Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

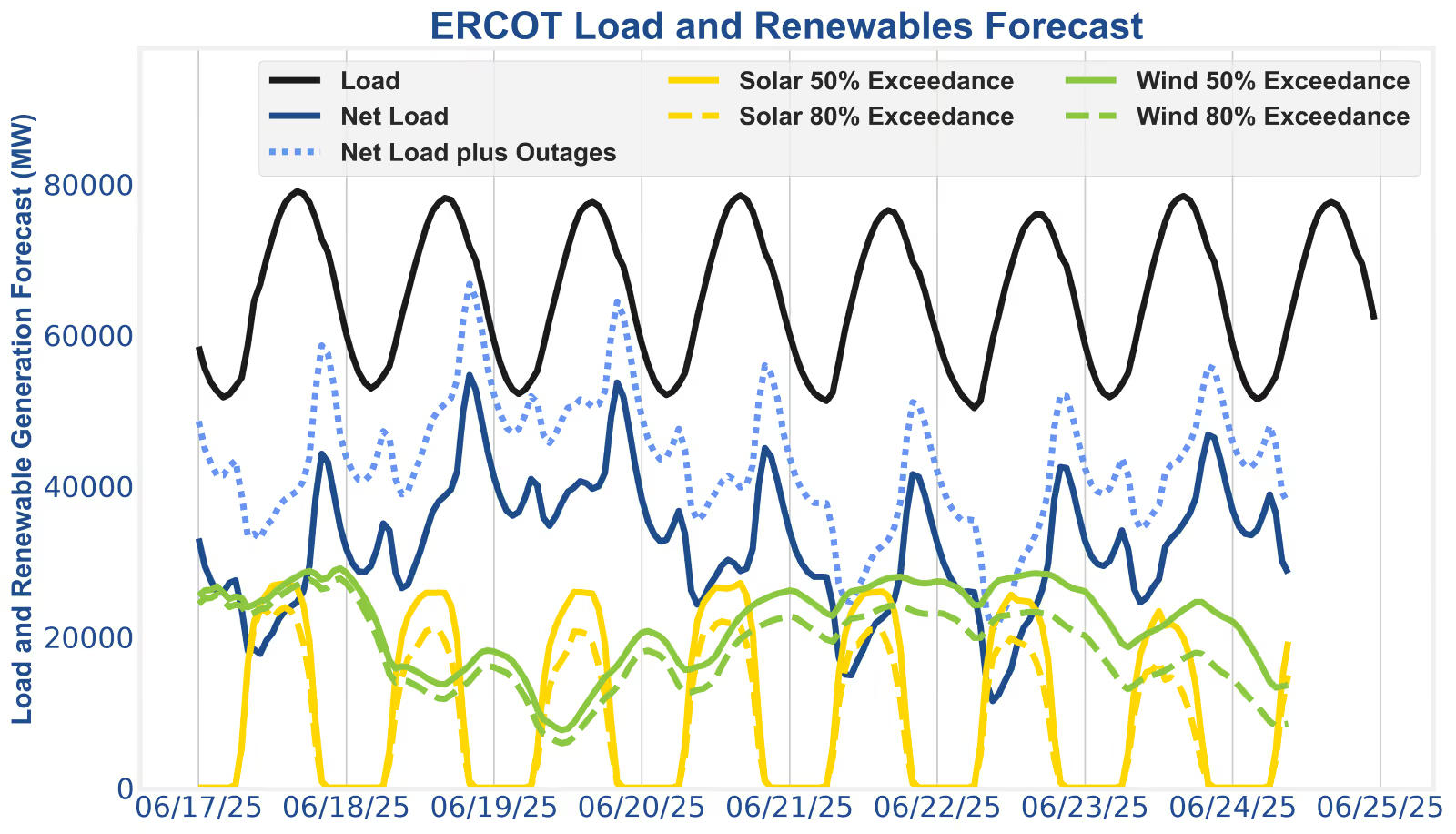

For the week of June 18th – 25th, mild market conditions will persist throughout ERCOT and CAISO. The 18th should be the largest revenue opportunity in both markets over the next week.

In ERCOT, strong wind production on the 20th through the 24th will stifle day-ahead energy prices. Asset operators should consider waiting for unexpected real-time energy volatility or, if they need to reign in their annual cycling numbers, loading up on cheap ancillary services (AS) and waiting out the wind.

