Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.png)

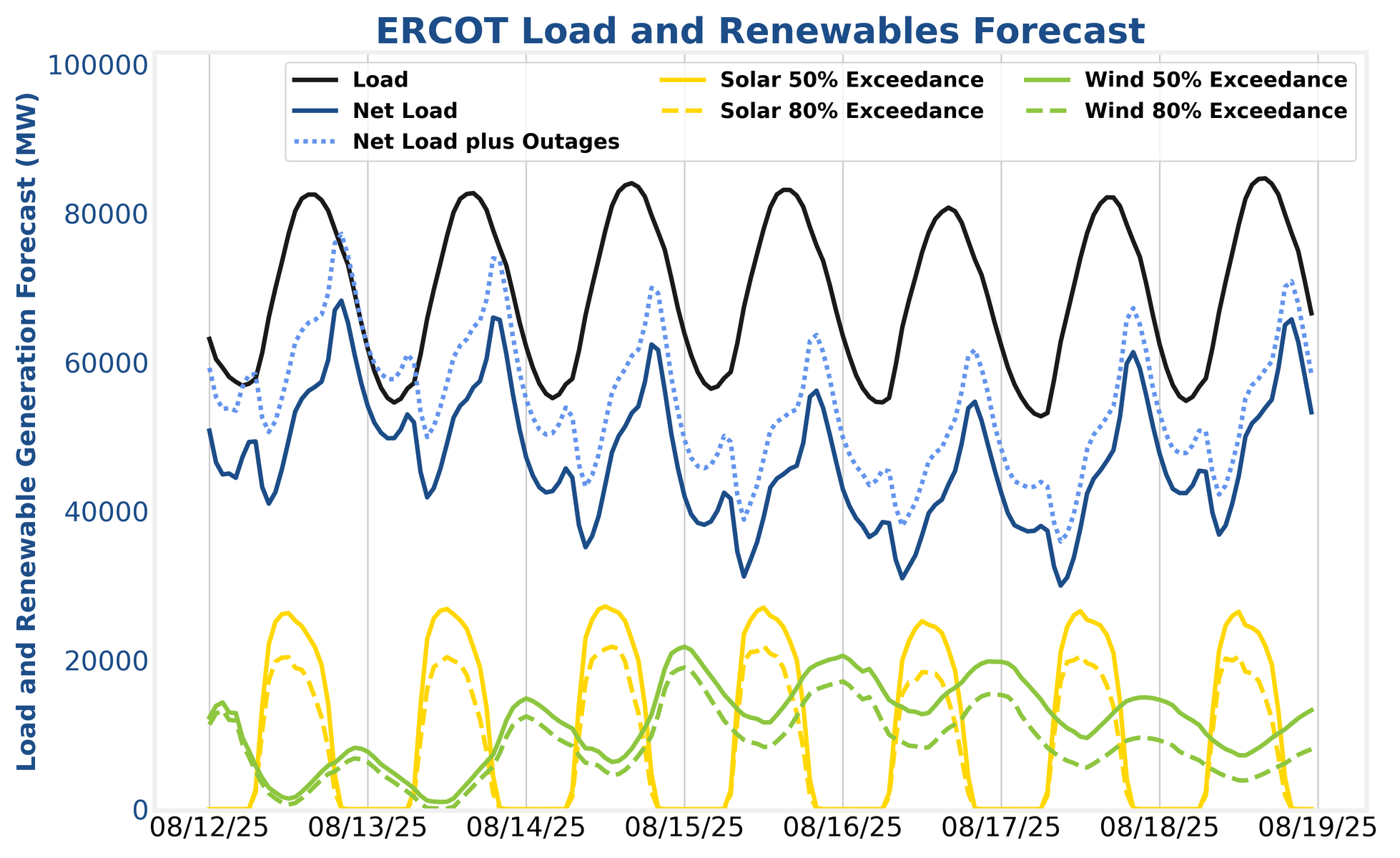

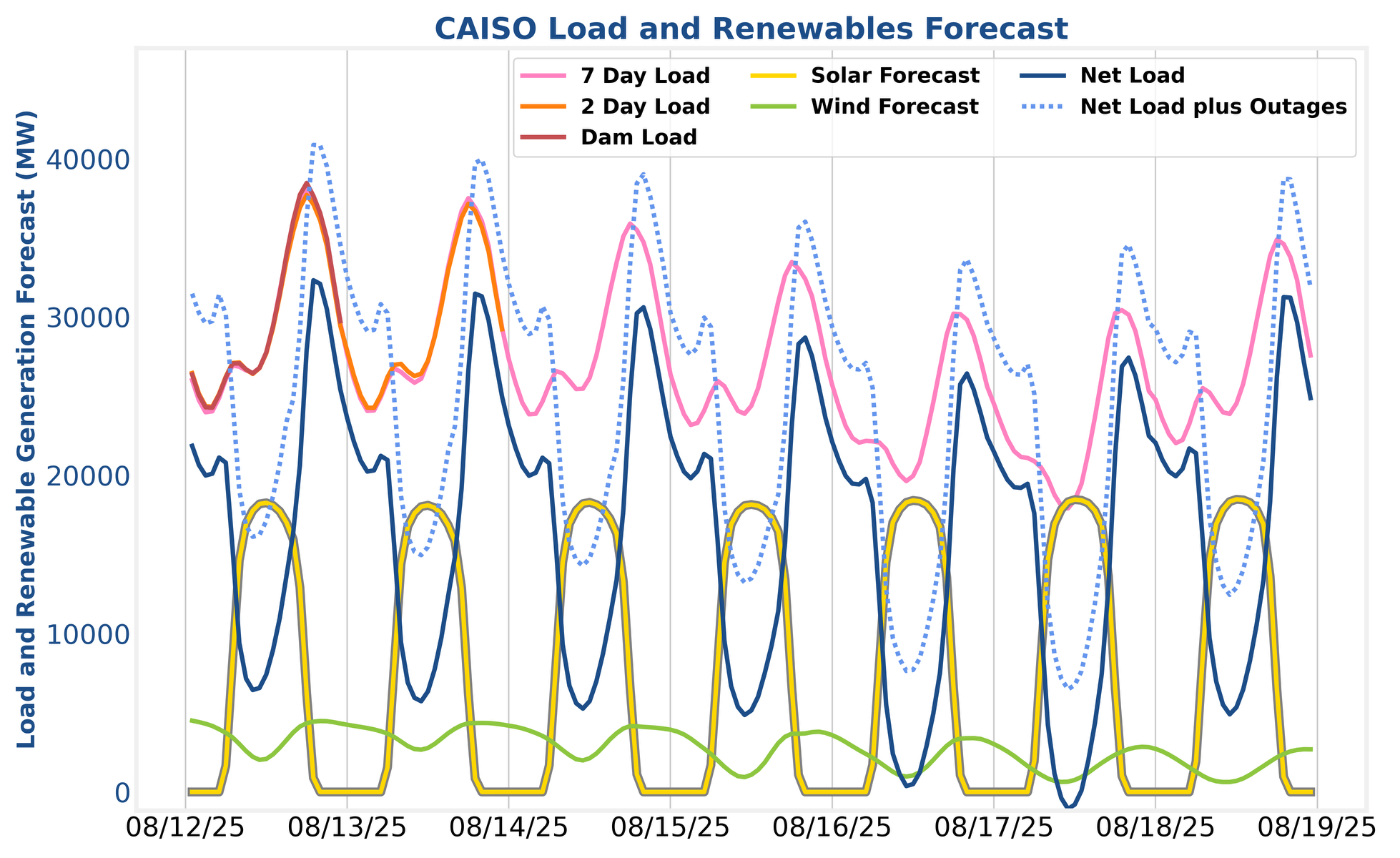

For the week of August 13th – 19th, the dog days of summer have taken hold and both the ERCOT and CAISO markets are set to be accordingly lethargic for the forecastable future.

In ERCOT, wind production will increase from where it was on the 12th, which should suppress market prices. Load is forecasted to pick back up on the 18th.

In CAISO, net load peaks will plummet going into the weekend so operators should focus on aggressive regulation strategies to squeeze out marginal revenue where they can.

