Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

For the week of June 25th – July 2nd, the heat and humidity wave pummeling the eastern half of the U.S. will spare CAISO and ERCOT. Higher renewable and storage penetrations combined with slightly cooler temps will keep prices in these two markets much milder than their less renewably evolved counterparts.

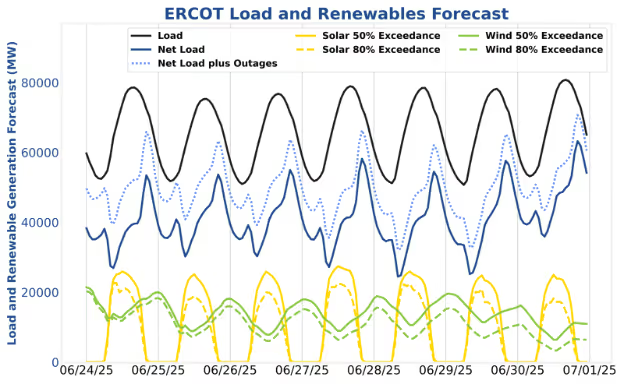

In ERCOT, asset traders should keep an eye on June 30th as wind production tapers off and higher temperatures inch gross load up. Energy conducive ancillary services (AS) participation and open energy capacity is the name of the game. Optimizers should not plan to enter July with available SoC.

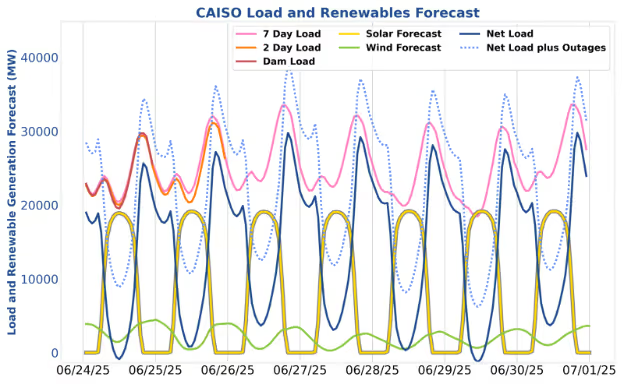

In CAISO, Gross load forecasts remain muted as heat throughout southern California avoids the main population centers. AS participation along with day-ahead energy discharge during the evening peaks has led to the strongest returns so far in June.

The net load peak on the 30th is currently forecasted to weigh in at 63 GW. On one hand, 63 GW is not much to write home about (for context, the 19th and 20th of August last summer were ~70 GW peaks, and there is about 6 GW more storage capacity waiting to pounce on structural volatility this time around). On the other hand, beggars can’t be choosers, and mediocre prices are better than weak prices. Asset operators should expect SmartBidder to target a diversified mix of energy and AS (mostly non-spin and reg-up) on the evening of the 30th. Day-ahead energy offers should be structured via tiered thresholds to realize increasing awards if the day-ahead market clears energy excessively high. Non-spin should be offered cheaply due to the high likelihood real-time prices come in over $75/MWh while the other AS products are offered conservatively according to SmartBidder’s opportunity cost framework.

Mt. Blue Sky remains the recommended SmartBidder strategy. Talk to your analyst about creating a customized version to adhere to your specific risk-tolerance thresholds.

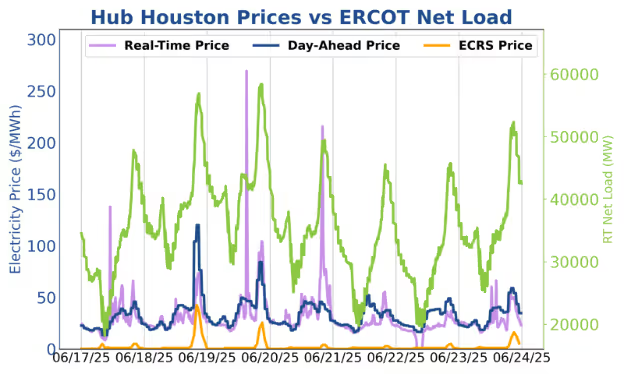

Friday the 20th was the most interesting day in ERCOT last week as east-west transmission constraints trapped strong Hub West wind production from getting to Hub North, which was feeling the heat through higher load in the population centers. As a result, ERCOT started the 8:00 hour with negative power prices in Hub West and $400/MWh LMPs across many nodes in the east. This contrast illustrates the value of AS obligation shifting for asset operators with batteries spread across multiple hubs since AS prices are ISO-wide. With RTC+B implementation in December, this market inefficiency will be readily monetizable by all asset operators (instead of just the big players with spread out portfolios) and thus will greatly decrease in value as the market becomes more efficient and AS prices fluctuate in real-time.

Solar production forecasts in CAISO are extremely stable over the next week, peaking at just shy of 20 GW each day. Temperature will move around a lot more than solar irradiance day-to-day, and therefore gross load peaks will fluctuate between 25 GW and 31 GW. The CAISO supply stack is very robust in this range, so day-ahead clearing prices will not vary much. Operators should concentrate on providing as much AS as SmartBidder thinks it can handle while preserving room to capture energy peaks. Day-ahead evening peak prices have been favorable while real-time prices have consistently come in above day-ahead prices for a few hours each overnight/morning. Mt Shasta is the recommended SmartBidder strategy.

