Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

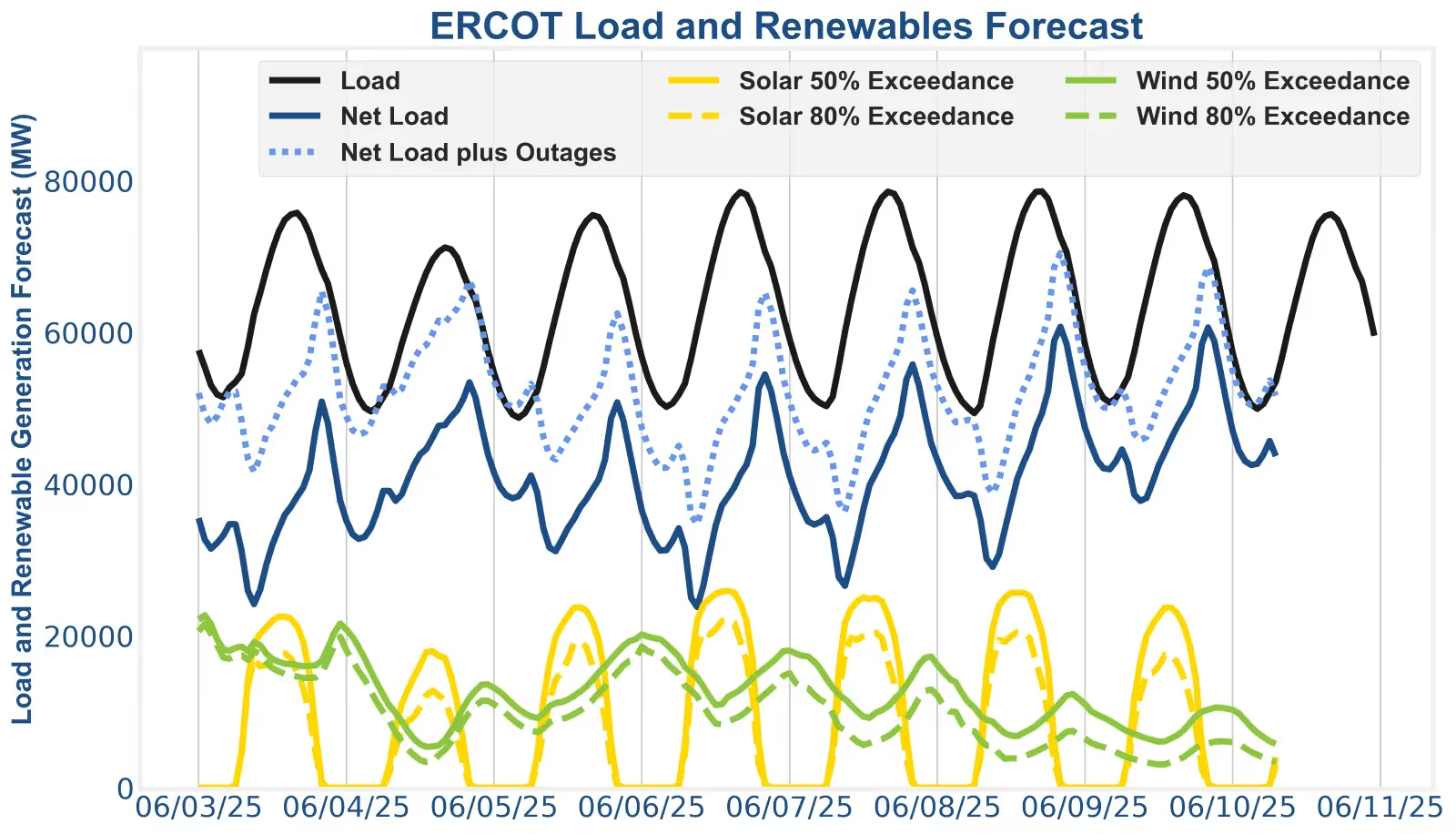

For the week of June 4 to 11, 2025, ERCOT operators will experience slightly improved revenue opportunities on the 8th and 9th due to lower wind production while CAISO putters along through cool market conditions.

In ERCOT, Ancillary Services (AS) revenues will fall due to lower procured quantities and fewer thermal outages. However, AS participation is still valuable to posture assets for extended peak discharge profiles while squeezing out the incremental revenue AS affords.

