Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

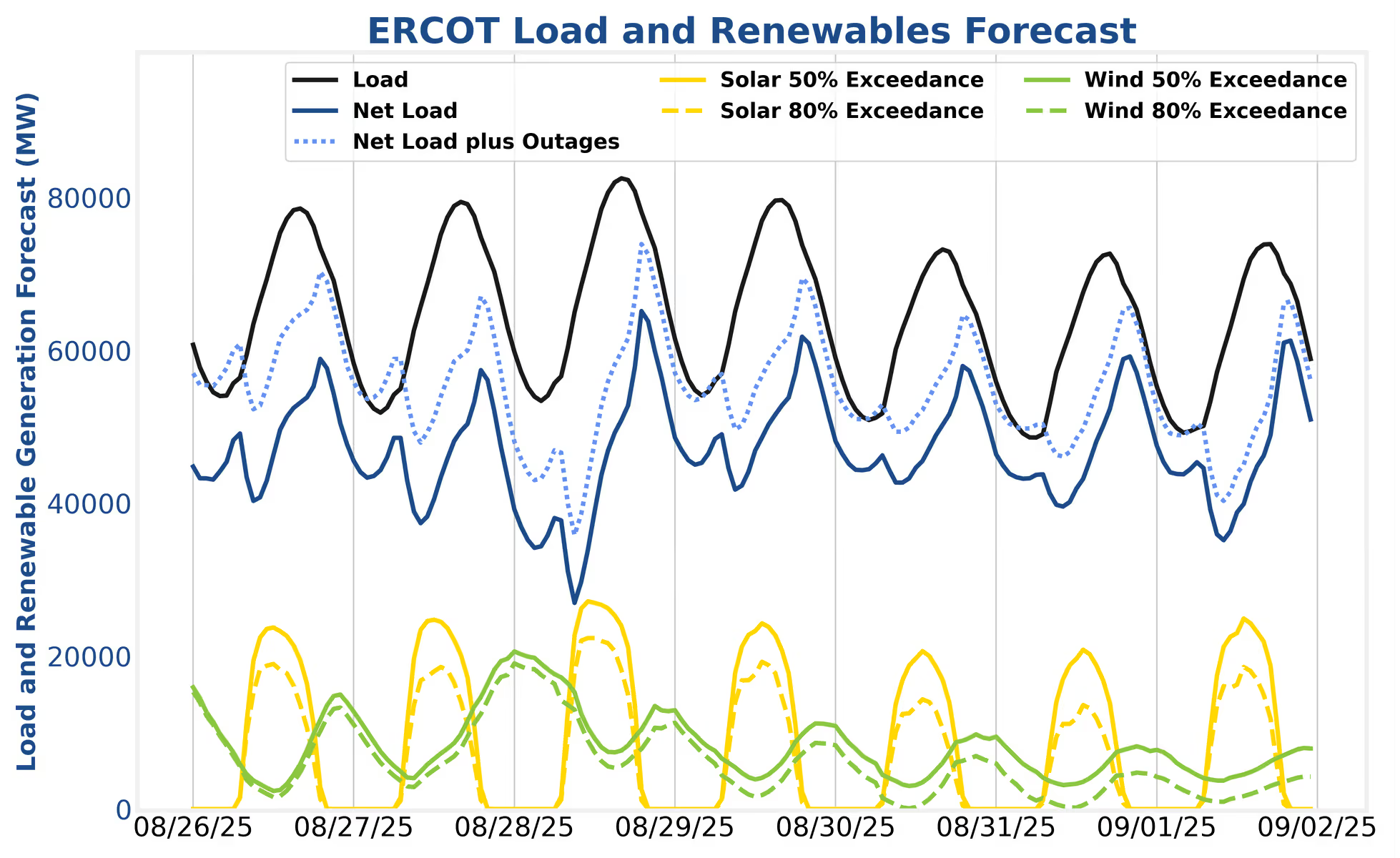

For the week of August 27th – September 2nd: The month of August will close with meager market movement in both ERCOT and CAISO due to cooler temps across the country.

