Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Massive structural changes to both supply and demand are creating unprecedented conditions in US electricity markets. Nowhere is this dynamic more pronounced than in the PJM capacity market, which has gone from historically low prices just two years ago to record-high prices at the most recent capacity auction in July 2025. While high capacity prices should provide the signal to support new entry, generators appear hesitant to enter due to stranded asset risk, low and uncertain accreditation, and shifting market rules. With capacity prices projected to stay high indefinitely, much remains uncertain in PJM, and capacity costs risk breaking the market.

In a recent webinar previewing Ascend's latest PJM energy market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss the implications of soaring capacity prices, the growing importance of performing under scarcity conditions, the impact of state/federal policies on the market, and opportunities for meeting demand growth.

During most of the past two decades, PJM experienced oversupply conditions, load declines, and low rates for electricity consumers. However, it was evident that change was coming. Just two years ago, low capacity prices triggered concern among key PJM stakeholders about thermal retirements and looming resource adequacy problems. It was clear that higher capacity prices would be needed to incentivize new unit entry and deter retirements, especially in the face of potentially immense demand growth.

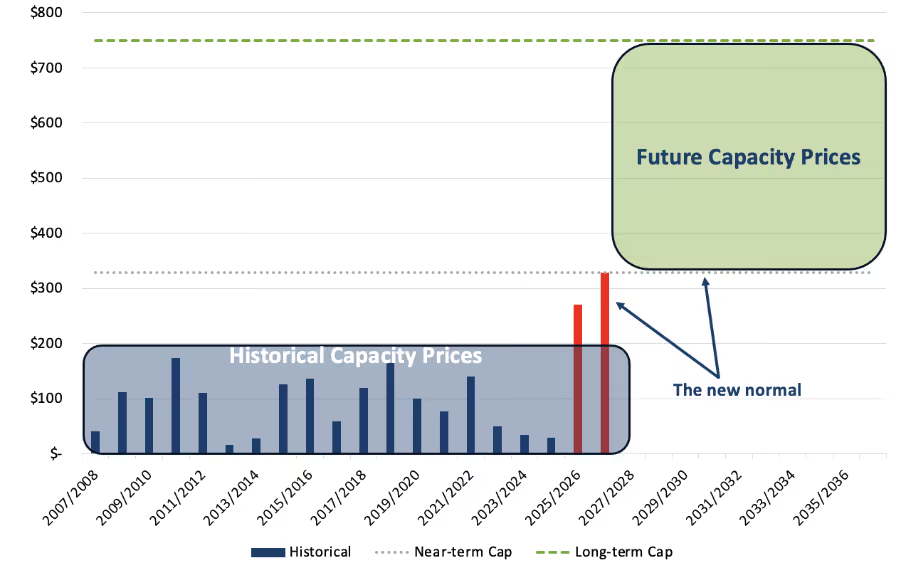

As load growth materialized in PJM’s forecasts, prices skyrocketed to record highs for the 2025/2026 base residual auction (BRA) in 2024, as shown in Figure 1. Then prices went even higher in July 2025 for the 2026/2027 BRA. While these results represented predictable outcomes based on market conditions, they generated negative responses from multiple stakeholders, including policymakers and ratepayers. While high prices were necessary for incentivizing new generation in PJM, stakeholders have shown a very limited appetite for paying for it.

In response to pressure from ratepayer stakeholders, including state policymakers, PJM made a number of capacity market changes, including the implementation of a price cap. However, these changes exacerbated the problem by undermining market confidence and weakening investment signals for new entry. PJM currently has more than 45 GW of generation with interconnection agreements, but very little is getting built.

At the same time, growing winter reliability risks pose a major problem for resource accreditation – and capacity prices. While solar generation and storage are well-suited to help manage summer peaks, long-duration winter peaks present an increasingly significant problem in terms of resource accreditation. Storage accreditation declines as storage penetration grows, and marginal ELCC accreditation accelerates the decline. Amplified forced outage and fuel disruption risks during cold weather also pose a problem for thermal accreditation, especially gas. Even without winter peaking, winter reliability will become a more binding constraint on resource adequacy than summer peaks as solar buildout grows.

