Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

For the week of August 20th – 26th: Elevated peaks will make Aug 20-21 in ERCOT and Aug 22 in CAISO the days to watch out for as high summer temperatures take over.

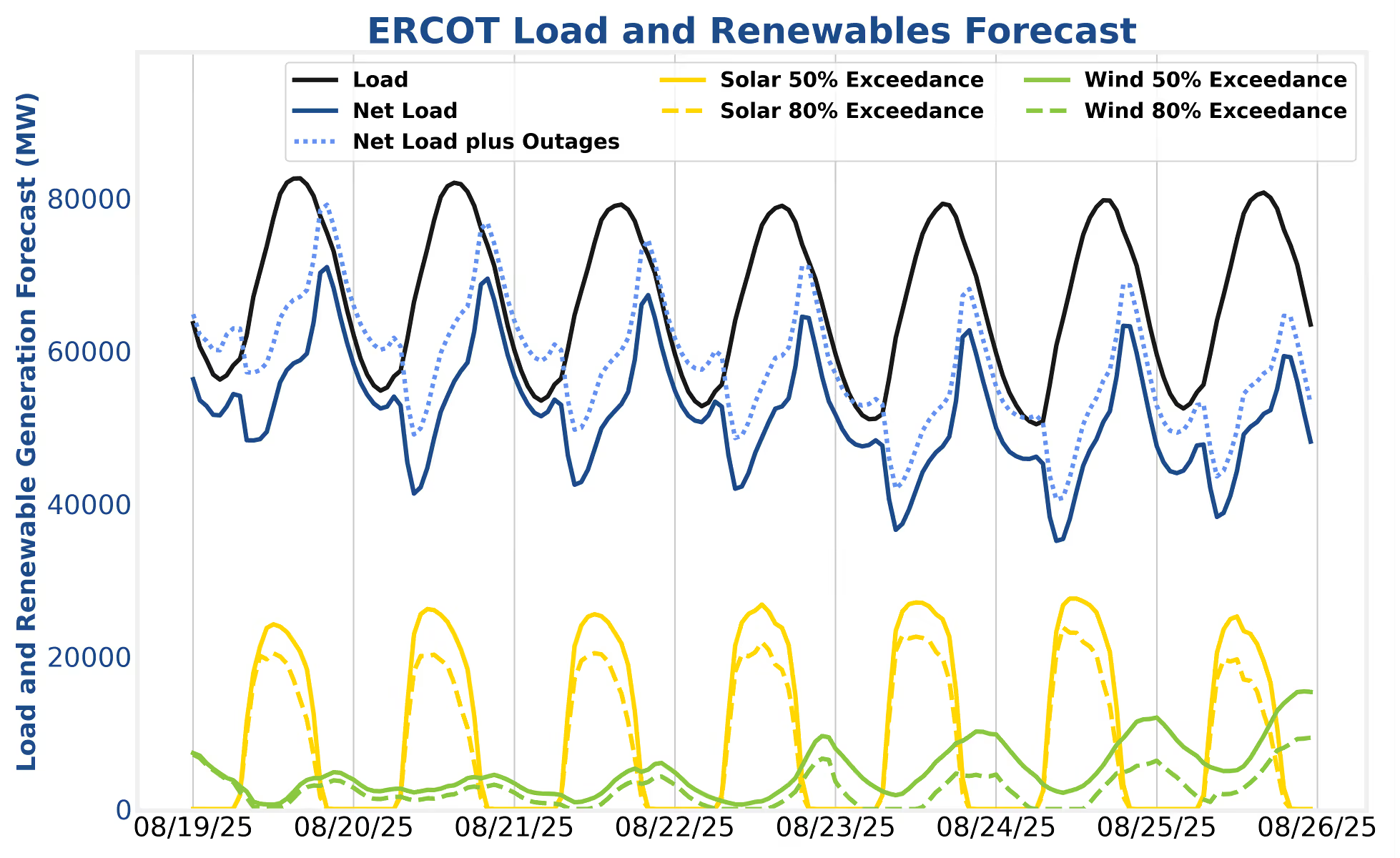

In ERCOT, high system loads and modest wind will keep net loads above 70 GW, with sharp evening ramps through the week. Solar variability on Aug 20–21 could push peaks even higher and drive real-time price volatility.

In CAISO, net load peaks will be elevated this week, likely driving higher evening prices. A day-ahead heavy strategy remains optimal, as added storage capacity and lower net loads should keep grid conditions less constrained than last year’s peak events.

