Let's Connect

Contact us

Thank you for reaching out, we will be in touch shortly!

Oops! Something went wrong while submitting the form.

Power markets in the United States have entered an era that is straining the limits of conventional forecasting solutions. Today, the grid is increasingly shaped by the uncertainty in utility-scale renewable production, the complexity of battery storage, and the unprecedented levels of data center-driven load growth. Prices are fundamentally different than even a few years ago. Legacy forecasting approaches that worked in eras dominated by thermal generation, and even during the recent era of high renewable penetration, are no longer adequate for an era in which large, concentrated, and responsive loads will push demand against the limits of supply.

In a recent webinar, Dr. Brent Nelson, Senior Managing Director of Market Intelligence for Ascend Analytics, and Robert LaFaso, Director of Market Intelligence, discussed the evolution of US power market complexity, key market dynamics that must be represented in modern forecasting approaches, principal energy price forecasting methodologies, and how Ascend is enhancing its core forecasting framework to better serve developers, asset operators, and investors navigating the dynamics of a rapidly changing grid.

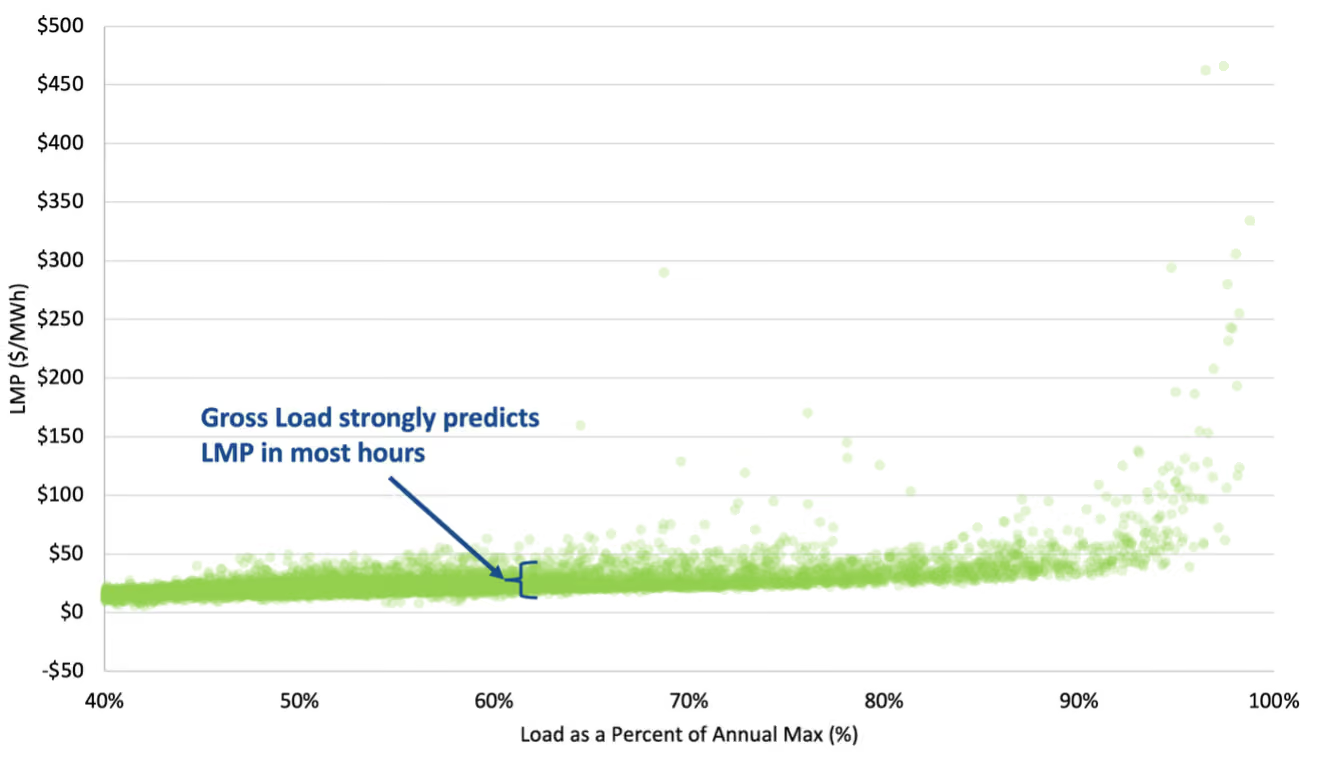

During the thermal-dominated era that existed prior to 2010, modeling power prices was relatively straightforward. Outside of hydro-dominated areas, thermal-heavy grids required only an understanding of the marginal offer prices at different load levels, with forecasts accounting for time-of-day and seasonal load, correlation between load and fuel, new entry economics and equilibrium in capacity expansion. Natural gas prices were the primary driver of uncertainty. As illustrated in Figure 1, gross load strongly predicted locational marginal pricing (LMP) in most hours in ERCOT in 2015. Accordingly, a simple supply stack model, calibrated to time-of-day and seasonal load patterns, was sufficient to accurately capture most market dynamics. Adding in physical-unit and power-flow constraints then made PCM modeling an accurate depiction of a thermal-only grid.