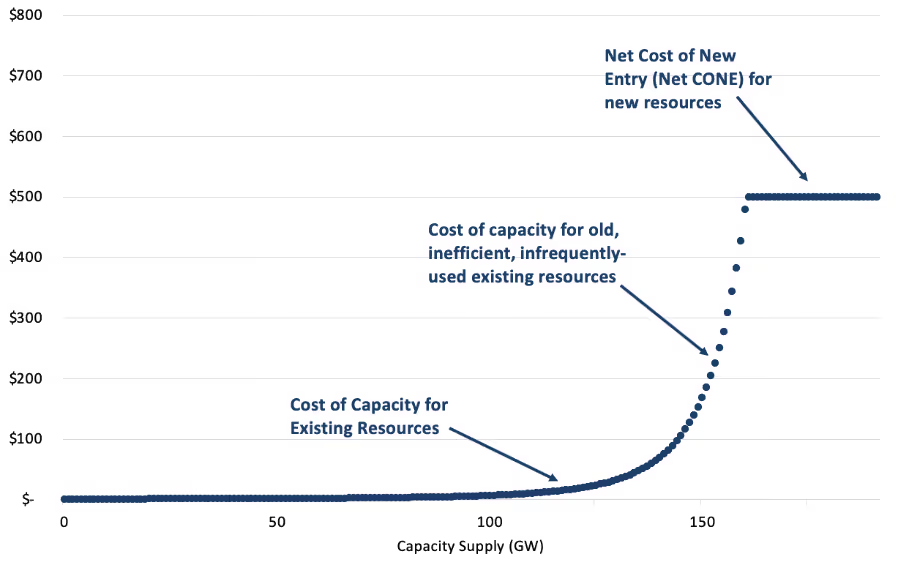

In the context of high, sustained capacity prices, another critical problem emerges: capacity markets break once the marginal cost of capacity diverges from the typical cost of capacity. As the example capacity supply curve in Figure 2 illustrates, building new capacity is more expensive than the cost of keeping existing capacity running and sets an upper limit for capacity prices. Demand growth will require new capacity to be built, causing capacity prices to be set by new unit entry. New unit entry will need to cover its cost of entry every year for its entire project life.

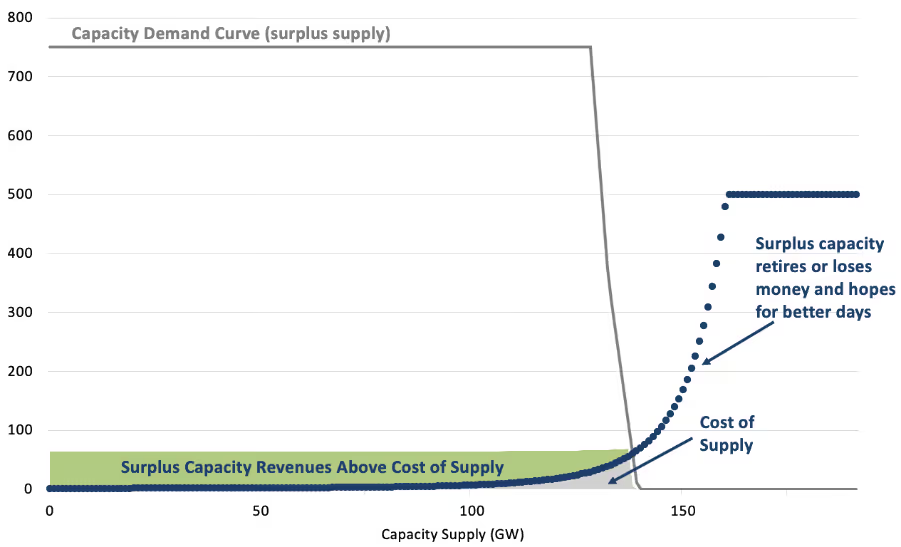

A capacity market works when the majority of the supply stack has a similar cost of capacity to the marginal unit, as shown in Figure 3. Capacity markets provide a market-clearing-price to all generators, regardless of their costs. Lower cost capacity resources earn extra revenues when capacity prices are set by higher cost units. Excess capacity either retires or operates at a loss while hoping for better future conditions.

