Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

.avif)

In California, a relative glut of energy capacity and lack of structural electricity demand growth have combined to make negative energy prices and curtailment increasingly prevalent during solar-generating hours throughout a growing number of months of the year. At the same time, overnight generation remains emissions-intensive and driven by gas prices while fundamental incompatibilities between the state's resource adequacy (RA) compliance structure and the California independent system operator's (CAISO) interconnection processes impede state clean energy goals. With potential for further price pressure due to federal policies and uncertain macroeconomic conditions, utilities, investors, and load-serving entities (LSEs) face serious challenges – and also have opportunities when it comes to storage.

In a webinar previewing Ascend's most recent CAISO power market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss the implications of federal tariffs, potential changes to the IRA, the costs of California meeting its clean energy goals, and the corresponding outlook for power, RA, and REC prices.

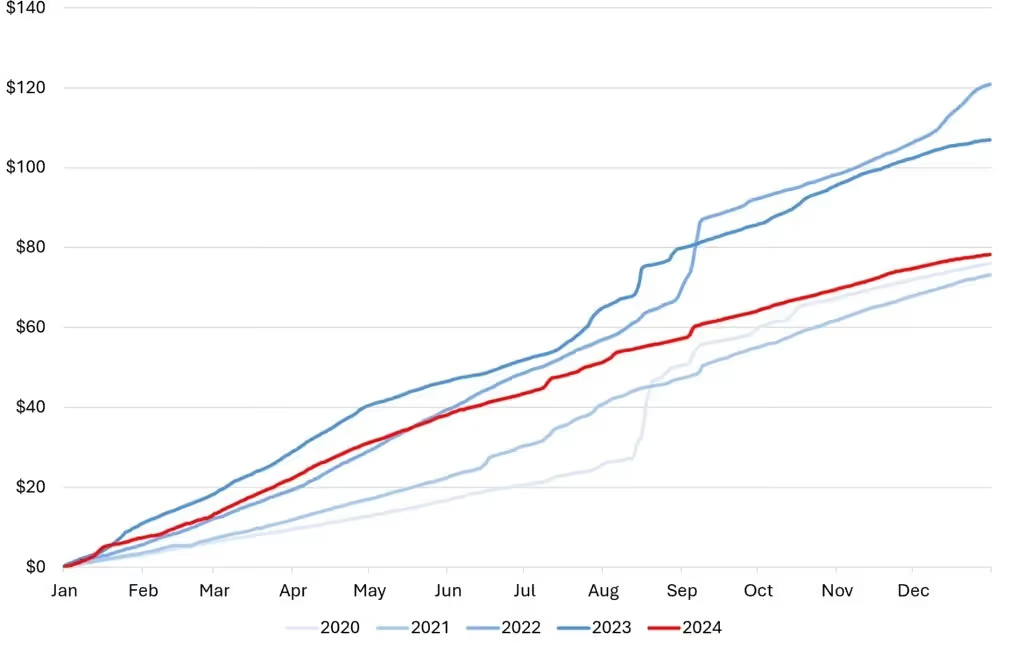

California power prices in 2024 saw very little action in terms of volatility, as shown in Figure 1, despite increasing negative prices and curtailment across more months of the year. This dynamic had multiple roots. While both average demand and peak demand rose slightly over 2023, both remained low relative to history.

Additionally, multiple factors have combined during recent years to dampen structural demand. California's population has stagnated during the past half-decade, while both behind-the-meter solar additions and energy efficiency measures have continued to grow. Expensive residential monthly retail rates, which have increased at an annual average compound growth rate of 8% since 2013, also play a significant role in mitigating structural load growth. Combined with frequent bureaucratic and permitting hurdles, high retail rates serve as a significant deterrent for large industrial loads such as data centers.

On the supply side, CAISO has recently added more than 10 GW of storage, with more coming, while also delaying retirements at Diablo Canyon and several once-through-cooling plants. Given minimal structural load growth, this means that California currently has ample capacity, which helps to mute high volatility during summer months or during scarcity conditions in general.

Gas prices also serve as an important driver of price volatility in California and in 2024 came in at about half the price that market forwards expected. Despite having additional supply and dampened demand, forward markets still exhibit inflated summer prices relative to actual prices.

Additionally, the increasingly flexible storage-filled supply stack is eroding the volatility premium in the CAISO real-time market. During peak days in 2024, storage contributed nearly 15% of capacity, up from 2% in 2022. Storage has also shown a habit of undercutting the most expensive imports and/or gas assets, as well as preventing Loss-of-Load based price spikes from setting system locational marginal pricing (LMP).

Ultimately, the California Public Utilities Commission (CPUC) will determine what LSEs must procure to meet peak load conditions. While other markets, such as ERCOT, live on the 'knife edge' of resource adequacy in order to drive revenue and incentivize new unit entry, California regulators have the ability to choose how far to err on the side of oversupply.

