Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

For the week of September 3rd – 9th: Briefly warmer weather in ERCOT will be buffeted by stronger wind production while load forecast variability will remain the key wildcard during CAISO evening peaks.

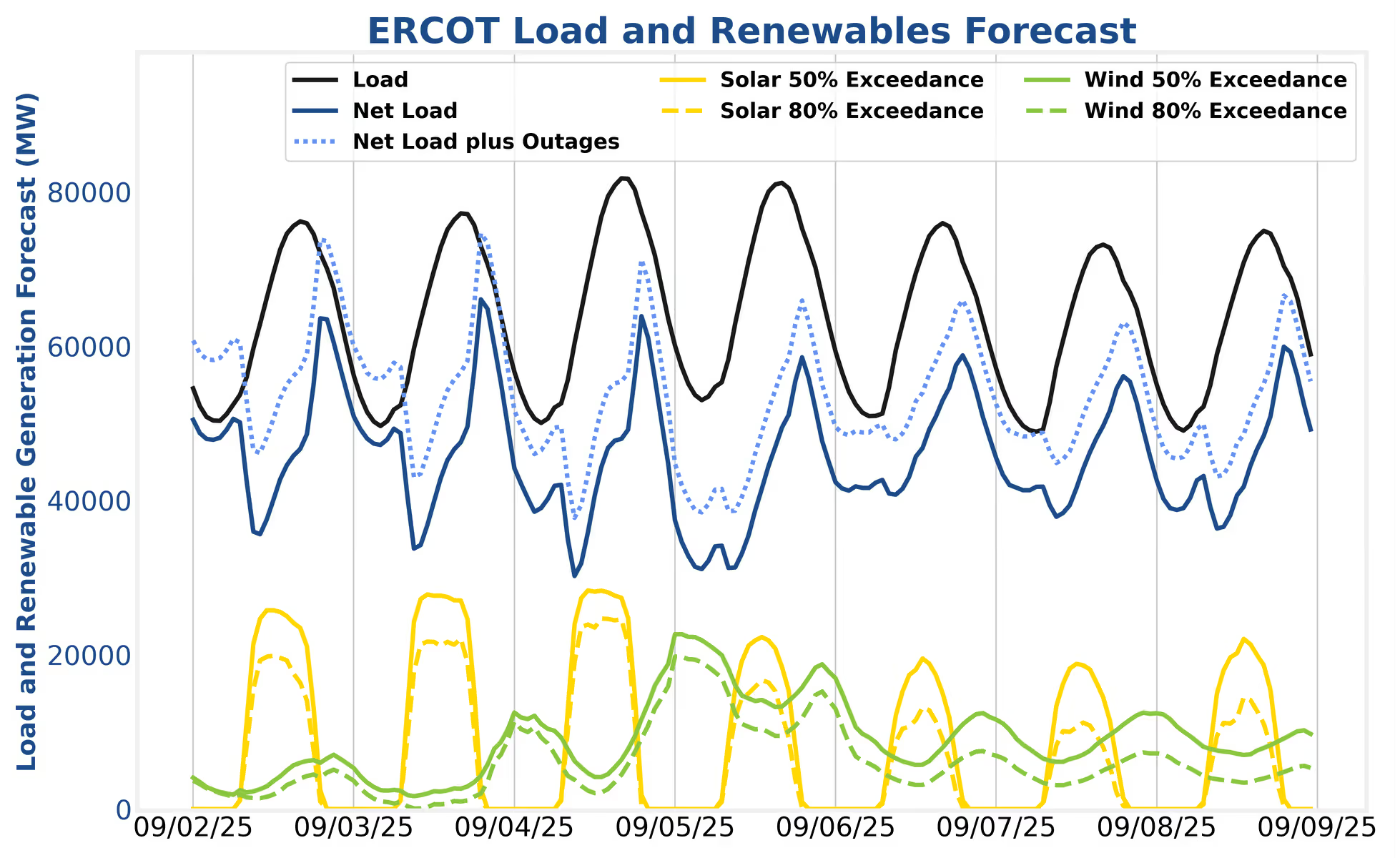

In ERCOT, gross load levels will be highest on the 4th and 5th, offset by strongly ramping wind production during the day on the 4th. Operators should target day-ahead energy discharge during the peak hours.

