Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.png)

For the week of August 6th – August 12th, ERCOT revenue opportunities will subside as consistently strong wind production takes the market reins. In CAISO, hotter temps throughout the population centers will bring a brief yet welcome reprieve from the market doldrums so far this summer.

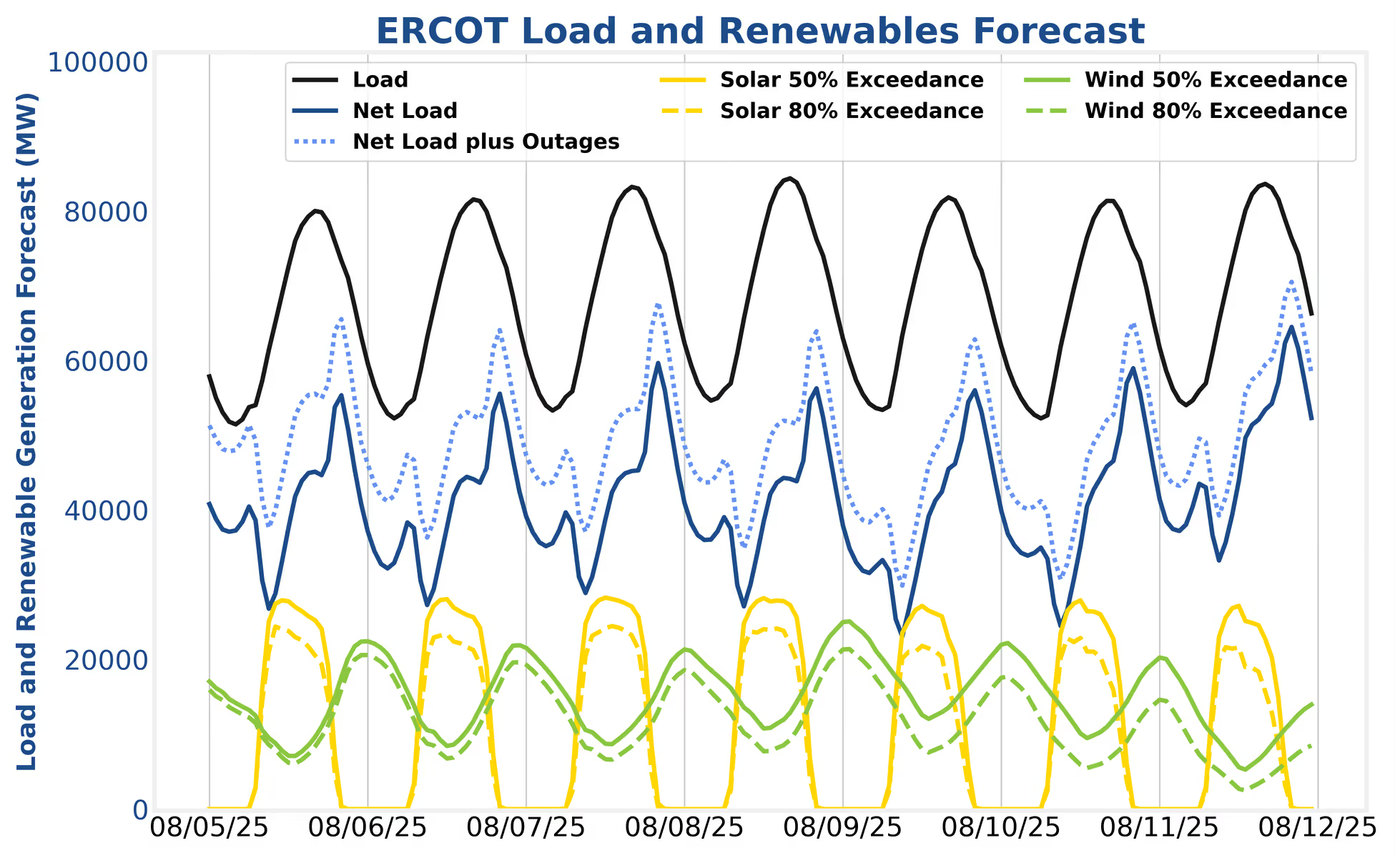

In ERCOT, market conditions will be stable and mild over the next week. Operators should evaluate performance during last week’s higher prices and make any necessary strategy tweaks for this week as the peaks arrive earlier in the evenings with the sun setting sooner given shorter days.