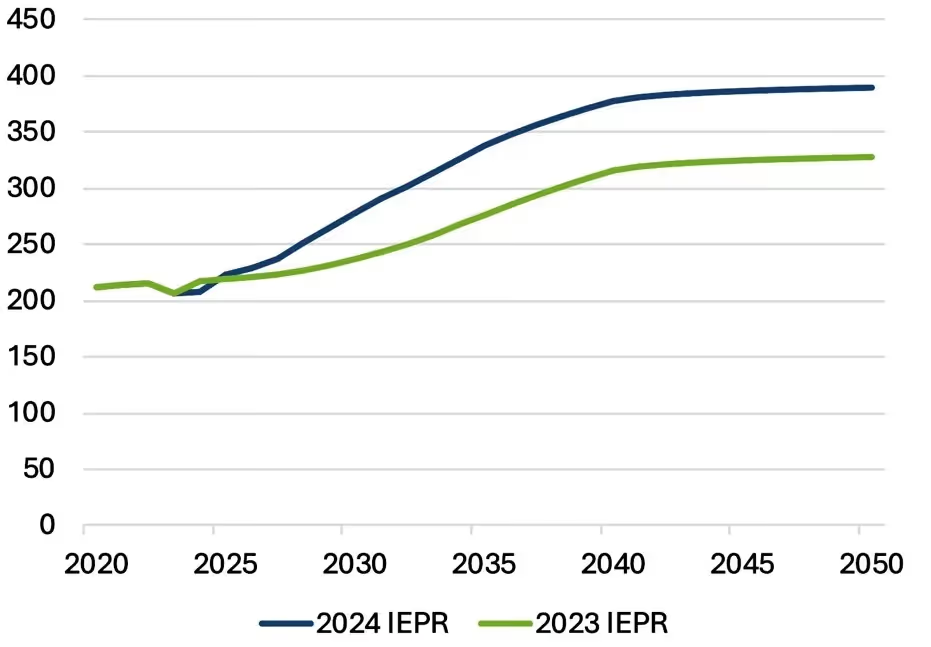

Going forward, it appears likely that state regulators will create a low price and revenue ceiling through bullish load forecasts and procurement mandates. For example, the most recent California Energy Commission (CEC) load forecast contains high projected load growth rates, as seen in Figure 2, and seems primed to ensure the state becomes oversupplied with capacity.

In this context, load will have strong incentives to manage peaks, since the value of avoiding peaks rises as the cost of capacity goes up. As the floor lifts, and negative pricing and curtailment persist and increase, a high-floor energy market for battery energy storage systems will emerge, though not for renewables or thermal generation. As the number of months with deep duck curves increases, batteries will be able to capitalize on the corresponding arbitrage opportunities.

As prices go lower, CAISO will also see more value flow to renewable energy credits (RECs), which means that standalone storage will increasingly benefit the RECs for renewable projects somewhere else. This also creates additional benefit for hybrid projects, which allow accounting for the value of preserved RECs in a way that a standalone storage unit cannot.

Achieving California's mandated clean energy goals will eventually require decarbonizing overnight generation. While the state's slice-of-day (SOD) resource adequacy (RA) methodology can ensure reliability, it still does not properly incentivize overnight decarbonization.

In its current state, SOD is disconnected from deliverability studies, which means that a resource is solely assessed for the ability to deliver load during peak conditions, even though a load-serving entity might need that resource to fill an overnight supply gap. As a result, the interconnection process reduces the availability of resources that could provide overnight RA.

Additionally, SOD undervalues long-duration storage through its inherent structure: a battery that covers more than 12 hours, for instance, inherently cannot be valued because the 24-hour slice, at best, has 12 hours of charging and 12 hours of discharging. Using the SOD framework, RA accounting is decoupled from allowed dispatch. For example, SOD allows two four-hour batteries to dispatch at the same time and still receive eight hours toward RA requirements, providing greater revenue opportunity than an eight-hour battery. The lack of vertical hourly slicing also means very long duration storage is needed to displace thermal RA to fill all overnight supply gaps.

Ultimately, California's current RA structure is not built in a way that incentivizes overnight decarbonization. While not the most urgent need, overnight decarbonization will become more pressing in the early to mid-2030s.

Access the full webinar recording, which offers guidance for where, what, and when to add new capacity resources in CAISO. The webinar also offers insights related to surging storage buildout, the north/south price divide in California, PPA and tolling costs, geospatial price dynamics, and updated energy demand forecasts.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

In California, a relative glut of energy capacity and lack of structural electricity demand growth have combined to make negative energy prices and curtailment increasingly prevalent during solar-generating hours throughout a growing number of months of the year. At the same time, overnight generation remains emissions-intensive and driven by gas prices while fundamental incompatibilities between the state's resource adequacy (RA) compliance structure and the California independent system operator's (CAISO) interconnection processes impede state clean energy goals. With potential for further price pressure due to federal policies and uncertain macroeconomic conditions, utilities, investors, and load-serving entities (LSEs) face serious challenges – and also have opportunities when it comes to storage.

