Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Version 9.4 of SmartBidder was released into production last Thursday. Notable updates include the following:

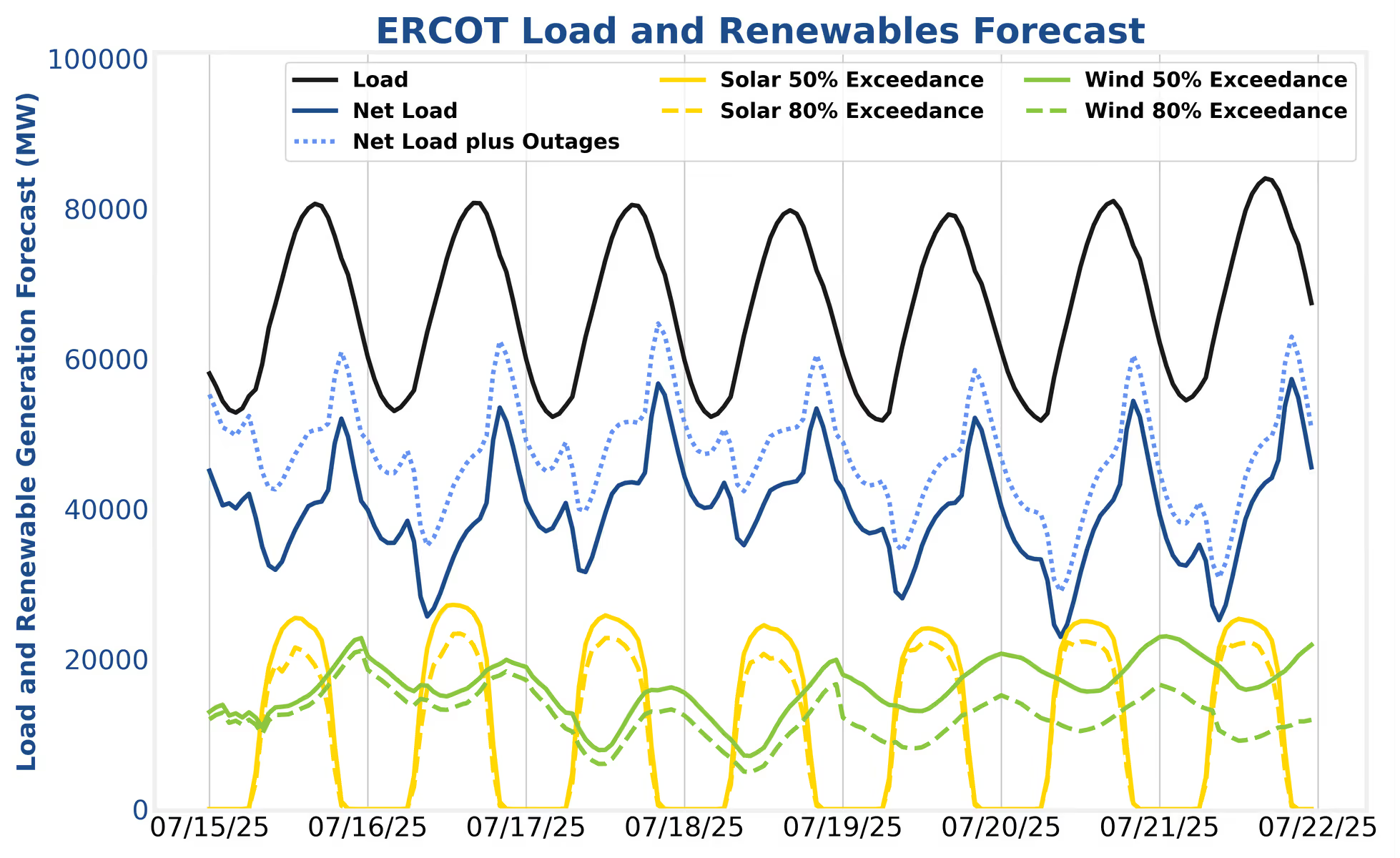

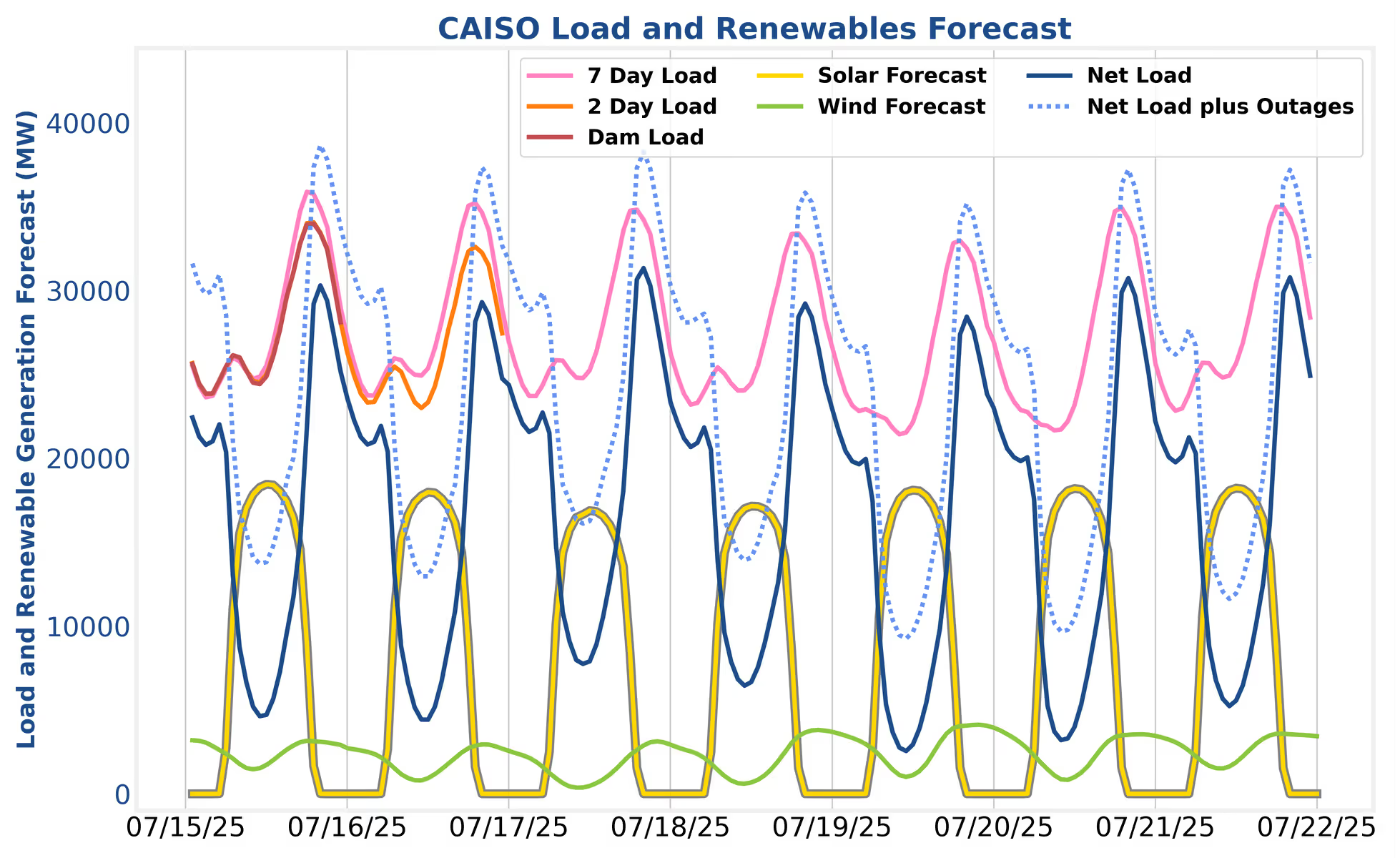

For the week of July 16th – 23rd, net load levels will stay below the moderate benchmark of 60 GW in ERCOT and only barely breach the similarly moderate benchmark of 30 GW in CAISO. Asset operators should work out their strategy and operational kinks while they can. August is right around the corner.