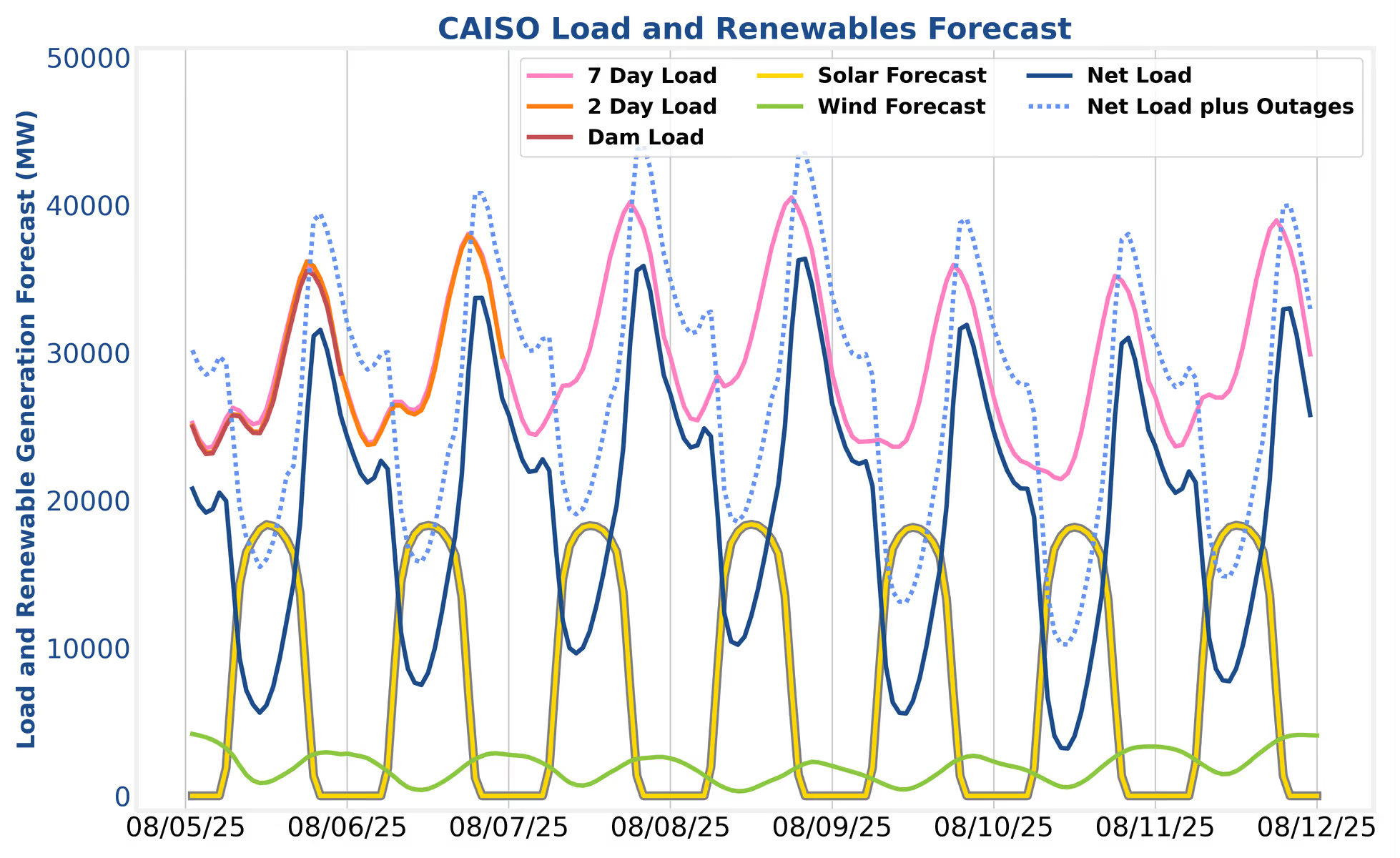

In CAISO, Thursday the 7th and Friday the 8th are the two days to lock in for this week. Operators should focus on picking up day-ahead energy discharge awards during the peak hours as energy arbitrage should be the centerpiece of BESS award stacks.

Typical Texas summer temperatures combined with wind production troughs of ~10 GW and higher will likely make this a week to forget. Day-ahead energy along with ECRS, spin, and reg-up should be the go-to products. Non-spin prices will look less attractive as more BESS operators become qualified for non-spin and ERCOT procures lower non-spin quantities during the peaks this August. Additionally, real-time energy prices will have a hard time breaching the $75/MWh deployment threshold on most days this week.