High system loads combined with modest wind production are projected to keep net load peaks consistently above 70 GW through the upcoming week. Strong solar output, paired with relatively weak wind in the first half of the week will drive sharp evening ramps as solar fades each day. The 20th and 21st stand out with unusually high variance in the solar forecast—severe weather across Texas could significantly reduce real-time (RT) solar generation, pushing net load peaks even higher and creating elevated price volatility in RT markets.

Following last week’s trend, heavy day-ahead (DA) participation remains the recommended strategy, with some room reserved for real-time activity on the 20th and 21st to capture volatility. SmartBidder’s Mt. Blue Sky strategy will pick up on these dynamics and hedge accordingly in the day-ahead market while positioning for evening scarcity risks. Talk with your analyst about tuning Mt. Blue Sky to your risk tolerance if you want to use this window to fine-tune performance or expand capabilities.

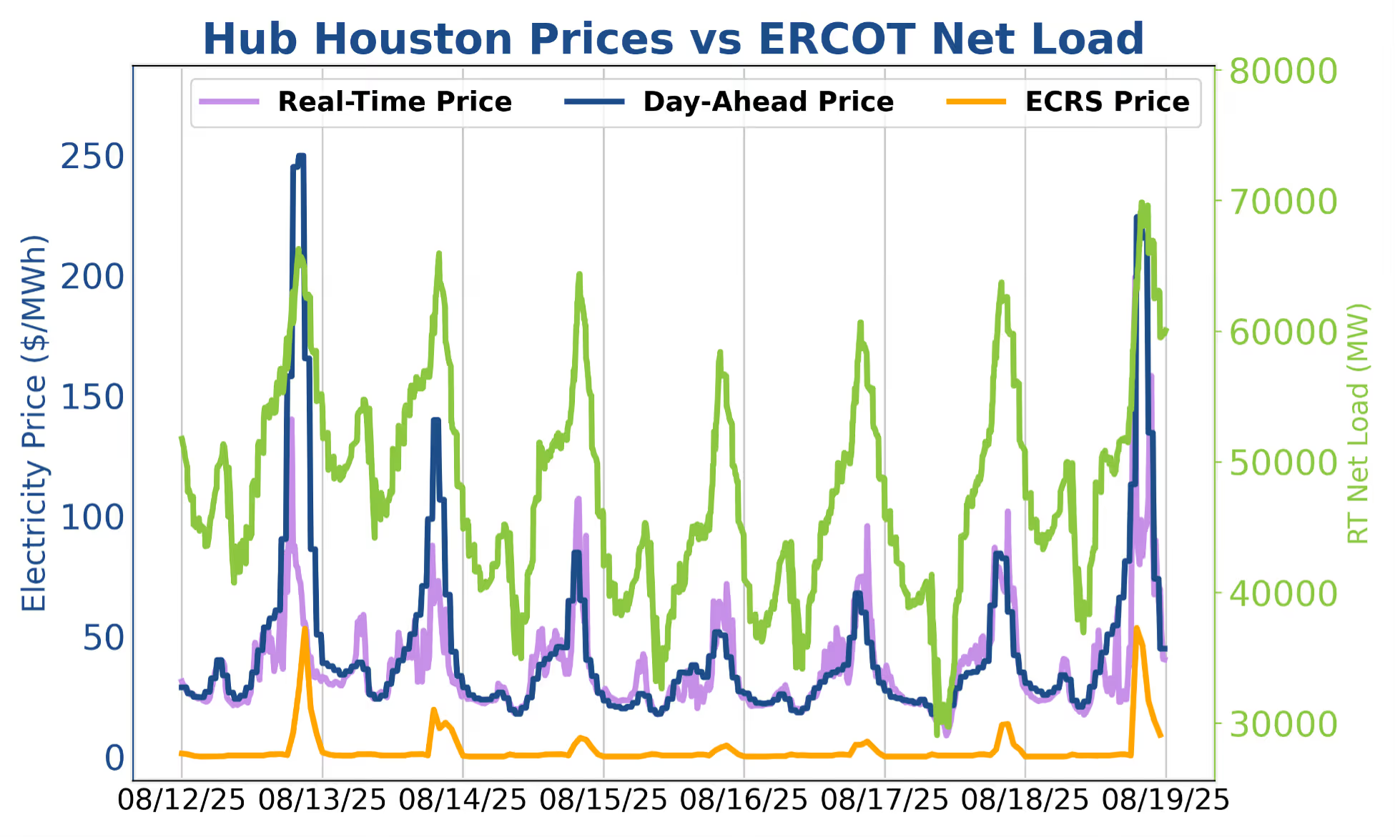

At most ERCOT nodes last week, day-ahead energy discharge opportunities far outpaced real-time on the lucrative 12th and 18th. While some negative DART spreads emerged on the 14th and 15th, SmartBidder’s opportunity cost-based bidding framework effectively preserved flexibility for real-time exposure.