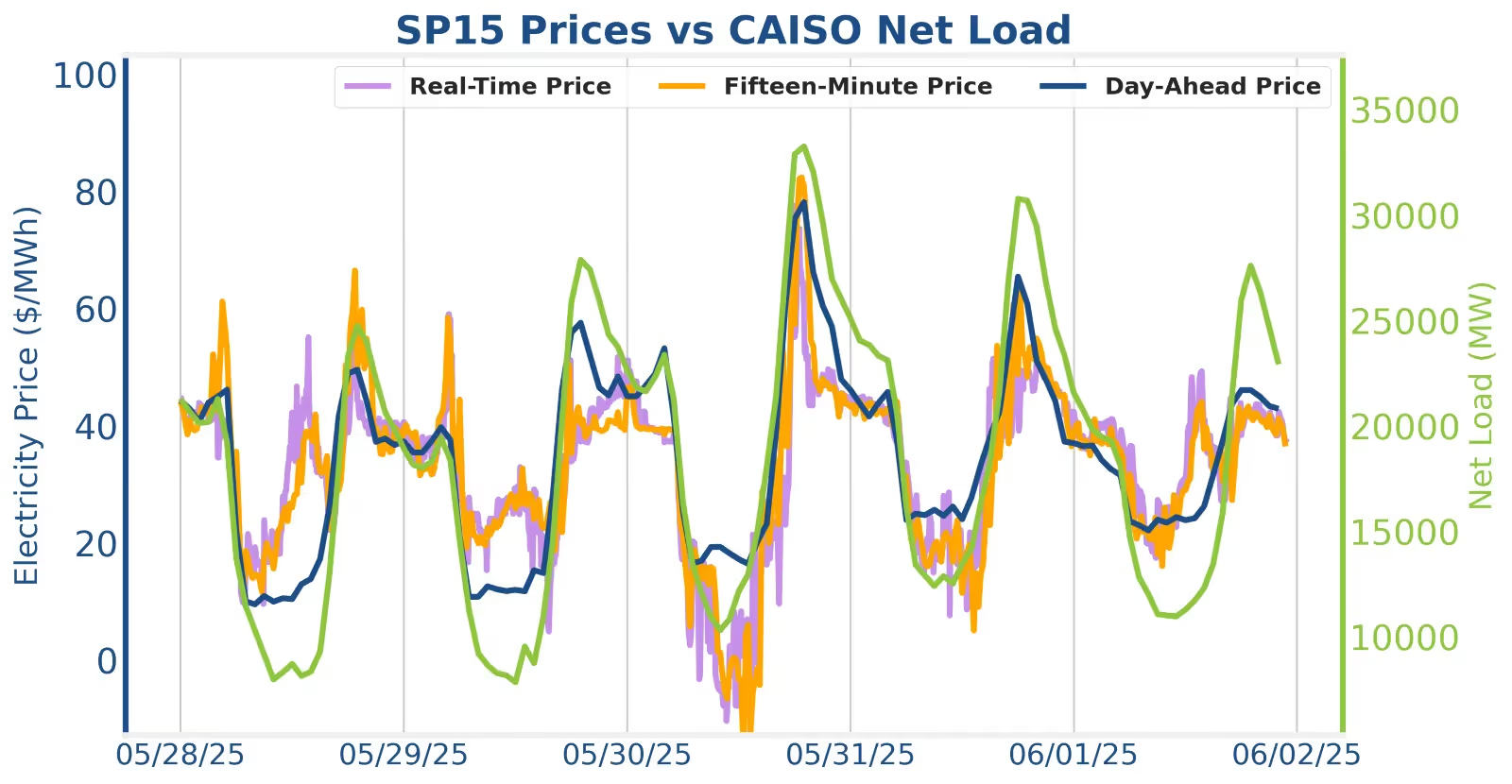

In CAISO, Day Ahead-Real Time (DART) spreads continue to fluctuate, and AS prices have fallen compared to spring levels. Operators should pay attention to local congestion that moves prices around as summer load shifts CAISO load distribution factors.

Summer weather has arrived in Texas. The next 3-4 months will determine whether 2025 continues to tightly track the scarce revenue opportunities from 2024 or if, against moderate odds, 2025 can elevate above mediocrity and provide a welcome boon to ERCOT generators.

Price formation will depend largely on weather conditions - chiefly the coincident temperature surges and wind troughs that so rarely act in concert. However, it will only take a handful of days with high, lingering load after the sun has set and low wind production to produce the momentous price spikes that can make or break yearly revenue stacks. A certain level of price volatility is wholly necessary for the health of the grid by incentivizing requisite new generation to continue entering the market. This will be the last summer before the RTC era in ERCOT and therefore the last opportunity for storage resources to accrue double-dipped revenues between AS and energy participation, stemming from a disjointed and inefficient AS procurement and deployment process.

