lately.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of June 12th – 17th, ERCOT and CAISO will both experience middling revenue opportunities as summer energy prices stay well in check.

In ERCOT, Heat will show up again on the 16th and 17th next week. Currently, the strong wind forecast is expected to keep net load at manageable levels. Operators should align for evening peak discharge in a mixture of day-ahead (DA) and real-time (RT) energy, augmenting with dispatch conducive ancillary services (AS) products.

In CAISO, slightly improved arbitrage spreads from warmer weather will dissipate into the weekend as strong solar production and low gross load bring the net load peak down to below 24 GW on the 14th. Operators should continue picking up AS revenue in addition to energy arbitrage.

Wind, solar, and gross load will all fluctuate around average levels this week in ERCOT. Revenue opportunities will remain elusive, barring unforeseen congestion or major forecasting misses. While warmer weather is on the horizon beginning on the 16th, with wind production around 20 GW, temperatures will need to climb well above100 Fahrenheit to push net load up to structural reserve margin tipping points.

In terms of BESS optimization strategy, traders should target energy arbitrage while preserving upside to capture any unexpected real-time volatility through full SoC, reg-up, and non-spin throughout the day. Peak strategies should also enable assets to fully empty between HE20 and HE22, with shorter duration assets picking up more AS awards and longer duration assets leaving more room for fuller energy base points. SmartBidder’s Mt Blue Sky strategy is fully capable of dialing up hedged mixtures of DA AS and energy while targeting 0% SoC at the start of HE23 within the opportunity cost framework. Talk to your analyst about configuring custom heat wave strategies for later this summer.

In addition to some mediocre evening peak action on the 7th and 9th, the most notable day in ERCOT last week was the 5th, as Houston experienced another bout of midday congestion. Reg-up throughput was strong throughout these $1,000/MWh prices that lasted about 30 minutes. Houston area assets should evaluate their midday AS strategies as summer, congestion-induced price spikes are starting to become a pattern. On the structural volatility side of the coin, net load peaked near 60 GW on the 7th and 9th, producing prices ranging between $100/MWh and $200/MWh in the energy markets.This will be an important benchmark later this summer when heat begins to arrive in force.

Hearty wind and solar production are projected to continue to reach the grid this week, with net loads remaining fairly muted despite warming temperatures. The 14th and 15th are the only days where projected net loads are expected to be below zero. Expect a continued trend of monotone renewable curtailment, similar to what was persistent in May. Continuing to operate in a more day-ahead heavy strategy is the recommended approach.

Evening peaks are the name of the game as we transition into the warmer months. Earlier in the week, day-ahead evening discharge prices consistently cleared above real-time, with real-time surpassing day-ahead only on the evenings of the 7th and 8th. Charging prices in CAISO remain mixed. While there are periods—prevalent almost daily—when real-time charging prices dip below day-ahead levels, these windows are typically fleeting given current market conditions. Only on the 7th did the lowest four real-time prices come in below the lowest four day-ahead prices. Charging in real-time energy continues to be the riskier strategy, as forecasting which hours will experience negative price spikes remains unreliable. For example, the first half of HE18 on the 6th offered the best charging prices of the day, while on the 9th, HE18 prices averaged higher than HE21. Operators relying more heavily on day-ahead energy will continue to miss out on real-time price spikes in both directions, but may opt for more consistent returns. Days like the 3rd—where real-time prices fell flat during both charging and discharging windows—have not been uncommon lately.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)