Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

For the week of July 3rd – 10th, CAISO chugs along with no major revenue opportunities in sight while lower wind production in ERCOT could lead to volatile prices if heat shows up after the holiday.

In ERCOT, there will be no fireworks on the Fourth of July holiday as strong wind production will keep net load to low levels. Wind production is forecasted to ramp down by the 6th and 7th as slightly hotter temperatures roll in.

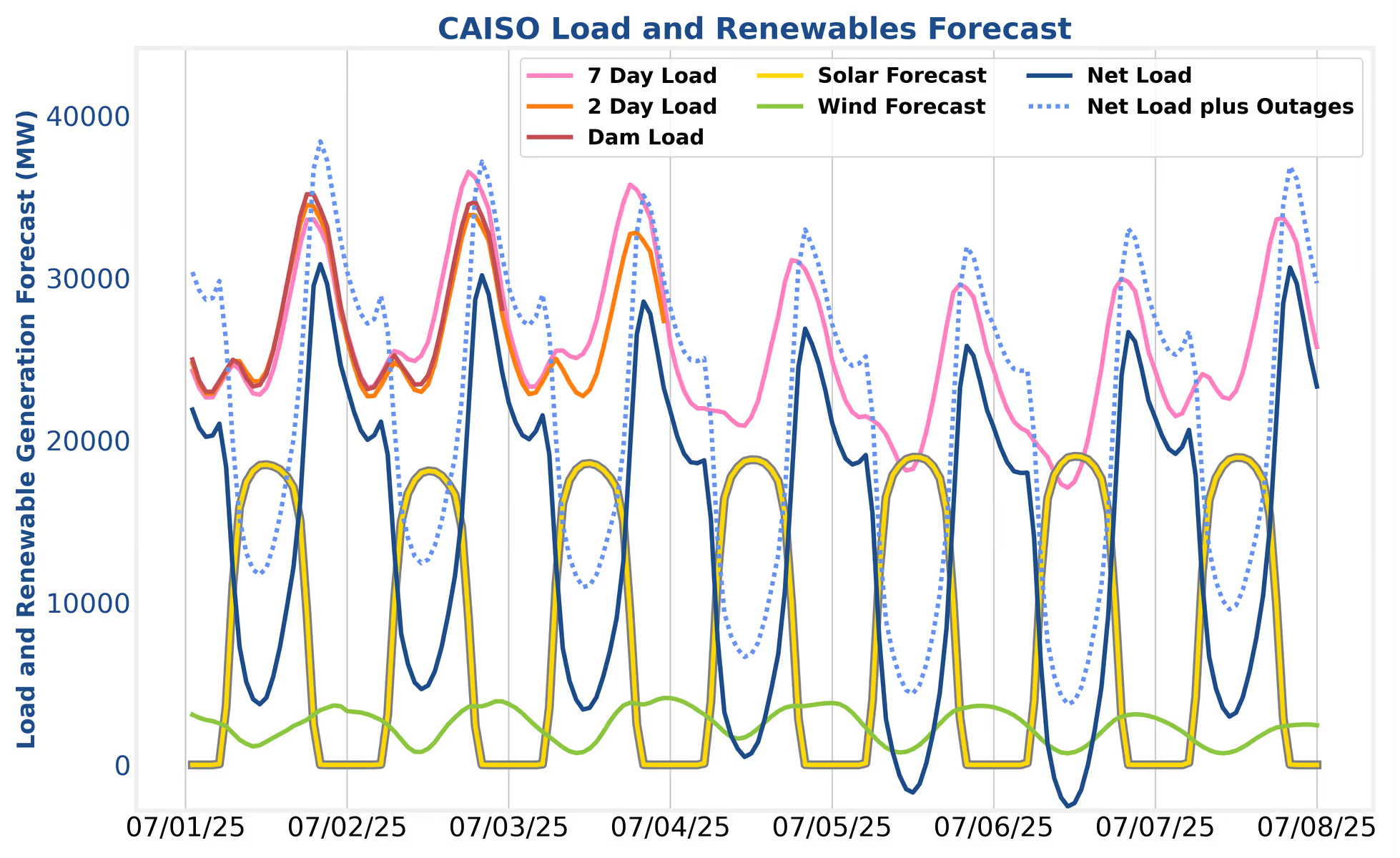

In CAISO, net load peaks will cool off heading into the Fourth of July holiday. Peaks will be back to 30 GW by the 7th.