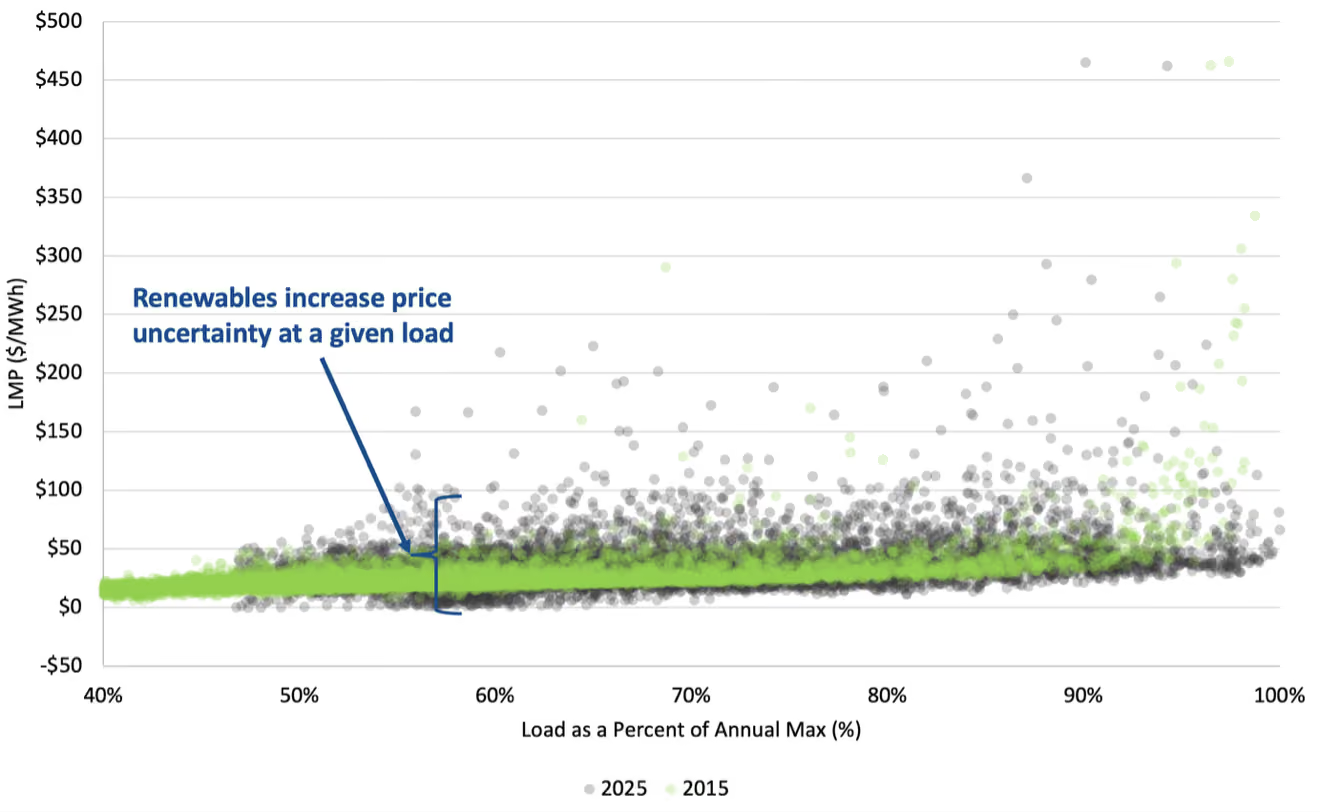

The buildout of utility-scale wind and solar during the 2010s and 2020s across several US power markets changed that. Weather became a driver for both demand and supply, introducing a second dimension of uncertainty into price formation. As shown in Figure 2, renewables increase price uncertainty at a given load level, making gross load a far less reliable predictor. To understand price, models had to capture not just the load, but also the level of renewables that would be produced as well as the impact that planning around uncertain renewable supply would have on the balance of the system.

With that new variability came new modeling requirements: price volatility, both positive and negative, had to be treated not as noise but as a key driver of investment decisions. This is especially true for flexible assets such as storage, in which revenues are indexed to volatility, and for non-dispatchable renewable resources for which production is dependent on real-time pricing. Reflecting real-time market dynamics, and the associated higher volatility and higher frequency of negative pricing events, became critical, not optional.

The emerging data center era compounds these challenges. Rapid demand growth, driven by hyperscalers and data center developers, is intersecting with a supply side constrained by interconnection queue backlogs, supply chain bottlenecks, and transmission limitations. Reserve margins are tightening, meaning markets will increasingly operate at or near the edge of the supply stack, where price formation is most nonlinear and hardest to model. Large flexible loads, including curtailable data centers and crypto mining operations, are becoming price-setters capable of both generating and suppressing volatility. Electrified heating is shifting the critical grid conditions from summer to winter and changing load shapes, as well as creating a system load profile that is even more correlated to weather than ever before. A forecasting framework that cannot reflect these dynamics will produce systematically distorted revenue and risk estimates.

