Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Decarbonizing US energy markets presents a number of difficult challenges. Overnight decarbonization effectively has not started, even for states such as California that have invested aggressively in renewable energy generation. The focus to this point has been on wind, solar, and short-duration solar, but none of these resources reliably serve overnight load. Decarbonization is also highly complicated in markets such as NYISO, ISO-NE, or PJM that experience frequent winter peaks. And while clean energy resources such as long-duration storage or hydrogen hold promise for reliability planners, high costs associated with these nascent technologies present significant obstacles.

At the Ascend Analytics 2025 Power Markets workshop, Robert LaFaso, Ascend's Director of Forecasting and Valuation, discussed the scope of the decarbonization problem in US energy markets, and the resources and actions that might help energy market stakeholders make progress toward decarbonization goals.

In order to understand the scope of the challenges that face energy market stakeholders with decarbonization goals, it is helpful to look at California, which has invested more aggressively in renewable energy resources than any other state. In so doing, California has succeeded in reducing emissions during the middle of the day and during peak evening hours, thanks to high levels of solar deployment as well as short-duration storage.

Overnight decarbonization, however, remains a significant challenge in California. On peak days, the California Independent System Operator (CAISO) would require nearly 30 GW of new clean generation to fully decarbonize; on typical winter days, the state would need 15 GW of 16-hour storage to decarbonize.

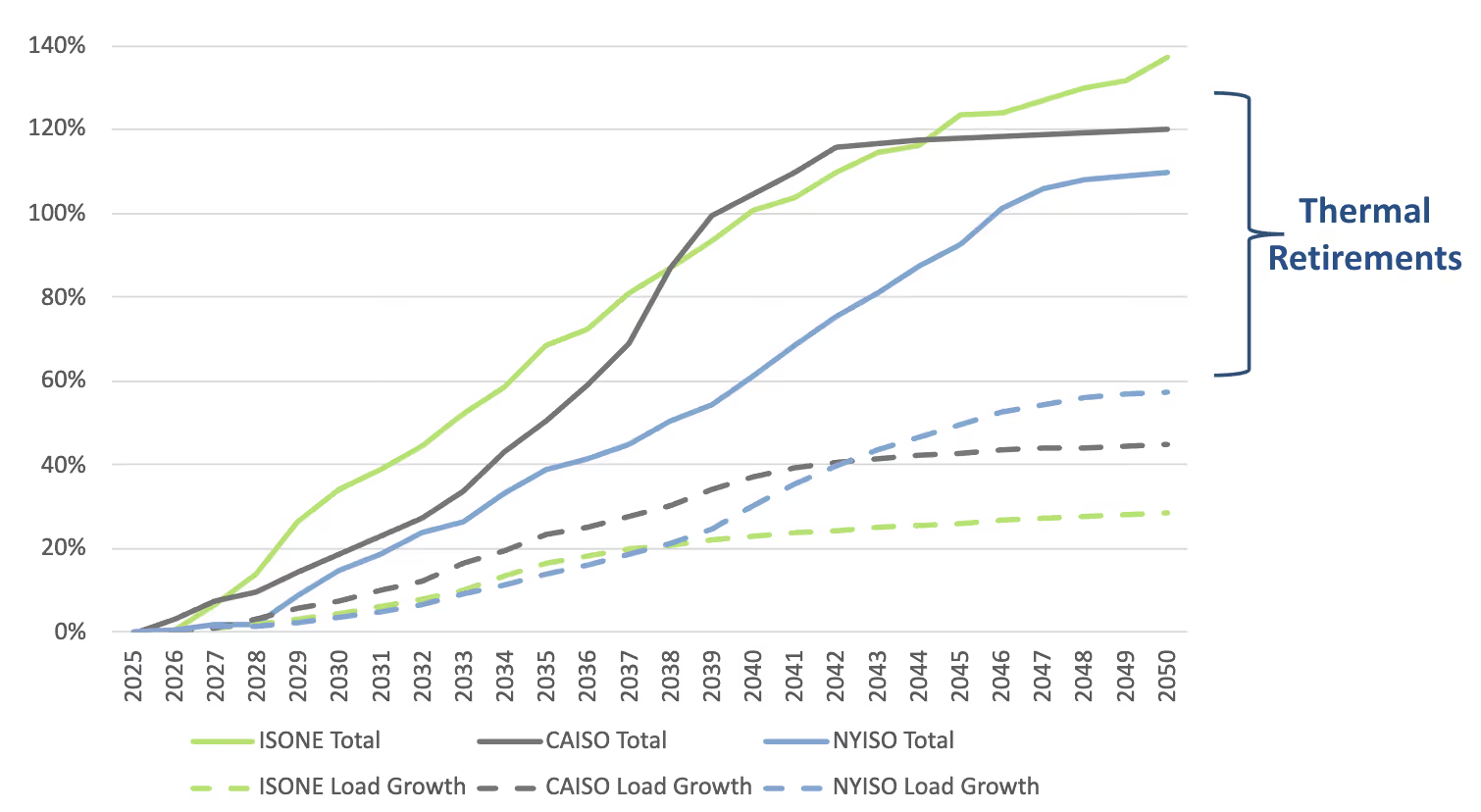

The scale of the decarbonization problem is compounded by load growth, as shown in Figure 1. Before a grid can even start to look at 'Green Overnight, it first must have the ability to install enough generation to offset peak load growth. If markets with zero emissions targets, such as CAISO, ISO-NE, or NYISO, want to meet those goals, they must install capacity equal to about 120% of their current peak load. Much of this new capacity will need to be long-duration resources.