Wind production will build to a crescendo on the 15th and send net load peaks back down to well below 60 GW. Operators should continue focusing on day-ahead energy, ECRS, and regulation up given how market dynamics have transformed the real-time energy and non-spin combination into a shell of its former late spring and early summer dominance.

SmartBidder’s Mt. Blue Sky strategy will recognize these patterns and the price peaks shifting to HE20 as the sun sets earlier each day. Talk to your analyst about tuning up Mt. Blue Sky to meet your risk tolerance if you want to take this window to tweak performance or capabilities.

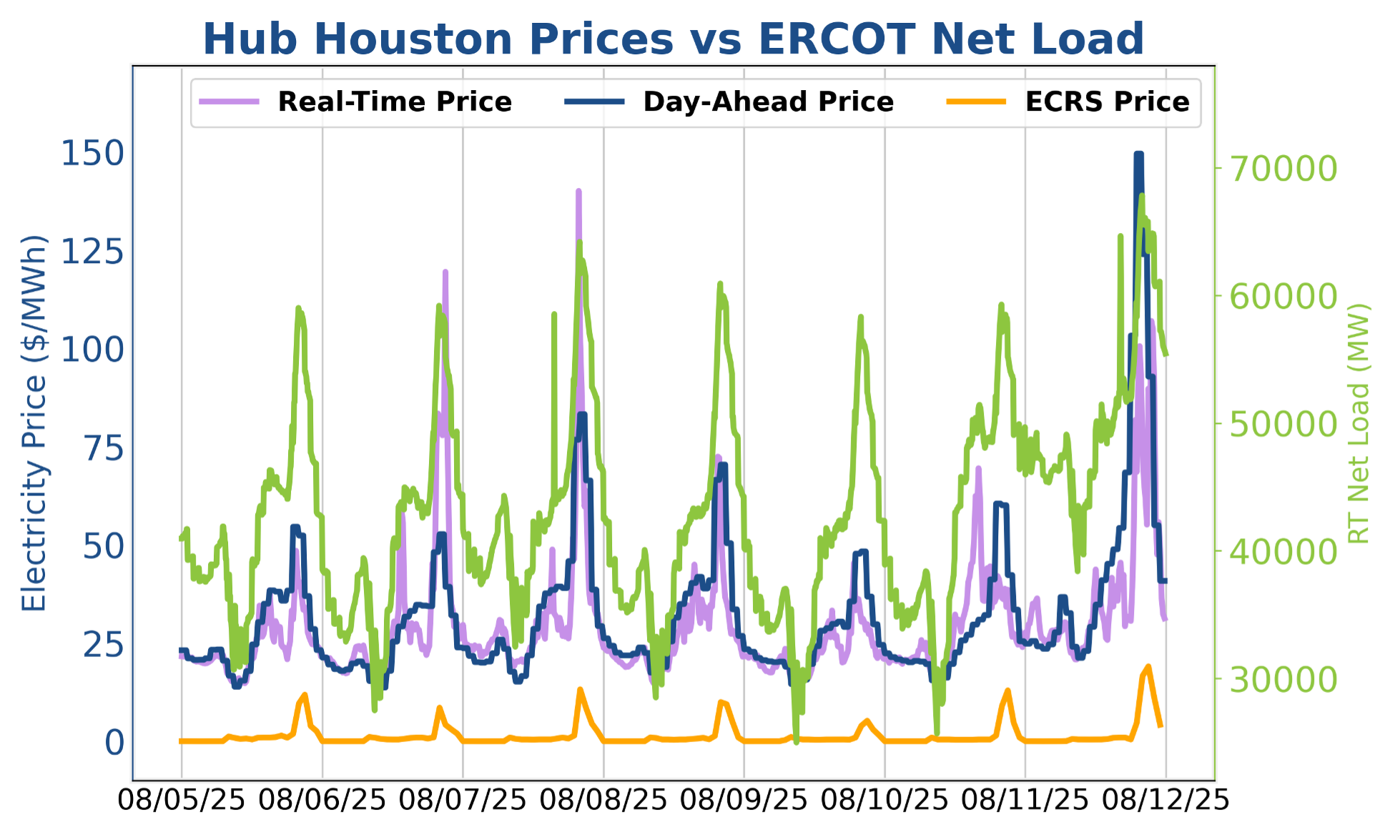

Last week was better spent on the beach than in the markets as day-ahead prices only peaked above $100/MWh on Monday the 11th. Even with poor energy prices, the ancillary service (AS) prices are poorer still and operators should be concentrating on energy arbitrage to fill the bulk of their revenue stack. Spin and ECRS have seen the strongest AS prices during the peaks with reg-up not far behind (and with the added benefit of more real-time energy throughput). The strongest strategy last week was Mt. Blue Sky with heavier participation in day-ahead energy, as the day-ahead (DA) energy discharge prices were better than real-time (RT) most days. Talk to your analyst about getting more aggressive with DA energy participation.

Net load levels will cool off in CAISO this week as they follow temperatures and the gross load peaks. With the macro CAISO market not delivering, operators should focus on understanding their individual nodal dynamics and how summer congestion impacts localized prices. Using the regional AS prices to play off localized energy prices can be a solid pathway to incremental revenue. Using all 24 hours to offer opportunistically in day-ahead is a good strategy for summer congestion, as that enables the battery to pick up on unexpectedly cheap charging day-ahead energy or expensive discharging prices that result from transmission constraints to bite at the local level. Batteries that cannot participate heavily in AS should count on a day-ahead energy strategy outperforming real-time energy arbitrage.

