Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

For the week of July 30th – August 5th, ERCOT price action will cool off heading into August as gross load drops off and wind production picks up. CAISO will exit the month without even a hint of system-wide price strength.

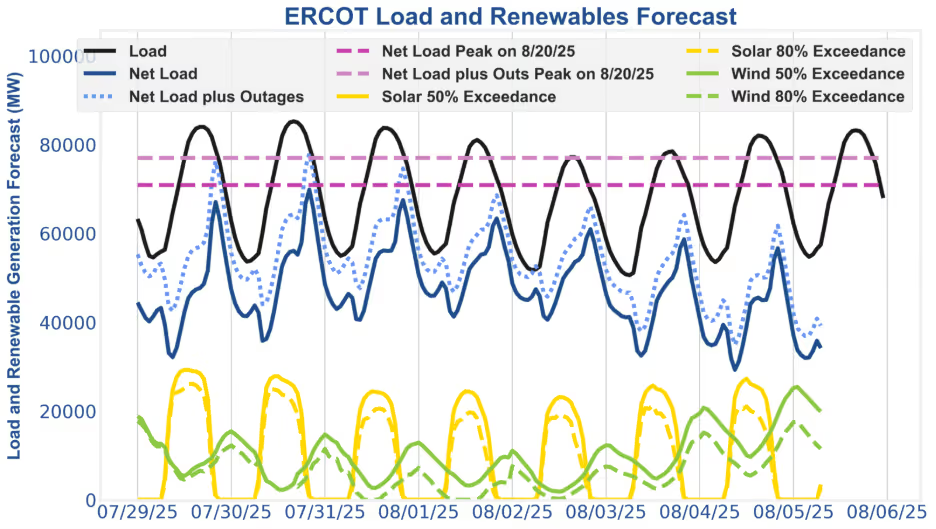

In ERCOT, the 30th should have the strongest day-ahead energy and ancillary service (AS) price action of the month though there is a chance real-time volatility could arise on any of the 29th, 30th, or 31st. Operators should continue focusing on day-ahead energy and real-time energy conducive AS products during the peak (primarily non-spin with reg-up on smaller net load peaking days and ECRS on larger net load peaking days).

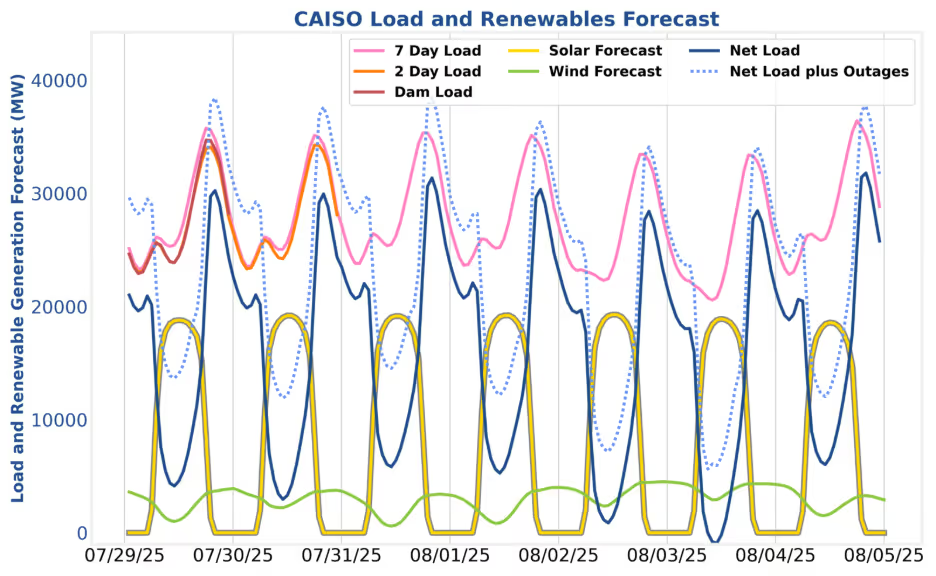

In CAISO, the market dynamics of the past few months will continue. Operators should try to take on as much regulation as possible while preserving 70-80% of their SoC room for energy TBX (and particularly day-ahead energy discharge).

While July might end with a bang, August is set to start off with a whimper as gross load cools off and the wind turbines spin again. That reprieve may be short-lived, however, as another round of heat is expected to arrive on the 5th.

As mentioned above, day-ahead energy discharge along with non-spin and regulation up for moderate days, and ECRS on more extreme days, is the recommended SmartBidder approach for the summer peaks. ECRS prices typically outperform regulation up and non-spin while preserving flexibility for real-time energy deployment — particularly during large net load misses when real-time prices spike. On weaker market days, offering into non-spin and reg-up — often priced at a discount to ECRS or spin — can still be advantageous, as these products provide easier access to the real-time energy market under milder conditions.

The SmartBidder Mt. Blue Sky strategy is designed to capture the essence of this approach and can be further tailored to match your specific risk tolerance and exposure to nodal price volatility.