We’re also seeing a growing pattern of muted real-time prices during the two-peak day-ahead hours on high-priced DA days. Not a hard rule, but increasingly common: real-time prices tend to swing before and after the DA peaks, with a noticeable trough in between—especially evident on the 18th. This is a pattern to continue to look out for when considering market participation. Talk to your analyst about exploring how to balance DA and RT exposure.

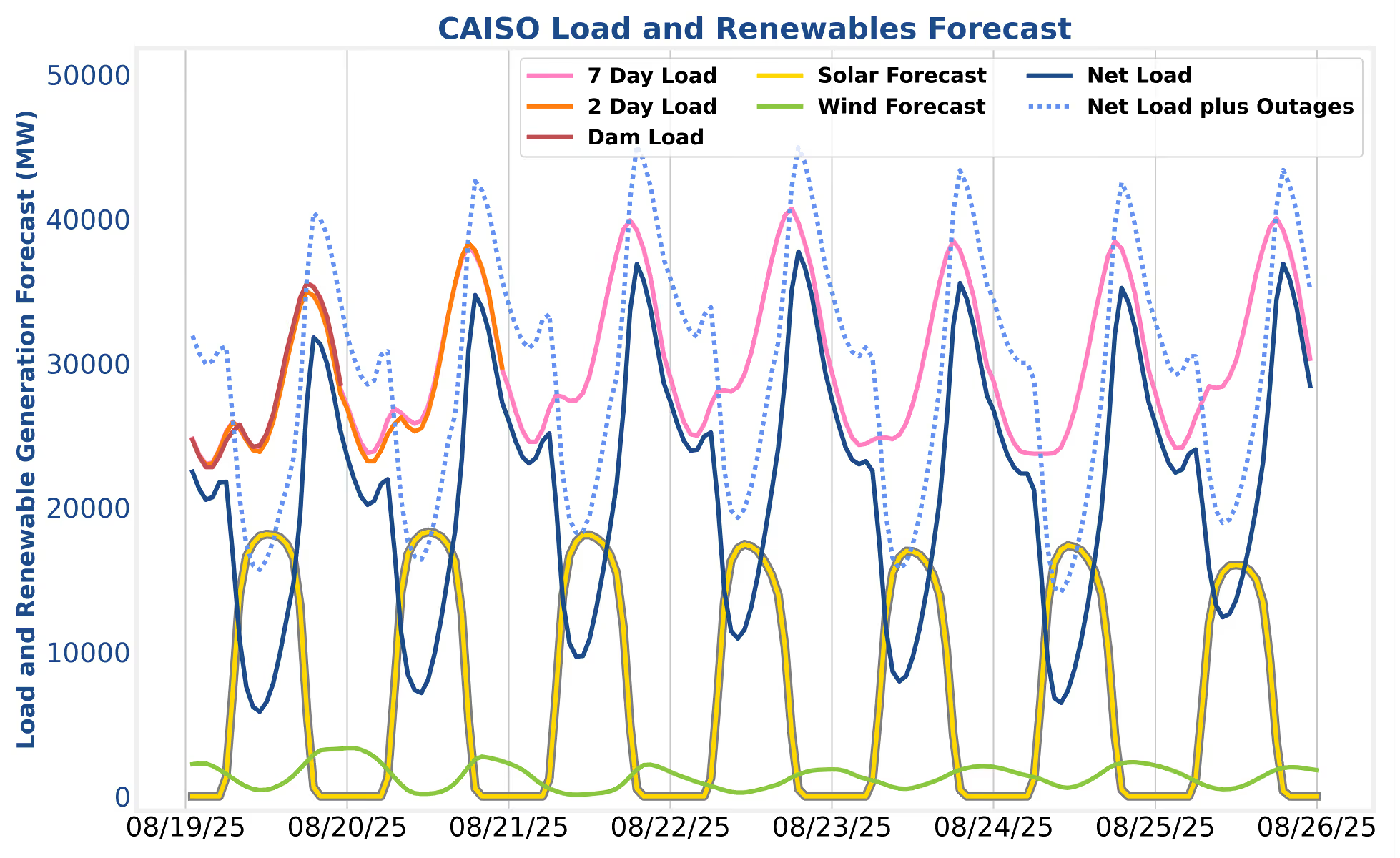

This week will serve as an important test of the updated CAISO grid. Net loads are projected to peak around 37.7 GW on the 22nd, with elevated levels above 35 GW persisting throughout the week. For comparison, the largest net load of 2024 was ~43 GW on 9/5/24. While this week’s peak may be the highest of 2025 to-date, it remains about 2.5 GW below the 40+ GW levels reached last year that drove more extreme conditions. Importantly, there is also roughly 3 GW of additional storage online compared to last summer. This added capacity is expected to mute scarcity conditions by reducing the likelihood that more expensive imports or gas plants set prices when there is a misalignment between forecasted and actual renewable generation. However, elevated loads at this time of year still have the potential to drive elevated prices. Hub-level day-ahead prices could reach triple digits this week, while continued over-procurement in the day-ahead market and added storage capacity may limit substantial real-time blowouts. The recommended approach remains to participate heavily in the day-ahead market.