In ERCOT, net load should push above 60 GW on the 28th due to higher load but will otherwise remain muted. Operators should focus on a mixture of day-ahead (DA) and real-time (RT) energy arbitrage after the slight favorability of real-time energy prices relative to day-ahead in the past week.

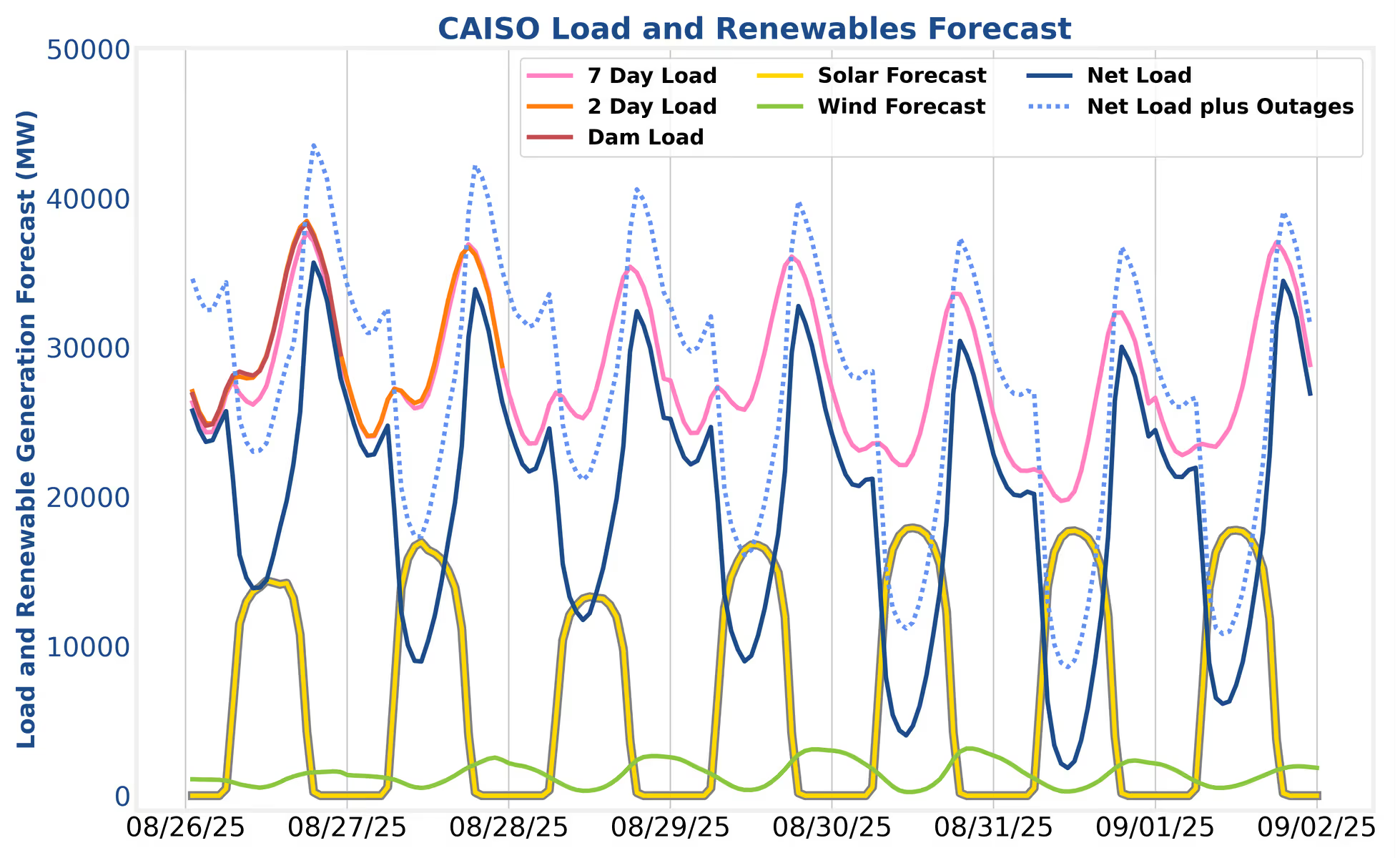

In CAISO, after a brief bright spot last week, market conditions will return to quieter volatility this week. Operators should continue to target day-ahead energy arbitrage along with regulation commitments around the edges where they have appropriate SoC/headroom.

Cool temps will usher in September and Texas high temperatures will struggle to break 80 degrees Fahrenheit on many days next week. This will not be kind to energy or ancillary services (AS) prices, and operators should not expect much from the day-ahead market. The SmartBidder team still recommends targeting day-ahead energy and AS positions, but operators should not be concerned about leaving room for real-time energy upside if day-ahead energy prices clear extremely low. The Mount Blue Sky strategy with the day-ahead energy offers priced economically relative to real-time energy, coupled with DART spread probability expectations is a nice way to opportunistically hedge in these conditions. As the sun sets earlier in the evening, a late summer heat wave could still bring big price spikes, but this is not the week.