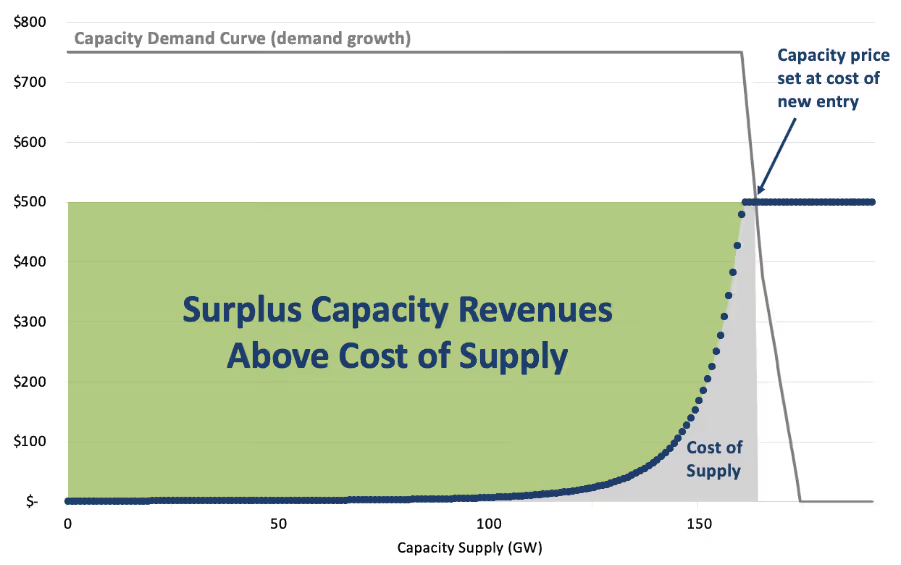

When load growth hits capacity markets, however, the entire stack gets paid the price for new entry, amplifying the total capacity market costs, as shown in Figure 4. When structural change causes capacity markets to clear at the cost of new entry, this cost flows across the entire supply stack, regardless of the amount of new entry needed. Very high capacity costs – on the order of an additional $25 billion – can be incurred just to compensate a small quantity of new entry.

So what to do? One option is to break up the market and re-regulate it. In so doing, regulated utilities would only receive cost recovery (plus rate of return), eliminating the capacity cost uplift that flows in capacity markets due to the market clearing price. However, a return to regulation would come at the cost of re-imposing investment risks on captive ratepayers rather than investors. It would also require destroying PJM in its current form.

Another, perhaps better, option involves subsidizing or procuring bilateral contracts with new entry so as to avoid extreme capacity market costs without dissolving the market. Subsidies or bilateral contracts for new entry are the only way to avoid exploding capacity costs, particularly for states that want to transition to clean supply and don’t want to provide a windfall to incumbent fossil generation.

These options are not just hypothetical, either. States are publicly considering either leaving PJM altogether or moving to secure their own state power supplies through subsidies and procurement.1

Storage is well-positioned as a clear lowest-cost capacity resource for the next decade or so while the ITC remains in place and gas turbine prices remain inflated. While accreditation hurts storage in PJM, gas accreditation has been significantly reduced, as well. Highly inflated costs for new gas turbines also create major investment risks for new gas, while a 30% ITC plus 10% energy community adder (common in PJM) make batteries a much lower cost capacity resource. Additionally, near-term thermal investment will be highly risky, as it will get outcompeted by lower-cost future thermal capacity.

Meanwhile, with capacity prices – and value – growing, the ability to perform during scarcity conditions will grow in importance. Scarcity pricing and pay-for-performance penalties will become increasingly consequential in a world of high capacity prices and low energy prices. With conservative resource accreditation, PJM is likely to be long most times and most years, and only become scarce when there is a perfect storm of factors: high load, high thermal outages, low renewable generation, and empty batteries. Capacity revenues will depend on being able to be available when other generation resources are not, and the consequences of not doing so will grow.

With energy cheap and capacity expensive, the value for shifting loads is also higher than ever. Load serving entities should do everything in their power, including retail rate design, efficiency programs, and demand response, to incentivize reduced consumption during peak conditions.

Access the full webinar recording, which offers guidance for where, what, and when to add new capacity resources in PJM. The webinar also offers insights related to emissions abatement opportunities, projected renewable energy buildout, and updated energy demand forecasts.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Massive structural changes to both supply and demand are creating unprecedented conditions in US electricity markets. Nowhere is this dynamic more pronounced than in the PJM capacity market, which has gone from historically low prices just two years ago to record-high prices at the most recent capacity auction in July 2025. While high capacity prices should provide the signal to support new entry, generators appear hesitant to enter due to stranded asset risk, low and uncertain accreditation, and shifting market rules. With capacity prices projected to stay high indefinitely, much remains uncertain in PJM, and capacity costs risk breaking the market.

In a recent webinar previewing Ascend's latest PJM energy market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss the implications of soaring capacity prices, the growing importance of performing under scarcity conditions, the impact of state/federal policies on the market, and opportunities for meeting demand growth.

During most of the past two decades, PJM experienced oversupply conditions, load declines, and low rates for electricity consumers. However, it was evident that change was coming. Just two years ago, low capacity prices triggered concern among key PJM stakeholders about thermal retirements and looming resource adequacy problems. It was clear that higher capacity prices would be needed to incentivize new unit entry and deter retirements, especially in the face of potentially immense demand growth.