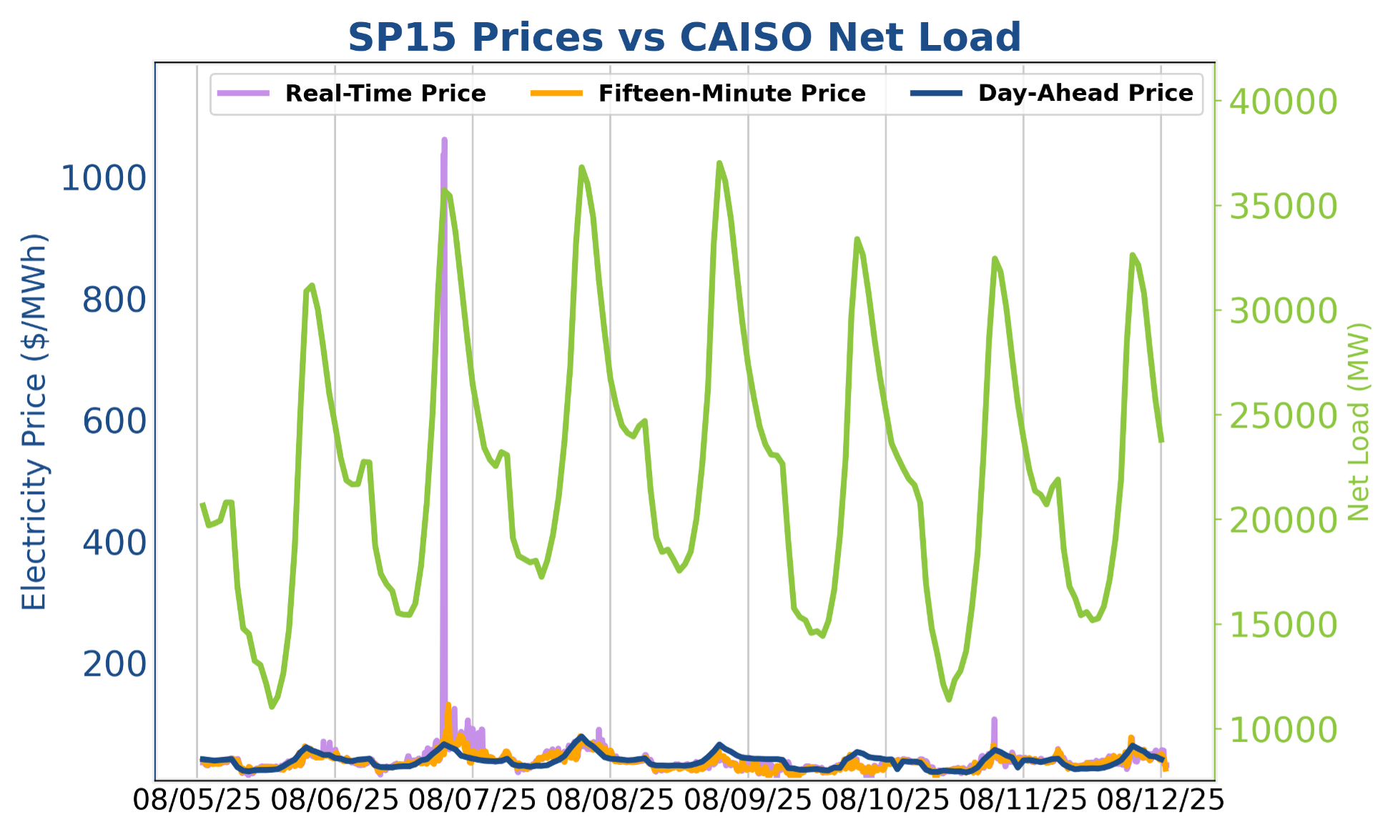

The high net load forecasts last week proved to consist of much more bark than bite as they were revised significantly downward and day-ahead price failed to clear above $100/MWh. Fifteen-minute prices largely followed their day-ahead counterparts. However, SP15 five-minute prices did hang out at ~$1000/MWh for about 15 minutes on the 6th. This revenue opportunity was largely unavailable to battery operators, however, as most BESS discharge offers were priced to clear and were awarded in the FMM rather than RTM market. For batteries that cannot participate in ancillaries, a DA TB4 strategy was more reliable than real-time energy arbitrage.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of August 13th – 19th, the dog days of summer have taken hold and both the ERCOT and CAISO markets are set to be accordingly lethargic for the forecastable future.

In ERCOT, wind production will increase from where it was on the 12th, which should suppress market prices. Load is forecasted to pick back up on the 18th.

In CAISO, net load peaks will plummet going into the weekend so operators should focus on aggressive regulation strategies to squeeze out marginal revenue where they can.

Wind production will build to a crescendo on the 15th and send net load peaks back down to well below 60 GW. Operators should continue focusing on day-ahead energy, ECRS, and regulation up given how market dynamics have transformed the real-time energy and non-spin combination into a shell of its former late spring and early summer dominance.

SmartBidder’s Mt. Blue Sky strategy will recognize these patterns and the price peaks shifting to HE20 as the sun sets earlier each day. Talk to your analyst about tuning up Mt. Blue Sky to meet your risk tolerance if you want to take this window to tweak performance or capabilities.