Cost remains a critical obstacle, however. Nearly all renewable resources with the potential to decarbonize overnight generation are nascent. Unsurprisingly, then, markets have not yet had success building long-duration non-thermal resources without subsidies.

Winter peaking makes the challenge even more difficult. The resources needed to offset growth in summer peak load are much less expensive than the resources needed to offset winter peak load growth. Summer peak shapes can be addressed with a combination of solar and short-duration storage. Meeting a winter peak with non-thermal resources, however, can only truly be addressed with multi-day/seasonal storage or renewable fuels. Offshore and onshore wind can be a part of the solution but both need firming capacity for reliability.

Meeting decarbonization targets is easier said than done, especially in markets, such as PJM, that have capacity market structures. In markets like PJM, generating units retire for one of two reasons: either they are not operating enough to earn meaningful margin in the spot market, or the capacity value they receive is lower than the unit's fixed operating expenses. With capacity prices going high and staying there, normal market signals that would push a unit to retire become obscured, making it difficult for thermal resources to economically retire. In markets such as CAISO and SPP, where bilateral capacity agreements are the norm, capacity procurement decisions can be made differently.

No matter the market, however, existing regulatory frameworks are creating the same issue: subsidies are flowing almost exclusively to incumbent generators. Other unintended consequences of regulatory actions are arising, as well. In California, for example, the Slice-of-Day program nominally includes a mechanism to value long-duration storage. In practice, the inflexible rules within the regulatory framework have made it more cost-effective to procure two 4-hour battery energy storage systems than one 8-hour long-duration system. This inflexibility also drives CAISO load-serving entities to use thermal resources to ensure overnight reliability. And in PJM, a 9x surge in capacity price has ratepayers paying every MW of generation at Net-CONE, despite single digit percent growth: each year, PJM is paying for 20x the resources that are actually newly installed.

Decarbonizing US energy markets requires tackling multiple issues in the near term. First, long-duration energy storage (LDES) is not currently cost-competitive with either short-duration storage or natural gas combustion turbines (CTs). Hundred-hour LDES can only beat CTs as a long-duration reliability resource with some large assumptions about accreditation: namely, if market stakeholders believe a marginal peaking event will be less than 100 hours, than a 100% effective load carrying capability (ELCC) can be assumed for LDES. Considering that Winter Storm Elliot in PJM lasted longer than 100 hours in December 2022, a 100% ELCC assumption would not likely find unanimous support.

The current CT supply chain shortage, which has pushed up CT cost estimates for 2030 delivery by more than 100%, also shapes the context for LDES cost-competitiveness. If peaks are shorter than 100 hours, and if CT costs remain elevated, then LDES becomes an economically viable solution.

Carbon tax policies are also likely needed to incentivize a transition to the use of non-thermal resources for overnight generation. Carbon prices disproportionally increase prices on a day's peak, which can boost energy arbitrage margins without flowing those dollars to carbon-emitting resources. For the foreseeable future, natural gas will remain the less expensive option per unit of energy; however, a carbon tax can make renewable fuel costs comparatively less 'after tax.'

There also exist two interesting non-hydrogen, non-storage solutions. Hybrid peaker-storage units represent a potentially useful compromise, and one that is beginning to appear in California. From a reliability planning perspective, the most efficient way to ensure 1-in-10 year system safety is to not retire existing assets and simply hybridize existing units to reduce legacy unit runtime and efficiently interconnect new clean resources. Nuclear energy is also enjoying a renaissance among certain energy market stakeholders, including the previous and current US presidential administrations. However, justifying the exorbitant cost of building nuclear, rather than any other resource, will be difficult.

Finally, solving decarbonization issues in US energy markets will require radical market restructuring. Whether the appetite to do so (and the ability to make it happen) exists remains questionable.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Decarbonizing US energy markets presents a number of difficult challenges. Overnight decarbonization effectively has not started, even for states such as California that have invested aggressively in renewable energy generation. The focus to this point has been on wind, solar, and short-duration solar, but none of these resources reliably serve overnight load. Decarbonization is also highly complicated in markets such as NYISO, ISO-NE, or PJM that experience frequent winter peaks. And while clean energy resources such as long-duration storage or hydrogen hold promise for reliability planners, high costs associated with these nascent technologies present significant obstacles.