Mt. Bluesky will adapt to the lower non-spin value and should target day-ahead energy and the higher valued ancillary services (AS) products accordingly.

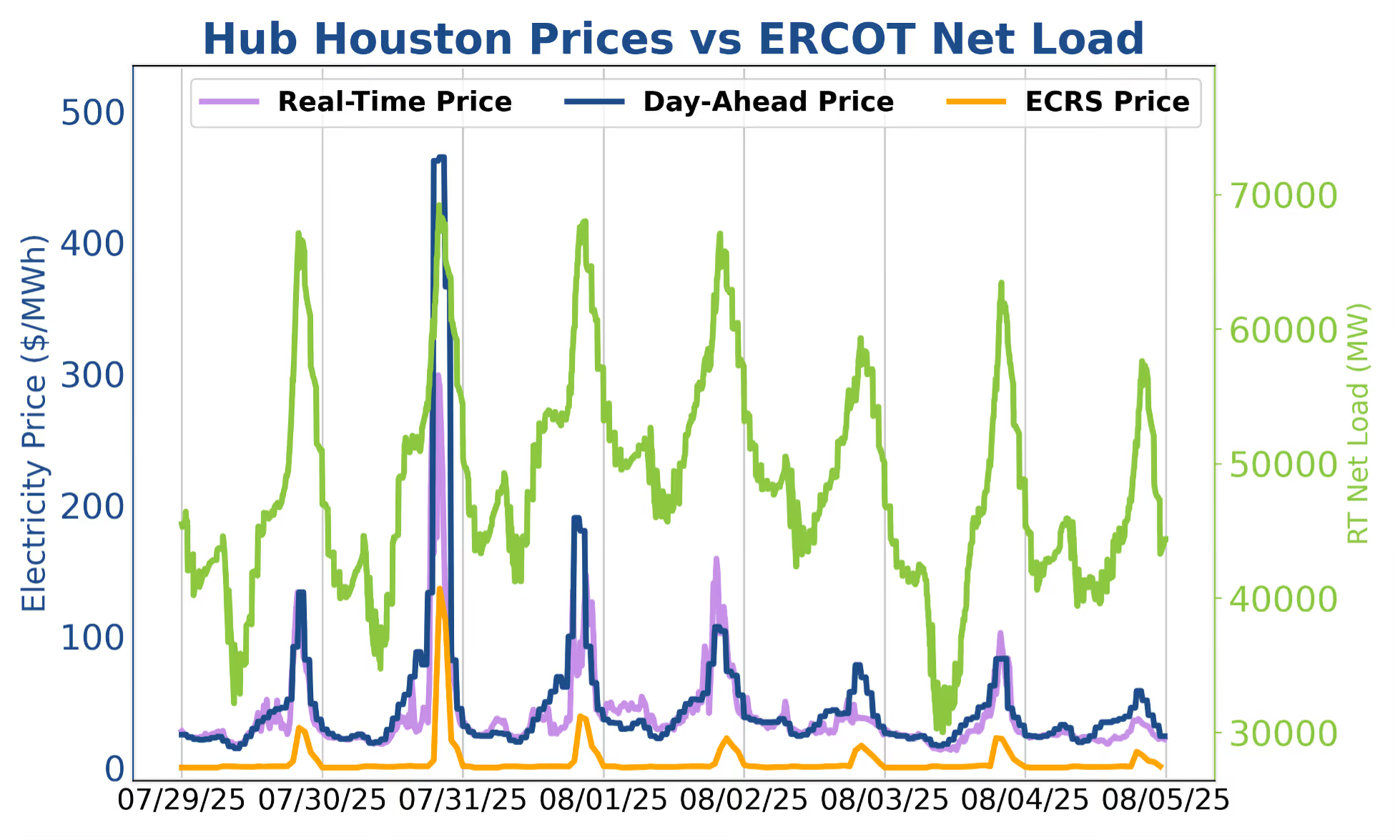

July 30th proved to be the best day of the summer so far in ERCOT with and day-ahead (DA) commitments winning the day with DA energy prices peaking around $500/MWh at most nodes, as well as ECRS and spin prices topping out at $136/MW. Real-time energy averaged ~$250/MWh during the peak as net load flirted with 70 GW, and BESS discharge peaked above 7 GW. Real-time prices are not spiking due to 7+ GW of BESS clearing to discharge along with a few more GW all jockeying for position in the SCED supply stack. Where the supply stack used to be paper thin, it is now filled with hundreds of batteries waiting around for real-time energy spikes and cannibalizing their collective opportunity. Such is the beauty, and, depending on your perspective, cruelty of competitive markets.