ERCOT is looking calm for the 2nd through 5th and asset operators will not need to worry about missing major market opportunities over the holiday(assuming this newsletter doesn’t jinx a massive wind forecast error). The market will be more interesting again the following week as wind production ramps down and gross load ticks up slightly due to warmer temperatures. For now, operators should continue rolling with their standard summer strategies. Lower non-spin procurement during the evening peak in July has increased the value of spinning reserve and ECRS relative to non-spin. SmartBidder is equipped to handle this natively by offering participation in each ancillary services (AS)during the peak based on the opportunity cost of clearing/non-clearing.

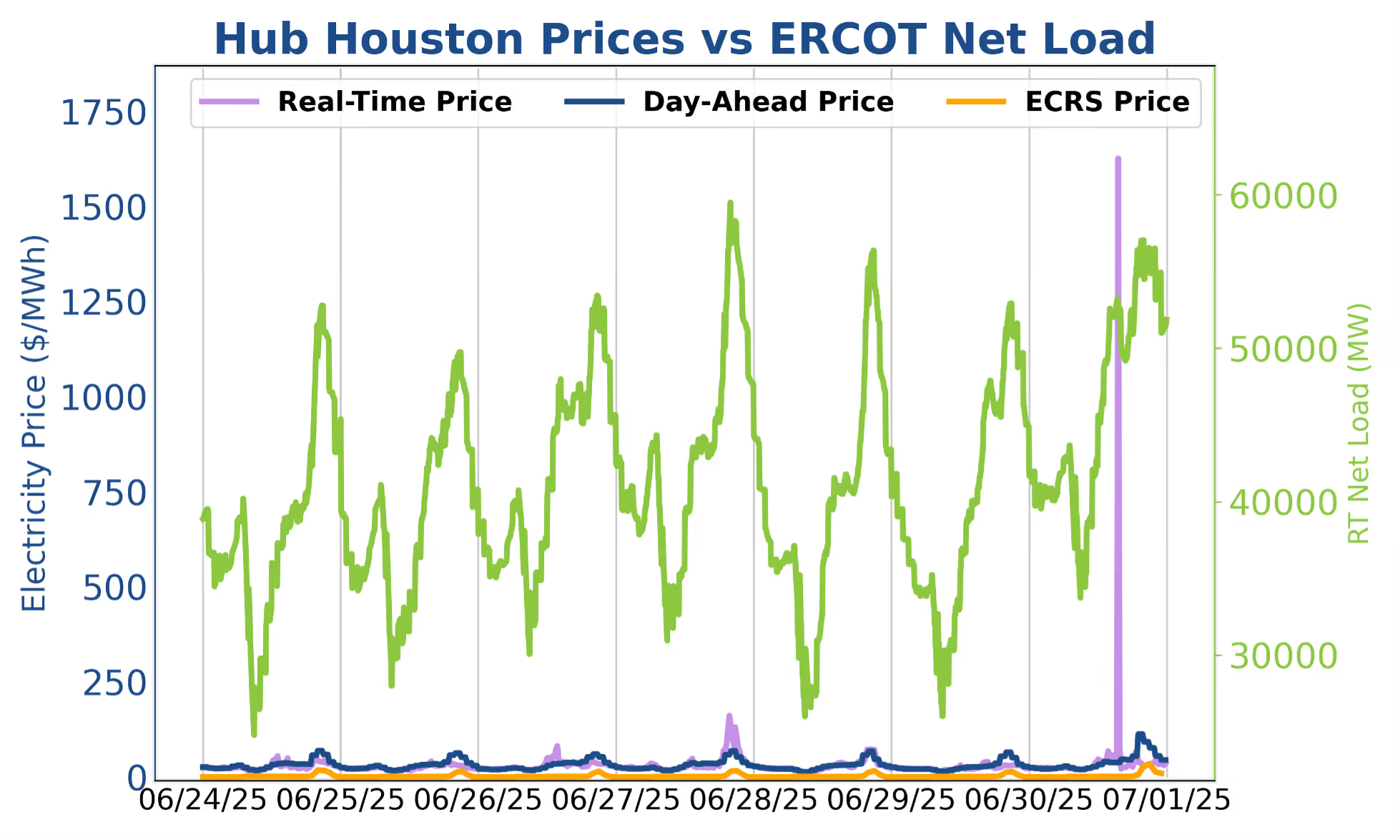

Net load has started to reach up towards true summer levels in ERCOT, but as of this writing the market is yet to experience the thin market conditions that create sustained high evening prices. Settlement point prices spiked briefly on the afternoon of the 30th but load curtailed and wind picked up enough to prevent even a moderate revenue opportunity in the evening. Net load nearly hit 60GW on the 27th as well, and real-time prices were a few hundred dollars at many nodes. Other days this week, day ahead (DA) prices during the evening were preferable. With summer here, it’s time to talk to your analyst about limiting day-ahead energy participation to create real-time exposure for price spikes. SmartBidder’s Mt. Blue Sky strategy is designed to use opportunity costs to offer a mixture of AS and energy that provides consistent returns under all market conditions.