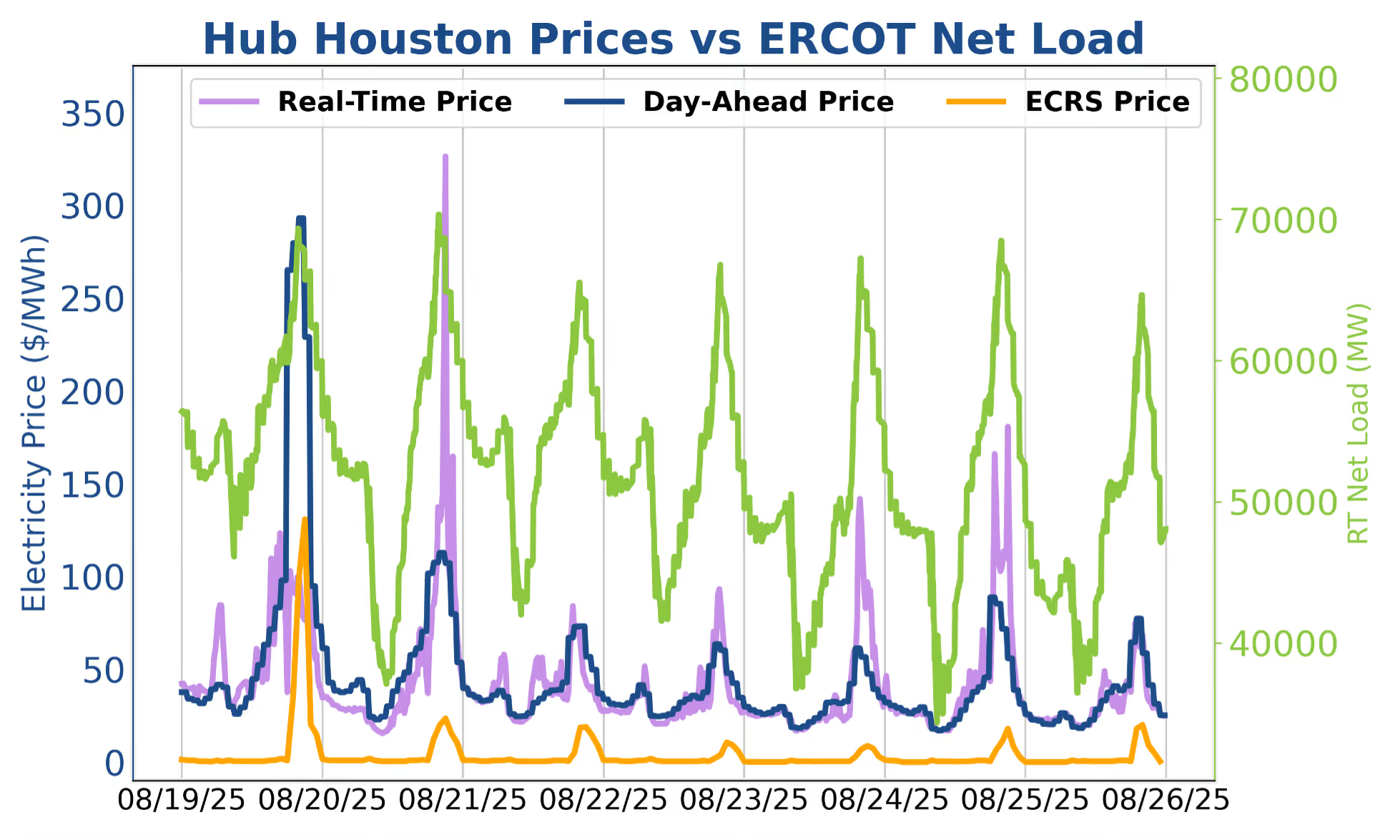

While the day-ahead energy prices were by far the most lucrative product during the higher net load peaking days of the past weeks, real-time energy prices did offer a little improvement beginning on the 20th. Even so, it is important to account for the additional difficulty in monetizing the real-time energy price spike on the 20th vs the day-ahead energy price peak on the 19th. On the 19th, HE 19, 20, and 21 all provided relatively equal value in day-ahead energy. On the 20th, the real-time energy price spike only lasted for about 30 minutes (around the start of HE22) of the roughly four-hour peak window, based on how the day-ahead energy prices cleared. Operators who correctly chose to target real-time energy still missed the additional revenue opportunity because they discharged too early. The key takeaway here is that the day-ahead energy market has not only provided high prices over the past few weeks, but it has also offered much easier revenue capture due to the inherently easier forecasting challenge.

Net load peaks in CAISO will simmer down as temperatures cool off. Charging dynamics should be more interesting on the 28th as solar production is ~5 GW off typical peak levels during the middle of the day. Arbitrage spreads on the 28th will likely be poor, similar to spreads on the 26th. Solar production will fully return for the weekend, and operators should begin to look for September heat waves to provide large revenue opportunities. For the remainder of this week, the SmartBidder team recommends day-ahead energy discharge during the evening peaks and heavy regulation participation on the 28th to offset poorer arbitrage conditions.