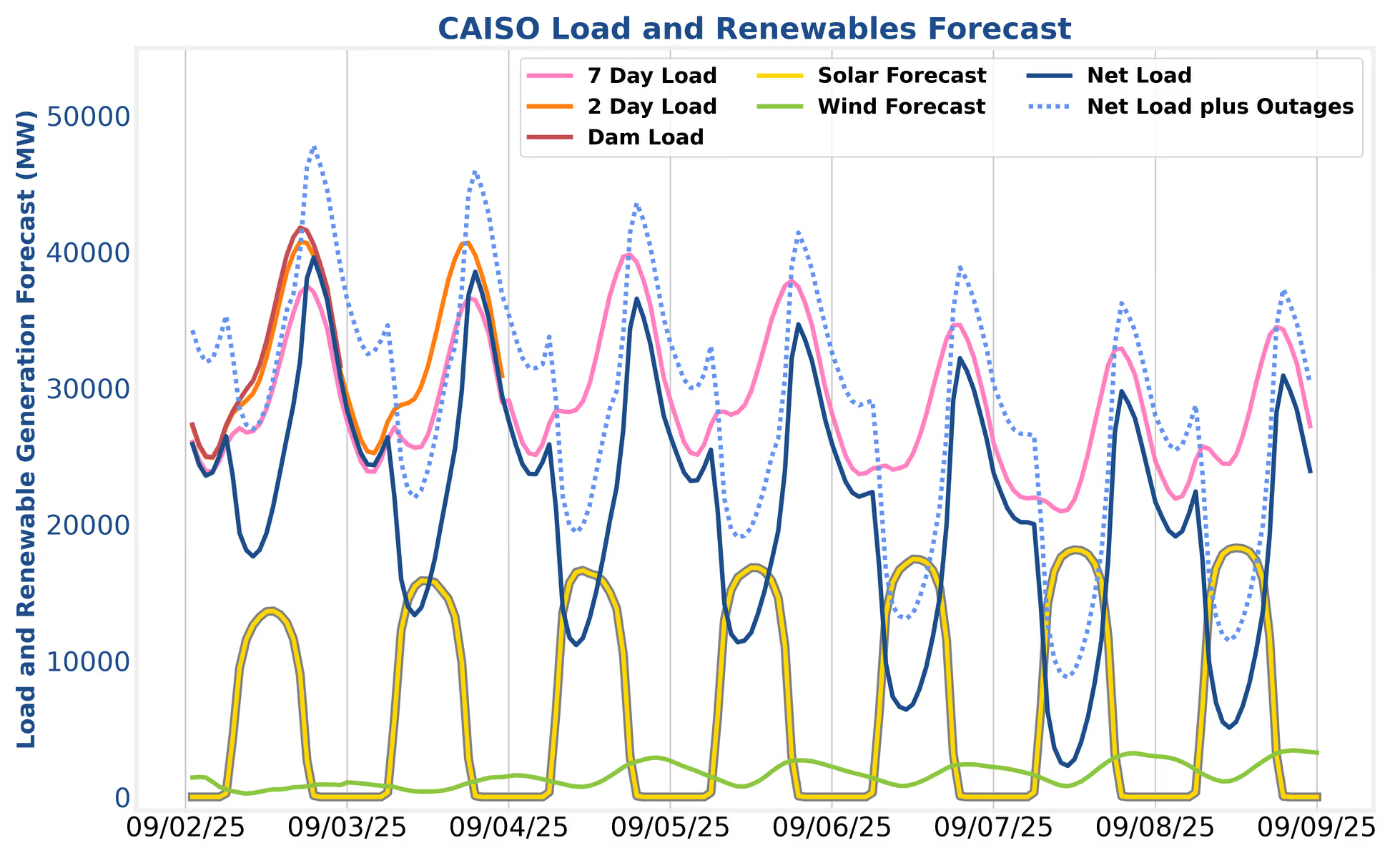

In CAISO, while the 7-day load forecast projects calmer conditions returning, that forecast has recently undershot load levels by several GW. Operators should rely on the day-ahead and two-day-ahead forecasts. Heavy day-ahead participation – both energy and economic ancillary services (AS) offers - is the SmartBidder recommended approach.

Wind production will ramp from near-zero levels on the 3rd to 20+ GW levels on the 5th before settling down to 10 GW averages for the 6th. Solar will shift from strong production north of 25 GW through the 4th to less than 20 GW by the 6th. Taken together with the load forecast peak variability, these shifting dynamics will largely conspire to wash out in the net load forecast. The 3rd and 4th will elicit the strongest peaks, up to 66 GW on the 3rd. For storage assets, these days should look familiar to the conditions of the past 3 months. Strategies that worked well throughout the summer should continue working well. Allowing Mt. Blue Sky to optimize across the AS products and energy, knowing that it will focus on day-ahead energy discharge, is the surest bet to maximal revenue capture as TBX strategies are increasingly hard to outperform.