Load is not expected to be extraordinary this week in CAISO, with temperatures in Los Angeles still getting down into the low 60s overnight. The SmartBidder team is pegging 38 GW as the peak net load threshold for potential real-time exposure to be able to strongly out perform a day-ahead energy heavy strategy. For this week, with consistent overnight wind and cool evening temperatures, net load is barely expected to crack 30 GW.A strategy that participates more heavily in the day-ahead market is recommended, while leaving some room for real-time exposure. The exception is the 5th and 6th when negative net load could push real-time charging prices below day-ahead levels and shift the balance towards areal-time strategy.

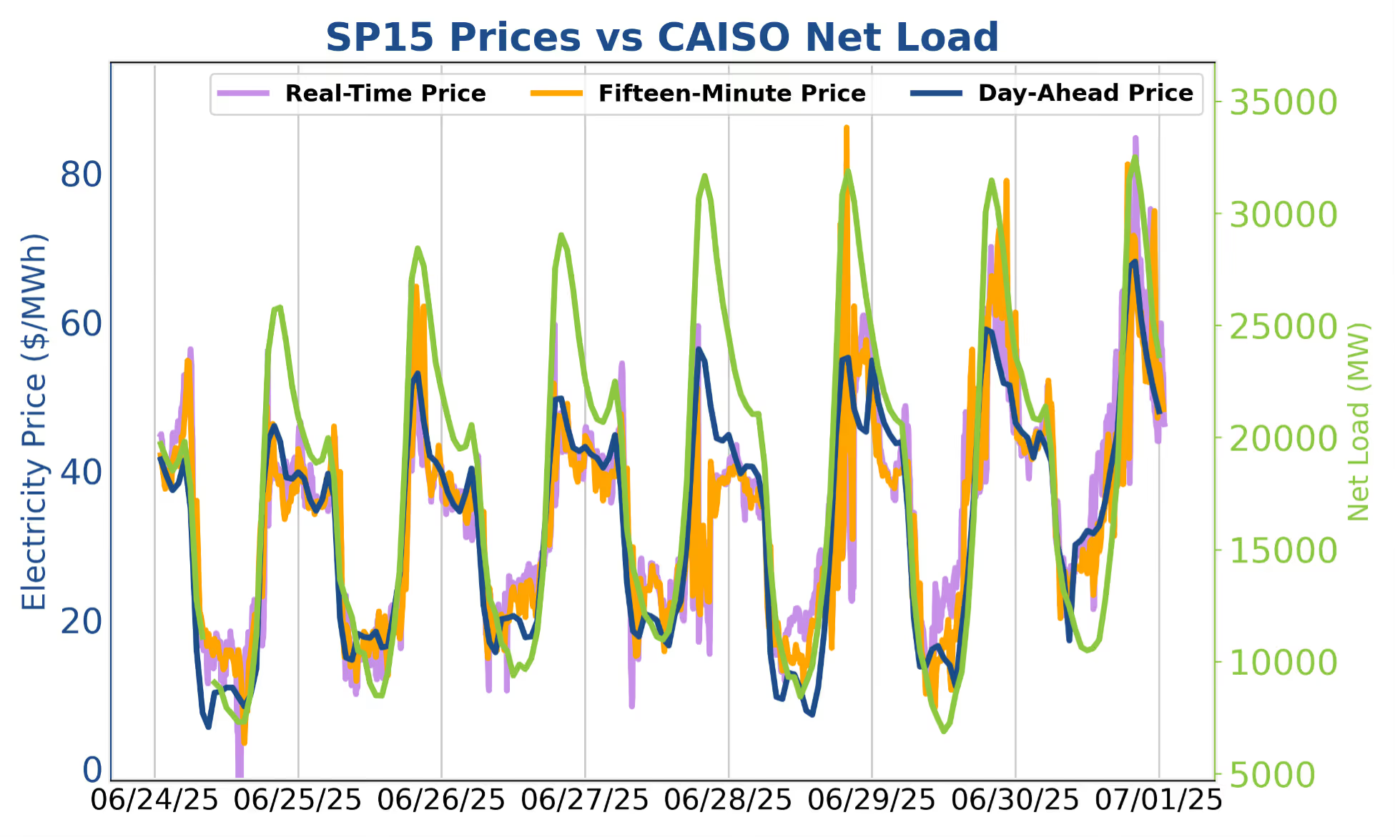

Last week marked the first full week of summer, and CAISO celebrated by dipping its toes into slightly improved real-time volatility. Evening real-time prices exceeded day-ahead prices for three consecutive days on the 28th, 29th, and 30th, although average day-ahead charging prices remained lower than their real-time counterparts. However, it wasn’t all sunshine and tan lines for evening real-time pricing: on the evening of the 27th, evening discharge prices sank, with the fifteen-minute market (FMM) settling in double digits below the day-ahead price.