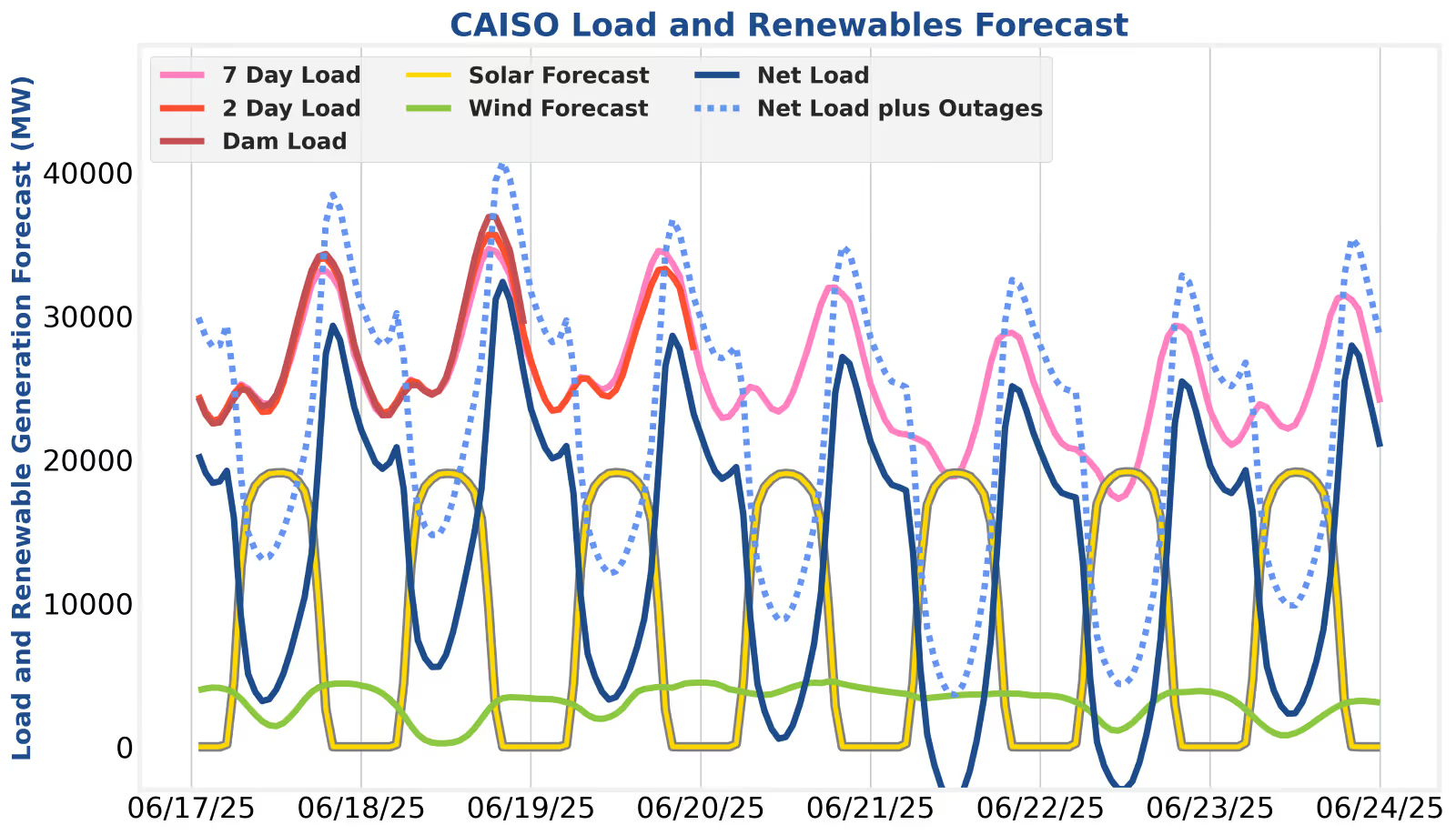

In CAISO, arbitrage spreads will tighten after the 18th, and operators will likely want to return to day-ahead energy discharge during the evenings to capitalize on strong TB4 performance that has been prevalent over the past weeks and months and is expected to continue.

