Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

While clean energy in US energy markets faces severe federal policy headwinds with several poison pills in the budget passed by the House, opportunities for clean energy development and offtake still exist. Continued state policy commitments and corporate demand create an ongoing floor for clean energy development. The immense scale of data center-driven load growth largely necessitates an all-resources approach, with many hyperscalers still pursuing carbon-free energy supply. Future adjustments to federal tax policies remain possible, and technology cost declines may happen rapidly enough to potentially offset much of the loss of tax credits.

At the Ascend Analytics 2025 Power Markets workshop, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss the policy and offtake outlook for clean energy, soaring load growth, the value transfer from energies and ancillaries into capacity, and energy market outlooks by asset class.

In the current US energy policy environment – especially at the federal level – the only certainty is uncertainty. Despite headwinds caused by tariffs, as well as development timeline and supply restriction poison pills in the proposed House budget bill, potential bright spots exist. For example, President Trump has shown a tendency to back off policy positions that produce negative market reactions. A variety of court cases are challenging executive orders, with a bipartisan US trade court having recently struck down reciprocal tariffs (although the decision was stayed while the appeals process continues). The Senate may well prove to be a moderating influence on the draconian budget that the House passed by a single vote. Reality matters, too: all sources of energy will be needed if there is even a remote chance of serving the load needed to power AI-related data center growth.

The outlook for tax credits may also be more positive than what is reflected in the current House budget bill, which effectively eliminates all tax credits for renewables not safe-harbored by the end of 2024 through unworkable and ill-defined Foreign Entity of Concern (FEOC) restrictions. As the bill goes through the reconciliation process, there will be pressure on Congress to remove the most damaging elements of energy policy.

Regardless of federal policy, state policy and corporate demand for clean energy will continue. Roughly half of US load occurs in states with clean energy mandates, thus producing a floor for clean energy demand that derives from state policy. In addition, offtake contracts will continue as some of the largest drivers of load growth are corporates with relatively firm clean energy commitments.

Willingness to pay, however, is not unlimited. Affordability concerns have been growing, even in states, such as New York, Massachusetts, and California, with strong commitments to renewable development. While these concerns will likely not cause states to abandon clean energy goals, they may slow their path to decarbonization.

While policy uncertainty surrounds energy markets, one thing remains clear: demand growth is increasing at rates not seen in half a century, which is driving an acute need for new generation capacity. Demand from electrification alone could double current electricity needs. This need is compounded by thermal retirements, onshoring of manufacturing, and load growth from data centers.

Assessing just how much generation will be needed to meet this demand becomes more complicated. The uncertainty alone in data center demand is immense: anywhere from 30-65 GW of potential growth have been projected over the next four years.

At the same time, natural gas combustion turbine (NGCT) supply remains extremely limited, with five-year wait times. Consequently, skyrocketing prices mean that prohibitively high costs are both constraining the pace of new build and creating significant cost risks for new gas plant development during this period of inflated costs. Given these dynamics, there is no realistic way to meet demand with just gas.

Ultimately, the only resources that can realistically meet load growth are those already in the interconnection queue, which are primarily clean resources, although there are some efforts to create expedited interconnection processes for dispatchable generation. However, NGCT supply constraints and federal policy uncertainty for renewables and storage are impeding project development.

In energy markets across the US, Ascend expects a value transfer from ancillaries and energy into capacity. Even outside of states with clean energy mandates, renewables will continue to impact wholesale prices and avoided costs. Pure economics create an upper bound on power prices, with renewables causing declining heat rates. In addition, clean energy policies in many states allow buildout in other states, causing price depression that amplifies beyond simply those states with clean energy mandates.