In a webinar previewing Ascend's most recent CAISO power market forecast, Dr. Gary Dorris, CEO at Ascend Analytics, joined Dr. Brent Nelson, Managing Director of Markets and Strategy, to discuss the implications of federal tariffs, potential changes to the IRA, the costs of California meeting its clean energy goals, and the corresponding outlook for power, RA, and REC prices.

California power prices in 2024 saw very little action in terms of volatility, as shown in Figure 1, despite increasing negative prices and curtailment across more months of the year. This dynamic had multiple roots. While both average demand and peak demand rose slightly over 2023, both remained low relative to history.

Additionally, multiple factors have combined during recent years to dampen structural demand. California's population has stagnated during the past half-decade, while both behind-the-meter solar additions and energy efficiency measures have continued to grow. Expensive residential monthly retail rates, which have increased at an annual average compound growth rate of 8% since 2013, also play a significant role in mitigating structural load growth. Combined with frequent bureaucratic and permitting hurdles, high retail rates serve as a significant deterrent for large industrial loads such as data centers.

On the supply side, CAISO has recently added more than 10 GW of storage, with more coming, while also delaying retirements at Diablo Canyon and several once-through-cooling plants. Given minimal structural load growth, this means that California currently has ample capacity, which helps to mute high volatility during summer months or during scarcity conditions in general.

Gas prices also serve as an important driver of price volatility in California and in 2024 came in at about half the price that market forwards expected. Despite having additional supply and dampened demand, forward markets still exhibit inflated summer prices relative to actual prices.

Additionally, the increasingly flexible storage-filled supply stack is eroding the volatility premium in the CAISO real-time market. During peak days in 2024, storage contributed nearly 15% of capacity, up from 2% in 2022. Storage has also shown a habit of undercutting the most expensive imports and/or gas assets, as well as preventing Loss-of-Load based price spikes from setting system locational marginal pricing (LMP).

Ultimately, the California Public Utilities Commission (CPUC) will determine what LSEs must procure to meet peak load conditions. While other markets, such as ERCOT, live on the 'knife edge' of resource adequacy in order to drive revenue and incentivize new unit entry, California regulators have the ability to choose how far to err on the side of oversupply.

Going forward, it appears likely that state regulators will create a low price and revenue ceiling through bullish load forecasts and procurement mandates. For example, the most recent California Energy Commission (CEC) load forecast contains high projected load growth rates, as seen in Figure 2, and seems primed to ensure the state becomes oversupplied with capacity.

In this context, load will have strong incentives to manage peaks, since the value of avoiding peaks rises as the cost of capacity goes up. As the floor lifts, and negative pricing and curtailment persist and increase, a high-floor energy market for battery energy storage systems will emerge, though not for renewables or thermal generation. As the number of months with deep duck curves increases, batteries will be able to capitalize on the corresponding arbitrage opportunities.

As prices go lower, CAISO will also see more value flow to renewable energy credits (RECs), which means that standalone storage will increasingly benefit the RECs for renewable projects somewhere else. This also creates additional benefit for hybrid projects, which allow accounting for the value of preserved RECs in a way that a standalone storage unit cannot.

Achieving California's mandated clean energy goals will eventually require decarbonizing overnight generation. While the state's slice-of-day (SOD) resource adequacy (RA) methodology can ensure reliability, it still does not properly incentivize overnight decarbonization.

In its current state, SOD is disconnected from deliverability studies, which means that a resource is solely assessed for the ability to deliver load during peak conditions, even though a load-serving entity might need that resource to fill an overnight supply gap. As a result, the interconnection process reduces the availability of resources that could provide overnight RA.

Additionally, SOD undervalues long-duration storage through its inherent structure: a battery that covers more than 12 hours, for instance, inherently cannot be valued because the 24-hour slice, at best, has 12 hours of charging and 12 hours of discharging. Using the SOD framework, RA accounting is decoupled from allowed dispatch. For example, SOD allows two four-hour batteries to dispatch at the same time and still receive eight hours toward RA requirements, providing greater revenue opportunity than an eight-hour battery. The lack of vertical hourly slicing also means very long duration storage is needed to displace thermal RA to fill all overnight supply gaps.

Ultimately, California's current RA structure is not built in a way that incentivizes overnight decarbonization. While not the most urgent need, overnight decarbonization will become more pressing in the early to mid-2030s.

Access the full webinar recording, which offers guidance for where, what, and when to add new capacity resources in CAISO. The webinar also offers insights related to surging storage buildout, the north/south price divide in California, PPA and tolling costs, geospatial price dynamics, and updated energy demand forecasts.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $25 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)