In ERCOT, despite gross load peak levels stepping up to over 80 GW, strong wind production will quench net load peaks next week. Traders should concentrate their efforts on the day-ahead versus real-time energy decision making process as AS value continues to erode relative to energy value.

In CAISO, day-ahead energy discharging prices continue to outperform real-time participation, as significant supply stack buildout will make real-time price blowouts difficult to capitalize on for the foreseeable future. Operators should concentrate on day-ahead energy discharge and revenue augmentation via AS.

Despite gross load peaks consistently hitting above 80 GW, net loads will not approach elevated levels given a strong solar/wind one-two-punch in the afternoons and evenings. HE17 gross load peaks (up to 84 GW on the 21st) are offset by ~25 GW of solar production, while wind production ramps up in the evenings to maintain lower net load as gross load and solar production drop off. The afternoon time periods are starting to become very sensitive to solar production forecast misses. A 5% solar forecast miss a few years ago was a small fraction of a GW deficit in the supply stack. Today, a 5% solar forecast miss is over a GW and can induce serious afternoon volatility that may sustain into the evening if wind production doesn’t ramp up as load ramps down. The myriad of weather-dependent factors at play (load, wind, and now solar), combined with the game theory elements of storage participation, enable operators who leverage massive amounts of data and state-of-the-art modeling to react to market probabilities and outcomes before they happen. This philosophy is the foundation of the SmartBidder Mt. Blue Sky and Longs Peak strategies, which have been created, trained, and tuned to charge towards volatility and discharge out of it.