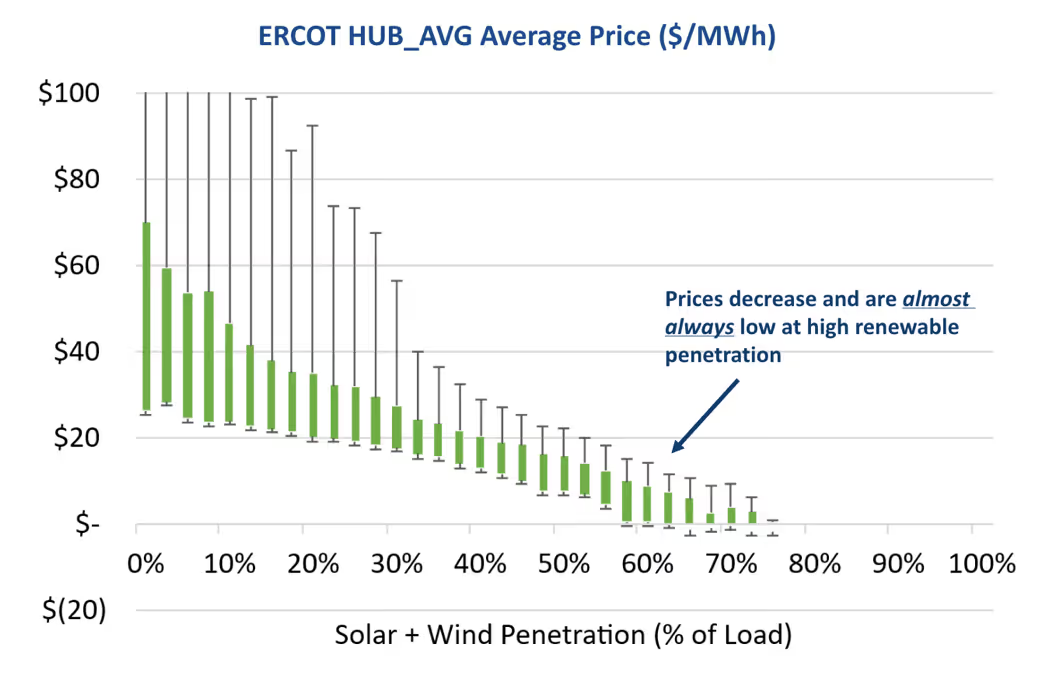

And where renewable resources are present, energy prices will be low. As seen in Figure 1, high renewable penetrations do not just cause prices to go low on average: high rates of penetration mean that prices are almost always low, which means an inability for other generation to earn margin most of the time as well as more price volatility.

Similarly, high rates of storage deployment cause rapid declines in ancillary prices, which reflect the opportunity costs for storage once storage becomes a price-setter. Ancillary services markets are already saturated with storage in California and ERCOT. Storage growth across other ISOs will produce the same effect.

Winter reliability risks also present major challenges for all asset classes. Renewables will see minimal capacity value as critical reliability periods will inherently be associated with low renewable production. Storage will see declining capacity accreditation as its penetration in the supply stack grows and shaved peaks widen. Marginal effective load carrying capability (ELCC) accreditation accelerates the decline. These dynamics can already be seen in PJM, where the risk of winter-peaking for reliability has been recognized through load accreditation for thermal generation and storage. Declining accreditation produces serious implications for capacity prices, which must rise correspondingly in order to compensate for the loss in accreditation.

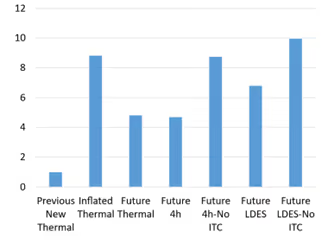

Thus, capacity prices will need to be sufficient to drive new unit entry, which means that capacity prices will go high and stay there. In locations with clean energy mandates, capacity prices will rise to levels needed for long-duration energy storage, as shown in Figure 2, while in markets where thermal generation can still enter, prices will likely persist close to thermal Gross CONE revenue requirements. With capacity prices and value growing, the most important ability for resource classes will be availability during scarcity conditions. In the long run, this means that ISOs are likely to be oversupplied for most of the year and in most years, which means energy prices will generally be low.

For thermal resources, availability when other resources are not available is imperative as performance during scarcity conditions becomes increasingly important. So too does preventative maintenance, weather-hardening, and the ability to secure fuel supply. For gas, sold-out order books for turbine manufacturers will severely constrain the ability to meet near-term load growth. Inflated near-term CapEx and expected backwardation create severe development risk for gas turbines, with later gas projects able to outcompete near-term ones. However, reciprocating engines may be well-positioned for the near term as a flexible, lower-cost capacity resource.

