Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

For the week of July 23rd – 29th, ERCOT is poised to run the hot-temps/low-wind gauntlet for the first time this summer while CAISO chugs along to the tune of $25/MWh arbitrage spreads.

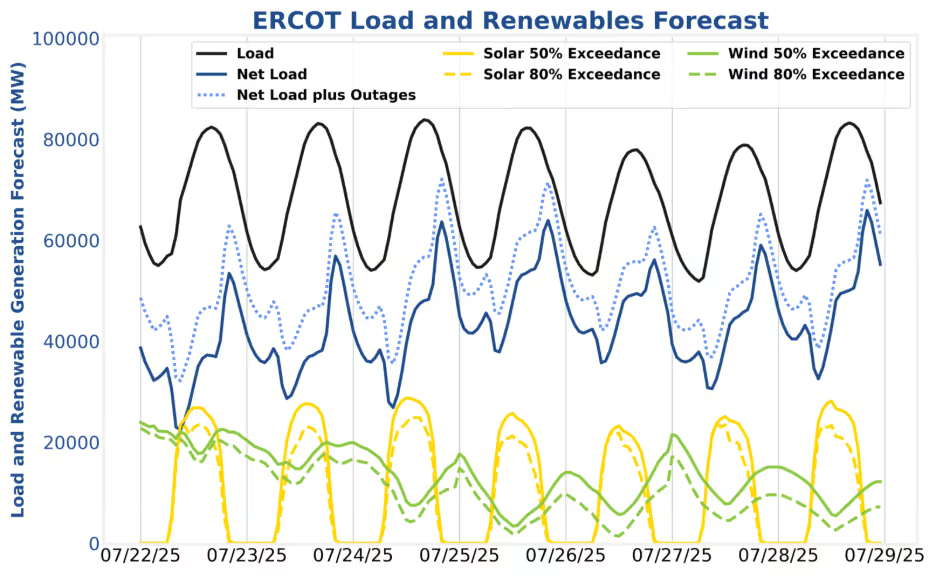

In ERCOT, net load levels are forecasted to peak at 64 GW on the 24th and 25th and 66 GW on the 28th. The 29th remains an open question as of this writing but could be the highest-peaking day of the bunch. Final tweaks to volatile-day strategies should be made, and maintenance should be canceled (if possible) as traders prepare for the strongest revenue opportunities of the summer to-date. Specific strategy recommendations are in the ERCOT section below.

In CAISO, day-ahead energy discharge and reg-down participation remain the name of the game. Arbitrage spreads will remain weak for the foreseeable future.

Revenue opportunities may shift from weak to promising on Thursday the 24th, Friday the 25th, Monday the 28th, and Tuesday the 29th. The change in fortune is owed to warmer temperatures combined with lower wind production. The “feels like temperature” will hit 106 degrees in Dallas on the 29th. Wind production is currently forecasted at 11 GW during the peak on the 28th and has plenty of downside room as the p20 forecast from ERCOT is currently at 6 GW during the peak. Wind production later in the week is still uncertain, and, the low levels could push net load even higher on the evening of the 28th. Asset operators should continue to monitor the forecasts as they evolve over the next several days.

The SmartBidder team recommends targeting a mixture of day-ahead energy, non-spin, and ECRS. Day-ahead prices often outperform real-time prices on the front half of extreme events before grid stress builds, and the non-spin and ECRS positions will lock in additional ancillary services (AS) revenue while ensuring real-time energy room if real-time prices do shoot for the stars. SmartBidder’s Mt. Blue Sky strategy can be tuned to limit day-ahead energy participation by hour and total MWh in a day to ensure these potential revenue opportunities aren’t missed. Non-spin and ECRS participation should be naturally facilitated by the active strategy, but can also be specifically incentivized via constraints for guaranteed behavior. Talk with your analyst about making any necessary adjustments.

