Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

-1-Data%20Centers.avif)

As AI development advances rapidly, data center-driven electricity demand is entering uncharted territory, with load estimated to grow between 37-66 GW during the next three years alone. Energy project developers and utilities are thus presented with significant opportunities as large corporate consumers with clean energy goals move quickly to secure supply.

As part of the 2025 Ascend Analytics Power Markets Workshop, Paul Saferstein, CFA, Senior Advisor for Data Centers, and Robert LaFaso, Director of Valuation and Forecasting, provided an overview of the data center industry structure, discussed ways that developers and utilities can align power procurement and project development activities with data center needs, and highlighted ways to capitalize on energy development opportunities in an uncertain and dynamic market environment.

Primarily, there exist two types of data center owners and operators. Hyperscalers, which are the half-dozen or so large corporate cloud providers that rely on data centers as a fundamental component of their business, are vertically integrated: they provide data center infrastructure, cloud services, and Internet/software as a service (SaaS). Boasting strong returns and deep pools of capital, hyperscalers prioritize speed to market, while emissions and costs remain in focus.

The second category contains retail and wholesale data centers, which also frequently provide data center services to hyperscalers. Wholesale data centers are more price-sensitive than hyperscalers, accepting yield-on-cost type contracts. However, with energy cost-pass through to tenants, speed to market becomes a top priority if a project can be de-risked with a pre-sold tenant lease, which serves as the data center industry equivalent to a power purchase agreement (PPA).

In the near term, load growth due to data center development is entering uncharted territory, and bringing with it high degrees of uncertainty. For example, estimated load growth during the next three years ranges from 37-66 GW. Such massive levels of variability make planning extremely difficult for utilities, developers, and investors. Several factors, such as a lack of clarity with regard to AI monetization, limited publicly available data, and a wide range of untested assumptions, limit the ability to precisely understand how the demand side might evolve within the next several years. But there is no denying the need for rapid expansion.

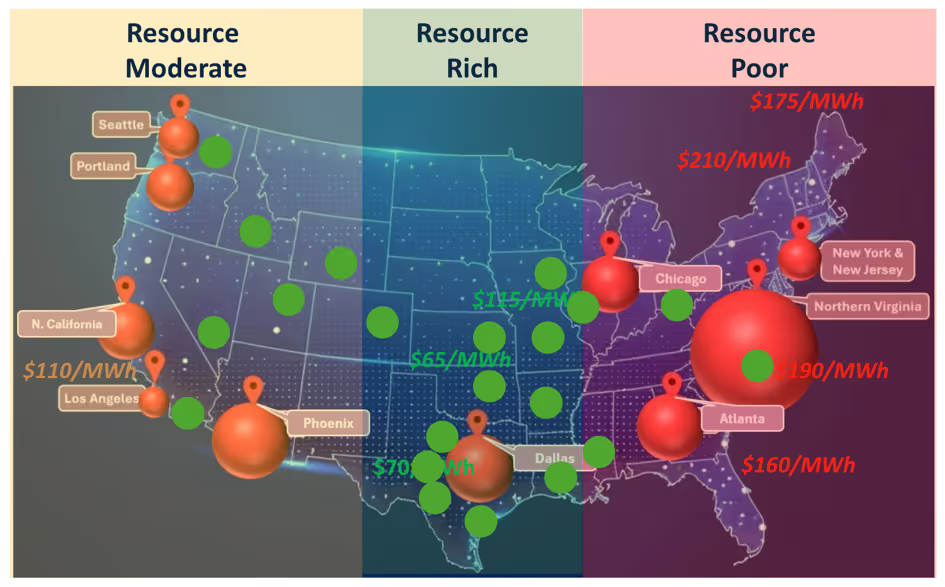

Historically, industry siting practices have followed sources of inexpensive power. With the current concept of cheap power coupled with the notion of zero-carbon power, data centers are moving toward locations that offer low-cost, low-emissions resources, yet are still near fiber routes, as seen in Figure 1. This marks a transition away from the fiber-rich, low-latency markets, such as those in northern Virginia or northern California, in which data centers have traditionally clustered.