The 18th and 19th will offer mediocre energy arbitrage opportunities before strong wind production takes the teeth out of the evening net load ramps beginning on the 20th. Operators should expect SmartBidder to adjust the day-ahead market strategy on the 20th as it adapts to lower day-ahead energy prices by pursuing additional AS participation. Gross load will consistently peak near 80 GW for the forecastable future. Any days with big wind forecast misses to the downside could open the door for real-time volatility.

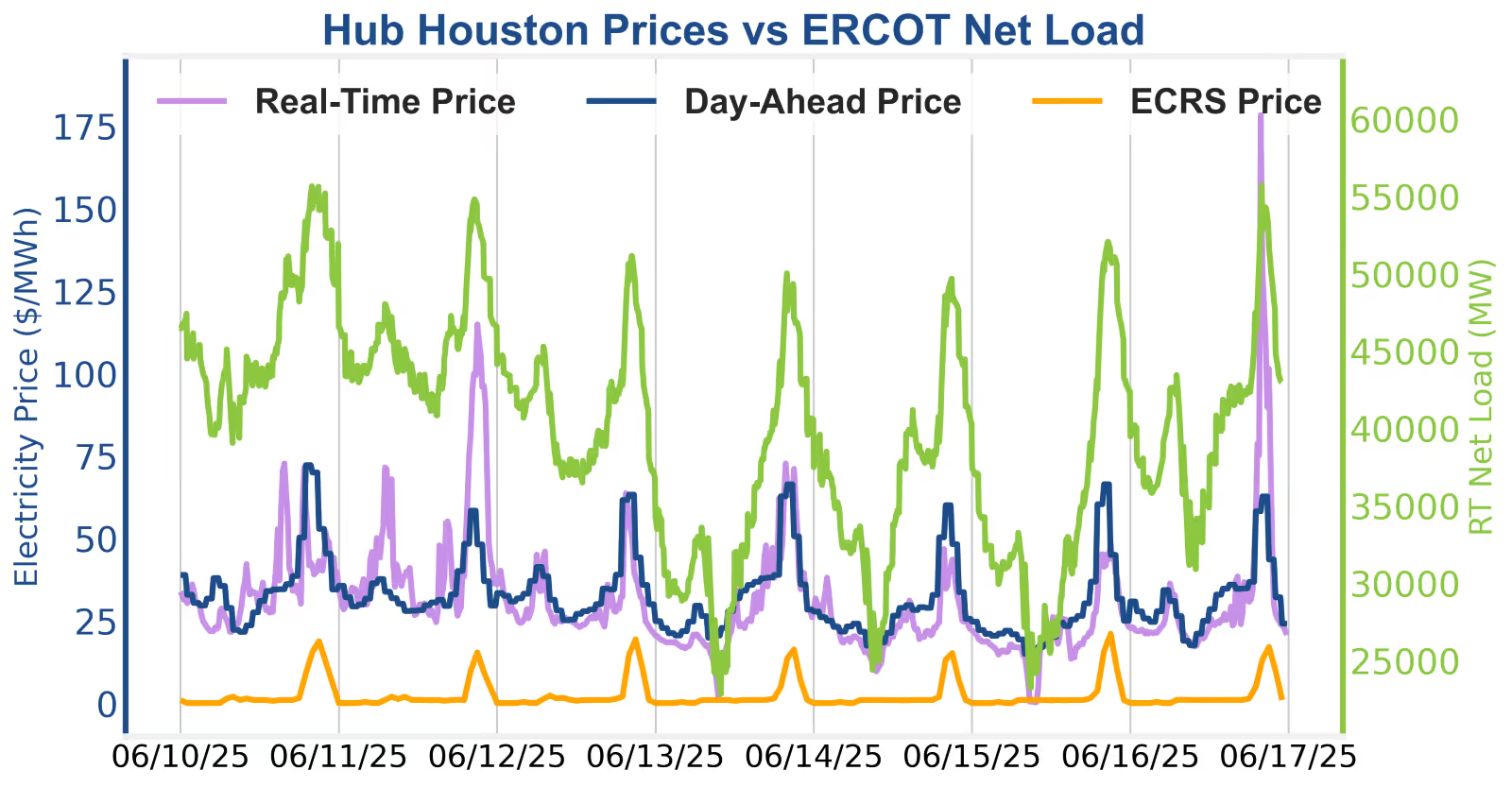

Evening DART spreads were variable last week in ERCOT as the 11th and 16th rewarded operators in the real-time market, while the 10th and 15th favored day-ahead energy discharge. AS prices have been priced around 25% of peak energy opportunities, emphasizing the need to preserve energy discharge capacity during the peaks for operators looking to maximize revenue over at least one cycle per day.