Three broad categories of methodologies exist for energy price forecasting, and each carries a distinct set of trade-offs.

Econometric, statistical, and machine learning/AI models estimate prices based on correlations and patterns observed in historical data. Their core strength is that they reproduce price levels, volatility patterns, and correlations that have occurred historically. Their core weakness is tied to their strength: historical correlations become unreliable guides to future prices when the supply stack evolves significantly, when new price-setting resources and behaviors appear, or when regulatory structures change. In a period of rapid grid transformation, backward-looking models face inherent structural challenges.

Production cost models are the most common approach, as they simulate the hourly dispatch of every generator and transmission constraint on the grid, producing price estimates from least-cost optimization. In theory, this makes PCMs ideal for reflecting discrete, known changes, such as accounting for a transmission upgrade that eliminates a congestion constraint.

In practice, however, PCMs face several serious limitations despite their ubiquity. They depend on accurate unit-level representation of every generator’s operational constraints and bidding behavior, which requires detailed unit-level information to be accurate and can include decisions that appear uneconomic or are otherwise opaque to modelers. PCMs also over-optimize around known load and generation profiles, failing to reflect opportunity cost bidding behavior and as a result systematically underpredicting the volatility and curtailment that stem from real market operations in an uncertain environment. Additionally, they do not scale well to real-time market modeling, which means they undervalue flexible assets and overvalue renewable projects with unmodeled curtailment risk. Finally, PCM precision erodes quickly as the forecast horizon extends: a detailed nodal model of a grid 20 years from now is built on inputs that are largely unknowable today.