On one hand, August peak futures have dropped from a high of ~$175/MWh on May 12 to $145/MWh at present with June weeks already slipping away. On the other hand, National Weather Service climatology has predicted hot, dry conditions that aim to land summer 2025 somewhere between 2023 and 2024 weather patterns. It’s time to flip the coins.

The SmartBidder team recommends deploying the Mount Blue Sky strategy or internally customized and risk-adjusted strategies for summer peak performance. We will keep you posted when volatility breaches the horizon.

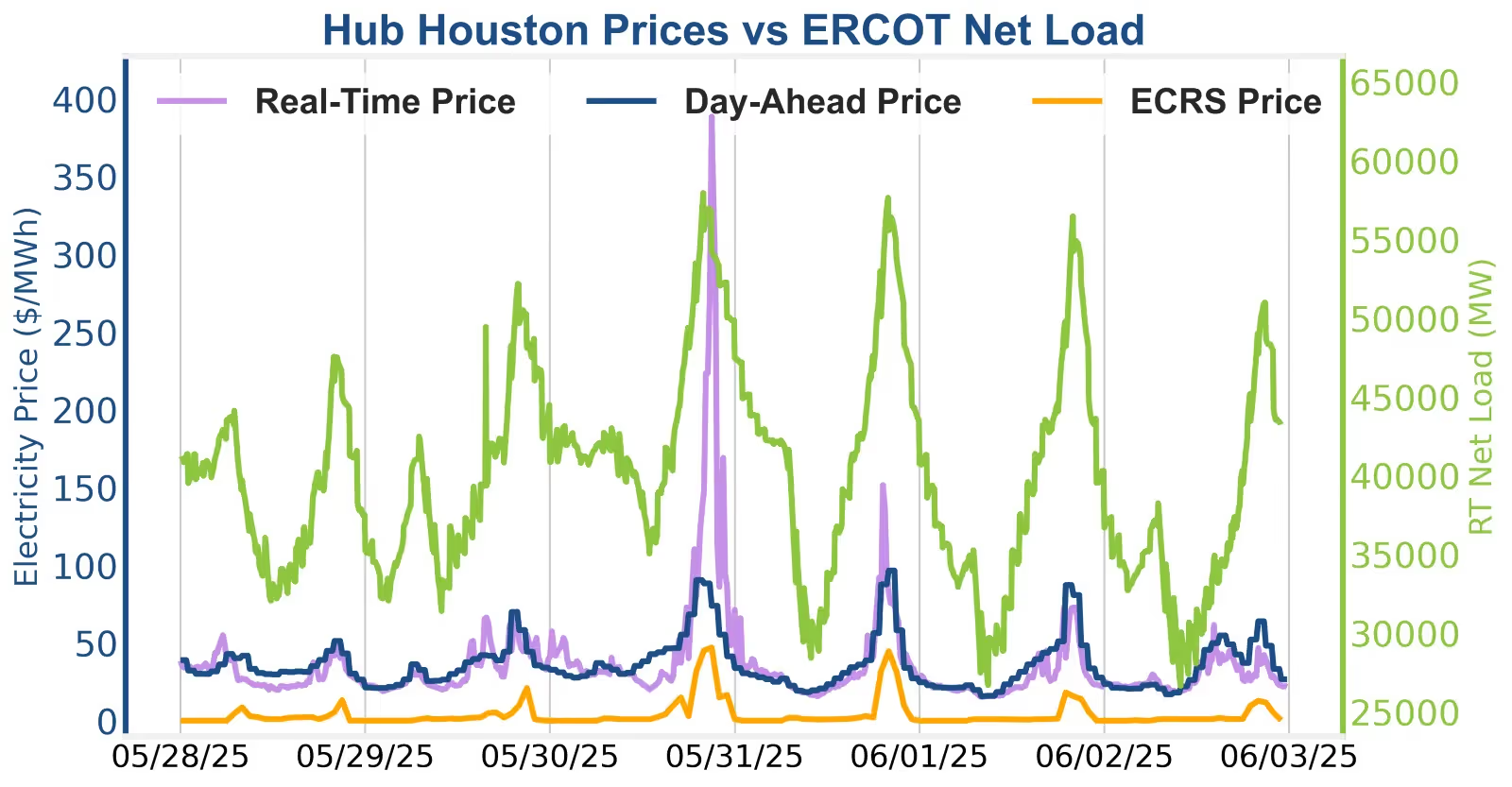

ERCOT closed out May with decent prices to cap a solid month with better AS revenues and a few readily monetizable price spikes. The evening of the 30th was the most interesting, as real-time prices spiked above $400/MWh during HE22 after the day-ahead energy price peak in HE20. Top performing assets picked up solid AS revenues in HE 20 and 21 before slamming the higher, second half of the peak in HE22.