Peak load forecasts for the evening of the 18th have steadily increased across the seven-day, two-day, and day-ahead timeframes. Net load has only exceeded 30 GW once in the past month, making the 18th a key day to watch this week. If there's another load forecast miss—similar to what occurred on the evening of the 16th—where real-time load comes in higher than forecasted and wind underperforms during the solar ramp-down, the elevated net load could drive real-time energy prices to once again outperform day-ahead prices. Operators who save capacity to participate in real-time on the evening of the 18th could see additional opportunities. Looking ahead to the remainder of the week, regulation and day-ahead energy arbitrage strategies will likely become optimalstarting on the 19th and into the weekend as net loads begin to stabilize.

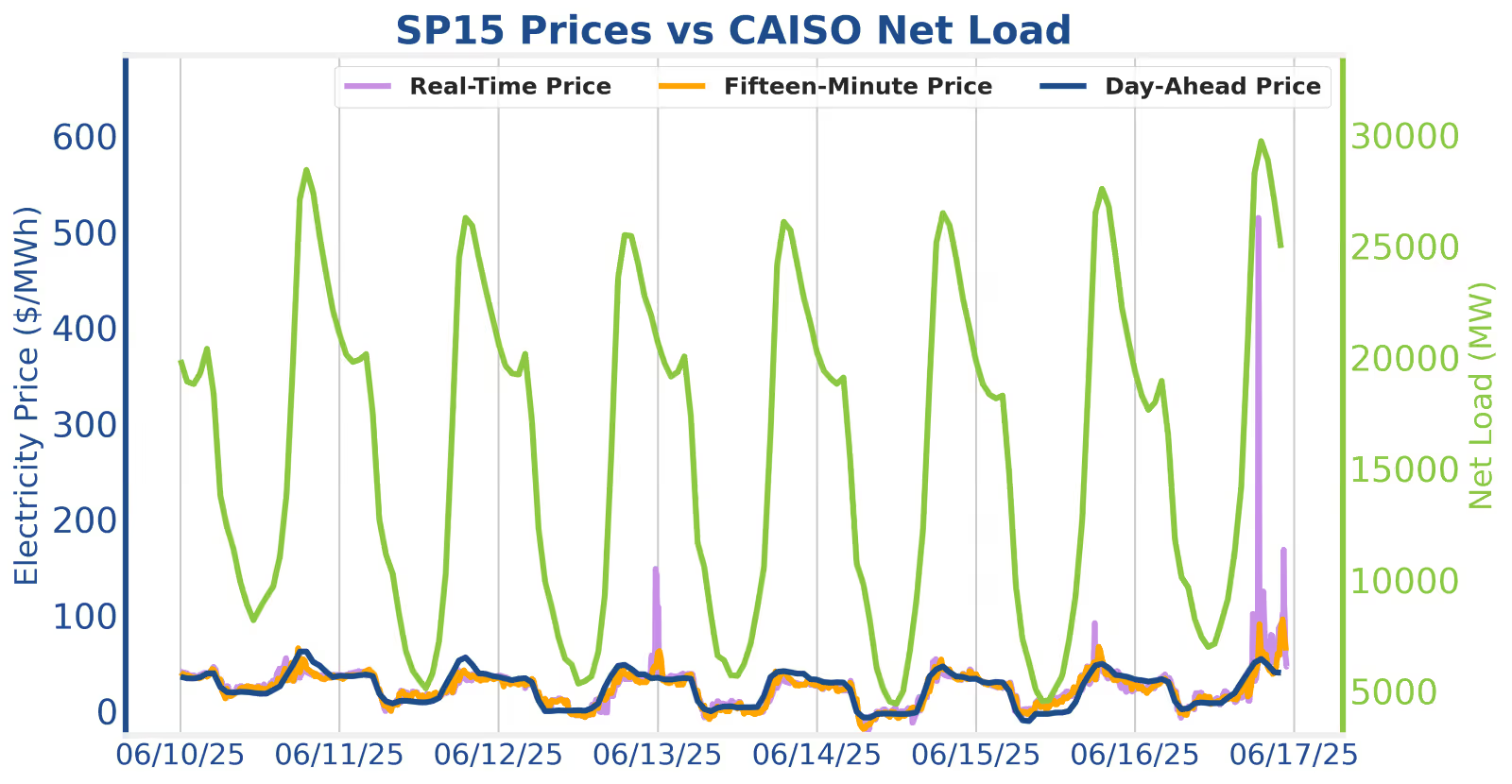

After a long stretch of positive evening DART spreads, real-time energy prices broke the pattern on the 16th. The CAISO battery fleet responded to the long-awaited real-time price spike by dispatching 10.4 GW, setting a new record for maximum battery discharge. Even though real-time five-minute prices spiked above $500/MWh in SP15, the Fifteen Minute Market (FMM) prices peaked closer to $100/MWh, paying out most battery operators less than they might have hoped. The price spike was fleeting, lasting only five minutes before returning to more typical levels mirroring the day-ahead price. Even with the unusual real-time volatility observed yesterday, only about two charge and two discharge hours in real-time were more favorable than their day-ahead counterparts.

Despite CAISO’s comparably smaller forecasted load growth versus other regions, we expect evening real-time price spikes like the one on the 16th to become more common as we move deeper into summer. CAISO recently set a new record for solar generation at 21.5 GW on the 13th, and this continued growth in solar output can make the evening ramp more challenging for thermal resources—leading to brief but notable real-time volatility.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of June 18th – 25th, mild market conditions will persist throughout ERCOT and CAISO. The 18th should be the largest revenue opportunity in both markets over the next week.

In ERCOT, strong wind production on the 20th through the 24th will stifle day-ahead energy prices. Asset operators should consider waiting for unexpected real-time energy volatility or, if they need to reign in their annual cycling numbers, loading up on cheap ancillary services (AS) and waiting out the wind.

In CAISO, arbitrage spreads will tighten after the 18th, and operators will likely want to return to day-ahead energy discharge during the evenings to capitalize on strong TB4 performance that has been prevalent over the past weeks and months and is expected to continue.