Ascend developed its Opportunity Cost Forecasting Framework (OCFF) to address the limitations of both statistical and production cost models. At its core, the OCFF treats price as a function of opportunity cost determined by rational market participants bidding competitively, with long-run market equilibrium as the binding constraint. The OCFF models weather as the fundamental driver of renewable generation, load, and price. It calibrates to observed market behavior and aligns to market forward prices in the near term, while enforcing equilibrium in the long run. The OCFF also incorporates non-economic driving forces, including clean energy policy trajectories and off-take demand preferences, that simple cost-optimization models cannot capture.

While the OCFF was built to accurately reflect the price formation dynamics of the renewables era, it was less well-equipped to reflect the inelastic pricing impacts that come with siting a large load or generation resource at a specific node, or to capture the price dynamics that emerge when flexible and curtailable load begins to operate at the edge of the supply stack.

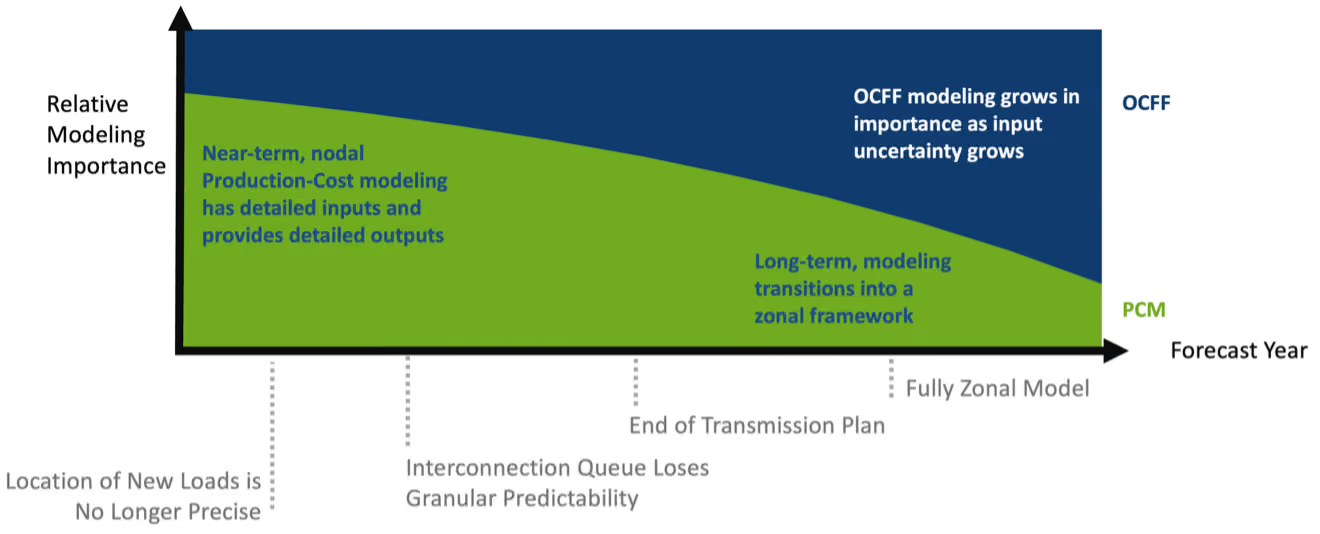

To address the complex realities of the data center era, Ascend advanced its forecasting approach by developing the Enhanced Opportunity Cost Forecasting Framework (EOCFF). The EOCFF integrates production cost modeling, with an emphasis on the front where nodal precision is most valuable. The framework progressively transitions to an opportunity cost forecasting approach in the long run as input uncertainty increases. As illustrated in Figure 3, PCM carries the highest relative modeling importance in the near term, when interconnection queues, transmission plans, and load locations are relatively well known. As that information degrades, the OCFF’s equilibrium-based framework becomes the dominant modeling lens.