Real-time revenue opportunities that occur post-day-ahead peak are becoming more commonplace in ERCOT. They are marked by wind production that fails to ramp up to day-ahead forecasts combined with the storage fleet discharging over real-time prices that are higher than peak day-ahead prices during the day-ahead peak and prior to the real-time spike. However, this behavior is certainly never guaranteed (see May 16) and a hedged approach of open real-time capacity, non-spin, reg-up, and ECRS during the peak is a solid way to pick up AS revenues and incrementally enable real-time base points as prices rise.

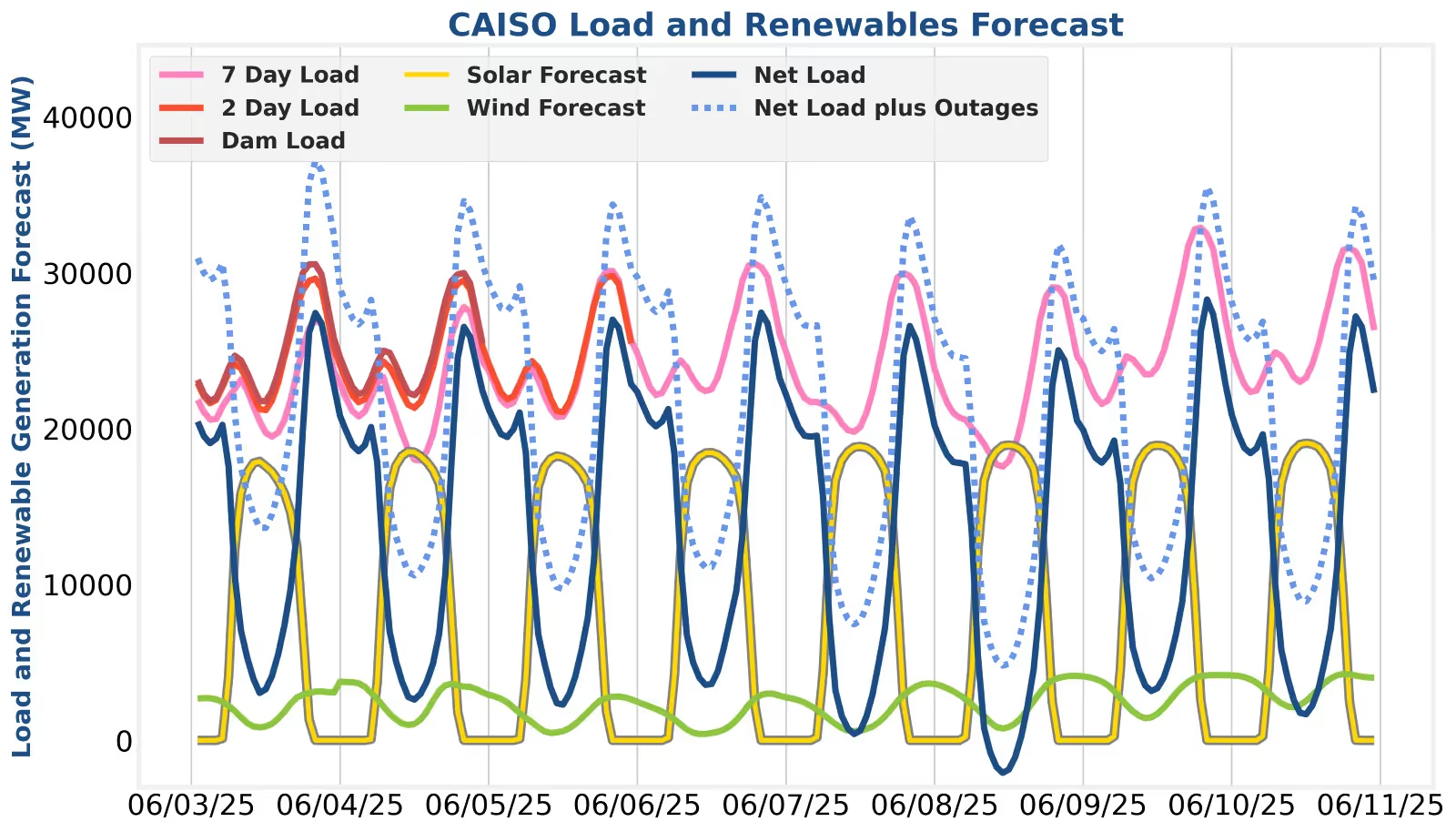

Net load peaks aren’t set to eclipse 30 GW this week, and revenue opportunities will be muted. Storage operators in CAISO should remain patient and plan their summer heat wave strategies. SmartBidder has significant configurability around where day-ahead charge and discharge bid tiers are set. Using this framework to split up capacity across day-ahead and real-time energy based on the DART spread probability forecast is the SmartBidder recommended way to hedge uncertainty between these day-ahead and real-time price spreads.