While energy project developers, utilities, and buyers will necessarily need to work with one another, these stakeholders do not always speak the same 'language.' Power decision analysis is complicated for many data center developers, who frequently have custom requirements. In thinking about grid power or microgrid power, data center stakeholders use a combination of fundamental and quantitative analysis that leverages high-level mathematical techniques, proprietary datasets, and cohesive teams with ample experience.

Developers and utilities may not necessarily have the experience or teams in place to efficiently understand data center stakeholder needs at an operational level. Similarly, energy developers and utilities often take very different approaches to energy project siting than data centers do with their own projects. Thus, it can be very useful to leverage an energy analytics consulting firm, such as Ascend Analytics, as a 'translator’ in order to efficiently and effectively understand stakeholder needs.

Other than speed to market, location is the most important aspect for data center developers. Identifying the optimal location to build a billion-dollar data center with a quarter-billion-dollar energy facility can feel sometimes like threading the eye of a needle.

Access to low-latency fiber routes remains important, though less so for AI model training than for providing real-time, latency-sensitive services. For data center stakeholders, building additional fiber routes is nowhere near as expensive or complex as building new transmission.

Reliability standards also matter. Unlike reliability standards for most load-serving entities, the majority of data centers currently require full “N+1” redundancy, with far stricter requirements in terms of acceptable outage time. Data center reliability standards exceed standard utility planning one-day in ten-years loss-of-load expectations as well.

In terms of speed to market, near-term queues in all US markets dictate where buildout can happen, and what it might look like. For the moment, interconnection constraints create a small sub-set of energy projects that can realistically achieve a near-term commercial operations date (CoD) for data center projects. CoD-ready generators are predominantly green, which will force the hand of energy-hungry buyers. Markets are all looking to accelerate their capacity expansion, but the regulatory process to approve queue shortcuts has slow and intensive FERC oversight.

Emissions matter, too. If emissions offsets and abatements are a goal for data center developers, then siting the project next to the load might not be the best idea. In a situation where capacity market prices differ zonally, siting the project in the same capacity zone, but in a more ideal location, hedges both power and capacity price, as well as doing a better job of covering emissions. Market, however, matters more than location. For example, the best locations for PV emissions abatement in ERCOT are well below average in PJM for emissions abatement, and the best location in CAISO is worse than the worst location in PJM.

As electricity demand continues to grow, so too do the number of conversations between utilities and data center operators about who should bear the cost of the transmission and distribution upgrades necessary to support load growth. Utilities have the potential to be in a strong negotiating position because 'power' is the scarce resource and hyperscalers – as effective monopolies – have the ability to fund all of their generation, transmission, and development requirements, while taking a manageable capital expenditure hit. Whether they are willing to do so as for-profit corporations, however, remains rightly questionable.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over 300 gigawatts and $25 billion in project assessments. Please contact us to learn more.

As AI development advances rapidly, data center-driven electricity demand is entering uncharted territory, with load estimated to grow between 37-66 GW during the next three years alone. Energy project developers and utilities are thus presented with significant opportunities as large corporate consumers with clean energy goals move quickly to secure supply.

As part of the 2025 Ascend Analytics Power Markets Workshop, Paul Saferstein, CFA, Senior Advisor for Data Centers, and Robert LaFaso, Director of Valuation and Forecasting, provided an overview of the data center industry structure, discussed ways that developers and utilities can align power procurement and project development activities with data center needs, and highlighted ways to capitalize on energy development opportunities in an uncertain and dynamic market environment.

Primarily, there exist two types of data center owners and operators. Hyperscalers, which are the half-dozen or so large corporate cloud providers that rely on data centers as a fundamental component of their business, are vertically integrated: they provide data center infrastructure, cloud services, and Internet/software as a service (SaaS). Boasting strong returns and deep pools of capital, hyperscalers prioritize speed to market, while emissions and costs remain in focus.