Operators should be wary of diving headfirst into increased real-time participation just yet, as net load has remained fairly tame—near or below 30 MW overall. As we continue into summer, these elevated evening real-time prices may become more common, but days like the 27th are good reminders that a blend of day-ahead and real-time energy remains the healthiest approach for now. Operators who cleared day-ahead charging while simultaneously placing day-ahead discharge bids, priced with consideration of the opportunity cost of real-time participation, were currently best positioned for this past week.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

For the week of July 3rd – 10th, CAISO chugs along with no major revenue opportunities in sight while lower wind production in ERCOT could lead to volatile prices if heat shows up after the holiday.

In ERCOT, there will be no fireworks on the Fourth of July holiday as strong wind production will keep net load to low levels. Wind production is forecasted to ramp down by the 6th and 7th as slightly hotter temperatures roll in.

In CAISO, net load peaks will cool off heading into the Fourth of July holiday. Peaks will be back to 30 GW by the 7th.

ERCOT is looking calm for the 2nd through 5th and asset operators will not need to worry about missing major market opportunities over the holiday(assuming this newsletter doesn’t jinx a massive wind forecast error). The market will be more interesting again the following week as wind production ramps down and gross load ticks up slightly due to warmer temperatures. For now, operators should continue rolling with their standard summer strategies. Lower non-spin procurement during the evening peak in July has increased the value of spinning reserve and ECRS relative to non-spin. SmartBidder is equipped to handle this natively by offering participation in each ancillary services (AS)during the peak based on the opportunity cost of clearing/non-clearing.

Net load has started to reach up towards true summer levels in ERCOT, but as of this writing the market is yet to experience the thin market conditions that create sustained high evening prices. Settlement point prices spiked briefly on the afternoon of the 30th but load curtailed and wind picked up enough to prevent even a moderate revenue opportunity in the evening. Net load nearly hit 60GW on the 27th as well, and real-time prices were a few hundred dollars at many nodes. Other days this week, day ahead (DA) prices during the evening were preferable. With summer here, it’s time to talk to your analyst about limiting day-ahead energy participation to create real-time exposure for price spikes. SmartBidder’s Mt. Blue Sky strategy is designed to use opportunity costs to offer a mixture of AS and energy that provides consistent returns under all market conditions.

Load is not expected to be extraordinary this week in CAISO, with temperatures in Los Angeles still getting down into the low 60s overnight. The SmartBidder team is pegging 38 GW as the peak net load threshold for potential real-time exposure to be able to strongly out perform a day-ahead energy heavy strategy. For this week, with consistent overnight wind and cool evening temperatures, net load is barely expected to crack 30 GW.A strategy that participates more heavily in the day-ahead market is recommended, while leaving some room for real-time exposure. The exception is the 5th and 6th when negative net load could push real-time charging prices below day-ahead levels and shift the balance towards areal-time strategy.

Last week marked the first full week of summer, and CAISO celebrated by dipping its toes into slightly improved real-time volatility. Evening real-time prices exceeded day-ahead prices for three consecutive days on the 28th, 29th, and 30th, although average day-ahead charging prices remained lower than their real-time counterparts. However, it wasn’t all sunshine and tan lines for evening real-time pricing: on the evening of the 27th, evening discharge prices sank, with the fifteen-minute market (FMM) settling in double digits below the day-ahead price.

Operators should be wary of diving headfirst into increased real-time participation just yet, as net load has remained fairly tame—near or below 30 MW overall. As we continue into summer, these elevated evening real-time prices may become more common, but days like the 27th are good reminders that a blend of day-ahead and real-time energy remains the healthiest approach for now. Operators who cleared day-ahead charging while simultaneously placing day-ahead discharge bids, priced with consideration of the opportunity cost of real-time participation, were currently best positioned for this past week.

The information provided in this newsletter is for educational and informational purposes only and should not be considered trading advice. Trading in energy markets carries inherent risks and short and medium-term forecasts are always subject to change and revision.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power supply, procurement, and investment markets to plan, operate, monetize, and manage risk across any energy asset portfolio. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

©2026 Ascend Analytics. All rights reserved. Privacy Policy.

-3.png)

.avif)