Due primarily to prohibitively high costs, nuclear is not a viable option to meet soaring energy demand for any stakeholders that are cost-sensitive. Much of the interest in nuclear generation as a carbon-free resource will likely diminish when the bill comes due, with the exception of regulated utilities with incentives to pursue expensive generation options under regulatory commissions that accommodate these high-cost options. In the near term, corporates might be willing to pay for nuclear, due to the need to move quickly as well as a relative lack of cost sensitivity. For ratepayers, however, nuclear should be an expensive and untenable option.

For renewables and storage, offtake remains necessary. While increased project costs from tax credit removals will partially reduce demand, many large corporates and states remain committed to clean energy goals, creating a resilient offtake pool. For storage, policy will still continue to drive development, as will growing offtake demand from corporates pursuing emissions reductions and clean energy load matching. For markets with low storage penetration, some storage makes economic sense as long as total storage penetration remains low and capacity accreditation remains high.

With regard to behind-the-meter (BTM) generation and virtual power plants (VPP), the economics should be changing positively. As system costs become increasingly concentrated in narrow periods of time, the value of BTM generation and load reduction/flexibility during critical conditions will grow in value. Retail rate designs tend to lag behind wholesale market trends, creating additional value for BTM peak-shifting resources amid declining capacity accreditation in wholesale markets. To create further incentives to reduce demand and keep peaks low, utilities and retailers should re-evaluate and redesign retail rates in recognition of shifting drivers of system costs.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

While clean energy in US energy markets faces severe federal policy headwinds with several poison pills in the budget passed by the House, opportunities for clean energy development and offtake still exist. Continued state policy commitments and corporate demand create an ongoing floor for clean energy development. The immense scale of data center-driven load growth largely necessitates an all-resources approach, with many hyperscalers still pursuing carbon-free energy supply. Future adjustments to federal tax policies remain possible, and technology cost declines may happen rapidly enough to potentially offset much of the loss of tax credits.

At the Ascend Analytics 2025 Power Markets workshop, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss the policy and offtake outlook for clean energy, soaring load growth, the value transfer from energies and ancillaries into capacity, and energy market outlooks by asset class.

In the current US energy policy environment – especially at the federal level – the only certainty is uncertainty. Despite headwinds caused by tariffs, as well as development timeline and supply restriction poison pills in the proposed House budget bill, potential bright spots exist. For example, President Trump has shown a tendency to back off policy positions that produce negative market reactions. A variety of court cases are challenging executive orders, with a bipartisan US trade court having recently struck down reciprocal tariffs (although the decision was stayed while the appeals process continues). The Senate may well prove to be a moderating influence on the draconian budget that the House passed by a single vote. Reality matters, too: all sources of energy will be needed if there is even a remote chance of serving the load needed to power AI-related data center growth.

The outlook for tax credits may also be more positive than what is reflected in the current House budget bill, which effectively eliminates all tax credits for renewables not safe-harbored by the end of 2024 through unworkable and ill-defined Foreign Entity of Concern (FEOC) restrictions. As the bill goes through the reconciliation process, there will be pressure on Congress to remove the most damaging elements of energy policy.

Regardless of federal policy, state policy and corporate demand for clean energy will continue. Roughly half of US load occurs in states with clean energy mandates, thus producing a floor for clean energy demand that derives from state policy. In addition, offtake contracts will continue as some of the largest drivers of load growth are corporates with relatively firm clean energy commitments.

Willingness to pay, however, is not unlimited. Affordability concerns have been growing, even in states, such as New York, Massachusetts, and California, with strong commitments to renewable development. While these concerns will likely not cause states to abandon clean energy goals, they may slow their path to decarbonization.

While policy uncertainty surrounds energy markets, one thing remains clear: demand growth is increasing at rates not seen in half a century, which is driving an acute need for new generation capacity. Demand from electrification alone could double current electricity needs. This need is compounded by thermal retirements, onshoring of manufacturing, and load growth from data centers.

Assessing just how much generation will be needed to meet this demand becomes more complicated. The uncertainty alone in data center demand is immense: anywhere from 30-65 GW of potential growth have been projected over the next four years.

At the same time, natural gas combustion turbine (NGCT) supply remains extremely limited, with five-year wait times. Consequently, skyrocketing prices mean that prohibitively high costs are both constraining the pace of new build and creating significant cost risks for new gas plant development during this period of inflated costs. Given these dynamics, there is no realistic way to meet demand with just gas.