As long as multiple GW of BESS assets continue to wait around for real-time energy price spikes, the SmartBidder team will recommend taking on substantial (but not greedy or excessive) day-ahead energy positions via the Mt. Blue Sky strategy with appropriate maximum MW and maximum MWh guardrails in place.

Net load levels in CAISO will take a credible step up on Thursday and Friday this week. Peaks are currently expected to come in just north of 36 GW. These are solid levels, but barring a massive load miss, will not send real-time prices to $1,000/MWh. The CAISO supply stack will be robust in this range and DART spreads should favor day-ahead energy.

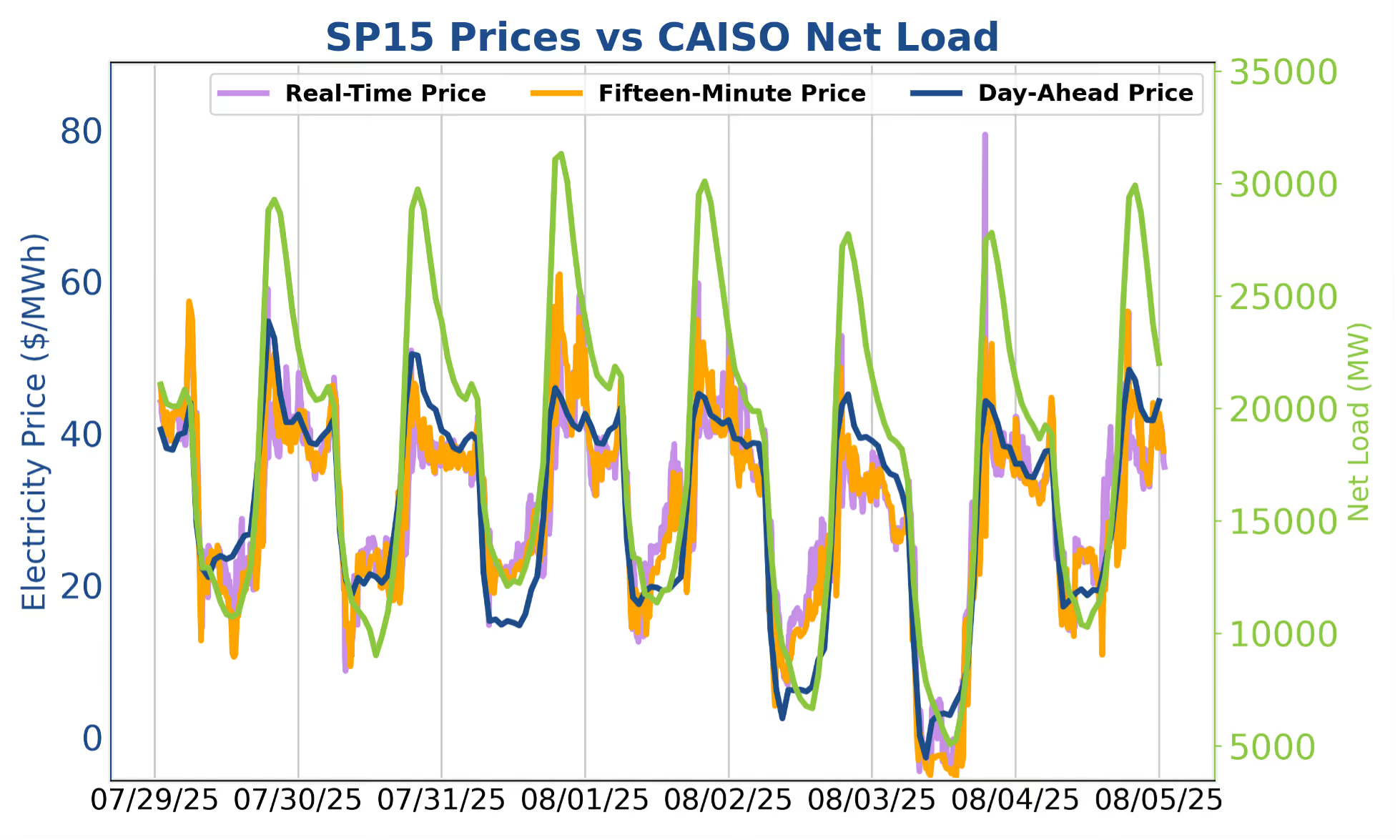

The SmartBidder view is that real-time price blowouts, while always possible, will require both 1) a substantial load forecast miss in the day-ahead timeframe and 2) a high (70%+) percentage of the CAISO battery fleet locking themselves up in day-ahead energy discharge. The probability of both factors aligning to favor real-time discharge is low. While real-time discharge prices have looked slightly more favorable since the end of July, the SmartBidder team recommends using the Mt. Shasta Strategy to target day-ahead energy discharge during the peak. Talk to your analyst about tweaking the strategy to ensure some day-ahead exposure if you have doubts about clearing into an appropriate amount.