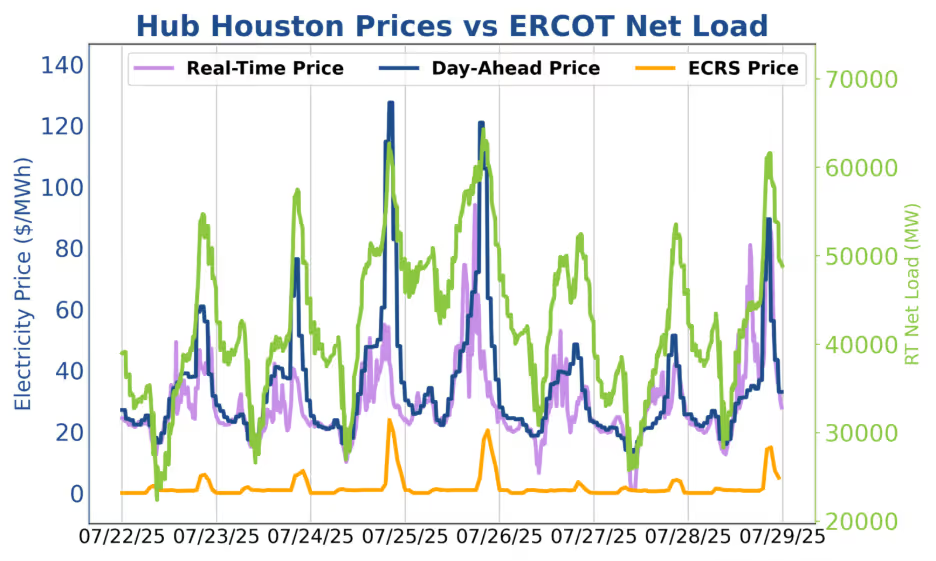

Market prices showed more volatility last week than the previous week, with both real-time and day-ahead energy prices (purple and blue lines) spiking above $100/MWh during peak net load periods—most notably on July 25 and 26. Day-ahead prices cleared higher than real-time prices on most days, making day-ahead participation the winning strategy in the first half of the week. Real-time prices, however, made a notable comeback in the latter half, with sharp peaks during early morning and late afternoon ramping hours.

ECRS prices (orange line) remained muted throughout, consistently clearing well below energy prices—typically just 15–20% of day-ahead prices. Despite the midweek movement, the market closed the week on a quieter note (though a strong rebound is likely in store at the time of this writing).

Net load in CAISO will elevate to slightly higher than 30 GW on both the 31st and 4th. However, these levels are nothing to write home about (and yet, as this is a newsletter, we will indeed write about it). Patience, more than any specific strategy configuration, is the recommended course of action. Frequent readers of this section will already know that the SmartBidder team recommends day-ahead energy discharge combined with as much reg participation (particularly reg-down) as CAISO will award. The charge decision is a bit of a pick-your-poison between the two energy markets and reg-down that varies day-to-day, week-to-week, and node-to-node.

One particularly robust SmartBidder strategy for standalone assets is to plan around a midnight SoC of 30%, offer economic reg-down and day-ahead energy charging bids for midday, and then economic reg and day-ahead energy discharge bids during the evening peak. The day-ahead energy discharge bids should be positioned more aggressively than the other bids so that the asset can lock in at least 30% day-ahead energy discharge and preserve more day-ahead energy discharge upside even if the charge bids don’t clear on price since CAISO will clear on spread. Talk to your analyst about dialing up this version of Mt. Shasta if you have questions or are curious about having it run in simulated fashion.