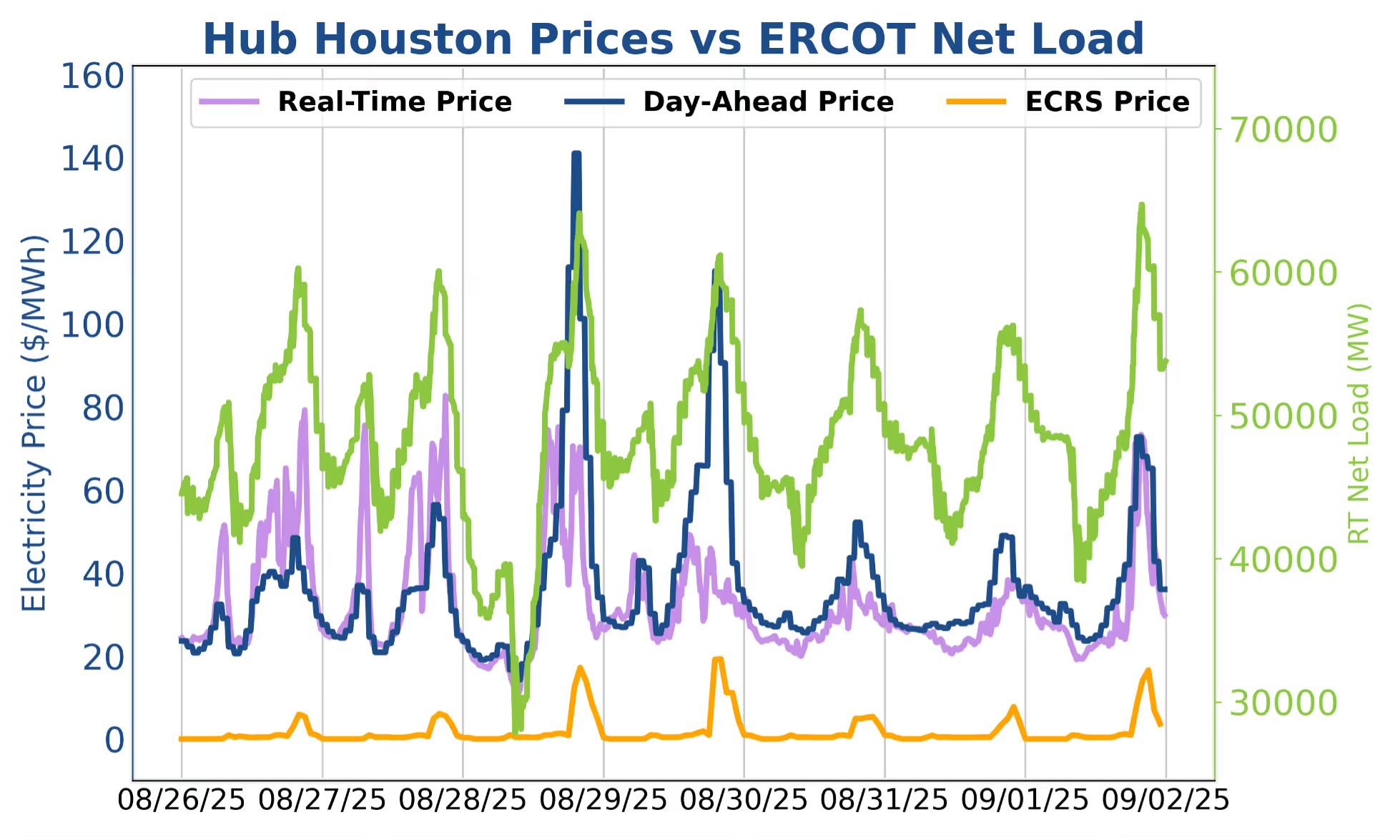

Real-time prices continued to outperform day-ahead prices on the 26th and 27th last week in ERCOT. The DART switch flipped back to favor day-ahead discharge on the 28th and remained that way for the following three days as well. In addition to the DART dynamics, a notable feature of last week’s market conditions in ERCOT was the morning peak prices on the 26th, 27th, and 28th. The 27th saw morning real-time prices breach $80/MWh at many nodes. With all the storage assets concentrating on the evenings, the morning hours are much more sensitive to traditional market tightness. As fall comes into season, operators should keep an eye out for the first substantial morning peaks as there is a good chance they will catch most of the ERCOT storage fleet empty, planning on a midday recharge for evening price action.

Seven-day load forecasting is always a challenging proposition and was on full display in CAISO over the past few days. On the 2nd for example, the seven-day load forecast (pink line) indicated a load peak of 36 GW while the two-day-ahead forecast (orange line) indicated a peak of 39 GW, and the day-ahead forecast (red line) came in at 40 GW. With no solar and very little wind during the peaks, these large gross load forecast swings translate almost 1:1 to net load forecast swings as well. Operators should keep a close eye on how the seven-day forecast evolves to the two-day-ahead and day-ahead each morning to stay on top of rapidly shifting conditions.