Real-time prices (both charging and discharging) have been higher in CAISO over the past week. The HE19 ramps have seen some higher prints in the last fifteen minutes of the hour as the sun begins to set earlier on the host of CAISO solar farms. Below $10/MW AS prices have made AS-heavy strategies more difficult to execute of late, but there is still value to be had for operators willing to commit to heavy AS positions at the expense of full energy arbitrage cycles.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of August 6th – August 12th, ERCOT revenue opportunities will subside as consistently strong wind production takes the market reins. In CAISO, hotter temps throughout the population centers will bring a brief yet welcome reprieve from the market doldrums so far this summer.

In ERCOT, market conditions will be stable and mild over the next week. Operators should evaluate performance during last week’s higher prices and make any necessary strategy tweaks for this week as the peaks arrive earlier in the evenings with the sun setting sooner given shorter days.

In CAISO, Thursday the 7th and Friday the 8th are the two days to lock in for this week. Operators should focus on picking up day-ahead energy discharge awards during the peak hours as energy arbitrage should be the centerpiece of BESS award stacks.

Typical Texas summer temperatures combined with wind production troughs of ~10 GW and higher will likely make this a week to forget. Day-ahead energy along with ECRS, spin, and reg-up should be the go-to products. Non-spin prices will look less attractive as more BESS operators become qualified for non-spin and ERCOT procures lower non-spin quantities during the peaks this August. Additionally, real-time energy prices will have a hard time breaching the $75/MWh deployment threshold on most days this week.

Mt. Bluesky will adapt to the lower non-spin value and should target day-ahead energy and the higher valued ancillary services (AS) products accordingly.

July 30th proved to be the best day of the summer so far in ERCOT with and day-ahead (DA) commitments winning the day with DA energy prices peaking around $500/MWh at most nodes, as well as ECRS and spin prices topping out at $136/MW. Real-time energy averaged ~$250/MWh during the peak as net load flirted with 70 GW, and BESS discharge peaked above 7 GW. Real-time prices are not spiking due to 7+ GW of BESS clearing to discharge along with a few more GW all jockeying for position in the SCED supply stack. Where the supply stack used to be paper thin, it is now filled with hundreds of batteries waiting around for real-time energy spikes and cannibalizing their collective opportunity. Such is the beauty, and, depending on your perspective, cruelty of competitive markets.

As long as multiple GW of BESS assets continue to wait around for real-time energy price spikes, the SmartBidder team will recommend taking on substantial (but not greedy or excessive) day-ahead energy positions via the Mt. Blue Sky strategy with appropriate maximum MW and maximum MWh guardrails in place.

Net load levels in CAISO will take a credible step up on Thursday and Friday this week. Peaks are currently expected to come in just north of 36 GW. These are solid levels, but barring a massive load miss, will not send real-time prices to $1,000/MWh. The CAISO supply stack will be robust in this range and DART spreads should favor day-ahead energy.

The SmartBidder view is that real-time price blowouts, while always possible, will require both 1) a substantial load forecast miss in the day-ahead timeframe and 2) a high (70%+) percentage of the CAISO battery fleet locking themselves up in day-ahead energy discharge. The probability of both factors aligning to favor real-time discharge is low. While real-time discharge prices have looked slightly more favorable since the end of July, the SmartBidder team recommends using the Mt. Shasta Strategy to target day-ahead energy discharge during the peak. Talk to your analyst about tweaking the strategy to ensure some day-ahead exposure if you have doubts about clearing into an appropriate amount.

Real-time prices (both charging and discharging) have been higher in CAISO over the past week. The HE19 ramps have seen some higher prints in the last fifteen minutes of the hour as the sun begins to set earlier on the host of CAISO solar farms. Below $10/MW AS prices have made AS-heavy strategies more difficult to execute of late, but there is still value to be had for operators willing to commit to heavy AS positions at the expense of full energy arbitrage cycles.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)