A minor heat wave drove the net load peak up to 33 GW on the 30th last week in CAISO, causing day-ahead and real-time prices to peak around $80/MWh. This will be a decent benchmark to return to during future heat waves this summer. DART spreads were mixed, favoring day-ahead charging on the 28th and 29th and then real-time charging on the 30th and 31st. Without consistent patterns in the DART spread, using a hedged approach based on the SmartBidder absolute and probabilistic DART forecasts is a savvy way to approach optimization under fickle DART conditions.

The information provided in this post is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of June 4 to 11, 2025, ERCOT operators will experience slightly improved revenue opportunities on the 8th and 9th due to lower wind production while CAISO putters along through cool market conditions.

In ERCOT, Ancillary Services (AS) revenues will fall due to lower procured quantities and fewer thermal outages. However, AS participation is still valuable to posture assets for extended peak discharge profiles while squeezing out the incremental revenue AS affords.

In CAISO, Day Ahead-Real Time (DART) spreads continue to fluctuate, and AS prices have fallen compared to spring levels. Operators should pay attention to local congestion that moves prices around as summer load shifts CAISO load distribution factors.

Summer weather has arrived in Texas. The next 3-4 months will determine whether 2025 continues to tightly track the scarce revenue opportunities from 2024 or if, against moderate odds, 2025 can elevate above mediocrity and provide a welcome boon to ERCOT generators.

Price formation will depend largely on weather conditions - chiefly the coincident temperature surges and wind troughs that so rarely act in concert. However, it will only take a handful of days with high, lingering load after the sun has set and low wind production to produce the momentous price spikes that can make or break yearly revenue stacks. A certain level of price volatility is wholly necessary for the health of the grid by incentivizing requisite new generation to continue entering the market. This will be the last summer before the RTC era in ERCOT and therefore the last opportunity for storage resources to accrue double-dipped revenues between AS and energy participation, stemming from a disjointed and inefficient AS procurement and deployment process.

On one hand, August peak futures have dropped from a high of ~$175/MWh on May 12 to $145/MWh at present with June weeks already slipping away. On the other hand, National Weather Service climatology has predicted hot, dry conditions that aim to land summer 2025 somewhere between 2023 and 2024 weather patterns. It’s time to flip the coins.

The SmartBidder team recommends deploying the Mount Blue Sky strategy or internally customized and risk-adjusted strategies for summer peak performance. We will keep you posted when volatility breaches the horizon.

ERCOT closed out May with decent prices to cap a solid month with better AS revenues and a few readily monetizable price spikes. The evening of the 30th was the most interesting, as real-time prices spiked above $400/MWh during HE22 after the day-ahead energy price peak in HE20. Top performing assets picked up solid AS revenues in HE 20 and 21 before slamming the higher, second half of the peak in HE22.

Real-time revenue opportunities that occur post-day-ahead peak are becoming more commonplace in ERCOT. They are marked by wind production that fails to ramp up to day-ahead forecasts combined with the storage fleet discharging over real-time prices that are higher than peak day-ahead prices during the day-ahead peak and prior to the real-time spike. However, this behavior is certainly never guaranteed (see May 16) and a hedged approach of open real-time capacity, non-spin, reg-up, and ECRS during the peak is a solid way to pick up AS revenues and incrementally enable real-time base points as prices rise.

Net load peaks aren’t set to eclipse 30 GW this week, and revenue opportunities will be muted. Storage operators in CAISO should remain patient and plan their summer heat wave strategies. SmartBidder has significant configurability around where day-ahead charge and discharge bid tiers are set. Using this framework to split up capacity across day-ahead and real-time energy based on the DART spread probability forecast is the SmartBidder recommended way to hedge uncertainty between these day-ahead and real-time price spreads.

A minor heat wave drove the net load peak up to 33 GW on the 30th last week in CAISO, causing day-ahead and real-time prices to peak around $80/MWh. This will be a decent benchmark to return to during future heat waves this summer. DART spreads were mixed, favoring day-ahead charging on the 28th and 29th and then real-time charging on the 30th and 31st. Without consistent patterns in the DART spread, using a hedged approach based on the SmartBidder absolute and probabilistic DART forecasts is a savvy way to approach optimization under fickle DART conditions.

The information provided in this post is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)