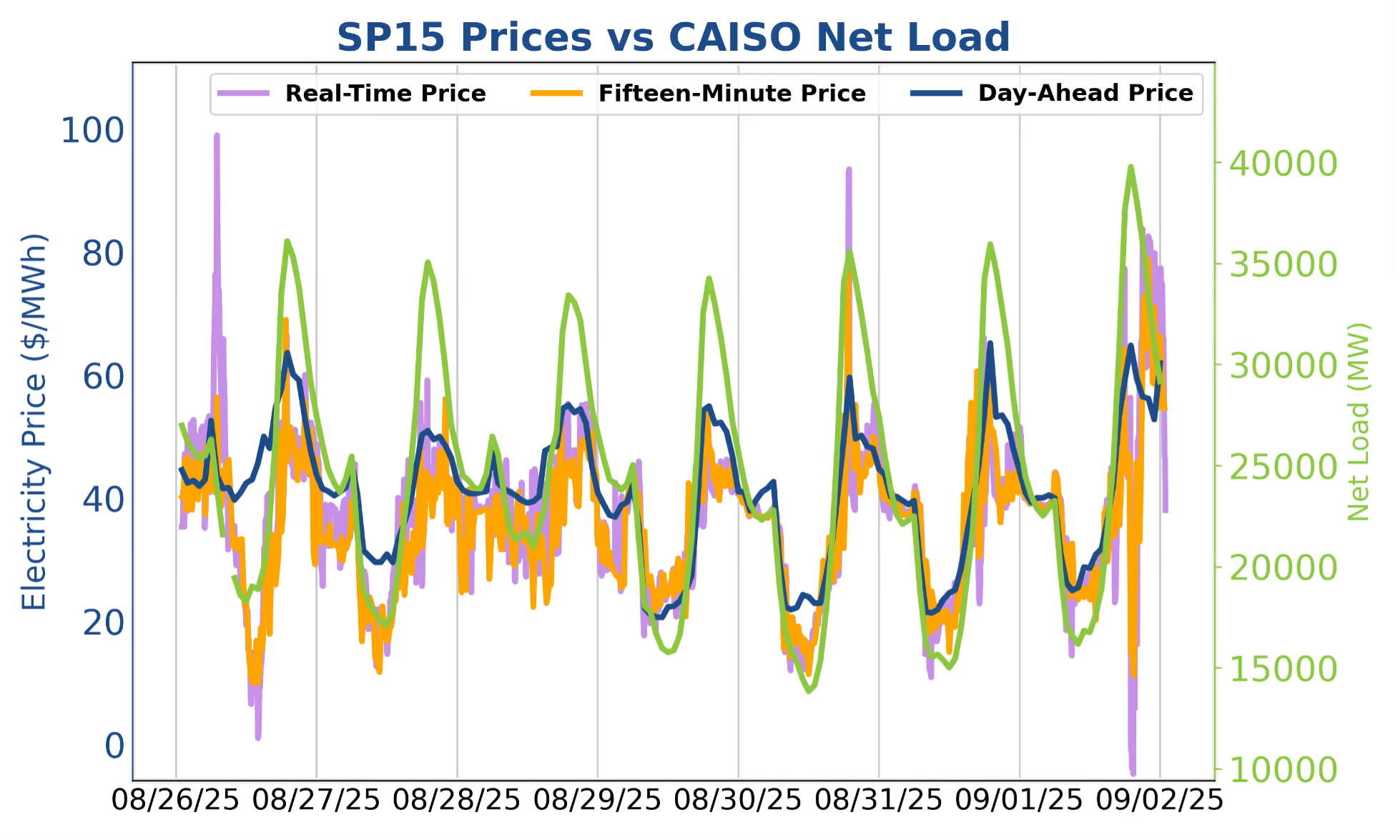

In terms of asset strategy, load forecasts revising higher each day is a sign of real-time favorability (if the higher load trend continues from day-ahead to real-time). The SmartBidder team still recommends targeting day-ahead energy discharge given the macro level favorability trends discussed in previous newsletters. However, discharge offers should be priced economically, close to the day-ahead price forecast. Under the current market regime, not clearing into day-ahead energy, or only clearing a smaller hedged amount, should be taken as an indicator that the market may have cleared day-ahead energy too low and real-time prices will outperform.

Net load peaks took a sharp step up on the 1st of September, peaking at 39.3 GW as real-time prices surged above day-ahead prices in NP15 ($250/MWh) and to a lesser extent in SP15 ($80/MWh). The net load peak on the 1st was one of the strongest of the summer season, but still ~2 GW below a top 10 net load print. Still, this was a good supply stack test for this net load range – a scenario that hadn’t been seen in about a month. The price impact of 8 GW of battery discharge during the peak periods means prices during 40 GW net load peaks will not reach as high as they used to.

Cloudy weather on the 27th and 28th elevated midday charging prices to $30-$40/MWh, producing arbitrage spreads that didn’t even meet many operators VOM costs. Regulation and opportunistic real-time charging and discharging is the recommended SmartBidder approach under these circumstances. The Mt. Shasta strategy should natively perform this way if the VOM is set correctly.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of September 3rd – 9th: Briefly warmer weather in ERCOT will be buffeted by stronger wind production while load forecast variability will remain the key wildcard during CAISO evening peaks.