The 18th and 19th will offer mediocre energy arbitrage opportunities before strong wind production takes the teeth out of the evening net load ramps beginning on the 20th. Operators should expect SmartBidder to adjust the day-ahead market strategy on the 20th as it adapts to lower day-ahead energy prices by pursuing additional AS participation. Gross load will consistently peak near 80 GW for the forecastable future. Any days with big wind forecast misses to the downside could open the door for real-time volatility.

Evening DART spreads were variable last week in ERCOT as the 11th and 16th rewarded operators in the real-time market, while the 10th and 15th favored day-ahead energy discharge. AS prices have been priced around 25% of peak energy opportunities, emphasizing the need to preserve energy discharge capacity during the peaks for operators looking to maximize revenue over at least one cycle per day.

Peak load forecasts for the evening of the 18th have steadily increased across the seven-day, two-day, and day-ahead timeframes. Net load has only exceeded 30 GW once in the past month, making the 18th a key day to watch this week. If there's another load forecast miss—similar to what occurred on the evening of the 16th—where real-time load comes in higher than forecasted and wind underperforms during the solar ramp-down, the elevated net load could drive real-time energy prices to once again outperform day-ahead prices. Operators who save capacity to participate in real-time on the evening of the 18th could see additional opportunities. Looking ahead to the remainder of the week, regulation and day-ahead energy arbitrage strategies will likely become optimalstarting on the 19th and into the weekend as net loads begin to stabilize.

After a long stretch of positive evening DART spreads, real-time energy prices broke the pattern on the 16th. The CAISO battery fleet responded to the long-awaited real-time price spike by dispatching 10.4 GW, setting a new record for maximum battery discharge. Even though real-time five-minute prices spiked above $500/MWh in SP15, the Fifteen Minute Market (FMM) prices peaked closer to $100/MWh, paying out most battery operators less than they might have hoped. The price spike was fleeting, lasting only five minutes before returning to more typical levels mirroring the day-ahead price. Even with the unusual real-time volatility observed yesterday, only about two charge and two discharge hours in real-time were more favorable than their day-ahead counterparts.

Despite CAISO’s comparably smaller forecasted load growth versus other regions, we expect evening real-time price spikes like the one on the 16th to become more common as we move deeper into summer. CAISO recently set a new record for solar generation at 21.5 GW on the 13th, and this continued growth in solar output can make the evening ramp more challenging for thermal resources—leading to brief but notable real-time volatility.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)