Last week was better spent on the beach than in the markets as day-ahead prices only peaked above $100/MWh on Monday the 11th. Even with poor energy prices, the ancillary service (AS) prices are poorer still and operators should be concentrating on energy arbitrage to fill the bulk of their revenue stack. Spin and ECRS have seen the strongest AS prices during the peaks with reg-up not far behind (and with the added benefit of more real-time energy throughput). The strongest strategy last week was Mt. Blue Sky with heavier participation in day-ahead energy, as the day-ahead (DA) energy discharge prices were better than real-time (RT) most days. Talk to your analyst about getting more aggressive with DA energy participation.

Net load levels will cool off in CAISO this week as they follow temperatures and the gross load peaks. With the macro CAISO market not delivering, operators should focus on understanding their individual nodal dynamics and how summer congestion impacts localized prices. Using the regional AS prices to play off localized energy prices can be a solid pathway to incremental revenue. Using all 24 hours to offer opportunistically in day-ahead is a good strategy for summer congestion, as that enables the battery to pick up on unexpectedly cheap charging day-ahead energy or expensive discharging prices that result from transmission constraints to bite at the local level. Batteries that cannot participate heavily in AS should count on a day-ahead energy strategy outperforming real-time energy arbitrage.

The high net load forecasts last week proved to consist of much more bark than bite as they were revised significantly downward and day-ahead price failed to clear above $100/MWh. Fifteen-minute prices largely followed their day-ahead counterparts. However, SP15 five-minute prices did hang out at ~$1000/MWh for about 15 minutes on the 6th. This revenue opportunity was largely unavailable to battery operators, however, as most BESS discharge offers were priced to clear and were awarded in the FMM rather than RTM market. For batteries that cannot participate in ancillaries, a DA TB4 strategy was more reliable than real-time energy arbitrage.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)