This design preserves the key strengths of each modeling approach while mitigating the weaknesses. The near-term PCM layer enables direct modeling of discrete physical changes, such as a transmission constraint resolution, a storage build concentrated in a specific area, or the price impact of adding a gigawatt-scale data center at a particular node.

Critically, the EOCFF also retains the core analytical principles that made the OCFF ideal for capturing the market dynamics of the renewables era. Forecasts remain calibrated to observed historical market behavior in a way that competing forecasts are not, providing a credible basis for downstream projections. As shown in Figure 4, Ascend forecasts also emphasize long-run equilibrium: when location-specific price differentials emerge that are not supported by real differences in resource quality or development cost, the model expects capacity expansion and investment patterns to close those gaps over time. Additionally, the EOCFF also incorporates assumptions about anticipated state- and federal-level clean energy policy evolution in base case forecasts rather than relying on ‘status quo policies,’ which are certain to be incorrect.

.avif)

The EOCFF also incorporates multiple methodological enhancements in how it constructs inputs to the production cost model. Rather than drawing on a single historical calendar year for weather, it uses Ascend’s PowerSIMM™ platform to simulate typical meteorological year (TMY) conditions, properly correlating renewable generation profiles across months rather than inheriting the idiosyncrasies of any single year.

Additionally, the EOCFF explicitly models new load types, including curtailable large load, crypto operations with curtailment prices pinned to mining efficiency and crypto pricing, and electrified heating with weather correlations that reflect future grid composition rather than historical norms. Storage opportunity cost bidding is modeled directly within the PCM layer, reflecting the way battery assets actually bid across their full dispatch curve, including the shift to market-cap pricing when dispatch becomes scarce.

The EOCFF produces several near-term analytical capabilities for Ascend that were not previously available at scale. Project-specific price elasticity studies can now quantify the nodal impact of large new loads or generation, including the timing and magnitude of congestion uplift throughout the day. TMY modeling allows analyzing where forward markets appear to misprice emerging supply and demand divergence. Weather sensitivity analysis enables stress-testing of hedging positions under a range of renewable generation scenarios. Rapid scenario modeling when policy or market rules change, such as new ancillary service product design in ERCOT, becomes faster and less costly.

Ultimately, power market forecasts during the data center era must be capable of capturing near-term physical specificity while being anchored in long-run market reality. The Enhanced Opportunity Cost Forecasting Framework is designed to hold both simultaneously, grounded by Ascend’s direct participation across procurement, operations, and development in a way that other forecasting approaches cannot replicate.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $50 billion in project financing assessments. Contact us to learn more.

Power markets in the United States have entered an era that is straining the limits of conventional forecasting solutions. Today, the grid is increasingly shaped by the uncertainty in utility-scale renewable production, the complexity of battery storage, and the unprecedented levels of data center-driven load growth. Prices are fundamentally different than even a few years ago. Legacy forecasting approaches that worked in eras dominated by thermal generation, and even during the recent era of high renewable penetration, are no longer adequate for an era in which large, concentrated, and responsive loads will push demand against the limits of supply.

In a recent webinar, Dr. Brent Nelson, Senior Managing Director of Market Intelligence for Ascend Analytics, and Robert LaFaso, Director of Market Intelligence, discussed the evolution of US power market complexity, key market dynamics that must be represented in modern forecasting approaches, principal energy price forecasting methodologies, and how Ascend is enhancing its core forecasting framework to better serve developers, asset operators, and investors navigating the dynamics of a rapidly changing grid.

During the thermal-dominated era that existed prior to 2010, modeling power prices was relatively straightforward. Outside of hydro-dominated areas, thermal-heavy grids required only an understanding of the marginal offer prices at different load levels, with forecasts accounting for time-of-day and seasonal load, correlation between load and fuel, new entry economics and equilibrium in capacity expansion. Natural gas prices were the primary driver of uncertainty. As illustrated in Figure 1, gross load strongly predicted locational marginal pricing (LMP) in most hours in ERCOT in 2015. Accordingly, a simple supply stack model, calibrated to time-of-day and seasonal load patterns, was sufficient to accurately capture most market dynamics. Adding in physical-unit and power-flow constraints then made PCM modeling an accurate depiction of a thermal-only grid.