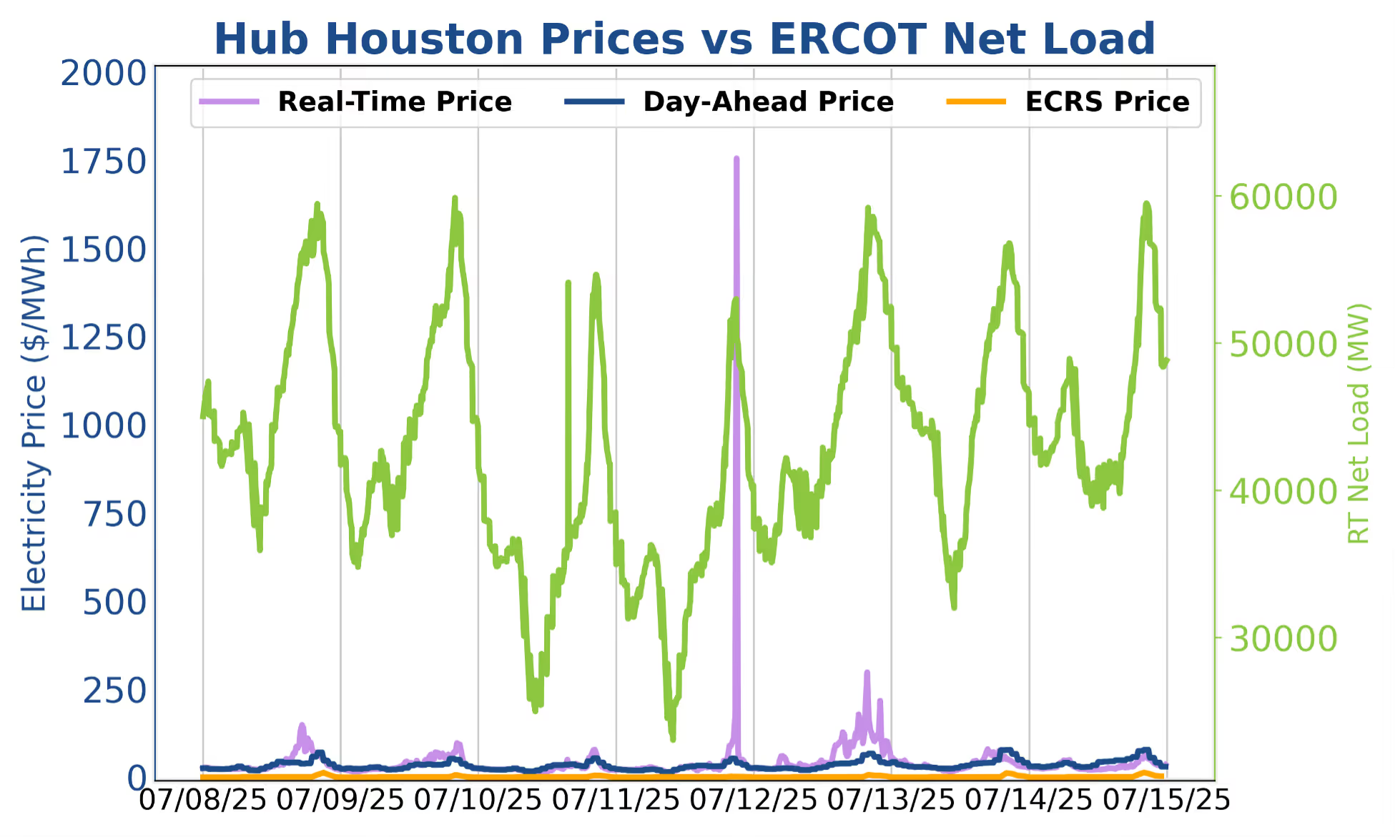

Friday night volatility continued in ERCOT last week as LMPs breached $4,000 system-wide for the first time this summer. The spike struck right at the start of HE22 over day-ahead prices around $60/MWh. Tight conditions in HE21 indicated volatility was in the mix. LMP prints before and after the spike were $250/MWh as the grid quickly responded. The evening of the 11th was the fourth of five straight days of real-time price outperformance in ERCOT that rewarded operators who forwent day-ahead energy commitments and punished operators who sold day-ahead virtual energy. The 14th was a return to more typical day-ahead outperformance.

Net load peaks will exceed 30 GW on the 17th but will not engender any major market events. On the charging side, solar production will fluctuate slightly more than usual, which could shake up charging DART spreads. Operators also need to be keeping a close eye on local congestion as heat lowers transmission carrying capacity and induces peculiar load patterns due to air conditioning demand. At a macro level, operators should target day-ahead energy discharge and as much regulation as they can take on without interfering with the bulk of their day-ahead capture. Talk to your analyst about tuning the Mt. Shasta strategy to fit your risk tolerance.