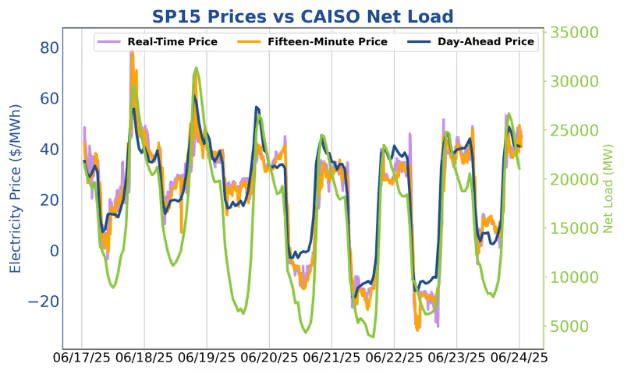

For the first time this summer, real-time charging prices fell below the day-ahead settlement prices in CAISO for three consecutive days. This trend, observed on the 20th, 21st, and 22nd, was driven by the lowest net loads of the week, which contributed to favorable mid-day real-time prices. Since CAISO is in a temperature-dominated load regime, these days also featured the lowest net loads during the evening peaks, resulting in muted evening real-time prices. On the evenings of the 20th and 21st, real-time prices remained below day-ahead levels, effectively offsetting the cheaper cost of charging earlier in the afternoon. Only the 22nd offered a clear advantage to opting out of day-ahead participation entirely. The day on last week's watch list, the 18th, ushered in a net load peak above 30 GW. Day-ahead prices cleared close to $60/MWh for HE20 and HE21—levels that real-time prices could barely muster the vigor to match, let alone exceed, for any sustained period.

Operators should continue to prioritize day-ahead energy participation, as real-time volatility remains limited. Days like the 19th still persist, where both the charging and discharging windows significantly favor day-ahead participation.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of June 25th – July 2nd, the heat and humidity wave pummeling the eastern half of the U.S. will spare CAISO and ERCOT. Higher renewable and storage penetrations combined with slightly cooler temps will keep prices in these two markets much milder than their less renewably evolved counterparts.

In ERCOT, asset traders should keep an eye on June 30th as wind production tapers off and higher temperatures inch gross load up. Energy conducive ancillary services (AS) participation and open energy capacity is the name of the game. Optimizers should not plan to enter July with available SoC.

In CAISO, Gross load forecasts remain muted as heat throughout southern California avoids the main population centers. AS participation along with day-ahead energy discharge during the evening peaks has led to the strongest returns so far in June.

The net load peak on the 30th is currently forecasted to weigh in at 63 GW. On one hand, 63 GW is not much to write home about (for context, the 19th and 20th of August last summer were ~70 GW peaks, and there is about 6 GW more storage capacity waiting to pounce on structural volatility this time around). On the other hand, beggars can’t be choosers, and mediocre prices are better than weak prices. Asset operators should expect SmartBidder to target a diversified mix of energy and AS (mostly non-spin and reg-up) on the evening of the 30th. Day-ahead energy offers should be structured via tiered thresholds to realize increasing awards if the day-ahead market clears energy excessively high. Non-spin should be offered cheaply due to the high likelihood real-time prices come in over $75/MWh while the other AS products are offered conservatively according to SmartBidder’s opportunity cost framework.

Mt. Blue Sky remains the recommended SmartBidder strategy. Talk to your analyst about creating a customized version to adhere to your specific risk-tolerance thresholds.

Friday the 20th was the most interesting day in ERCOT last week as east-west transmission constraints trapped strong Hub West wind production from getting to Hub North, which was feeling the heat through higher load in the population centers. As a result, ERCOT started the 8:00 hour with negative power prices in Hub West and $400/MWh LMPs across many nodes in the east. This contrast illustrates the value of AS obligation shifting for asset operators with batteries spread across multiple hubs since AS prices are ISO-wide. With RTC+B implementation in December, this market inefficiency will be readily monetizable by all asset operators (instead of just the big players with spread out portfolios) and thus will greatly decrease in value as the market becomes more efficient and AS prices fluctuate in real-time.

Solar production forecasts in CAISO are extremely stable over the next week, peaking at just shy of 20 GW each day. Temperature will move around a lot more than solar irradiance day-to-day, and therefore gross load peaks will fluctuate between 25 GW and 31 GW. The CAISO supply stack is very robust in this range, so day-ahead clearing prices will not vary much. Operators should concentrate on providing as much AS as SmartBidder thinks it can handle while preserving room to capture energy peaks. Day-ahead evening peak prices have been favorable while real-time prices have consistently come in above day-ahead prices for a few hours each overnight/morning. Mt Shasta is the recommended SmartBidder strategy.

For the first time this summer, real-time charging prices fell below the day-ahead settlement prices in CAISO for three consecutive days. This trend, observed on the 20th, 21st, and 22nd, was driven by the lowest net loads of the week, which contributed to favorable mid-day real-time prices. Since CAISO is in a temperature-dominated load regime, these days also featured the lowest net loads during the evening peaks, resulting in muted evening real-time prices. On the evenings of the 20th and 21st, real-time prices remained below day-ahead levels, effectively offsetting the cheaper cost of charging earlier in the afternoon. Only the 22nd offered a clear advantage to opting out of day-ahead participation entirely. The day on last week's watch list, the 18th, ushered in a net load peak above 30 GW. Day-ahead prices cleared close to $60/MWh for HE20 and HE21—levels that real-time prices could barely muster the vigor to match, let alone exceed, for any sustained period.

Operators should continue to prioritize day-ahead energy participation, as real-time volatility remains limited. Days like the 19th still persist, where both the charging and discharging windows significantly favor day-ahead participation.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)