The buildout of utility-scale wind and solar during the 2010s and 2020s across several US power markets changed that. Weather became a driver for both demand and supply, introducing a second dimension of uncertainty into price formation. As shown in Figure 2, renewables increase price uncertainty at a given load level, making gross load a far less reliable predictor. To understand price, models had to capture not just the load, but also the level of renewables that would be produced as well as the impact that planning around uncertain renewable supply would have on the balance of the system.

With that new variability came new modeling requirements: price volatility, both positive and negative, had to be treated not as noise but as a key driver of investment decisions. This is especially true for flexible assets such as storage, in which revenues are indexed to volatility, and for non-dispatchable renewable resources for which production is dependent on real-time pricing. Reflecting real-time market dynamics, and the associated higher volatility and higher frequency of negative pricing events, became critical, not optional.

The emerging data center era compounds these challenges. Rapid demand growth, driven by hyperscalers and data center developers, is intersecting with a supply side constrained by interconnection queue backlogs, supply chain bottlenecks, and transmission limitations. Reserve margins are tightening, meaning markets will increasingly operate at or near the edge of the supply stack, where price formation is most nonlinear and hardest to model. Large flexible loads, including curtailable data centers and crypto mining operations, are becoming price-setters capable of both generating and suppressing volatility. Electrified heating is shifting the critical grid conditions from summer to winter and changing load shapes, as well as creating a system load profile that is even more correlated to weather than ever before. A forecasting framework that cannot reflect these dynamics will produce systematically distorted revenue and risk estimates.

Three broad categories of methodologies exist for energy price forecasting, and each carries a distinct set of trade-offs.

Econometric, statistical, and machine learning/AI models estimate prices based on correlations and patterns observed in historical data. Their core strength is that they reproduce price levels, volatility patterns, and correlations that have occurred historically. Their core weakness is tied to their strength: historical correlations become unreliable guides to future prices when the supply stack evolves significantly, when new price-setting resources and behaviors appear, or when regulatory structures change. In a period of rapid grid transformation, backward-looking models face inherent structural challenges.

Production cost models are the most common approach, as they simulate the hourly dispatch of every generator and transmission constraint on the grid, producing price estimates from least-cost optimization. In theory, this makes PCMs ideal for reflecting discrete, known changes, such as accounting for a transmission upgrade that eliminates a congestion constraint.

In practice, however, PCMs face several serious limitations despite their ubiquity. They depend on accurate unit-level representation of every generator’s operational constraints and bidding behavior, which requires detailed unit-level information to be accurate and can include decisions that appear uneconomic or are otherwise opaque to modelers. PCMs also over-optimize around known load and generation profiles, failing to reflect opportunity cost bidding behavior and as a result systematically underpredicting the volatility and curtailment that stem from real market operations in an uncertain environment. Additionally, they do not scale well to real-time market modeling, which means they undervalue flexible assets and overvalue renewable projects with unmodeled curtailment risk. Finally, PCM precision erodes quickly as the forecast horizon extends: a detailed nodal model of a grid 20 years from now is built on inputs that are largely unknowable today.

Ascend developed its Opportunity Cost Forecasting Framework (OCFF) to address the limitations of both statistical and production cost models. At its core, the OCFF treats price as a function of opportunity cost determined by rational market participants bidding competitively, with long-run market equilibrium as the binding constraint. The OCFF models weather as the fundamental driver of renewable generation, load, and price. It calibrates to observed market behavior and aligns to market forward prices in the near term, while enforcing equilibrium in the long run. The OCFF also incorporates non-economic driving forces, including clean energy policy trajectories and off-take demand preferences, that simple cost-optimization models cannot capture.