As load growth materialized in PJM’s forecasts, prices skyrocketed to record highs for the 2025/2026 base residual auction (BRA) in 2024, as shown in Figure 1. Then prices went even higher in July 2025 for the 2026/2027 BRA. While these results represented predictable outcomes based on market conditions, they generated negative responses from multiple stakeholders, including policymakers and ratepayers. While high prices were necessary for incentivizing new generation in PJM, stakeholders have shown a very limited appetite for paying for it.

In response to pressure from ratepayer stakeholders, including state policymakers, PJM made a number of capacity market changes, including the implementation of a price cap. However, these changes exacerbated the problem by undermining market confidence and weakening investment signals for new entry. PJM currently has more than 45 GW of generation with interconnection agreements, but very little is getting built.

At the same time, growing winter reliability risks pose a major problem for resource accreditation – and capacity prices. While solar generation and storage are well-suited to help manage summer peaks, long-duration winter peaks present an increasingly significant problem in terms of resource accreditation. Storage accreditation declines as storage penetration grows, and marginal ELCC accreditation accelerates the decline. Amplified forced outage and fuel disruption risks during cold weather also pose a problem for thermal accreditation, especially gas. Even without winter peaking, winter reliability will become a more binding constraint on resource adequacy than summer peaks as solar buildout grows.

In the context of high, sustained capacity prices, another critical problem emerges: capacity markets break once the marginal cost of capacity diverges from the typical cost of capacity. As the example capacity supply curve in Figure 2 illustrates, building new capacity is more expensive than the cost of keeping existing capacity running and sets an upper limit for capacity prices. Demand growth will require new capacity to be built, causing capacity prices to be set by new unit entry. New unit entry will need to cover its cost of entry every year for its entire project life.

A capacity market works when the majority of the supply stack has a similar cost of capacity to the marginal unit, as shown in Figure 3. Capacity markets provide a market-clearing-price to all generators, regardless of their costs. Lower cost capacity resources earn extra revenues when capacity prices are set by higher cost units. Excess capacity either retires or operates at a loss while hoping for better future conditions.

When load growth hits capacity markets, however, the entire stack gets paid the price for new entry, amplifying the total capacity market costs, as shown in Figure 4. When structural change causes capacity markets to clear at the cost of new entry, this cost flows across the entire supply stack, regardless of the amount of new entry needed. Very high capacity costs – on the order of an additional $25 billion – can be incurred just to compensate a small quantity of new entry.

So what to do? One option is to break up the market and re-regulate it. In so doing, regulated utilities would only receive cost recovery (plus rate of return), eliminating the capacity cost uplift that flows in capacity markets due to the market clearing price. However, a return to regulation would come at the cost of re-imposing investment risks on captive ratepayers rather than investors. It would also require destroying PJM in its current form.

Another, perhaps better, option involves subsidizing or procuring bilateral contracts with new entry so as to avoid extreme capacity market costs without dissolving the market. Subsidies or bilateral contracts for new entry are the only way to avoid exploding capacity costs, particularly for states that want to transition to clean supply and don’t want to provide a windfall to incumbent fossil generation.

These options are not just hypothetical, either. States are publicly considering either leaving PJM altogether or moving to secure their own state power supplies through subsidies and procurement.1

Storage is well-positioned as a clear lowest-cost capacity resource for the next decade or so while the ITC remains in place and gas turbine prices remain inflated. While accreditation hurts storage in PJM, gas accreditation has been significantly reduced, as well. Highly inflated costs for new gas turbines also create major investment risks for new gas, while a 30% ITC plus 10% energy community adder (common in PJM) make batteries a much lower cost capacity resource. Additionally, near-term thermal investment will be highly risky, as it will get outcompeted by lower-cost future thermal capacity.

Meanwhile, with capacity prices – and value – growing, the ability to perform during scarcity conditions will grow in importance. Scarcity pricing and pay-for-performance penalties will become increasingly consequential in a world of high capacity prices and low energy prices. With conservative resource accreditation, PJM is likely to be long most times and most years, and only become scarce when there is a perfect storm of factors: high load, high thermal outages, low renewable generation, and empty batteries. Capacity revenues will depend on being able to be available when other generation resources are not, and the consequences of not doing so will grow.

With energy cheap and capacity expensive, the value for shifting loads is also higher than ever. Load serving entities should do everything in their power, including retail rate design, efficiency programs, and demand response, to incentivize reduced consumption during peak conditions.

Access the full webinar recording, which offers guidance for where, what, and when to add new capacity resources in PJM. The webinar also offers insights related to emissions abatement opportunities, projected renewable energy buildout, and updated energy demand forecasts.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)