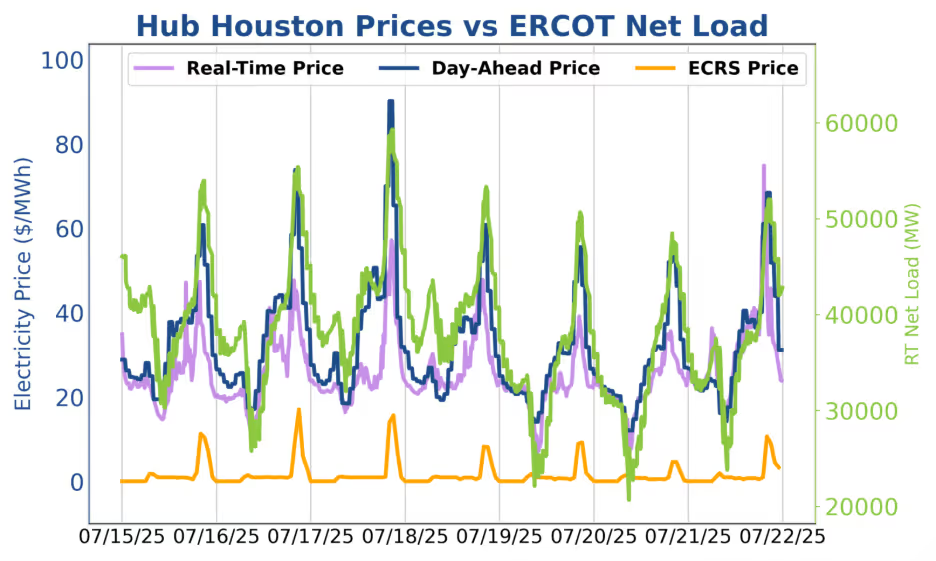

Market prices failed to break $100/MWh, and day-ahead energy prices (blue line) closely tracked net load (green line) throughout the week. The fundamentals of quiet market conditions were on full display last week. ECRS price peaks were about 1/5 of day-ahead energy price peaks, and operators who sold day-ahead virtual positions were handsomely rewarded after the beating short DART took the previous week.

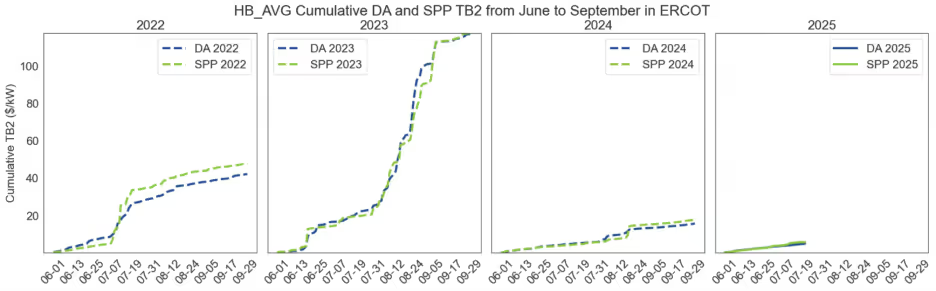

As shown in the TB2 tracker below, ERCOT prices are underperforming the past three years so far this summer, netting $4.8/kW for day-ahead and $5.7/kW for real-time top two hours minus the bottom two hours so far from June to present. This is only slightly off pace from 2024, but substantially below both 2022 and 2023, although we are not yet halfway through the summer weeks.