At the Ascend Analytics 2025 Power Markets workshop, Robert LaFaso, Ascend's Director of Forecasting and Valuation, discussed the scope of the decarbonization problem in US energy markets, and the resources and actions that might help energy market stakeholders make progress toward decarbonization goals.

In order to understand the scope of the challenges that face energy market stakeholders with decarbonization goals, it is helpful to look at California, which has invested more aggressively in renewable energy resources than any other state. In so doing, California has succeeded in reducing emissions during the middle of the day and during peak evening hours, thanks to high levels of solar deployment as well as short-duration storage.

Overnight decarbonization, however, remains a significant challenge in California. On peak days, the California Independent System Operator (CAISO) would require nearly 30 GW of new clean generation to fully decarbonize; on typical winter days, the state would need 15 GW of 16-hour storage to decarbonize.

The scale of the decarbonization problem is compounded by load growth, as shown in Figure 1. Before a grid can even start to look at 'Green Overnight, it first must have the ability to install enough generation to offset peak load growth. If markets with zero emissions targets, such as CAISO, ISO-NE, or NYISO, want to meet those goals, they must install capacity equal to about 120% of their current peak load. Much of this new capacity will need to be long-duration resources.

Cost remains a critical obstacle, however. Nearly all renewable resources with the potential to decarbonize overnight generation are nascent. Unsurprisingly, then, markets have not yet had success building long-duration non-thermal resources without subsidies.

Winter peaking makes the challenge even more difficult. The resources needed to offset growth in summer peak load are much less expensive than the resources needed to offset winter peak load growth. Summer peak shapes can be addressed with a combination of solar and short-duration storage. Meeting a winter peak with non-thermal resources, however, can only truly be addressed with multi-day/seasonal storage or renewable fuels. Offshore and onshore wind can be a part of the solution but both need firming capacity for reliability.

Meeting decarbonization targets is easier said than done, especially in markets, such as PJM, that have capacity market structures. In markets like PJM, generating units retire for one of two reasons: either they are not operating enough to earn meaningful margin in the spot market, or the capacity value they receive is lower than the unit's fixed operating expenses. With capacity prices going high and staying there, normal market signals that would push a unit to retire become obscured, making it difficult for thermal resources to economically retire. In markets such as CAISO and SPP, where bilateral capacity agreements are the norm, capacity procurement decisions can be made differently.

No matter the market, however, existing regulatory frameworks are creating the same issue: subsidies are flowing almost exclusively to incumbent generators. Other unintended consequences of regulatory actions are arising, as well. In California, for example, the Slice-of-Day program nominally includes a mechanism to value long-duration storage. In practice, the inflexible rules within the regulatory framework have made it more cost-effective to procure two 4-hour battery energy storage systems than one 8-hour long-duration system. This inflexibility also drives CAISO load-serving entities to use thermal resources to ensure overnight reliability. And in PJM, a 9x surge in capacity price has ratepayers paying every MW of generation at Net-CONE, despite single digit percent growth: each year, PJM is paying for 20x the resources that are actually newly installed.

Decarbonizing US energy markets requires tackling multiple issues in the near term. First, long-duration energy storage (LDES) is not currently cost-competitive with either short-duration storage or natural gas combustion turbines (CTs). Hundred-hour LDES can only beat CTs as a long-duration reliability resource with some large assumptions about accreditation: namely, if market stakeholders believe a marginal peaking event will be less than 100 hours, than a 100% effective load carrying capability (ELCC) can be assumed for LDES. Considering that Winter Storm Elliot in PJM lasted longer than 100 hours in December 2022, a 100% ELCC assumption would not likely find unanimous support.

The current CT supply chain shortage, which has pushed up CT cost estimates for 2030 delivery by more than 100%, also shapes the context for LDES cost-competitiveness. If peaks are shorter than 100 hours, and if CT costs remain elevated, then LDES becomes an economically viable solution.

Carbon tax policies are also likely needed to incentivize a transition to the use of non-thermal resources for overnight generation. Carbon prices disproportionally increase prices on a day's peak, which can boost energy arbitrage margins without flowing those dollars to carbon-emitting resources. For the foreseeable future, natural gas will remain the less expensive option per unit of energy; however, a carbon tax can make renewable fuel costs comparatively less 'after tax.'

There also exist two interesting non-hydrogen, non-storage solutions. Hybrid peaker-storage units represent a potentially useful compromise, and one that is beginning to appear in California. From a reliability planning perspective, the most efficient way to ensure 1-in-10 year system safety is to not retire existing assets and simply hybridize existing units to reduce legacy unit runtime and efficiently interconnect new clean resources. Nuclear energy is also enjoying a renaissance among certain energy market stakeholders, including the previous and current US presidential administrations. However, justifying the exorbitant cost of building nuclear, rather than any other resource, will be difficult.

Finally, solving decarbonization issues in US energy markets will require radical market restructuring. Whether the appetite to do so (and the ability to make it happen) exists remains questionable.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)