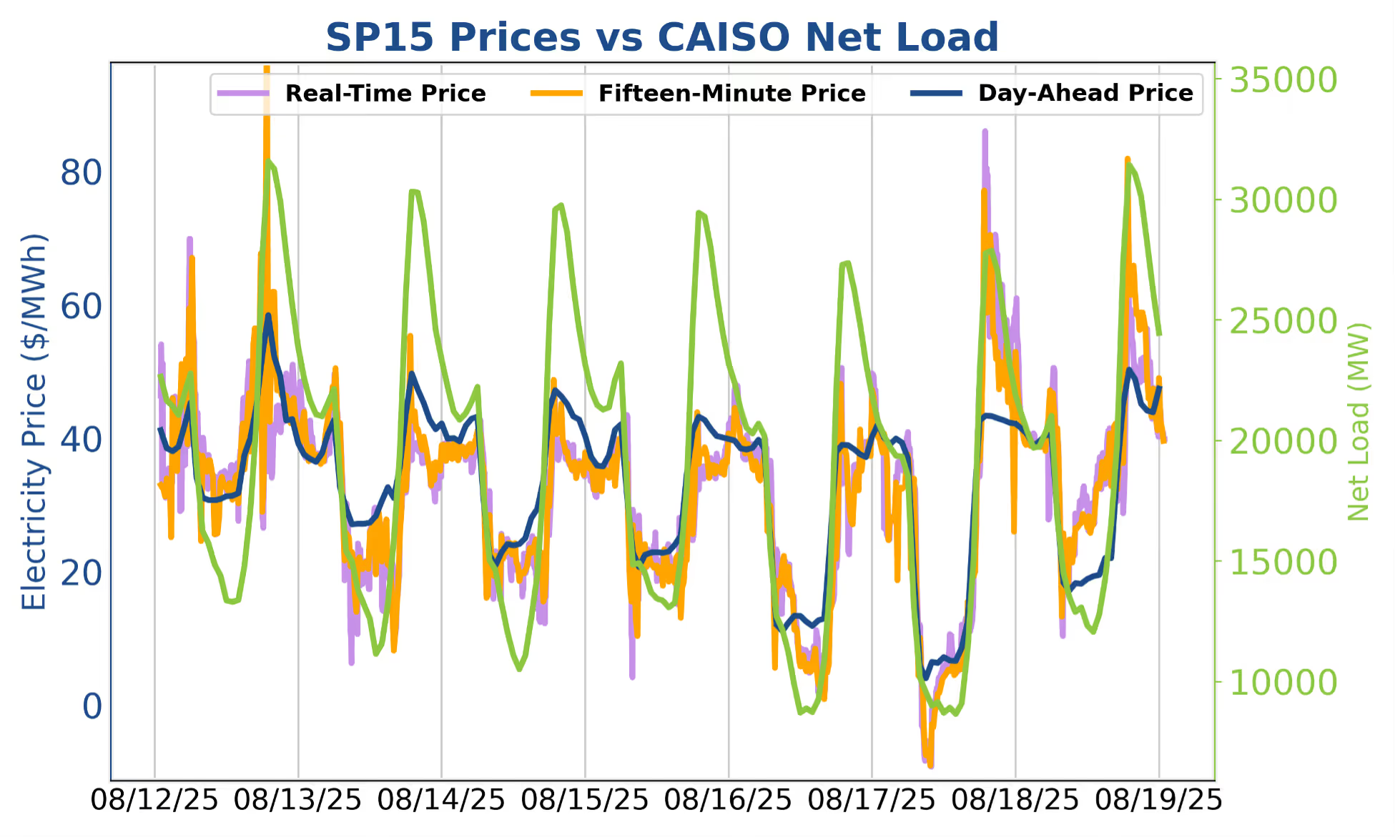

CAISO’s real-time market showed some signs of life on the evening of the 17th and 18th, but the best strategy this week was still a day-ahead heavy strategy. Batteries that can participate in regulation may have had some chance for upside, but otherwise DA TBx remained the best strategy. The charging prices were better in real-time on a few days, but this was not enough to offset day-ahead discharge opportunities. Next week could change the trend, but DA TBx remained dominant last week.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of August 20th – 26th: Elevated peaks will make Aug 20-21 in ERCOT and Aug 22 in CAISO the days to watch out for as high summer temperatures take over.

In ERCOT, high system loads and modest wind will keep net loads above 70 GW, with sharp evening ramps through the week. Solar variability on Aug 20–21 could push peaks even higher and drive real-time price volatility.

In CAISO, net load peaks will be elevated this week, likely driving higher evening prices. A day-ahead heavy strategy remains optimal, as added storage capacity and lower net loads should keep grid conditions less constrained than last year’s peak events.

High system loads combined with modest wind production are projected to keep net load peaks consistently above 70 GW through the upcoming week. Strong solar output, paired with relatively weak wind in the first half of the week will drive sharp evening ramps as solar fades each day. The 20th and 21st stand out with unusually high variance in the solar forecast—severe weather across Texas could significantly reduce real-time (RT) solar generation, pushing net load peaks even higher and creating elevated price volatility in RT markets.

Following last week’s trend, heavy day-ahead (DA) participation remains the recommended strategy, with some room reserved for real-time activity on the 20th and 21st to capture volatility. SmartBidder’s Mt. Blue Sky strategy will pick up on these dynamics and hedge accordingly in the day-ahead market while positioning for evening scarcity risks. Talk with your analyst about tuning Mt. Blue Sky to your risk tolerance if you want to use this window to fine-tune performance or expand capabilities.