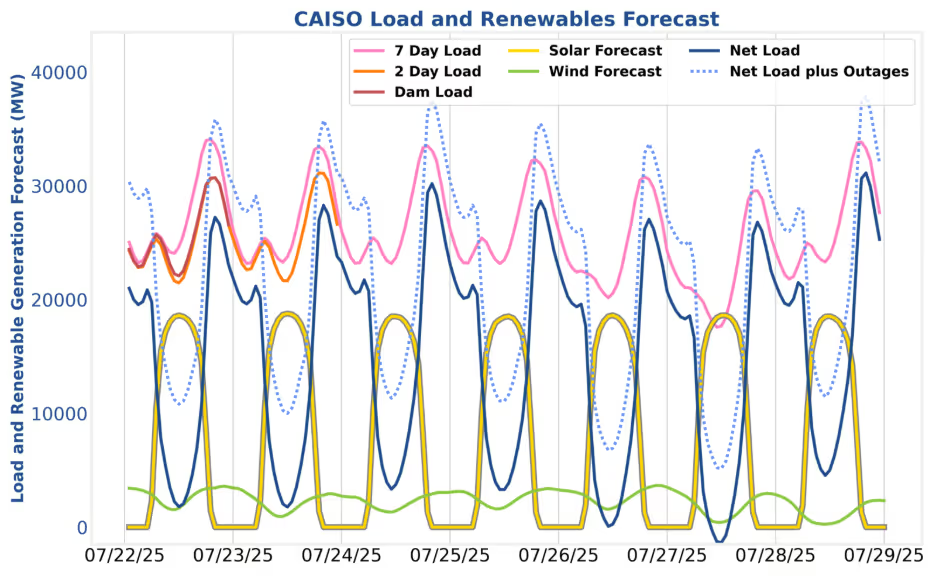

This week in CAISO, load is expected to stay below 35 GW, with projected net load peaking just above 30 GW on the 28th. Arbitrage spreads will be muted and fluctuate between $20/MWh and $30/MWh depending on the node and the day. Regulation participation is still a viable pathway to exceeding TB4 revenue, and SmartBidder’s Mt Shasta strategy has been exceeding TB4 by ~15+% so far this summer for standalone resources. While arbitrage spreads are poor, co-located resources should also consider participating in reg-down during the earlier charging hours as an additional source of revenue. Co-located resources that participate in reg-down should be wary of the unexpected throughput reg-down brings, only offering into the product economically through HE12 or HE13. This approach ensures that if throughput is less than expected there is ample time to place charge bids to capitalize on full SOC prior to elevated evening prices.

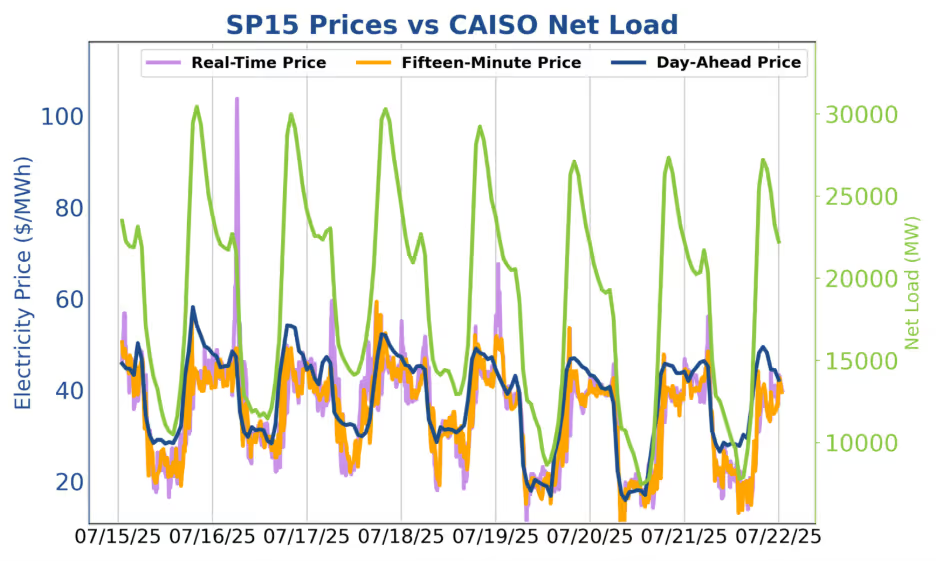

Last week in CAISO, we again saw the benefits of a day-ahead-heavy strategy given current market conditions. Real-time charging prices on the 17th, 18th, and 21st were lower than their day-ahead counterparts, but evening real-time discharging prices remained muted. As a result, the largest arbitrage spreads for a 4-hour BESS continued to favor day-ahead energy. At a few nodes, congestion briefly pushed real-time prices more negative, but these periods were fleeting and inconsistent. For example, while real-time prices from HE15 to HE17 on the 15th, 16th, and 18th were among the lowest of the week, on the 17th, real-time prices came in nearly $15/MWh above day-ahead. Operators who blended day-ahead energy with reg-down participation were best positioned to capture limited arbitrage opportunities—especially early in the week when higher midday net load narrowed the spread between charging and discharging windows.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of July 23rd – 29th, ERCOT is poised to run the hot-temps/low-wind gauntlet for the first time this summer while CAISO chugs along to the tune of $25/MWh arbitrage spreads.