The second category contains retail and wholesale data centers, which also frequently provide data center services to hyperscalers. Wholesale data centers are more price-sensitive than hyperscalers, accepting yield-on-cost type contracts. However, with energy cost-pass through to tenants, speed to market becomes a top priority if a project can be de-risked with a pre-sold tenant lease, which serves as the data center industry equivalent to a power purchase agreement (PPA).

In the near term, load growth due to data center development is entering uncharted territory, and bringing with it high degrees of uncertainty. For example, estimated load growth during the next three years ranges from 37-66 GW. Such massive levels of variability make planning extremely difficult for utilities, developers, and investors. Several factors, such as a lack of clarity with regard to AI monetization, limited publicly available data, and a wide range of untested assumptions, limit the ability to precisely understand how the demand side might evolve within the next several years. But there is no denying the need for rapid expansion.

Historically, industry siting practices have followed sources of inexpensive power. With the current concept of cheap power coupled with the notion of zero-carbon power, data centers are moving toward locations that offer low-cost, low-emissions resources, yet are still near fiber routes, as seen in Figure 1. This marks a transition away from the fiber-rich, low-latency markets, such as those in northern Virginia or northern California, in which data centers have traditionally clustered.

While energy project developers, utilities, and buyers will necessarily need to work with one another, these stakeholders do not always speak the same 'language.' Power decision analysis is complicated for many data center developers, who frequently have custom requirements. In thinking about grid power or microgrid power, data center stakeholders use a combination of fundamental and quantitative analysis that leverages high-level mathematical techniques, proprietary datasets, and cohesive teams with ample experience.

Developers and utilities may not necessarily have the experience or teams in place to efficiently understand data center stakeholder needs at an operational level. Similarly, energy developers and utilities often take very different approaches to energy project siting than data centers do with their own projects. Thus, it can be very useful to leverage an energy analytics consulting firm, such as Ascend Analytics, as a 'translator’ in order to efficiently and effectively understand stakeholder needs.

Other than speed to market, location is the most important aspect for data center developers. Identifying the optimal location to build a billion-dollar data center with a quarter-billion-dollar energy facility can feel sometimes like threading the eye of a needle.

Access to low-latency fiber routes remains important, though less so for AI model training than for providing real-time, latency-sensitive services. For data center stakeholders, building additional fiber routes is nowhere near as expensive or complex as building new transmission.

Reliability standards also matter. Unlike reliability standards for most load-serving entities, the majority of data centers currently require full “N+1” redundancy, with far stricter requirements in terms of acceptable outage time. Data center reliability standards exceed standard utility planning one-day in ten-years loss-of-load expectations as well.

In terms of speed to market, near-term queues in all US markets dictate where buildout can happen, and what it might look like. For the moment, interconnection constraints create a small sub-set of energy projects that can realistically achieve a near-term commercial operations date (CoD) for data center projects. CoD-ready generators are predominantly green, which will force the hand of energy-hungry buyers. Markets are all looking to accelerate their capacity expansion, but the regulatory process to approve queue shortcuts has slow and intensive FERC oversight.

Emissions matter, too. If emissions offsets and abatements are a goal for data center developers, then siting the project next to the load might not be the best idea. In a situation where capacity market prices differ zonally, siting the project in the same capacity zone, but in a more ideal location, hedges both power and capacity price, as well as doing a better job of covering emissions. Market, however, matters more than location. For example, the best locations for PV emissions abatement in ERCOT are well below average in PJM for emissions abatement, and the best location in CAISO is worse than the worst location in PJM.

As electricity demand continues to grow, so too do the number of conversations between utilities and data center operators about who should bear the cost of the transmission and distribution upgrades necessary to support load growth. Utilities have the potential to be in a strong negotiating position because 'power' is the scarce resource and hyperscalers – as effective monopolies – have the ability to fund all of their generation, transmission, and development requirements, while taking a manageable capital expenditure hit. Whether they are willing to do so as for-profit corporations, however, remains rightly questionable.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over 300 gigawatts and $25 billion in project assessments. Please contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)