At most ERCOT nodes last week, day-ahead energy discharge opportunities far outpaced real-time on the lucrative 12th and 18th. While some negative DART spreads emerged on the 14th and 15th, SmartBidder’s opportunity cost-based bidding framework effectively preserved flexibility for real-time exposure.

We’re also seeing a growing pattern of muted real-time prices during the two-peak day-ahead hours on high-priced DA days. Not a hard rule, but increasingly common: real-time prices tend to swing before and after the DA peaks, with a noticeable trough in between—especially evident on the 18th. This is a pattern to continue to look out for when considering market participation. Talk to your analyst about exploring how to balance DA and RT exposure.

This week will serve as an important test of the updated CAISO grid. Net loads are projected to peak around 37.7 GW on the 22nd, with elevated levels above 35 GW persisting throughout the week. For comparison, the largest net load of 2024 was ~43 GW on 9/5/24. While this week’s peak may be the highest of 2025 to-date, it remains about 2.5 GW below the 40+ GW levels reached last year that drove more extreme conditions. Importantly, there is also roughly 3 GW of additional storage online compared to last summer. This added capacity is expected to mute scarcity conditions by reducing the likelihood that more expensive imports or gas plants set prices when there is a misalignment between forecasted and actual renewable generation. However, elevated loads at this time of year still have the potential to drive elevated prices. Hub-level day-ahead prices could reach triple digits this week, while continued over-procurement in the day-ahead market and added storage capacity may limit substantial real-time blowouts. The recommended approach remains to participate heavily in the day-ahead market.

CAISO’s real-time market showed some signs of life on the evening of the 17th and 18th, but the best strategy this week was still a day-ahead heavy strategy. Batteries that can participate in regulation may have had some chance for upside, but otherwise DA TBx remained the best strategy. The charging prices were better in real-time on a few days, but this was not enough to offset day-ahead discharge opportunities. Next week could change the trend, but DA TBx remained dominant last week.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)