Ultimately, the only resources that can realistically meet load growth are those already in the interconnection queue, which are primarily clean resources, although there are some efforts to create expedited interconnection processes for dispatchable generation. However, NGCT supply constraints and federal policy uncertainty for renewables and storage are impeding project development.

In energy markets across the US, Ascend expects a value transfer from ancillaries and energy into capacity. Even outside of states with clean energy mandates, renewables will continue to impact wholesale prices and avoided costs. Pure economics create an upper bound on power prices, with renewables causing declining heat rates. In addition, clean energy policies in many states allow buildout in other states, causing price depression that amplifies beyond simply those states with clean energy mandates.

And where renewable resources are present, energy prices will be low. As seen in Figure 1, high renewable penetrations do not just cause prices to go low on average: high rates of penetration mean that prices are almost always low, which means an inability for other generation to earn margin most of the time as well as more price volatility.

Similarly, high rates of storage deployment cause rapid declines in ancillary prices, which reflect the opportunity costs for storage once storage becomes a price-setter. Ancillary services markets are already saturated with storage in California and ERCOT. Storage growth across other ISOs will produce the same effect.

Winter reliability risks also present major challenges for all asset classes. Renewables will see minimal capacity value as critical reliability periods will inherently be associated with low renewable production. Storage will see declining capacity accreditation as its penetration in the supply stack grows and shaved peaks widen. Marginal effective load carrying capability (ELCC) accreditation accelerates the decline. These dynamics can already be seen in PJM, where the risk of winter-peaking for reliability has been recognized through load accreditation for thermal generation and storage. Declining accreditation produces serious implications for capacity prices, which must rise correspondingly in order to compensate for the loss in accreditation.

Thus, capacity prices will need to be sufficient to drive new unit entry, which means that capacity prices will go high and stay there. In locations with clean energy mandates, capacity prices will rise to levels needed for long-duration energy storage, as shown in Figure 2, while in markets where thermal generation can still enter, prices will likely persist close to thermal Gross CONE revenue requirements. With capacity prices and value growing, the most important ability for resource classes will be availability during scarcity conditions. In the long run, this means that ISOs are likely to be oversupplied for most of the year and in most years, which means energy prices will generally be low.

For thermal resources, availability when other resources are not available is imperative as performance during scarcity conditions becomes increasingly important. So too does preventative maintenance, weather-hardening, and the ability to secure fuel supply. For gas, sold-out order books for turbine manufacturers will severely constrain the ability to meet near-term load growth. Inflated near-term CapEx and expected backwardation create severe development risk for gas turbines, with later gas projects able to outcompete near-term ones. However, reciprocating engines may be well-positioned for the near term as a flexible, lower-cost capacity resource.

Due primarily to prohibitively high costs, nuclear is not a viable option to meet soaring energy demand for any stakeholders that are cost-sensitive. Much of the interest in nuclear generation as a carbon-free resource will likely diminish when the bill comes due, with the exception of regulated utilities with incentives to pursue expensive generation options under regulatory commissions that accommodate these high-cost options. In the near term, corporates might be willing to pay for nuclear, due to the need to move quickly as well as a relative lack of cost sensitivity. For ratepayers, however, nuclear should be an expensive and untenable option.

For renewables and storage, offtake remains necessary. While increased project costs from tax credit removals will partially reduce demand, many large corporates and states remain committed to clean energy goals, creating a resilient offtake pool. For storage, policy will still continue to drive development, as will growing offtake demand from corporates pursuing emissions reductions and clean energy load matching. For markets with low storage penetration, some storage makes economic sense as long as total storage penetration remains low and capacity accreditation remains high.

With regard to behind-the-meter (BTM) generation and virtual power plants (VPP), the economics should be changing positively. As system costs become increasingly concentrated in narrow periods of time, the value of BTM generation and load reduction/flexibility during critical conditions will grow in value. Retail rate designs tend to lag behind wholesale market trends, creating additional value for BTM peak-shifting resources amid declining capacity accreditation in wholesale markets. To create further incentives to reduce demand and keep peaks low, utilities and retailers should re-evaluate and redesign retail rates in recognition of shifting drivers of system costs.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)