In ERCOT, gross load levels will be highest on the 4th and 5th, offset by strongly ramping wind production during the day on the 4th. Operators should target day-ahead energy discharge during the peak hours.

In CAISO, while the 7-day load forecast projects calmer conditions returning, that forecast has recently undershot load levels by several GW. Operators should rely on the day-ahead and two-day-ahead forecasts. Heavy day-ahead participation – both energy and economic ancillary services (AS) offers - is the SmartBidder recommended approach.

Wind production will ramp from near-zero levels on the 3rd to 20+ GW levels on the 5th before settling down to 10 GW averages for the 6th. Solar will shift from strong production north of 25 GW through the 4th to less than 20 GW by the 6th. Taken together with the load forecast peak variability, these shifting dynamics will largely conspire to wash out in the net load forecast. The 3rd and 4th will elicit the strongest peaks, up to 66 GW on the 3rd. For storage assets, these days should look familiar to the conditions of the past 3 months. Strategies that worked well throughout the summer should continue working well. Allowing Mt. Blue Sky to optimize across the AS products and energy, knowing that it will focus on day-ahead energy discharge, is the surest bet to maximal revenue capture as TBX strategies are increasingly hard to outperform.

Real-time prices continued to outperform day-ahead prices on the 26th and 27th last week in ERCOT. The DART switch flipped back to favor day-ahead discharge on the 28th and remained that way for the following three days as well. In addition to the DART dynamics, a notable feature of last week’s market conditions in ERCOT was the morning peak prices on the 26th, 27th, and 28th. The 27th saw morning real-time prices breach $80/MWh at many nodes. With all the storage assets concentrating on the evenings, the morning hours are much more sensitive to traditional market tightness. As fall comes into season, operators should keep an eye out for the first substantial morning peaks as there is a good chance they will catch most of the ERCOT storage fleet empty, planning on a midday recharge for evening price action.

Seven-day load forecasting is always a challenging proposition and was on full display in CAISO over the past few days. On the 2nd for example, the seven-day load forecast (pink line) indicated a load peak of 36 GW while the two-day-ahead forecast (orange line) indicated a peak of 39 GW, and the day-ahead forecast (red line) came in at 40 GW. With no solar and very little wind during the peaks, these large gross load forecast swings translate almost 1:1 to net load forecast swings as well. Operators should keep a close eye on how the seven-day forecast evolves to the two-day-ahead and day-ahead each morning to stay on top of rapidly shifting conditions.

In terms of asset strategy, load forecasts revising higher each day is a sign of real-time favorability (if the higher load trend continues from day-ahead to real-time). The SmartBidder team still recommends targeting day-ahead energy discharge given the macro level favorability trends discussed in previous newsletters. However, discharge offers should be priced economically, close to the day-ahead price forecast. Under the current market regime, not clearing into day-ahead energy, or only clearing a smaller hedged amount, should be taken as an indicator that the market may have cleared day-ahead energy too low and real-time prices will outperform.

Net load peaks took a sharp step up on the 1st of September, peaking at 39.3 GW as real-time prices surged above day-ahead prices in NP15 ($250/MWh) and to a lesser extent in SP15 ($80/MWh). The net load peak on the 1st was one of the strongest of the summer season, but still ~2 GW below a top 10 net load print. Still, this was a good supply stack test for this net load range – a scenario that hadn’t been seen in about a month. The price impact of 8 GW of battery discharge during the peak periods means prices during 40 GW net load peaks will not reach as high as they used to.

Cloudy weather on the 27th and 28th elevated midday charging prices to $30-$40/MWh, producing arbitrage spreads that didn’t even meet many operators VOM costs. Regulation and opportunistic real-time charging and discharging is the recommended SmartBidder approach under these circumstances. The Mt. Shasta strategy should natively perform this way if the VOM is set correctly.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)