In ERCOT, net load levels are forecasted to peak at 64 GW on the 24th and 25th and 66 GW on the 28th. The 29th remains an open question as of this writing but could be the highest-peaking day of the bunch. Final tweaks to volatile-day strategies should be made, and maintenance should be canceled (if possible) as traders prepare for the strongest revenue opportunities of the summer to-date. Specific strategy recommendations are in the ERCOT section below.

In CAISO, day-ahead energy discharge and reg-down participation remain the name of the game. Arbitrage spreads will remain weak for the foreseeable future.

Revenue opportunities may shift from weak to promising on Thursday the 24th, Friday the 25th, Monday the 28th, and Tuesday the 29th. The change in fortune is owed to warmer temperatures combined with lower wind production. The “feels like temperature” will hit 106 degrees in Dallas on the 29th. Wind production is currently forecasted at 11 GW during the peak on the 28th and has plenty of downside room as the p20 forecast from ERCOT is currently at 6 GW during the peak. Wind production later in the week is still uncertain, and, the low levels could push net load even higher on the evening of the 28th. Asset operators should continue to monitor the forecasts as they evolve over the next several days.

The SmartBidder team recommends targeting a mixture of day-ahead energy, non-spin, and ECRS. Day-ahead prices often outperform real-time prices on the front half of extreme events before grid stress builds, and the non-spin and ECRS positions will lock in additional ancillary services (AS) revenue while ensuring real-time energy room if real-time prices do shoot for the stars. SmartBidder’s Mt. Blue Sky strategy can be tuned to limit day-ahead energy participation by hour and total MWh in a day to ensure these potential revenue opportunities aren’t missed. Non-spin and ECRS participation should be naturally facilitated by the active strategy, but can also be specifically incentivized via constraints for guaranteed behavior. Talk with your analyst about making any necessary adjustments.

Market prices failed to break $100/MWh, and day-ahead energy prices (blue line) closely tracked net load (green line) throughout the week. The fundamentals of quiet market conditions were on full display last week. ECRS price peaks were about 1/5 of day-ahead energy price peaks, and operators who sold day-ahead virtual positions were handsomely rewarded after the beating short DART took the previous week.

As shown in the TB2 tracker below, ERCOT prices are underperforming the past three years so far this summer, netting $4.8/kW for day-ahead and $5.7/kW for real-time top two hours minus the bottom two hours so far from June to present. This is only slightly off pace from 2024, but substantially below both 2022 and 2023, although we are not yet halfway through the summer weeks.

This week in CAISO, load is expected to stay below 35 GW, with projected net load peaking just above 30 GW on the 28th. Arbitrage spreads will be muted and fluctuate between $20/MWh and $30/MWh depending on the node and the day. Regulation participation is still a viable pathway to exceeding TB4 revenue, and SmartBidder’s Mt Shasta strategy has been exceeding TB4 by ~15+% so far this summer for standalone resources. While arbitrage spreads are poor, co-located resources should also consider participating in reg-down during the earlier charging hours as an additional source of revenue. Co-located resources that participate in reg-down should be wary of the unexpected throughput reg-down brings, only offering into the product economically through HE12 or HE13. This approach ensures that if throughput is less than expected there is ample time to place charge bids to capitalize on full SOC prior to elevated evening prices.

Last week in CAISO, we again saw the benefits of a day-ahead-heavy strategy given current market conditions. Real-time charging prices on the 17th, 18th, and 21st were lower than their day-ahead counterparts, but evening real-time discharging prices remained muted. As a result, the largest arbitrage spreads for a 4-hour BESS continued to favor day-ahead energy. At a few nodes, congestion briefly pushed real-time prices more negative, but these periods were fleeting and inconsistent. For example, while real-time prices from HE15 to HE17 on the 15th, 16th, and 18th were among the lowest of the week, on the 17th, real-time prices came in nearly $15/MWh above day-ahead. Operators who blended day-ahead energy with reg-down participation were best positioned to capture limited arbitrage opportunities—especially early in the week when higher midday net load narrowed the spread between charging and discharging windows.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)