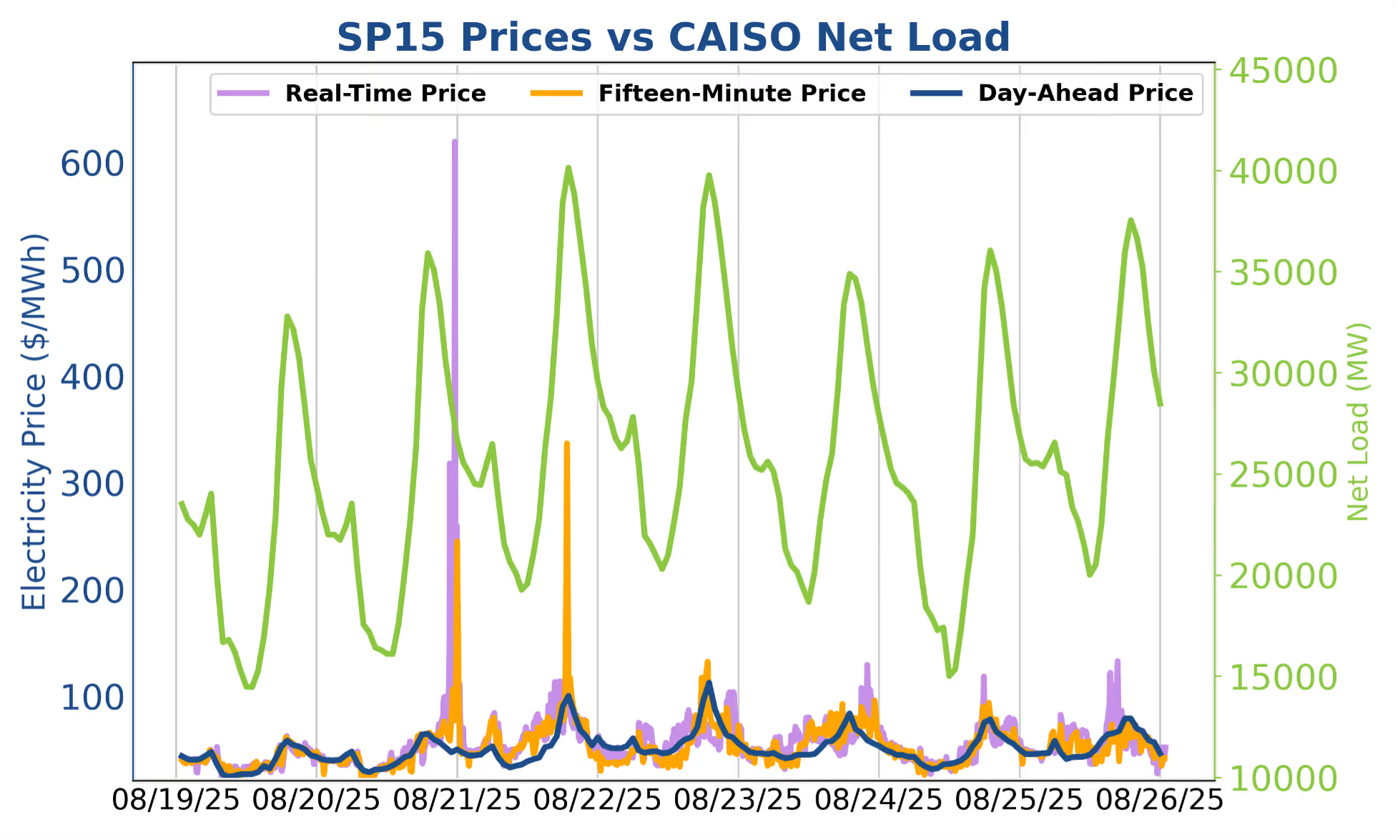

CAISO gave us a taste of volatility last week, with evening DA prices on the 21st and 22nd eclipsing triple digits for the first time this year. Despite the strong DA prices, real-time remained relatively muted, with only a few short-lived 15-minute intervals clearing substantially above their DA counterparts. The fifteen-minute market spiked around midnight on the 21st to $200+ for a single interval, and again later that day during HE19, hitting $300+ for one 15-minute period. DA prices during those windows were approximately $50/MWh and $90/MWh, respectively. The midnight spike was difficult for battery operators to capture without near-perfect foresight, given it occurred well after the evening peak. However, operators not fully committed in DA energy on the 21st had the potential to realize short-lived but substantial returns.

As expected during scarcity conditions, Regulation Up and Spin were the highest-priced ancillary products during the evening peak hours, both reaching $50/MWh during HE20 on the 22nd. Operators should continue to bid into ancillaries opportunistically relative to DA energy, maximizing ancillary participation during peak conditions if the opportunity cost of ancillaries exceeds the expected benefit of discharging during peak hours.

The remainder of the week tracked with prior trends, as real-time arbitrage opportunities remained limited. Summer conditions continue to drive higher load and higher prices, but without curtailment pricing to capture, the advantage of charging in real-time is limited. Evening real-time spikes in the fifteen-minute market remain fleeting, frequently followed by sharp corrections in the next interval. Heavy day-ahead participation remains the recommended approach.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of August 27th – September 2nd: The month of August will close with meager market movement in both ERCOT and CAISO due to cooler temps across the country.