While the OCFF was built to accurately reflect the price formation dynamics of the renewables era, it was less well-equipped to reflect the inelastic pricing impacts that come with siting a large load or generation resource at a specific node, or to capture the price dynamics that emerge when flexible and curtailable load begins to operate at the edge of the supply stack.

To address the complex realities of the data center era, Ascend advanced its forecasting approach by developing the Enhanced Opportunity Cost Forecasting Framework (EOCFF). The EOCFF integrates production cost modeling, with an emphasis on the front where nodal precision is most valuable. The framework progressively transitions to an opportunity cost forecasting approach in the long run as input uncertainty increases. As illustrated in Figure 3, PCM carries the highest relative modeling importance in the near term, when interconnection queues, transmission plans, and load locations are relatively well known. As that information degrades, the OCFF’s equilibrium-based framework becomes the dominant modeling lens.

This design preserves the key strengths of each modeling approach while mitigating the weaknesses. The near-term PCM layer enables direct modeling of discrete physical changes, such as a transmission constraint resolution, a storage build concentrated in a specific area, or the price impact of adding a gigawatt-scale data center at a particular node.

Critically, the EOCFF also retains the core analytical principles that made the OCFF ideal for capturing the market dynamics of the renewables era. Forecasts remain calibrated to observed historical market behavior in a way that competing forecasts are not, providing a credible basis for downstream projections. As shown in Figure 4, Ascend forecasts also emphasize long-run equilibrium: when location-specific price differentials emerge that are not supported by real differences in resource quality or development cost, the model expects capacity expansion and investment patterns to close those gaps over time. Additionally, the EOCFF also incorporates assumptions about anticipated state- and federal-level clean energy policy evolution in base case forecasts rather than relying on ‘status quo policies,’ which are certain to be incorrect.

The EOCFF also incorporates multiple methodological enhancements in how it constructs inputs to the production cost model. Rather than drawing on a single historical calendar year for weather, it uses Ascend’s PowerSIMM™ platform to simulate typical meteorological year (TMY) conditions, properly correlating renewable generation profiles across months rather than inheriting the idiosyncrasies of any single year.

Additionally, the EOCFF explicitly models new load types, including curtailable large load, crypto operations with curtailment prices pinned to mining efficiency and crypto pricing, and electrified heating with weather correlations that reflect future grid composition rather than historical norms. Storage opportunity cost bidding is modeled directly within the PCM layer, reflecting the way battery assets actually bid across their full dispatch curve, including the shift to market-cap pricing when dispatch becomes scarce.

The EOCFF produces several near-term analytical capabilities for Ascend that were not previously available at scale. Project-specific price elasticity studies can now quantify the nodal impact of large new loads or generation, including the timing and magnitude of congestion uplift throughout the day. TMY modeling allows analyzing where forward markets appear to misprice emerging supply and demand divergence. Weather sensitivity analysis enables stress-testing of hedging positions under a range of renewable generation scenarios. Rapid scenario modeling when policy or market rules change, such as new ancillary service product design in ERCOT, becomes faster and less costly.

Ultimately, power market forecasts during the data center era must be capable of capturing near-term physical specificity while being anchored in long-run market reality. The Enhanced Opportunity Cost Forecasting Framework is designed to hold both simultaneously, grounded by Ascend’s direct participation across procurement, operations, and development in a way that other forecasting approaches cannot replicate.

AscendMI™ (Ascend Market Intelligence) delivers proprietary power market forecasts that have been trusted in hundreds of projects and resource planning activities, supporting over $50 billion in project financing assessments. Contact us to learn more.

Ascend Analytics is the leading provider of market intelligence and analytics solutions for the power industry.

The company’s offerings enable decision makers in power development and supply procurement to maximize the value of planning, operating, and managing risk for renewable, storage, and other assets. From real-time to 30-year horizons, their forecasts and insights are at the foundation of over $50 billion in project financing assessments.

Ascend provides energy market stakeholders with the clarity and confidence to successfully navigate the rapidly shifting energy landscape.

-3.avif)

.avif)