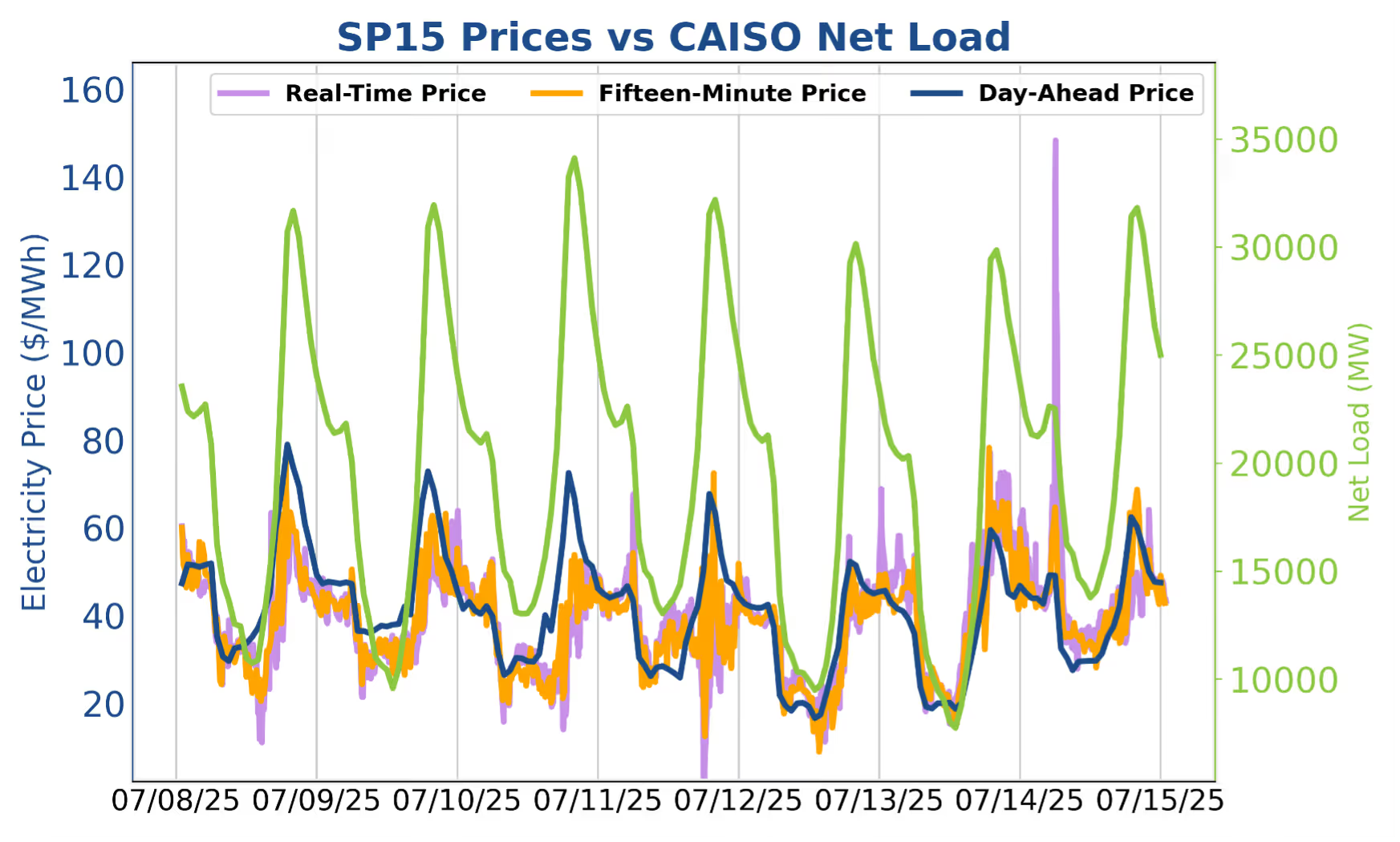

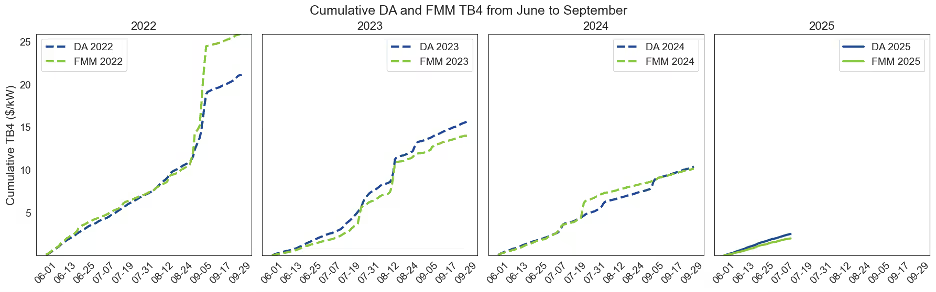

As shown in the standard weekly chart above and in the holistic yearly chart below, day-ahead market participation in CAISO is yielding incrementally more value versus making a living off of real-time fifteen-minute prices. Operators should favor day-ahead energy discharge as much as possible. Real-time price blowouts can still occur but will only happen under improbable conditions (i.e. massive load forecast miss in day-ahead combined with extremely high levels of BESS commitment in day-ahead). Relative to past summers, CAISO TB4 spreads in both markets are keeping pace with 2024 but are substantially below 2022 and 2023. August and September are typically the most lucrative months, so it remains to be seen if 2025 can muster some momentum or if it will continue crawling along.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Version 9.4 of SmartBidder was released into production last Thursday. Notable updates include the following:

For the week of July 16th – 23rd, net load levels will stay below the moderate benchmark of 60 GW in ERCOT and only barely breach the similarly moderate benchmark of 30 GW in CAISO. Asset operators should work out their strategy and operational kinks while they can. August is right around the corner.

In ERCOT, despite gross load peak levels stepping up to over 80 GW, strong wind production will quench net load peaks next week. Traders should concentrate their efforts on the day-ahead versus real-time energy decision making process as AS value continues to erode relative to energy value.

In CAISO, day-ahead energy discharging prices continue to outperform real-time participation, as significant supply stack buildout will make real-time price blowouts difficult to capitalize on for the foreseeable future. Operators should concentrate on day-ahead energy discharge and revenue augmentation via AS.

Despite gross load peaks consistently hitting above 80 GW, net loads will not approach elevated levels given a strong solar/wind one-two-punch in the afternoons and evenings. HE17 gross load peaks (up to 84 GW on the 21st) are offset by ~25 GW of solar production, while wind production ramps up in the evenings to maintain lower net load as gross load and solar production drop off. The afternoon time periods are starting to become very sensitive to solar production forecast misses. A 5% solar forecast miss a few years ago was a small fraction of a GW deficit in the supply stack. Today, a 5% solar forecast miss is over a GW and can induce serious afternoon volatility that may sustain into the evening if wind production doesn’t ramp up as load ramps down. The myriad of weather-dependent factors at play (load, wind, and now solar), combined with the game theory elements of storage participation, enable operators who leverage massive amounts of data and state-of-the-art modeling to react to market probabilities and outcomes before they happen. This philosophy is the foundation of the SmartBidder Mt. Blue Sky and Longs Peak strategies, which have been created, trained, and tuned to charge towards volatility and discharge out of it.

Friday night volatility continued in ERCOT last week as LMPs breached $4,000 system-wide for the first time this summer. The spike struck right at the start of HE22 over day-ahead prices around $60/MWh. Tight conditions in HE21 indicated volatility was in the mix. LMP prints before and after the spike were $250/MWh as the grid quickly responded. The evening of the 11th was the fourth of five straight days of real-time price outperformance in ERCOT that rewarded operators who forwent day-ahead energy commitments and punished operators who sold day-ahead virtual energy. The 14th was a return to more typical day-ahead outperformance.

Net load peaks will exceed 30 GW on the 17th but will not engender any major market events. On the charging side, solar production will fluctuate slightly more than usual, which could shake up charging DART spreads. Operators also need to be keeping a close eye on local congestion as heat lowers transmission carrying capacity and induces peculiar load patterns due to air conditioning demand. At a macro level, operators should target day-ahead energy discharge and as much regulation as they can take on without interfering with the bulk of their day-ahead capture. Talk to your analyst about tuning the Mt. Shasta strategy to fit your risk tolerance.

As shown in the standard weekly chart above and in the holistic yearly chart below, day-ahead market participation in CAISO is yielding incrementally more value versus making a living off of real-time fifteen-minute prices. Operators should favor day-ahead energy discharge as much as possible. Real-time price blowouts can still occur but will only happen under improbable conditions (i.e. massive load forecast miss in day-ahead combined with extremely high levels of BESS commitment in day-ahead). Relative to past summers, CAISO TB4 spreads in both markets are keeping pace with 2024 but are substantially below 2022 and 2023. August and September are typically the most lucrative months, so it remains to be seen if 2025 can muster some momentum or if it will continue crawling along.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)