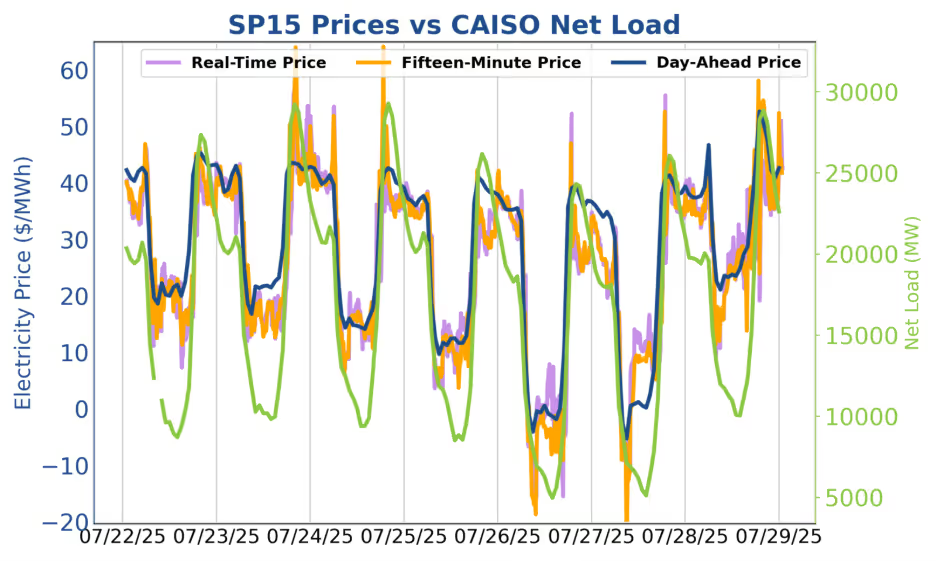

Last week saw relatively stable conditions in California. Wholesale prices largely reflected ample solar and wind as net load dipped to around 25 GW mid-week between the 25th - 28th. Some real-time opportunities did emerge earlier in the week — particularly on the 23rd and 24th — when net load climbed toward 30 GW, but these events were exceptions rather than a shift in trend. Real-time charging also remained inconsistent; for example, on the 27th, when prices surged well above day-ahead levels during prime midday net load hours. On the whole, the market continues to crawl forward under mild load conditions, and consistent real-time value will likely remain elusive until net loads push higher.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of July 30th – August 5th, ERCOT price action will cool off heading into August as gross load drops off and wind production picks up. CAISO will exit the month without even a hint of system-wide price strength.

In ERCOT, the 30th should have the strongest day-ahead energy and ancillary service (AS) price action of the month though there is a chance real-time volatility could arise on any of the 29th, 30th, or 31st. Operators should continue focusing on day-ahead energy and real-time energy conducive AS products during the peak (primarily non-spin with reg-up on smaller net load peaking days and ECRS on larger net load peaking days).

In CAISO, the market dynamics of the past few months will continue. Operators should try to take on as much regulation as possible while preserving 70-80% of their SoC room for energy TBX (and particularly day-ahead energy discharge).

While July might end with a bang, August is set to start off with a whimper as gross load cools off and the wind turbines spin again. That reprieve may be short-lived, however, as another round of heat is expected to arrive on the 5th.

As mentioned above, day-ahead energy discharge along with non-spin and regulation up for moderate days, and ECRS on more extreme days, is the recommended SmartBidder approach for the summer peaks. ECRS prices typically outperform regulation up and non-spin while preserving flexibility for real-time energy deployment — particularly during large net load misses when real-time prices spike. On weaker market days, offering into non-spin and reg-up — often priced at a discount to ECRS or spin — can still be advantageous, as these products provide easier access to the real-time energy market under milder conditions.

The SmartBidder Mt. Blue Sky strategy is designed to capture the essence of this approach and can be further tailored to match your specific risk tolerance and exposure to nodal price volatility.

Market prices showed more volatility last week than the previous week, with both real-time and day-ahead energy prices (purple and blue lines) spiking above $100/MWh during peak net load periods—most notably on July 25 and 26. Day-ahead prices cleared higher than real-time prices on most days, making day-ahead participation the winning strategy in the first half of the week. Real-time prices, however, made a notable comeback in the latter half, with sharp peaks during early morning and late afternoon ramping hours.

ECRS prices (orange line) remained muted throughout, consistently clearing well below energy prices—typically just 15–20% of day-ahead prices. Despite the midweek movement, the market closed the week on a quieter note (though a strong rebound is likely in store at the time of this writing).

Net load in CAISO will elevate to slightly higher than 30 GW on both the 31st and 4th. However, these levels are nothing to write home about (and yet, as this is a newsletter, we will indeed write about it). Patience, more than any specific strategy configuration, is the recommended course of action. Frequent readers of this section will already know that the SmartBidder team recommends day-ahead energy discharge combined with as much reg participation (particularly reg-down) as CAISO will award. The charge decision is a bit of a pick-your-poison between the two energy markets and reg-down that varies day-to-day, week-to-week, and node-to-node.

One particularly robust SmartBidder strategy for standalone assets is to plan around a midnight SoC of 30%, offer economic reg-down and day-ahead energy charging bids for midday, and then economic reg and day-ahead energy discharge bids during the evening peak. The day-ahead energy discharge bids should be positioned more aggressively than the other bids so that the asset can lock in at least 30% day-ahead energy discharge and preserve more day-ahead energy discharge upside even if the charge bids don’t clear on price since CAISO will clear on spread. Talk to your analyst about dialing up this version of Mt. Shasta if you have questions or are curious about having it run in simulated fashion.

Last week saw relatively stable conditions in California. Wholesale prices largely reflected ample solar and wind as net load dipped to around 25 GW mid-week between the 25th - 28th. Some real-time opportunities did emerge earlier in the week — particularly on the 23rd and 24th — when net load climbed toward 30 GW, but these events were exceptions rather than a shift in trend. Real-time charging also remained inconsistent; for example, on the 27th, when prices surged well above day-ahead levels during prime midday net load hours. On the whole, the market continues to crawl forward under mild load conditions, and consistent real-time value will likely remain elusive until net loads push higher.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)