In ERCOT, net load should push above 60 GW on the 28th due to higher load but will otherwise remain muted. Operators should focus on a mixture of day-ahead (DA) and real-time (RT) energy arbitrage after the slight favorability of real-time energy prices relative to day-ahead in the past week.

In CAISO, after a brief bright spot last week, market conditions will return to quieter volatility this week. Operators should continue to target day-ahead energy arbitrage along with regulation commitments around the edges where they have appropriate SoC/headroom.

Cool temps will usher in September and Texas high temperatures will struggle to break 80 degrees Fahrenheit on many days next week. This will not be kind to energy or ancillary services (AS) prices, and operators should not expect much from the day-ahead market. The SmartBidder team still recommends targeting day-ahead energy and AS positions, but operators should not be concerned about leaving room for real-time energy upside if day-ahead energy prices clear extremely low. The Mount Blue Sky strategy with the day-ahead energy offers priced economically relative to real-time energy, coupled with DART spread probability expectations is a nice way to opportunistically hedge in these conditions. As the sun sets earlier in the evening, a late summer heat wave could still bring big price spikes, but this is not the week.

While the day-ahead energy prices were by far the most lucrative product during the higher net load peaking days of the past weeks, real-time energy prices did offer a little improvement beginning on the 20th. Even so, it is important to account for the additional difficulty in monetizing the real-time energy price spike on the 20th vs the day-ahead energy price peak on the 19th. On the 19th, HE 19, 20, and 21 all provided relatively equal value in day-ahead energy. On the 20th, the real-time energy price spike only lasted for about 30 minutes (around the start of HE22) of the roughly four-hour peak window, based on how the day-ahead energy prices cleared. Operators who correctly chose to target real-time energy still missed the additional revenue opportunity because they discharged too early. The key takeaway here is that the day-ahead energy market has not only provided high prices over the past few weeks, but it has also offered much easier revenue capture due to the inherently easier forecasting challenge.

Net load peaks in CAISO will simmer down as temperatures cool off. Charging dynamics should be more interesting on the 28th as solar production is ~5 GW off typical peak levels during the middle of the day. Arbitrage spreads on the 28th will likely be poor, similar to spreads on the 26th. Solar production will fully return for the weekend, and operators should begin to look for September heat waves to provide large revenue opportunities. For the remainder of this week, the SmartBidder team recommends day-ahead energy discharge during the evening peaks and heavy regulation participation on the 28th to offset poorer arbitrage conditions.

CAISO gave us a taste of volatility last week, with evening DA prices on the 21st and 22nd eclipsing triple digits for the first time this year. Despite the strong DA prices, real-time remained relatively muted, with only a few short-lived 15-minute intervals clearing substantially above their DA counterparts. The fifteen-minute market spiked around midnight on the 21st to $200+ for a single interval, and again later that day during HE19, hitting $300+ for one 15-minute period. DA prices during those windows were approximately $50/MWh and $90/MWh, respectively. The midnight spike was difficult for battery operators to capture without near-perfect foresight, given it occurred well after the evening peak. However, operators not fully committed in DA energy on the 21st had the potential to realize short-lived but substantial returns.

As expected during scarcity conditions, Regulation Up and Spin were the highest-priced ancillary products during the evening peak hours, both reaching $50/MWh during HE20 on the 22nd. Operators should continue to bid into ancillaries opportunistically relative to DA energy, maximizing ancillary participation during peak conditions if the opportunity cost of ancillaries exceeds the expected benefit of discharging during peak hours.

The remainder of the week tracked with prior trends, as real-time arbitrage opportunities remained limited. Summer conditions continue to drive higher load and higher prices, but without curtailment pricing to capture, the advantage of charging in real-time is limited. Evening real-time spikes in the fifteen-minute market remain fleeting, frequently followed by sharp corrections in the next interval. Heavy day-ahead participation remains the recommended approach.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)